CHAPTER 3

We’ve come to associate content on the Internet as “free.” In fact, under the ad‐based Internet model, we expect all content to be free. Tweets, memes, videos, articles—you name it—if it’s not free, then the vast majority of us are just clicking away from it. For this reason, it’s hard for most people to wrap their minds around purchasing something digital, such as a non‐fungible token (NFT), which otherwise appears to be free: “Why would I want to buy something that anyone can view online, take a screen capture, and then claim ‘ownership’ of the digital result?”

The answer to this question is multifaceted, and we’ll get into the reasons why throughout this chapter. However, just as we first covered why people collect in Chapter 2, “What Are NFTs?” we’d like to address an initial principle around “value” in order to create a baseline understanding of why NFTs have value.

Why Do Collectibles Have Value?

World War II recalibrated the importance of resources. Most of us are familiar with the nationwide rationing of sugar, meat, gasoline, tires, and paper. But did you know that copper was also on the list of resources in short supply?

Copper was essential to generator and motor windings, as well as radio circuitry and ammunition. With WWII taking place on land, air, and water, there were many more machines that needed copper wiring in order to operate. Not to mention, we could never create enough ammunition to fight the war.

Domestically, though, the United States wasn’t producing nearly enough copper to satisfy the wartime needs. And can you guess who was one of the biggest consumers of copper at that time? The U.S. Mint.

In December 1942, Congress passed a bill authorizing the U.S. Mint to explore different metals for use in pennies. As a result, starting in 1943, the composition of pennies changed from 95 percent copper, 4 percent zinc, and 1 percent tin to almost entirely steel with a thin zinc coating to avoid rusting.

About 1.1 billion steel pennies later, the U.S. public pushed back against the change in appearance from brown to silver‐colored pennies, and the lighter‐weighted composition also confused vending machines. And so, the steel pennies ceased production in 1943, and we reverted to a 95 percent copper and 5 percent zinc penny composition (until 1982 when it was changed again to copper‐plated zinc).

Within the one‐year transition of materials, extra planchets (round metal disks ready to be stamped) of both copper and steel carried over into the following year. This resulted in 1943 copper pennies and 1944 steel pennies, which were supposed to be discontinued the year prior, but were produced anyway, most likely in error.

Approximately 40 copper pennies were created in 1943, and 35 steel pennies were made in 1944. When compared to the billion‐plus pennies produced over those two years, these 75 errors were instantly rare.

In the process of contributing their part to the wartime effort, the U.S. Mint simultaneously created a rarified collectible for numismatists everywhere.

Fast‐forward many decades, and estimates place the 1943 copper penny at somewhere between $150,000 to $200,000, and the 1944 steel penny somewhere between $75,000 and $110,000 (depending on their condition, of course).

However, as the saying always goes, art is worth whatever someone is willing to pay for it. This applies to collectibles as well.

In 2010, Bill Simpson, co‐owner of the Texas Rangers, spent a record‐breaking $1.7 million on a 1943‐D copper penny and seven years later dropped another $1 million on a 1943‐S copper penny (the “D” designates the Denver Mint, and the “S” designates the San Francisco Mint). These two purchases completed his collection of a 1943 copper penny from all three U.S. Mints in existence at the time (the other one being 1943‐P, where the “P” stands for Philadelphia).

The fact that a penny, with a street value of 1 cent, can fetch a seven‐figure price tag is absurd. But we can’t think of a better metaphor for how collectibles appreciate and how they can represent a value far more than originally intended.

Simply because something is rare doesn’t mean that it’s valuable, though. There are many factors that affect the price of collectibles as follows:

· Proof of Provenance

Provenance relates to the origin of an item. When referring to collectibles, provenance is a record of ownership used as a guide to authenticity or quality. Proof of provenance, therefore, recognizes that a given collector’s item is in fact what it claims to be. With respect to art, provenance is the documented chain of title from the current owner all the way back to the artist. When it comes to art and collectibles transactions, provenance can make or break a sale.

