ACCUSTOMED AS WE ARE TO THE NOTION of national railroads and large rail monopolies, it is hard to imagine today that the early railroads were made up of hundreds of small companies, each serving its own limited local area. Local entrepreneurs created these railroads, largely from a desire to improve transportation for their own goods rather than as a result of any grand vision. However, as the railroads expanded, they became more ambitious in scope, and economies of scale became evident. Not only was it convenient for people to travel long journeys on one train, it was also more profitable for the train companies to operate in this way. It was relatively cheaper to carry goods over a longer distance, as loading and unloading them was expensive.

Lines gradually grew longer. In Britain, the London and Birmingham Railway was the first railroad more than 100 miles (160km) long, and a civil engineering project far larger than any that had gone before. Robert Stephenson, son of George Stephenson (see The Father of Railroads), was appointed chief engineer in 1833 and the railroad, London’s first main line, opened five years later in 1838. Other, longer, railroads soon followed, such as the Great Western from London to Bristol, constructed by engineer Isambard Kingdom Brunel between 1835 and 1841 at a cost of $32.5 million (£6.5 million), and the London and Southampton, completed in 1840. In the United States, both the pioneering railroads—the 136-mile (219-km) Charleston and Hamburg, opened in 1833, and the Baltimore and Ohio, whose first section ran from 1830—were ambitious projects that extended far inland from the Atlantic Coast port cities they served.

The men who managed the railroad companies were generally enterprising and progressive, and could see the benefits of far-reaching railroad networks. As the railroads became established, these men dreamed up ever-grander plans, and railroad promoters raised financing for their construction. These longer railroads began to sprout branches, and the companies grew. Given the advantage of large networks, it was inevitable that railroad companies should come together first to provide joint services. However, even as they extended their reach, the railroad companies remained distinct until competition between them made the creation of monopolies attractive and they began to merge—a process that accelerated when railroads fell on hard times, and rivals took over their struggling competitors.

Consolidated railroad companies soon became the biggest enterprises in the world. In many respects, their development prefigured the growth of capitalism. Before the railroads, there were no large companies in any industry, with the exception of quasi-government organizations such as the Dutch East India Company. Factories were still just small buildings where goods were made, owned by local entrepreneurs and supplying their immediate area. These firms employed local people and were part of the local community.

The railroads were a totally new and different sort of enterprise. To begin with, they stretched dozens and later hundreds of miles, taking them across many different localities. Then, they demanded a new style of management with complex organizational structures. Furthermore, the companies needed bosses with vision and great ability, able to see the bigger picture as well as being industrious. In Britain, already off to a head start with the railroads, the first larger-scale, consolidated, companies began to emerge. The new companies were powerful and self-important, as testified by the grand stations they erected in major cities (see Turnouts and Sidings). The first mega-company to spring from the dozens of smaller railroads was the Midland Railway, created by entrepreneur George Hudson (see George Hudson). In 1844, Hudson created the Midland by consolidating three lines: the North Midland Railway, the Midland Counties Railway, and the Birmingham and Derby Junction Railway, all of which converged at Derby. The new, combined railroad created the core of a line that ran all the way from London to York, offering a more convenient service to its passengers, with fewer changes of train. Hudson had also built the Newcastle and Darlington Junction Railway, which he now linked to the rest of his network via York, so that he had control of more than 1,000 miles (1,600km) of railroad. He continued to consolidate the network throughout the 1840s by taking over other smaller Midlands lines. In 1842, Hudson cleverly created the Railway Clearing House, an organization that enabled all the railroad companies—of which there were now more than a hundred in Britain—to collect revenues from each other when passengers used more than one company’s trains on a journey. Until then, passengers had been obliged to change trains and buy a new ticket at each stage of the journey. Sadly, for all his entrepreneurial genius, Hudson turned out to be a fraudster. The ticket-sharing plan, however, long outlasted his downfall and the collapse of his railroad empire.

Despite the obvious advantages of consolidation, British politicians were reluctant to let the railroads merge, fearing that monopolies would exploit the public. However, the financial weakness of some railroads forced the government to accept the idea, especially at times of economic downturn, so throughout the mid-19th century, companies continued to merge.

One of the merger beneficiaries, the London and North Western Railway (LNWR), was, for a while the world’s biggest company, employing 15,000 people at its peak. Its brilliant manager, Captain Mark Huish, was a former Indian Army officer. He shrewdly negotiated takeovers, managed the company in an innovative manner, and introduced novel accounting methods essential for the company’s size. The LNWR was created in July 1846 by the merger of the Grand Junction Railway, the London and Birmingham Railway, and the Manchester and Birmingham Railway. This created a network of 350 miles (560km). The core route connected London with Birmingham, Crewe, Chester, Liverpool, and Manchester. Although it covered less ground than rivals such as the Midland, the LNWR offered the best route between London and the main towns of northwest England.

Once it was in a position of strength, the LNWR bullied rivals into forced mergers or disadvantageous deals to run on their tracks. But the bully-boy tactics did not always work. Two small railroads that combined to run on a shorter route between Birmingham and Chester than their big rival were warned off by Huish: “I need not say if you should be unwise enough to encourage such a proceeding, it must result in a general fight…” To his alarm, they resisted the threat, fought a three-year battle through the courts, and, surprisingly, won. However, this was an exception. For the most part, the big bullies effectively quashed their smaller rivals.

