CHAPTER 3

“Growing big is the best way for Chinese banks to make more money . . . This model of growth, however, neither assures the long-term sustainable development of the banking sector nor satisfies the need of a balanced economic and social structure. Things are very complicated; so will be the solutions.”

Xiao Gang, Chairman, Bank of China

August 25, 20101

When the Asian Financial Crisis threatened the stability of China’s financial institutions in 1997, Zhu Rongji sponsored a group of reformers surrounding Zhou Xiaochuan, then chairman of the CCB, to come up with a plan. The immediate threat to confidence in the banks was addressed by the MOF injecting new capital into the banks in 1998. As a second step, Zhou’s group proposed a “good bank/bad bank” approach to strengthen the balance sheets of the Big 4 banks. Modeled after the Resolution Trust Corporation (RTC) in the US, asset-management companies (AMCs) would be established for each of the banks. The AMCs would become the “bad” banks holding the non-performing loans (NPLs) of the resulting “good” banks. These bad banks would be financed by the government and be responsible for recovering whatever value possible from NPLs. The State Council approved the proposal and in 1999 the AMCs were set up. (See appendix for organizational charts of China’s resulting financial system).

In 2000, huge problem-loan portfolios were transferred to the AMCs, freeing the banks of massive burdens and enabling them to attract such blue-chip strategic investors as Bank of America and Goldman Sachs. These international investors were brought in less for their money than for the expertise that the government hoped could be transferred to its banks. But, in a rising crescendo of criticism, conservative and nationalist critics claimed a “sell-out” to foreign interests. Even so, in 2005, CCB enjoyed a wildly successful IPO in Hong Kong, raising billions of dollars in new capital. With this IPO, Zhu and Zhou’s efforts achieved a very significant success where, several years before, few had believed such a thing possible for a Chinese bank. Unfortunately, the very success of bank reform fed the fire of conservative criticism which was now amplified by the PBOC’s institutional rivals, who wanted to cut Zhou and the central bank down to size. Among these rivals were the NDRC, the CSRC, the CBRC and, most particularly, the MOF. The impact of this concerted criticism affected the financial restructuring process, beginning with ICBC and continuing through to ABC. It also had the effect of ending Zhou’s integrated approach to capital-market and regulatory reform.

The practical consequence for the bank reform was the creation of two different approaches to balance-sheet restructuring. Of course, the original plan for all four banks was superficially retained, even after the MOF assumed the leading position in the reform of ICBC and ABC in 2005. No better ideas had been generated as a result of all the criticism, so each of the four banks raised capital through IPOs. But the paths to restructuring differed, as did the manner in which NPL portfolios were disposed of. The major financial liabilities remaining on bank balance sheets arising from the two different approaches are shown in Table 3.1. Information in this table is derived from the banks’ financial statements under the footnote “Debt securities classified as receivables.” The table illustrates the continuing and material exposure of China’s major banks to securities created as a result of their restructuring a decade ago. The simple message of these “receivables” is that the old bad debt has not gone away; it is still on bank balance sheets but has been reclassified, in part, as “receivables” that may never be received.

TABLE 3.1 Restructuring “receivables” on bank balance sheets

Source: Bank audited financial statements, December 31, 2009

What is the nature and value of these assets? The various PBOC securities, as well as the 1998 MOF bond, are clear obligations of the sovereign. But what value should be assigned to the AMC bonds or, for that matter, the MOF “receivable?” Obviously a receivable due from the MOF is similar to a government bond . . . on the surface. The bond, however, has been approved by the State Council and the NPC as part of the national budget. Such government bonds will be repaid either by state tax revenues or further bond issues. Who has approved the issuance of that IOU? How will it be repaid? These are important questions, given each bank’s massive credit exposure to these securities. For example, the total of these restructuring assets is nearly twice ICBC’s total capital, with the AMC bonds alone representing 53 percent. The sections below seek to understand how these obligations arose and what they practically represent in order to determine their value and structural implications for the banking system as a whole.

THE PEOPLE’S BANK OF CHINA RESTRUCTURING MODEL

From the viewpoint of strengthening the banks, the original PBOC model was the most effective, providing additional capital to the banks through a combination of more new money and better valuations for problem loans. In the first step in 1998, bank capital was topped up to minimum levels required by international standards. This was followed by the transfer of US$170 billion of bank NPL portfolios to the AMCs at 100 cents on the dollar. These “bad banks” paid cash, using a combination of PBOC loans and AMC bonds, for the bad-loan portfolios. However, these injections of cash came just at a time when inflation was looming. Consequently, the PBOC sterilized the incremental cash on bank balance sheets by forced purchases of PBOC bills, which could not be used in any further financing transactions. This is the source of the PBOC securities listed in Table 3.1. In 2003, additional bad loans remaining on the balance sheets of CCB and BOC were completely written off up to the amount of the total capital of each bank, a total of RMB92 billion (US$12 billion). Bank capital was then replenished from the country’s foreign-exchange reserves and with investments from foreign strategic investors. CCB and BOC were restructured in this way and completed successful IPOs in 2005 and 2006.

The partial recapitalization of the Big 4 banks, 1998

On the collapse of GITIC and amid rumors of bank insolvency, in 1998 Zhu Rongji ordered a rapid recapitalization of the Big 4 banks to at least minimum international standards, which were the only standards available to China. A mountain of bad loans had been created in the late 1980s and early 1990s and ignored for 10 years. This was the typical approach of the bureaucracy toward intractable problems. By 1998, however, it had become obvious to the government that such methods increased systemic risk. At that time, China’s banks had never been audited to strict professional standards or, for that matter, to any professional standard. As with GITIC, no one could say with confidence how big the problem might be. Given Wang Qishan’s experience in having to answer an angry Premier’s questions about GITIC’s black hole, one can imagine the pressure people at the MOF must have felt as they sought to come up with a figure that would satisfy Premier Zhu.

There was, of course, no time for a real audit, but someone was clever enough to come up with a number purportedly sufficient to raise bank capital adequacy to eight percent of total assets, in line with the Basel Agreement on international banking standards. This figure turned out to be RMB270 billion (US$35 billion). For China, in 1998, this was a huge sum of money, equivalent to nearly 100 percent of total government bond issuance for the year, 25 percent of foreign reserves and about four percent of GDP. To do this, the MOF nationalized savings deposits largely belonging to the Chinese people (see Table 3.2).

TABLE 3.2 Composition of Big 4 bank deposits, 1978–2005

Source: China Financial Statistics 1949–2005

In the first step, the PBOC reduced by fiat the deposit-reserve ratio imposed on the banks, from 13 percent to eight percent. This move freed up RMB270 billion in deposit reserves which were then used on behalf of each bank to acquire a Special Purpose Treasury Bond of the same value issued by the MOF (see Figure 3.1).2 In the second step, the MOF took the bond proceeds and lent them to the banks as capital (see Figure 3.2). This washing of RMB270 billion through the MOF in effect made the banks’ depositors—both consumer and corporate—de facto shareholders, but without their knowledge or attribution of rights.