· Historical Significance

The time period in which a collectible was created, or the historical story leading up to its creation, can impact the price of the collectible. The fact that WWII inadvertently caused the creation of the rare 1943 and 1944 pennies plays into the story of that coin. It adds to the complexity of why it happened, which is in stark contrast to the many other error coins that have been released from mints throughout history simply by mistake.

· Sentiment

The emotional connection between collector and collectible cannot be downplayed either. And this sentimental connection can lead collectors to overpay for a collectible just because it means something significant to them.

· Condition

Obviously, the condition of a collectible matters. Collectibles of all kinds are analyzed and graded for their wear and tear. When it comes to one‐of‐one, unique pieces, the condition doesn’t play a significant role. However, when multiples of a collectible exist, as is the case in the wartime penny example, the better the condition the higher the value. This is why collectors go to great lengths to preserve the quality of their collections.

· Collection Completion

Owning the entire set or variations of a collectible also plays into the price. For ultra‐collectors like Bill Simpson, the thrill of the hunt takes over, and they want to have a complete collection. The rarer the collectible, the harder it is to complete the set. Therefore, acquiring an entire set of a collectible increases the value of the individual parts. In other words, it makes the collectibles more marketable.

It goes without saying that the value of collectibles may be an enigma to outsiders. Imagine trying to buy a million‐dollar house with one of those rare pennies. You’d be laughed out of the room (by those who aren’t aware of the penny’s rareness).

Collectible value is rarely understood by people outside of that collectible’s universe. But that’s the point. Collectibles are largely driven upward in value because there are collectors. Supply and demand are the main function behind the value of collectibles. All of the other factors play into the story of the collectible, but if there’s no demand, then there’s really no value (at that point).

Another group of collectors who understand the principles that drive value are fine art collectors. And if there’s one thing that all collectors must address, it’s the piece’s authenticity.

To understand NFTs and their value, let’s first explore the problems afflicting the traditional art and collectibles worlds. Both fields throughout the years have been plagued by fakes, forgeries, other shenanigans, and lots of question marks.

The Problems with Traditional Art

A dirty little secret in the art world is that forgeries have for ages littered the art market, and the problem still exists today. According to a 2014 report by Switzerland’s Fine Art Expert Institute (FAEI), 50 percent (that’s right, 50 percent) of fine art in circulation on the market is forged or misattributed. Although that figure has been disputed, forgeries nonetheless continue to be discovered in private collections, galleries, and museums in a global market that saw more than $64 billion in sales in 2019.

Recent Forgery Scams

Art forgeries and fakes have been going on for millennia, yet the authentication methods have not changed at all. The following are just some of the recent art forgery scams that highlight the fallibility of the methods used to authenticate works of art.

The Old Masters Forgery Scam.

A Frans Hals portrait, supposedly painted in the 17th century, was sold for $10 million in 2011. In 2016, it was found to have modern‐day materials in the canvas, proving it a forgery. It’s believed that this scandal could involve up to 25 Old Master paintings with a total value of $255 million.

The Knoedler Forgery Ring.

Between 1994 and 2008, the Knoedler Gallery sold more than two dozen forgeries, with an aggregate value of $80 million, to unsuspecting buyers. A Long Island art dealer, together with her boyfriend and his brother, engaged an artist in Queens, New York, to create paintings in the styles of Jackson Pollock, Mark Rothko, and Robert Motherwell, among others. The ringleaders also created forged provenance (chain of title) documents.

Fake Giacometti Bronzes.

A forger of Swiss artist Alberto Giacometti was finally busted in 2011 after selling more than 1,000 forged sculptures and fake bronzes to the tune of nearly $9 million over a 30‐year span. Because recasting is easier than painting, the sculpture market is even shadier than the painting market. The scam continues to have repercussions today, as many of the forged sculptures are still on the market.

Fakes Sold on eBay.

In 2016, a Michigan art dealer was caught using several aliases over a span of 10 years to sell dozens of forged artworks on eBay. The forged artists included Willem de Kooning, Franz Kline, and Joan Mitchell, among others. The forger also created fake receipts, bills of sale, and correspondence in order to provide provenance for the forged works. The Smithsonian may have been taken, as it has six works in its collection from this dealer.