In continental Europe, major networks were soon created from the plethora of companies that had started running rail services. In France, six big regional companies were formed with government encouragement between 1858 and 1862. The most ambitious, the Paris–Lyon–Mediterranée (PLM) , soon extended over the border to Switzerland and Italy, creating an international network. The Rothschild banking family owned the PLM, along with a second French company, the Nord, and it looked for a time as if the Rothschilds would establish themselves as the dominant force in European railroads. At one point they also controlled the Austrian Südbahn, which included the Semmering Railway (see Crossing the Alps), and had concessions on various Italian lines. After unification, however, Italy prevented the Rothschilds from expanding their railroad empire and effectively blocked the creation of “the biggest international railway company that had ever been seen.” Instead, four big Italian companies were formed, but the poverty of the country and its difficult terrain, with the Apennines running down its spine, made it hard to make a profit. The nation suffered a railroad crisis every few years and, unwilling to allow foreign takeovers, Italy in 1905 became one of the first nations to nationalize its railroad system. In the early days of Swiss railroads, meanwhile, the plutocrat Alfred Escher (see Alfred Escher) more or less oversaw the explosion in railroad construction from the 1850s, and became so powerful that he was nicknamed “King Alfred.”

The American railroads soon eclipsed all others in scale. The distances to be covered were huge, so big companies such as the Erie and New York Central Railroad and the Pennsylvania Railroad emerged early in railroad history. When the first transcontinental was completed in 1869 (see Crossing America), the Union Pacific and Central Pacific railroads became the railroad giants. After them, a series of American railroads earned that accolade as railroad barons consolidated the network.

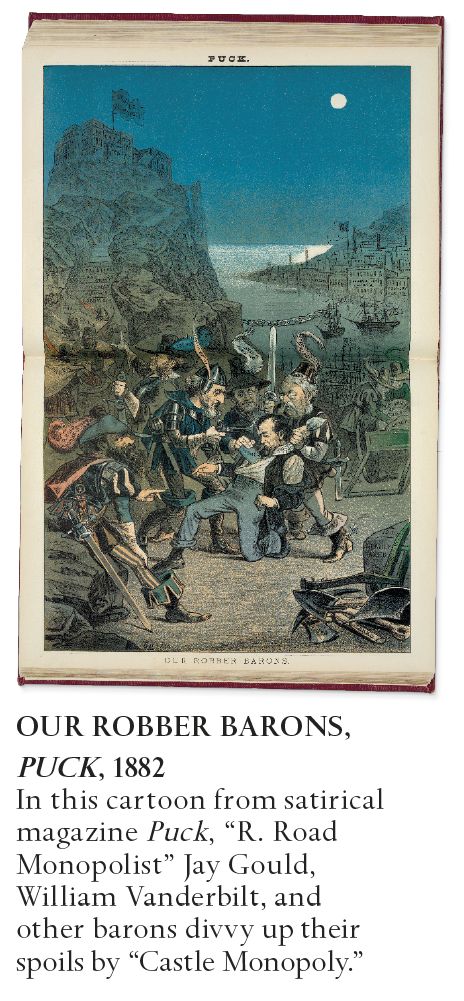

By 1900, seven companies controlled most of the US railroads. Many of their proprietors became infamous, among them Jay Gould and his son George, J. P. Morgan, Edward Harriman, and the Vanderbilts. William, the younger Vanderbilt, demonstrated the attitude of the new railroad barons to their passengers when asked by a reporter why a popular fast train was no longer operating: “The public be damned! … I don’t take any stock in this silly nonsense about working for anybody but our own,” he is alleged to have replied. Daniel Drew, one of the first of these “robber barons”—a term applied by Atlantic Monthly in 1870 to the new breed of capitalists—was also one of the biggest rogues. As company treasurer of the Erie, Drew agreed several times for the company to borrow money against newly issued shares, and then used his position as an insider to profit from the trade in these shares—insider trading was not regulated at the time.

J. P. Morgan was the most successful of these entrepreneurs, forging a railroad empire that stretched across the US by taking over ailing companies and reorganizing them. Unlike Drew, Morgan actually improved the railroads he acquired. So too did Harriman, who became known as the “greatest rail baron in America.” His background, as with most of these moguls, was modest: he started out as a messenger boy, but made money on the stock exchange and invested in railroads. He boosted his assets by purchasing rolling stock, improving tracks, and establishing good management. His first major acquisition was the Illinois Central Railroad. After the Panic of 1893—the last of a series of major 19th-century recessions caused by boom and bust in the business cycle—he added the massive Union Pacific to his set. Harriman made it profitable by straightening out bends in the track—many added unnecessarily by the builders to take advantage of government subsidies—and reducing grades, and it became a moneymaker. By the turn of the century, Harriman controlled more track than any individual in the history of American railroads. He was the baron of barons.

All too soon, the advent of the motorcar brought about the decline of the railroads, and empires were broken up or bailed out by the government. In the US, however, one last pair of barons emerged in the 1920s: the Van Sweringens. This strange pair of reclusive brothers were property developers who bought a railroad for its development potential and ended up with an empire that included the Erie, the Chesapeake and Ohio Railroad, and the Pere Marquette Railroad, which operated a series of lines in the Great Lakes area. Following the 1929 crash, however, their empire was broken up even more quickly than they had built it up. With this, the era of the big railroad barons finally came to an end.