FIGURE 3.1 Step 1 in recapitalization of the Big 4 Banks, 1998

FIGURE 3.2 Step 2 in recapitalization of the Big 4 Banks, 1998

As part of the CCB and BOC restructurings in 2003, these nominally MOF funds totaling RMB93 billion for the two banks were transferred entirely to bad-debt reserves and then used to write off similar amounts of bad loans.3 This left the Ministry of Finance responsible for repayment. For the banks this was a good deal, as the MOF was now obligated not just to “repay” what was originally the banks’ money anyway, but to use its own funds to do so. It is no wonder, therefore, that the bond maturities were extended to 2028, just as it is no wonder that the MOF did not support the PBOC approach to bank restructuring. How could it when, without the approval of State Council and National People’s Congress, it had no access to such massive amounts of money?

Bad banks and good banks, 1999

Having shored up the banks by such accounting legerdemain, work began on preparing them for an eventual IPO. Zhou Xiaochuan proposed the international “good bank/bad bank” strategy that had been used successfully in the Scandinavian countries and the US. This involved the establishment of a “bad bank” to hold the problem assets spun off by what then becomes a “good bank.” Zhou proposed the creation of one “bad” bank, called an “asset-management company,” for each of the four state-owned banks. It was a critical part of the plan that, after the NPL portfolios had been worked out, the AMCs would be closed and their net losses crystallized and written off, a process that was expected to take 10 years. In 1999, the State Council approved the plan and the four AMCs were established.

The MOF capitalized each AMC by purchasing Special AMC Bonds totaling RMB40 billion or roughly US$1 billion each (see Figure 3.3). In line with the plan to close the companies, these bonds had a maturity of 10 years. But RMB40 billion was hardly enough to acquire bank NPL portfolios. More funds were needed and where else to get them but from the banks themselves? The AMCs, therefore, issued 10-year bonds to their respective banks in the amount of RMB858 billion (US$105 billion).

FIGURE 3.3 AMC capitalization by the MOF and each bank, 1999

These bonds represent the major flaw in the PBOC plan. The significance of the bonds is that the banks remain heavily exposed to their old problem loans even after they had been nominally “removed” from their balance sheets. The banks had simply exchanged one set of demonstrably non-performing assets for another of highly questionable value. The scale of this exposure was also huge in comparison to bank capital (see Table 3.1). Given the size of the bank recapitalization problem in comparison to China’s financial capacity at the time, the government had little choice but to rely on the banks. But this approach was not in line with the international model and did not solve the problem.

In the Scandinavian and US experience, the national treasury had not only capitalized the bad banks, but it had also provided financing to them so that the resulting “good” banks had no remaining exposure to their old bad loans. They had become the problem of the national treasury and ultimately their cost would be paid for from taxes. In China, as long as the government’s reliance on the banks to fund the AMCs remained “inside the system,” it may not have mattered. A supportive bank regulator could rule that AMC bonds were those of semi-sovereign entities and the question as to their creditworthiness could be avoided. But once these banks became listed on international markets and were subject to scrutiny by other regulators and investors, international auditors would inevitably question the valuation of these bonds. The AMCs were thinly capitalized at about US$5 billion. The bonds they had issued totaled US$105 billion and the assets they funded had, by definition, little value. What if the AMCs could not achieve sufficient recoveries on the NPL portfolios to repay the bonds due in 2009?

NPL portfolio acquisition by the AMCs, 2000

The first acquisition of bad-loan portfolios by the new AMCs began and was completed in 2000. A total of RMB1.4 trillion (US$170 billion) in NPLs was transferred at full face value, dollar-for-dollar, from the banks to the AMCs. This was funded by the bond issues and a further RMB634 billion (US$75 billion) in credit extended by the PBOC (see Figure 3.4). The obvious question that arises is: if these loans were really worth full face value, why were they spun off in the first place? There are a number of possible reasons for this. One is that any write-down by the banks in 2000 would have wiped out all capital injected by the MOF in 1998 and there was, as yet, no consensus on where new capital would come from. Given the amounts involved, there were, after all, limited choices. This is surely part of the answer. Another part is that this transfer was equivalent to an indirect injection of capital since the replacement of bad loans with cash would free up loan-loss reserves (if any). Going forward, it would improve bank profitability and capital by reducing the need for loan-loss provisioning.

FIGURE 3.4 AMCs’ additional funding from the PBOC, 2000

The rest of the answer is that the government was unable to reach consensus on the valuation of these “bad” loans. After all, these loans had all been made to SOEs which were, by definition, state-owned. Anything less than full value would suggest that the state was unable to meet its own obligations, a position anathema to Party ideologues. But that was just the point: the state was unable to meet these obligations. So instead of bankrupting all SOE borrowers—that is, basically the entire industrial sector—the Party chose to keep the potential losses concentrated on bank balance sheets. Instead of resolutely addressing the problem by writing the loans down, it decided to push the matter off into the future and on to some other politician’s agenda. Of course, in 2009, the Party decided to do the same thing, so the AMC obligations were pushed off a further 10 years. This is how things work “inside the system.”

PBOC recapitalizes CCB and BOC, 2003

Official data indicate that after this first tranche of bad loans was removed in 2000, the four banks still had RMB2.2 trillion (US$260 billion) more on their books, and this was before a stricter international loan-classification system was implemented in 2002. The government took a hard look at bank capital levels, but its own resources remained very limited. Its conservative approach extended to an aversion to increasing the national debt. If the banks were truly to be strengthened, they needed more capital and a lot of it. Zhou’s plan had concluded that this could only be provided by international investors. But the problem was how to make bank balance sheets and business prospects strong enough to attract them.

The question boiled down, in part, to how much each bank could afford to actually write off. The PBOC found that of the four banks, only BOC and CCB had sufficient retained earnings and registered capital to make full write-offs of their remaining bad loans while leaving a small but positive capital base. Neither ICBC nor ABC was capable of achieving this in 2003, and both would have ended up with negative capital; that is, they would have been factually bankrupt. But if BOC and CCB’s RMB93 billion in capital was to be written down, where could the money be found to build it back up? After much argument, Zhou Xiaochuan proposed the only possible solution: use the foreign-exchange reserves. As the famously outspoken Xie Ping, then director of the PBOC’s powerful Financial Stability Bureau, put it: “This time, we did not just play a game with accounting [a direct jab at the MOF’s methods in 1998]. Real money went into the banks.”

Zhou’s plan was approved by the State Council and on the last day of 2003, each bank transferred the value of its capital and retained earnings4 into bad-debt reserves and wrote it all off. In other words, the MOF’s total capital contribution to the two banks—RMB93 billion—was written off, but the MOF remained obligated to repay its 1998 Special Bonds. This fact alone highlights the seriousness of the Party’s intention to restructure the banks and is emblematic of the PBOC’s ascendancy over the MOF at the time. The two banks each received US$22.5 billion from the country’s foreign-exchange reserves by means of the PBOC entity Central SAFE Investment (discussed in greater detail in Chapter 5). Shortly thereafter, in May and June 2004, the banks disposed of an additional total of RMB442 billion in problem assets via a PBOC-sponsored auction process prearranged to create loan recoveries and further additions to their capital accounts. As a result of all these actions, BOC and CCB were in a position to attract foreign strategic investors and ultimately to proceed with IPOs in 2005 (see Table 3.3). But the side effect was to exacerbate the political struggle over bank reform: the PBOC now owned 100 percent of both CCB and BOC.5

TABLE 3.3 PBOC/Huijin ownership rights in major Chinese banking institutions

Source: Huijin; bank annual financial reports and ABC offering prospectus

Note: Dates of IPOs include those for both Hong Kong (H) and Shanghai (A) IPOs. “Other State” investors include strategic Chinese investors such as SOEs. For BOC, all NSSF (4.46 percent) and foreign strategic investor shares (13.91 percent) were converted into H-shares at the time of the IPO and are included in the Public number. Jianyin is a 100 percent subsidiary of Huijin.