Note that these are just a few of the most recent high‐profile forgery scams. Going back a little further, between 1985 and 1995, Londoner John Myatt, often touted as one of the masters (of forgery), painted more than 200 forgeries of artists such as Chagall, Picasso, and Monet, which he had sold for multiple millions of pounds, duping the most prestigious galleries, collectors, and auction houses. Today, the art world is no better off when it comes to forgeries, and there doesn’t appear to be any relief in sight.

Connoisseur Fallibility

In the art world, paintings and other works of art are authenticated by connoisseurs. These are experts who gander at a work attempting to sense the presence of the artist’s hand. They then render a completely subjective opinion based upon their “expertise” and “experience.” The obvious drawbacks of this system of authentication are that it’s completely subjective—the so‐called experts are fallible, have biases, and are potentially corruptible. When dealing with a painting that could have a value of tens or hundreds of millions of dollars, it’s not that hard to get “fooled.”

The high‐end art world is also like a high school clique. If they don’t want you in, you’re going to have a tough time. Take, for example, a painting that then 73‐year‐old, foul‐mouthed trucker Teri Horton bought at a thrift shop for $5. The 2006 documentary film Who the #$&% Is Jackson Pollock? (Picturehouse, 2006) follows her journey to get the painting recognized by the art world as a Jackson Pollock. Not surprisingly, given the lack of provenance, the experts declared that the painting was an obvious forgery. Frankly, we’d be skeptical too. But then Teri Horton hired a forensics scientist who found a fingerprint on the back of the canvas that matched a fingerprint from a paint can at Jackson Pollock’s studio. It also matched fingerprints found on other authentic Jackson Pollock paintings. On top of that, the composition of the paint on Teri’s painting and paint from the floor of Jackson Pollock’s studio matched identically under gas chromatograph analysis. Yet despite the forensic evidence, the “experts” to this day still insist that their original subjective conclusions are correct with one of them declaring that the painting just “doesn’t sing like a Pollock.”

It’s shocking that many billions of dollars of value in the art world are relying on “experts.” There’s also no telling how many forgeries continue to lie in plain sight, once authenticated by connoisseurs.

Provenance Issues

The other factor utilized to authenticate works of art is their provenance, which as noted previously is a documented chain of title from the current owner all the way back to the artist. Oftentimes with art forgeries, the painting was “newly discovered” and has no, or little, provenance documentation. At other times, as in some of the previous examples, the provenance is completely fabricated with false documents.

Even more harrowing is the fact that scammers with forged paintings have been inserting fake provenances into the archives of storied institutions such as the Tate Gallery, the Victoria and Albert Museum, and the British Council, among others. How can any polluted archive be trusted with respect to any painting? It’s not even known how widespread this practice is. Some archives may not even know if and to what extent they contain fake provenances. Additionally, some forgers have even printed fake catalogs and placed them in museum libraries.

It’s unfathomable how disgraceful the art world has been, and continues to be, when it comes to authenticating works of art, especially when tens or hundreds of millions of dollars can be at stake. How can any work of art be trusted at this point?

The Problems with Collectibles and Memorabilia

The size of the global collectibles market is an estimated $370 billion. This covers a range of collectible items from sports cards and memorabilia to antiques, comic books, coins, stamps, and, of course, Beanie Babies, among several other types of collectibles. Similar to the art world, fakes and forgeries in the collectibles market are rampant. Up to 80 percent of antiques sold online are likely looted or fake. Twenty years ago (and perhaps still today) a potential 90 percent of sports memorabilia sold in the United States was fake. The FBI even had to crack down on counterfeit Beanie Babies.

Forgeries

All types of forgeries flood the collectibles market. The following examples are but a drop in the ocean.

Fake Signatures.

In the 1990s, in what was dubbed Operation Bullpen, the FBI infiltrated the nationwide memorabilia fraud market and cracked down on several forgery rings and individuals involved in forging signatures for all types of sports and celebrity memorabilia. Experts and cooperating subjects estimated that forged memorabilia comprised more than $100 million each year. The operation resulted in the following accomplishments:

· 63 charges and convictions

· Seizures exceeding $4.9 million

· 18 forgery rings dismantled

· More than $300,000 in restitution paid to more than 1,000 victims

· $15,253,000 in economic loss prevented in the seizure of tens of thousands of pieces of forged memorabilia through 75 search warrants and more than 100 undercover evidence purchases

One of the persons convicted in Operation Bullpen, Greg Marino, the subject of an ESPN film The Counterfeiter, is known as the world’s greatest forger. From Babe Ruth to Mickey Mantle to Ty Cobb to Albert Einstein to Alfred Hitchcock, even Abraham Lincoln and many, many others, Greg Marino was the master. He would often forge hundreds of pieces of memorabilia a day. And that was just one forger of many.

Since Operation Bullpen, the industry has implemented authentication procedures whereby an “authenticator” would witness a signature and place an “authentication” sticker on the item or provide some other form of “authentication” certificate. Not surprisingly, fake authentication stickers and certificates have been popping up with forged items, somewhat akin to fake provenances for artworks.

I (Matt) have a friend, let’s call him Barney, who used to go to baseball card conventions and collect signatures of the players who would ask $10 or so to sign a baseball. He got Ted Williams, Dom DiMaggio, Jim Rice, and Carl Yastrzemski for me. There’s no “authentication” sticker, as none were available at the time, but I completely trust Barney; we grew up together.

Signature analysis experts could easily spot a crude forgery, but what about more masterful forgeries, like one by Greg Marino? We do feel that signature analysis is likely more scientific than art connoisseurship, but how can anyone really be sure that any signed collectible is authentic?

Altered and Counterfeit Cards.

In addition to bagging multiple signature forgers, Operation Bullpen dismantled two counterfeiting card rings.

The most famous altered card incident is the subject of a book, The Card: Collectors, Con Men, and the True Story of History’s Most Desired Baseball Card (William Morrow, 2007) by New York Daily News reporters Michael O’Keefe and Teri Thompson. The book focuses on one of the world’s most expensive baseball cards, a 1909 T206 Honus Wagner. Only about 50 of such cards are known to exist, and most of them look like they’ve been around for a century. But one had sharp corners and appeared to have withstood the effects of time. It fetched a price of $2.8 million in 2007. It turns out that a sports memorabilia dealer had trimmed the edges to make the card appear as if it was pristinely preserved, and it worked…until he finally got caught.

Recently, altering of sports trading cards caught the attention of the FBI, who identified hundreds of cards sold for a combined $1.4 million, which were allegedly retouched or otherwise improperly modified by “card doctors.”

The investigation also focused on Professional Sports Authenticator (PSA), the largest sports card grading company, on whom collectors rely to help determine the condition of cards, which has a major effect on a card’s market value. PSA is currently a defendant in a class action lawsuit.

Fake Game‐Worn Items.

Fake game‐worn sports jerseys and equipment is another area of rampant fraud in the collectibles market. In 2012, a Florida man was convicted on federal fraud charges for passing off replica sports jerseys as game‐used. He would add patches and other identifiable marks so that they would look like professional athletes had worn them in games.

More recently, in 2018, New York Giants quarterback Eli Manning settled a civil lawsuit, which alleged that he was pawning off non‐game‐used equipment as game‐used. Game‐used helmets and jerseys have a distinctly higher value due to their scarcity and historical significance. Manning had entered into a deal with Steiner Sports, a well‐known sports memorabilia company, who wanted Manning to provide two game‐used helmets and jerseys. Manning then allegedly sent an email to the Giants equipment manager, asking him to send Steiner Sports “two helmets that can pass as game‐used.”

Degradation

Many collectibles are also subject to the travails of time, degrading over the years. There’s even an entire industry of grading collectibles, particularly sports trading cards and comic books. Ultraviolet light, humidity, and even oxygen can have deleterious effects on collectibles of all kinds, not to mention handling of the collectible or the occasional accident. Although there are means to slow the aging process and provide some protection, a minute percentage of collectibles can be found in pristine condition.