“Commercial” NPL disposals, 2004–2005

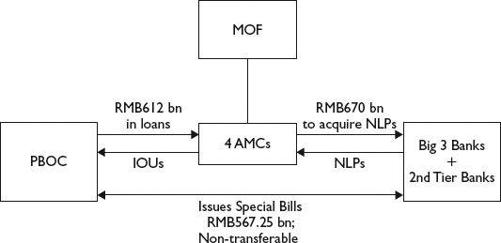

In line with the PBOC blueprint, a second round of NPL acquisition by the AMCs, totaling RMB1.6 trillion (US$198 billion), followed in 2004 and 2005. In addition to a second batch of bad loans of RMB705 billion from ICBC, portfolios also included RMB603 billion from a number of smaller, second-tier banks. For these transactions, the PBOC provided the necessary funding, with estimated credits of up to RMB700 billion (see Figure 3.5 and Table 3.4) But this time, the PBOC had already taken a down payment copied straight out of the MOF’s 1998 playbook: in 2004, it had issued compulsory Special Bills totaling RMB567.25 billion (US$70 billion) to BOC, CCB and ICBC. These bills could not be sold into the market and were designed to mature in June 2009 as a part of the unwinding of the entire AMC arrangement.

FIGURE 3.5 PBOC funding for ICBC NPL disposal and commercial loan auctions

TABLE 3.4 AMC funding obligations, 2000–2005

Source: Caijing ![]() , July 25, 2007: 65; PBOC, Financial Stability Reports, various

, July 25, 2007: 65; PBOC, Financial Stability Reports, various

In issuing the bills, the PBOC accomplished two things. First, it removed the liquidity it had created by financing the NPL spin-offs; and, second, it in effect extracted from the banks a partial pre-payment of about 33 percent of its maximum lending to the AMCs. In essence, this Special Bill was a predecessor to the mammoth Special Bond issued by the MOF in 2007 to capitalize CIC and it was issued largely for the same reason: to control excess liquidity.

The ICBC and ABC recapitalizations, 2005 and 2007

In contrast to its involvement with BOC and CCB—where its 1998 cash capital contribution had been fully written off but its liability stayed in place—in the case of ICBC, the MOF’s original RMB85 billion remained, so that the PBOC/Huijin’s contribution was reduced to US$15 billion, equivalent to 50 percent of the bank’s equity. Two years later, in 2007, ABC’s recapitalization followed the ICBC model, but things appeared to have changed completely. As before, Huijin contributed new capital from exchange reserves to the tune of US$19 billion to ABC, and the MOF’s 1998 contribution remained in place. But, as will be discussed in Chapter 5, by this stage, Huijin belonged to the MOF, not to the PBOC.

While, on the surface, things appeared to be consistent with the PBOC approach, in fact the entire structure of bank ownership had reverted to the status quo of the pre-reform era, with the MOF in control. Not only ownership was affected; the entire restructuring of problem-loan portfolios was different, as was the government’s attitude towards the banks. With the apparently successful rehabilitation of BOC and CCB, the Party was, in effect, telling the banks that they now had to share the burden. From this came the lending binge of 2009; the banks had once again reverted to their role as a simple utility.

THE MINISTRY OF FINANCE RESTRUCTURING MODEL

The MOF, of course, was unhappy with its subordination to the PBOC following the restructuring of the banks up to 2004. Historically, this was almost the first time that their roles had been reversed. However, as described above, from 2005, the MOF was able to exert its influence over the banking system once again, a process that culminated with the establishment of China Investment Corporation (CIC) in late 2007 (see Chapter 5). The principal difference between the MOF’s approach and that of the PBOC was that it assumed direct responsibility for the funding and repayment of problem-loan disposals. This, in fact, appeared to nudge things much closer to the international model. The PBOC had succeeded in pushing the MOF away from control of the reform process, but its complex funding arrangements for NPL disposals, although practical given the government’s limitations, had never been a good solution. From the start, the AMCs had been thinly capitalized and faced the hopeless task of recovering 100 cents on each dollar of problem loans. How could they really be expected to repay the PBOC, much less the banks?

Looked at closely, however, the MOF’s solution also had its weak points. In 2005, when it assumed control of ICBC’s ongoing restructuring, the MOF partially replaced AMC bonds with its own paper. That year, a bad-loan portfolio of RMB246 billion was transferred to a “co-managed account” (see Appendix) and ICBC—unlike in the BOC and CCB cases—did not receive cash. Instead, it received what can be called “MOF IOUs” as well as the traditional AMC bonds (see Figure 3.6).

FIGURE 3.6 NPL restructuring for ICBC and ABC, 2005 and 2007

The case of ABC, too, is a pure example of this same MOF approach. Some 80 percent—RMB665.1 billion (US$97.5 billion)—of its NPLs was replaced on a full book-value basis by an unfunded MOF IOU.6 As with ICBC, the NPL hole on its balance sheet was replaced with a piece of paper conveying the MOF’s vague promise to pay “in following years”, according to the related footnote in its annual financial statement. For ICBC’s receivable, this period is five years; for ABC, it is 15.

On the plus side, this receivable had the advantage of being a direct MOF obligation and relieved the banks of any problem-loan liabilities. Moreover, since ICBC and ABC did not receive cash, excess liquidity did not become a problem. These were the advantages to this approach, but there were also disadvantages.

The details of the underlying transactions for the two banks show that this approach is another instance of pushing problems off into the distant future. Actual title to the problem loans was transferred to the “co-managed” account with the MOF. The banks were authorized by the MOF to provide NPL disposal services. But what exactly is this MOF IOU? It may represent the obligation of the Ministry itself, but, notwithstanding the fact that the MOF represents the sovereign in debt issuance, does its IOU represent a direct obligation of the Chinese government? It would have been a far cleaner break had the MOF simply issued a bond, funding the AMCs directly from the proceeds and using cash to acquire the NPLs. There would have been no need for the PBOC to extend credit at all. That was how the United States Department of Treasury funded the Resolution Trust Corporation during the savings-and-loan crisis.

The approach would have cleaned up the banks completely and the liability would have been indisputably with that department with taxing authority. To have done so, however, the MOF would have had to include the required debt issues in its national budget and received the approval of the National People’s Congress. An unfunded IOU, in contrast, is entirely “off the balance sheet” (biaowai ![]() ) and would only have been approved as a part of the overall bank-restructuring plan approved by the State Council. Indeed, it is possible that the use of IOUs did not even require State Council approval, as these instruments are purely unfunded contingent liabilities. Contingent liabilities are not included, at least publicly, in the national budget, or anywhere else for that matter.

) and would only have been approved as a part of the overall bank-restructuring plan approved by the State Council. Indeed, it is possible that the use of IOUs did not even require State Council approval, as these instruments are purely unfunded contingent liabilities. Contingent liabilities are not included, at least publicly, in the national budget, or anywhere else for that matter.

Then, of course, repayment of its IOUs does not rely on the national budget: it turns out that the banks themselves would be the sole source of cash for funding these payments. Footnotes in the ICBC’s audited financial statements and the ABC IPO prospectus indicate that IOU repayment would come from recoveries on problem loans, bank dividends, bank tax receipts and the sale of bank shares. In other words, the banks would be indirectly paying themselves back over “the following years” since it is entirely unlikely that the MOF would sell (or be allowed to sell) any of its holdings in the banks. Since such funding sources represent future payment streams, it appears that the co-managed funds simply hold the two banks’ NPLs on a consignment basis; they are a convenient parking lot. Given the experience of the AMCs in problem-loan recovery (see below), there is little likelihood that either bank could do much better. The establishment of the Beijing Financial Asset Exchange in early 2010 is highly suggestive of how the banks will dispose of the bad loans in those co-managed accounts. The shareholders of this new exchange, which is located in the heart of the Beijing financial district, include Cinda Investment, Everbright Bank and the Beijing Equity Exchange. Its stated mission is to dispose of non-performing loans by means of an auction process. Perhaps this exchange will lead the disposal process for the two banks. But what entities have the financial capacity to acquire large NPL portfolios and who will take the inevitable write-down? In the end, the MOF will have to issue a bond to cover the net remainder of both of its IOUs or else extend their maturities. Other than avoiding a discussion with the National People’s Congress, it is entirely unclear exactly what is gained by taking this approach.

All of this simply serves to focus the light on the one practical source of repayment: bank dividends. This takes the story right back to bank dividend policies noted in Chapter 2. As will be discussed in regard to CIC in the next chapter, the Ministry of Finance’s arrangement has significant disadvantages, even compared with the far-from-perfect PBOC model.

“Bad bank” performance and its implications

By the end of 2006, BOC, CCB and ICBC had all completed their IPOs and the AMCs shortly thereafter had finished their workouts of their NPL portfolios. Given the weight of the AMCs on each bank’s balance sheet, the question must be asked: how well did these bad banks perform their task? As of 2005, even after the second round of spin-offs, the Big 4 and the second-tier banks still had more than RMB1.3 trillion (US$158 billion) of bad loans on their books. The total of the first two rounds at full face value, together with those remaining as of FY2005, amounted to RMB4.3 trillion. The AMCs were funded by obligations totaling RMB2.7 trillion (US$330 billion), as shown in Table 3.4. These liabilities were all designed, even if poorly, to be repaid by cash generated from loan recoveries. Obviously, as the first portfolio of RMB1.4 billion and parts of the second group of portfolios were acquired at face value, repayment was an impossibility from the start. From their first day of operation, the AMCs were technically bankrupt, and practically little different from the “co-managed accounts” now used by the MOF.

At the end of 2006, when more than 80 percent of the first batch of problem loans had been worked out, recovery rates were reportedly around 20 percent—hardly enough to pay back the interest on the various bonds and loans. While recoveries from the second, largely “commercial,” batch suggest a higher rate, industry sources suggest that actual recoveries lagged the prices paid. As 2009 approached and passed, the Party was faced with the problem of how to write off losses that may have amounted to 80 percent of AMC asset portfolios, or about RMB1.5 trillion. But losses could easily have been even greater than that and even long-term industry participants are unsure just what this figure might be.

With some 12,000 staff, the AMCs had their own operating expenses, including interest expense on their borrowed funds. An estimate of operating losses exclusive of any loan write-offs is shown in Table 3.5. The table uses loan recoveries as a source of operating revenue, an incorrect accounting treatment. But reports indicate that, indeed, the AMCs did use recoveries to make interest payments on their obligations to the PBOC and the banks. Had they not, the banks would have been forced to make provisions against the AMC bonds on their books or the MOF would have had to make the interest payments. There is no indication that this happened. For the sake of arriving at an estimated recovery, figures used in Table 3.5 are assumed to be 20 percent for loans acquired at full face value and 35 percent for loans acquired through an auction, where the AMCs are assumed to have paid 30 percent. Operating expenses are based on 10 percent of NPL disposals, as stipulated by the MOF.

TABLE 3.5 AMC estimated income statement, 1998–2008

Source: Caijing ![]() , May 12, 2008; 77–80 and November 24, 2008; 60–62

, May 12, 2008; 77–80 and November 24, 2008; 60–62

Note: US dollar values: RMB 8.28/US$1.00

|

RMB billion |

||

|

1st Round: 1999–2003 |

FY2003 |

US$ billion |

|

Total acquisitions |

1,393.9 |

168.4 |

|

Disposals to 2008 |

1,156.6 |

139.7 |

|

Recovered, assume 20% |

231.3 |

27.9 |

|

less: |

||

|

Interest expense on PBOC loans/AMC bonds, 1999–2003 |

190.0 |

22.9 |

|

Operating expense, assume half of MOF target 10% of disposals |

57.9 |

7.0 |

|

Total operating expense |

247.9 |

29.9 |

|

Pre-tax gain/loss |

−16.6 |

−2.0 |

|

Registered capital |

40.0 |

4.8 |

|

Retained earnings |

−16.6 |

−2.0 |

|

Accumulated write-offs—Round 1 |

−925.3 |

−111.8 |

|

2nd Round: 2004–2005 |

FY2005 |

US$ billion |

|

Total acquistions—face value |

1,639.7 |

198.1 |

|

Total acquistions—auction value, assume 30% |

491.1 |

59.3 |

|

NPLs remaining from Round 1 |

237.9 |

28.6 |

|

Assumed disposals—100% |

1,639.7 |

198.1 |

|

Recovered on auction NPLs, assume 35% |

171.9 |

20.8 |

|

Recovered, Round 1 remainders, assume 10% |

23.7 |

2.9 |

|

Total recoveries |

195.6 |

23.6 |

|

less: |

||

|

Interest expense on PBOC loans/AMC bonds, 2004–2005 |

95.0 |

11.5 |

|

Operating expense, assume half of MOF target 10% of disposals |

82.0 |

9.9 |

|

Total operating expense |

177.0 |

21.4 |

|

Pre-tax gain/loss |

18.7 |

2.3 |

|

Registered capital |

40.0 |

4.8 |

|

Retained earnings |

−2.1 |

−0.3 |

|

Accumulated write-offs—Round 2 |

−533.2 |

−64.4 |

|

Write-offs − Round 1 + Round 2 |

−1,458.5 |

−176.1 |

The resulting analysis suggests that the four AMCs lost their RMB40 billion in capital entirely, with estimated write-offs of RMB1.5 trillion (US$176 billion) yet to be taken. This represents a loss rate of around 50 percent. While the profit or loss of the AMCs is only a rough guess, the amount of the write-offs is a more accurate figure and, what is more, they remain on the balance sheets of these four non-public, non-transparent enterprises.

The reason write-downs have not been taken is straightforward. A full or even partial write-off would lead to the outright bankruptcies of the AMCs, confronting the government with a difficult choice: either the banks would suffer significant losses on the AMC bonds or the MOF would have to bear the burden and explain to the NPC. At the outset of the reform process and the creation of the bad banks, their closure and full write-offs, including MOF payment on their bonds, had been part of the plan and explained as such.

Over the years, however, the plan had been changed and the MOF had assumed responsibility as a result of its bureaucratic victory over the PBOC. Now, in 2009, the banks seemed to be performing like world-beaters and the AMCs were noisily talking up their panoply of financial licenses; everyone had deliberately forgotten the history. Why should the MOF rock the boat when it is far easier to defer any decision until a more convenient time?

This is just what happened. In 2009, as their bonds came due, the AMCs were not closed down and their bonds were not repaid. Instead, the State Council approved the extension of bond tenors for a further 10 years. To support their full valuation on bank balance sheets, the MOF provided international auditors written support for the payment of interest and principal. Each bank’s annual financial report contains language such as the following from CCB’s 2008 report: “According to a notice issued by the MOF, starting from January 1, 2005, the MOF will provide financial support if Cinda is unable to repay the interest in full. The MOF will also provide support for the repayment of bond principal, if necessary.” Of course, a “notice” is not quite a guarantee; the MOF would never commit itself in writing to that. It does mean that it will in some way support the repayment of these obligations, unless at some point it is unwilling or unable to do so. Guarantees always come due at inconvenient times, as their extension in 2009 indicates. Until then, CCB, BOC and ICBC continue to carry these bonds at full value. As Table 3.1 shows, a default, or even a write-down of their value, would significantly impair the capital base of these banks and inevitably require yet another recapitalization exercise.

THE “PERPETUAL PUT” OPTION TO THE PBOC

This review of how the asset-management companies were used to resolve the problem-loan crisis in the banks highlights perhaps the most important part of the banking system: the perpetual “put” the PBOC has extended to the AMCs. In fact, this “put” extends beyond the AMCs to the entire financial system and weakens any reform effort that might be undertaken. It is the Party’s shield against financial catastrophes. In the name of “financial stability” the Party has required the PBOC to underwrite all financial cleanups, of which there have been many—from the trust-company fiascos of the 1990s, the securities bankruptcies of 2004–05 to the banks—at a publicly estimated (and probably underestimated) cost of over US$300 billion as of year-end 2005 (see Table 3.6).7 With this option available to them, bank management need care little about loan valuations, credit and risk controls. They can simply outsource lending mistakes to the AMCs, perhaps on a so-called negotiated “commercial” basis, and the AMCs will be almost automatically funded by the PBOC.

TABLE 3.6 Estimated historical cost to the PBOC of “Financial Stability” to FY2005

|

Time Period |

Amount (RMB billion) |

Use |

|

1997–2005 |

159.9 |

Re-lending to closed trust cos., urban bank co-ops, and rural agricultural co-ops to repay individual and external debt |

|

1998 |

604.1 |

Re-lending to the 4 AMCs for first-round acquisition of bank NPLs |

|

From 2002 |

30.0 |

Re-lending to 11 bankrupt securities companies to repay individual debt |

|

2003 and 2005 |

490.2 |

Huijin recapitalizes BOC, CCB, and ICBC |

|

2004–2005 |

1,223.6 |

Re-lending to 4 AMCs for second-round acquisition of bank NPLs |

|

2005 |

60.0 |

Additional lending to bankrupt securities companies to repay individual debt |

|

2005 |

10.0 |

Re-lending to Investor Protection Fund |

|

Total |

2,577.8 |

|

|

US$ billion |

315.5 |

Source: The Economic Observer ![]() , November 14, 2005: 3; PBOC Financial Stability Report 2006: 4; Caijing

, November 14, 2005: 3; PBOC Financial Stability Report 2006: 4; Caijing ![]() , July 25, 2005: 67

, July 25, 2005: 67

The new Great Leap Forward Economy

Added to the still unresolved loans of the 1990s, the US$1.4 trillion lending binge of 2009 will inevitably lead to correspondingly large loan losses in the near future (see Figure 3.7). The borrowers and projects are the same as in the previous cycle—infrastructure projects, SOEs and local-government “financing platforms, which will be discussed further in Chapter 5. But this time, their scale of borrowing is much, much larger; the press has even taken to referring to this as “Great Leap Forward Lending,” harking back to Mao Zedong’s ill-considered Great Leap Forward of 1958–1961. In early 2010, the regulators and Party spokesmen have taken the line that such investments will pay off over time. This is being echoed by brigades of analysts the world over, but the implication is well-understood by the Party itself. As one official put it simply: “In the near term, there will be no cash flow.” In other words, a large portion of these loans, over 30 percent of which reportedly went to localities, are already in default. Can the demise of the AMCs as originally called for in 1999 really be expected when their use has proven to be so great? To what extent can the Ministry of Finance continue to issue its IOUs?

FIGURE 3.7 Incremental bank lending, 1993–2009

Source: PBOC, Financial Stability Reports, various

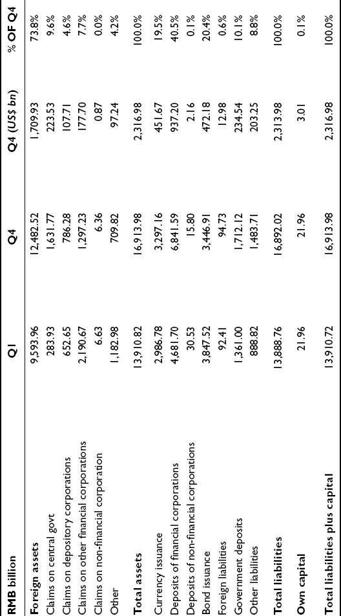

Against this background, it is not surprising that questions have been raised about the PBOC’s ability to continue to write the check for the Party’s profligate management of the country’s finances. It is interesting that the PBOC made public its own balance sheet for 2007 and that discussion around a recapitalization was rumored at about the same time (see Table 3.7).8 This may well explain, at least in part, the use of IOUs written by the MOF for the Agricultural Bank of China restructuring. The 2007 figures show that the central bank is leveraged at nearly 800 times its own capital.

TABLE 3.7 PBOC balance sheet, 2007

Source: PBOC, Financial Stability Report, 2008

It should not be surprising, therefore, that in August 2005, the PBOC created its own asset-management company designed to take “problems left over from history” off its own balance sheet. Huida Asset Management Company (Huida) was described in its brief appearances in the press as the fifth AMC and its operations since 2005 have remained mysterious since it did not sell its distressed-debt portfolios to outside investors. Huida was meant to operate as the twin to Huijin; Huijin made investments in the financial system that created problem assets while Huida was to collect on unpaid loans associated with such assets when and if they were taken on by the PBOC as part of its operations to maintain financial stability.

Huida, like Huijin, was a creation of the Financial Stability Bureau of the PBOC and all its senior management were staff in the Bureau, just as others were senior staff of Huijin.9 But unlike Huijin’s bank investments, the PBOC wanted to remove problem assets from its own balance sheet. Consequently, the actual equity investor in Huida had to be a third party and, given its close connections with the PBOC, Cinda AMC was the obvious choice (see Figure 3.8).

FIGURE 3.8 The establishment of Huida AMC, 2005

What were included in such problem assets?10 On Huida’s business license, the targeted assets were related to real-estate loans in Hainan and Guangxi and portfolios assumed as part of the GITIC and the Guangdong Enterprise bankruptcies. Interestingly, these figures are not included in Table 3.6, but can be estimated at around RMB100 billion.11 Despite such explicitness, financial circles at the time believed that the PBOC’s real intention was to put Huida in charge of working out the loans, totaling RMB634 billion, the central bank had made to the four asset-management companies in 2000. With a capitalization of just RMB100 million, whether it assumed the old problem assets or any part of the PBOC’s more recent AMC loans, Huida was going to be highly leveraged.

Assuming Huida did take on some or all of the PBOC’s AMC loans, such a transaction is illustrated in Figure 3.9. As previously described, the PBOC made loans to Cinda AMC in 2000 to enable it to purchase, on a dollar-for-dollar basis, problem-loan portfolios from China Construction Bank. These loans became assets on the balance sheet of the central bank that it then sold to Huida. Huida could only pay for such loan assets, however, if the PBOC lent it money in turn, which appears to have been the case. The net result of such a transaction was that Huida owned the loan assets associated with Cinda, while on its own books, the PBOC now held Huida loan assets.

FIGURE 3.9 The transfer of AMC loan portfolios to Huida

The only problem with this arrangement is that Huida is a 100 percent subsidiary of Cinda AMC. In other words, Cinda’s loan obligations to the PBOC (and ultimately Huida) were being held by itself. If such accounts could be consolidated, then the assets would offset the liabilities and everything would just disappear! None of this makes sense, except from a bureaucratic angle: the PBOC was able to park problem assets off its own balance sheet and Cinda—as a non-listed, and undoubtedly non-audited, entity—had no need to consolidate Huida on its own balance sheet. At best, these loans became a contingent liability: if Huida could not collect, then the PBOC’s loan to Huida would not be repaid. As noted previously, contingent liabilities (biaowai zhaiquan ![]() ) are not considered to be real in China’s financial practice; where in the national budget report are such things mentioned? A look at Cinda AMC’s excellent website fails to provide any proof of Huida’s existence as a 100 percent subsidiary. One wonders if there is a sixth or even a seventh asset-management company lurking out there in China’s financial system.

) are not considered to be real in China’s financial practice; where in the national budget report are such things mentioned? A look at Cinda AMC’s excellent website fails to provide any proof of Huida’s existence as a 100 percent subsidiary. One wonders if there is a sixth or even a seventh asset-management company lurking out there in China’s financial system.

But this is all just window-dressing compared to the PBOC’s huge exposure to foreign currencies, shown as “Foreign Assets” on its balance sheet. Strengthening its capital base, therefore, would appear prudent. By doing so, the government could openly demonstrate its commitment to a strong banking system. Of course, the sovereign, with its vast riches, stands behind the PBOC, but it is not so simple.

China’s massive foreign-exchange reserves give a false appearance of wealth: at the time the PBOC acquires these foreign currencies, it has already created renminbi. Under what conditions can these reserves be used again domestically without creating even larger monetary pressures? As they are, the reserves are simply assets parked in low-yielding foreign bonds and Beijing’s ability to use them is very limited. If the MOF is content to extend the life of the AMCs, consider how much more politically complex the issue of recapitalizing the PBOC would be.

In any event, the government appears to lack the desire to take on such subjects. The pressure to pursue meaningful financial reform has diminished since the struggles of 2005. Drowned in the flood of Party-supported “loans”, China’s banks in 2009 were back to where they left off before the entire recapitalization program began in 1998: they are financial utilities directed by the Party, just as was the case when the Great Leap Forward began more than 50 years ago. Whatever problems may arise can easily be dealt away to obscure entities that few know or will remember.

CHINA’S LATEST BANKING MODEL

As Chen Yuan remarked, China should not bring “that American stuff over here . . . it should build its own banking system.” It is doing just that with the bits and pieces of its old financial system that have been assembled by the asset-management companies. Before the final clean-up of the Agricultural Bank of China and the 2009 loan surge, the fate of the AMCs was actively discussed among the Big 4 banks and the State Council. What should have happened, but apparently will not happen now, was described thus by one of their senior managers:

For losses stemming from the first package of policy NPLs, the state will bear the burden [an estimated US$112 billion]. The losses on the commercially acquired NPLs [an estimated US$64 billion] are to come from the AMCs’ own operating profit after deducting the PBOC re-lending interest. If the price the NPLs were acquired at was not right, then any losses on the PBOC’s loans will be made up by AMC capital. In the end, the most likely outcome is that the AMCs will have to wrangle with the state.12

This AMC official knew full well that if the AMCs were to take write-offs, they would be bankrupted, forcing the MOF to step in and cover the value of their outstanding bonds and loans from the PBOC. Failing this, the banks would bear losses to their capital that they were (and are) not in any position to bear.

The collapse of Lehman Brothers in September 2008, however, changed this equation completely. The Chinese government acted as if a veil had been removed from its eyes as the international banking system teetered on the verge of collapse. Since at least 1994 and certainly from 1998, bank reform and regulation had been based on the American financial experience. Citibank, Morgan Stanley, Goldman Sachs and Bank of America were seen as the epitome of financial practice and wisdom. This American model and the vigorous efforts of the bank regulator and other market-oriented reformers to channel Chinese financial development within its framework immediately lost all credibility. But there was nothing to take its place. The banks, suddenly without restrictions, not only went on their famous lending binge, but also sought to grab as many new financial licenses as possible. As one senior banker said: “No one knows what the new banking model will be, so in the meantime, it’s better to grab all the licenses we can.” The easiest place to find a handful of these licenses was the AMCs. How did they come by so many?

In addition to taking on problem-loan portfolios from the banks, the asset-management companies also assumed the debt obligations of a host of bankrupt securities, leasing, finance, and insurance companies and commodities brokers. Of the collapse of this part of China’s financial system just five years ago, the world remains ignorant. In many of these cases, the AMCs were meant to restructure debt into equity and then sell it to third parties, including foreign banks and corporations. The proceeds of such sales would have partially or, if well negotiated, fully repaid the old debt. But in the great majority of cases, these zombie companies were never sold, nor were they closed. Ultimately, their names changed and their staff employed, they emerged as AMC subsidiaries. Orient AMC, for example, proudly boasts a group of 11 members, incorporating securities, asset appraisal, financial leasing, credit rating, hotel management, asset management, private equity and real-estate development. Cinda, the largest and most aggressive AMC, has 14, including securities, insurance, trust and fund-management companies. By acquiring the parent AMCs, Chinese banks could in one swoop hold licenses that would, on the surface, catapult them into the league of universal banks.

Of course, the banks were egged on by the AMCs, which did not want to be closed down. There was also an element of vindication: the AMCs were the repositories of unwanted staff who had been spun off as part of bank restructuring. Both began a game of chicken with the government, with the NPL write-offs as the target. By mid-2009, persistent rumors emerged that ICBC and CCB had each submitted concrete plans to the State Council to invest up to US$2 billion for a 49 percent stake in their respective affiliated AMCs. The very idea is astounding: 49 percent of what? But this was no rumor: by late 2009 Caijing ![]() magazine reported that the State Council had approved CCB’s 49 percent investment in Cinda valued at RMB23.7 billion (US$3.5 billion), with the MOF continuing to hold the balance.13 The total resulting registered capital of Cinda, including the MOF’s original RMB10 billion, was reported to be RMB33.7 billion. This is outrageous because it means not a penny of losses—operating or credit—had been taken by Cinda over its 10 years of operation. This is simply not possible, even if Cinda were the best-managed of the four companies. Or perhaps the operations of its myriad new subsidiaries had offset such losses. Who knew?

magazine reported that the State Council had approved CCB’s 49 percent investment in Cinda valued at RMB23.7 billion (US$3.5 billion), with the MOF continuing to hold the balance.13 The total resulting registered capital of Cinda, including the MOF’s original RMB10 billion, was reported to be RMB33.7 billion. This is outrageous because it means not a penny of losses—operating or credit—had been taken by Cinda over its 10 years of operation. This is simply not possible, even if Cinda were the best-managed of the four companies. Or perhaps the operations of its myriad new subsidiaries had offset such losses. Who knew?

Even were it not bankrupt, one wonders at the amazing valuations characterizing the proposed Cinda transaction. Are Cinda and its unknown subsidiary, Huida, any different from those puffed up special-purpose vehicles whose deflation led to the bankruptcy of Enron, not to mention the near collapse of the American financial system in 2008? And there was more to the new arrangements. On the same day the Cinda deal was mooted, the MOF announced that Cinda’s RMB247 billion bond owed to CCB was to be extended for a further 10 years. This action undoubtedly represents the first step to extending the institutional life of the other three companies as well.14

The year 2009 marked the end of banking reform as advanced since 1998. What will follow is beginning to look like a glossier version of the old Soviet command model of the 1980s and early 1990s. In the end, the Cinda deal could not be done in its proposed form. By mid-2010, however, a new structure for Cinda had been rolled out. Cinda was incorporated, with the MOF as the sole shareholder, and its valueless assets, including the loans it owes the PBOC, were spun off into the now increasingly ubiquitous “co-managed account” in return for more MOF IOUs. This left Cinda and its bevy of financial licenses able to begin the search for a “strategic investor,” which, of course, is expected to be CCB. From this continual recycling of debt, it seems that, despite its fantastic riches, the Party—and certainly the MOF—lacks the wisdom and the determination to complete the bank reform begun in 1998.

IMPLICATIONS

The question is often raised: does it matter how the Party manages this machinery for failed financial transactions? China, after all, has the wealth to absorb losses of this scale, if it is determined to do so. The answer to this question must be “Yes.” Every day, the press carries stories about China’s National Champions and its new sovereign-wealth fund seeking out investment opportunities in international markets. The internationalization of the renminbi has made headlines as China seeks to challenge the dominance of the dollar as the international currency for trade and, perhaps someday, the international reserve currency. But little is heard from China’s banks; why?

When in 2008 the Western banking sector was in full disarray and the world was applauding the Chinese for their stimulus package, Merrill Lynch and Morgan Stanley were going for a song. Where were China’s banks? A small deal in South Africa and a community bank in California were all there was to show for these proud financial giants. More recently, the head of one of the Big 4 banks dismissed the growth opportunities of developed markets such as the US: tell that to Jamie Dimon!15 One can well imagine how the US Government would have been forced to react had ICBC come to the Department of Treasury in those dark days with a full cash offer for Citigroup, Wachovia, Washington Mutual or Merrill Lynch. For China, the whole shopping basket would have been cheap. Opportunities forgone in a period such as the world has just passed through may never present themselves again. In contrast, China’s corporates, the China Development Bank, and its sovereign-wealth fund have actively sought international investments: why haven’t the banks?

Put another way: if market valuations for Chinese banks are real and the banks are in such great shape, why hasn’t China’s banking model been exported? As US and European regulators and governments look for a way to prevent the next financial crisis, why is China’s model—with its asset-management companies, outright state ownership and central bank lending—not invoked? If, as some predict, China seeks to replace the US at the center of the global economy at some time in the near future, one would expect it to export not just capital, but also intellectual property. It is nowhere to be seen, nor is it expected.

The story of the past 10 years suggests that China’s banks, despite their Fortune 500 rankings, are not even close to becoming internationally competitive. They simply do not operate like banks as understood in the developed world. Their years of protective isolation within the “system” have produced institutions wholly reliant on government-orchestrated instruction and support. When the Organization Department determines a bank CEO’s future, what can be expected? Despite the prolonged effort to reform the corporate-governance mechanism of the banks, can anyone believe that a bank’s board of directors is more representative of its controlling shareholder than its Party Committee? These banks are undeniably big, as they always were, but they are neither creative nor innovative. Their market capitalizations are the result of clever manipulation of valuation methodologies, not representative of their potential for value creation. In 2010, as one Chinese bank after another announced multi-billion-dollar capital-raising plans, one wonders what happened to the huge amounts of capital each had raised just three or four short years ago. Despite apparently outstanding profits, they have not grown their capital fast enough and that is even without considering any mark-to-market valuation of the now perpetual AMC bonds or their huge exposures to the domestic bond markets. The fact is they are now, and were even after their IPOs, undercapitalized for the risks they carry on their balance sheets, and this accounts for their outstanding return-on-equity ratios.

China’s banks are at the mercy of domestic political disputes and this emphasizes their passive role in the economy. As others have noted, China’s banks have traditionally operated like public utilities. Zhu Rongji’s effort to push the banks toward an international model has been stopped and the banks have reverted to their traditional role. Without question, in 2010, they are again huge deposit-taking institutions, extending loans as directed by their Party leaders. Whatever degree of influence their boards of directors and senior management may have gained over the past decade, from 2009, they are no longer much more than window-dressing, as is the previously well-regarded bank regulator. If banks are about measuring and valuing risk, these entities, having begun to learn, have now quickly forgotten.

Any argument that they have no need to study “that American stuff” since the bulk of their “lending” is to state enterprises is demonstrably specious: SOEs don’t repay their loans. Banks know that it does not matter whether or not such loans are repaid. First, the Party has taken all responsibility and management cannot be blamed for following orders. Second, as this chapter has shown, there is already a well-proven infrastructure in place to hide bad loans. The future development of the AMCs, as well as the almost-virtual “co-managed account,” now seems assured. Careers can be lost only if managers fail to heed the Party’s rallying cry. It is the Party, and not the market, that runs China and its capital-allocation process.

In the absence of public scrutiny, few have called into question the quality of bank balance sheets and earnings. This is understandable domestically, where the media is subject to the Party’s “guidance,” but it is also the case outside of China. International stock markets and brigades of young equity analysts have lent the credibility of their institutions to the idea that banks in China are just that, banks, and have value, if not as individual institutions, then as proxies of the country’s economy. That is just the point: they are indeed proxies of the economy “inside the system.” In this economy, the Party makes what organizational arrangements it likes, a prime example being the bank buy-back of the un-restructured AMCs. The public line supporting this idea as put forth by an analyst at a major American bank goes: “The asset managers will have the largest capitalized banks in the world behind them which are interested in their expanded business, so there are valid business reasons why this [investment in the AMCs] should happen.” Other foreign analysts at major institutions have eagerly echoed this thought.

Such unthinking commentary does China no service. It would be even more dangerous if the Chinese government were lulled into believing that the Big 4 banks are in fact world class and proceeded to encourage them to expand internationally. What effect would the consequent scrutiny by Western regulators and media have? Having seen what constant media focus on sub-prime debt and securitization vehicles caused in the US in 2008, however, no one should be sanguine. Bear Stearns and Lehman Brothers, it should be remembered, disappeared over a weekend. China’s political elite has surely learned a lesson from this experience, just as it has from other international financial crises.

In China, political imperatives make significant internationalization of the banks unlikely. The Big 4 banks form the very core of the Party’s political power; they work in a closed system with risk and valuation managed by political fiat. True, China’s banks have taken on an international guise by public listings, advertising campaigns and consumer lending. As 2009 has shown, however, such change is superficial: true reform of their business model remains a goal that will be the more difficult to reach the closer it is made to seem. These banks will always be closely guarded and directly controlled domestic institutions. Leaders of major international banks in recent years have spoken of creating “fortress balance sheets” able to withstand significant economic stress. In China, there is also the drive to create a fortress, but it is one that seeks to insulate the banks from all external and internal sources of change in the belief that risk should remain under the Party’s control.

In 2009, China’s banks extended a tidal wave of loans exceeding RMB10 trillion. If in the next few years, these loans do not give rise to a significant volume of NPLs and continue to be carried on balance sheets at full face value, the banking system by definition must continue to be closed. On the other hand, if risk classifications based on international standards are applied consistently, a repeat of the 1990s experience is in the making, with huge volumes of unpaid loans and the banks again in need of a massive recapitalization. Already, the tsunami of lending and high dividend payouts have stretched bank capital-adequacy ratios and forced the need for more capital, which comes largely from the state itself. It is somewhat ironic that the demand for capital can also be mitigated by reducing loan assets, ensuring that the AMCs will continue to play a central role.

There is a further important aspect to this arrangement. Over the past several years, China’s banks have enthusiastically entered consumer businesses; credit and debit cards, auto loans and mortgages have become common in the country’s rich coastal areas. From 2008, the collapse in exports has revealed a great weakness in China’s export-dependent economic model; experts from all sides have urged the government to develop a domestic consumption model similar to that of the US (always the US model!). Pushing in the same direction is China’s ageing demographic. If the government does seek to replace export demand with domestic consumption, this suggests that the domestic savings rate will decline, as will household deposits. What will happen to the banks then? Today’s financial system is almost wholly reliant on the heroic savings rates of the Chinese people; they are the only source of non-state money in the game. The AMC/PBOC arrangement works for now because everyone saves and liquidity is rampant. What happens to bank funding if the Chinese people learn to borrow and spend with the same enthusiasm as their American friends? From this viewpoint, a profusion of new investment and consumer-lending products appears unlikely. Similarly, this view suggests that full funding for social security is a reform whose time will not come.

Finally, there is the foreign banking presence. International banks were very active in the negotiations leading to China’s accession to the World Trade Organization, producing a detailed schedule that opened China’s domestic banking markets. China has largely abided by the agreement and, over the past eight years, foreign banks have invested heavily in developing networks and new banking products. With a focus primarily on domestic consumers, new branch networks and the brand advertising of the major American and European banks have become common in China’s major cities and media. Foreign banks have also been quick to engage in the development of a market for local-currency risk-management products.

These banks understand that China and its financial system are in transition and most are prepared to persist in the expectation that at some time in the not-too-distant future, the market will be open fully to them. This was the commonly held position prior to 2008. But the conclusions about the global financial crisis now being drawn by the Chinese government suggest that opening and reform along the lines of the now apparently discredited international financial model will no longer continue. This is not to say there is another model . . . except for the prolongation of the status quo, and this is the direction to which recent events point. What future, then, is there for foreign banks in China?

In summary, China’s banks operate within a comfortable cocoon woven by the Party and produce vast, artificially induced, profits that redound handsomely to the same Party. As demonstrated by the 2008 Olympics or the wild celebrations of the country’s sixtieth anniversary, the Party excels in managing the symbolism of economic reform and modernization. Ironically, however, if the Asian Financial Crisis in 1997 caused one set of Chinese leaders to see the need for true transformational reform of the financial system, the global crisis of 2008 has had the opposite effect on the current generation of leadership. Their call for a massive stimulus package reliant on bank loans may have washed away for good the fruits of the previous 10 years of reform. Even more ironic, while the “good” banks have been weakened, the “bad” banks created for the earlier reform effort are being strengthened, perhaps in preparation for the next inevitable wave of “reform.” If emerging markets are so defined because their institutions are always “in play,” buffeted by the prevailing political needs of the government, then real change depends on the next major crisis and a Party leadership willing to accept that today’s symbols do not reflect underlying reality and that the true needs of China’s economy are not being met.

ENDNOTES

1 China Daily, August 25, 2010: 9.

2 The bonds originally had a 10-year maturity, but this, as well as the coupon, changed in 2005. The new coupon is a more manageable 2.25 percent despite its much longer tenor, which was extended to 2028.

3 In ABC’s case, this bond was just replaced by an MOF IOU.

4 The RMB93 billion noted is the amount injected into the two banks in 1998 by the MOF’s arrangements as part of the RMB270 billion Special Bond. As the total NPL ratio for the banks stood at 40 percent at that time, it cannot be the case that any of the banks had any real retained earnings.

5 In fact, the PBOC slightly diversified CCB’s shareholders by allowing a number of central SOEs, as well as the National Social Security Fund, to hold shares. Hence, the PBOC held only a little more than 95 percent of CCB at this point.

6 The original AMC bond, totaling RMB138 billion, owed to ABC from 1999 was replaced by the IOU; RMB150.6 billion in NPL assets was used to offset a PBOC loan of the same amount.

7 See The Economic Observer![]() , December 26, 2005: 34. This number may be even larger. The PBOC, in its Financial Stability Report 2005, has also reported a figure of RMB3.24 trillion or US$390 billion.

, December 26, 2005: 34. This number may be even larger. The PBOC, in its Financial Stability Report 2005, has also reported a figure of RMB3.24 trillion or US$390 billion.

8 Keith Bradsher, “Main Bank of China is in Need of Capital,” New York Times, September 5, 2008.

9 Yu Ning, “Huida deng chang ![]() (Huida takes the stage),” Caijing

(Huida takes the stage),” Caijing ![]() , July 25, 2005: 65.

, July 25, 2005: 65.

10 See “Huida zichan tuoguan fuchu shuimian Zhan Hanqiao huoren rending shizhang ![]() (Huida Asset Management surfaces; Zhang Hanqiao likely appointed as Chairman),” China Business News

(Huida Asset Management surfaces; Zhang Hanqiao likely appointed as Chairman),” China Business News![]() , August 3, 2005: 1.

, August 3, 2005: 1.

11 The absence of the Hainan and Guangdong figures makes one wonder about the fate of the huge amounts of “triangle debt” Zhu Rongji untangled in the early 1990s that were left over from the 1980s banking debacle.

12 Caijing ![]() , May 12, 2008: 79.

, May 12, 2008: 79.

13 www.caijing.com.cn/2009-09-23/110258742.html

14 The bond owed to Bank of China by its related AMC, Orient, was also extended as it came due in 2010; without question the similar Huarong bond held by ICBC can also be expected to see its life extended later in 2010.

15 CEO and Chairman of JPMorgan Chase & Co.