As a collectible degrades, so does its value.

Digital Art Before NFTs

As discussed earlier, digital art is art that exists in a digital medium, such as an image or video. As the music industry frustratingly discovered, digital files can be copied and sent throughout cyberspace without any loss of quality. After a decade of figuring out what to do, the music industry developed digital rights management (DRM) techniques to slow the pervasive copying of songs in digital (mainly MP3) format. Streaming services such as Spotify were developed, as well as novel forms of royalties to monetize these new music distribution technologies.

Large stock photo, video, and clip art houses vigorously attempt to protect the work in their catalogs as well. They engage companies with software that crawls the web, searching for copies of images in their clients’ catalogs. If you’re a blogger or you posted a picture that you found on your website, you may have received a threatening email from one of these companies asking that you pay a license fee. How effective this is we’re not sure, but some people probably pay, and others probably just remove the offending image.

But what about digital artists, the vast majority of whom are independent? They don’t have the means to enforce their copyrights across the Internet. It’s a gargantuan task for an individual. And how could you even sell, or rather, who would buy, a digital art piece if anyone can just copy and share it? We suppose that the artist could print it out and sell it. But then it’s not digital art anymore, and you’re dealing with the fraud‐ridden art world. Out of the frying pan and into the fire.

The True Advantage of NFTs

NFTs solve the major problems plaguing traditional art and collectibles—authenticity and provenance—and they provide several other advantages as well.

Authenticity

Unlike the fine art world, NFTs don’t require experts akin to dime‐store psychics summoning the spirit of the artist to tell them whether he or she painted a particular piece. The authenticity of an NFT is verified by the blockchain.

As discussed, an NFT is a smart contract, and each smart contract, like a blockchain wallet, has its own address. In the case of an Ethereum‐based NFT, the NFT’s smart contract has a 42‐character Ethereum address. Anyone can go to a block explorer, enter an NFT’s address into the search bar, and easily find the NFT’s smart contract. Additionally, the block explorer will show the address that originated the NFT. If the smart contract address matches the artist’s (or other known creator’s) address, the NFT is authentic. If it doesn’t match, the NFT is not authentic and is not from the purported artist or another known creator. That’s it. No uncertainty, no “experts,” and no hocus pocus.

On marketplaces, such as OpenSea, you can also verify who created the NFT. On an NFT’s page, just scroll down to the Trading History section and scroll all the way down in that section to see who created the NFT. If that is the verified name or address of the artist (or another known creator), then the NFT is authentic.

Provenance

NFTs have built‐in provenance, a chain of title from the creator to the current owner. In fact, chain of title is the basis of blockchain verification, which applies to all cryptocurrencies.

As we discussed in Chapter 2, each transaction on the blockchain must be verified. Let’s discuss in some detail how the validation process works.

A blockchain is a decentralized network, meaning that there is not one central authority or location of a blockchain (see Figure 3.1). There are multiple (thousands in some cases) copies of the blockchain (the list of all transactions) on different computers in different geographic locations worldwide.

Each copy of the blockchain is maintained by different people or groups. Each one of the computers in the network is referred to as a node. All nodes are constantly syncing with each other through a decentralized peer‐to‐peer network to maintain the integrity of the transaction data.

FIGURE 3.1 A centralized versus decentralized system

Miners or validators earn (or win) the right to validate transactions in a block. This is determined by the proof‐of‐work or proof‐of‐stake method, discussed later in the chapter. The validator must determine if the address sending the cryptocurrency actually has that amount of cryptocurrency to send. This is done by going up the chain: the sending address received the cryptocurrency from wallet B, which received it from wallet C, which received it from wallet D, and so forth, up to the latest verified block, which, in effect, validates the transaction all the way to the first block (the genesis block) of the blockchain.

Similarly, every owner (original, interim, and current) and transaction of an NFT is recorded on the blockchain. So, when you do a search of an NFT’s address on a block explorer or check the trading history on a marketplace, you will see the NFT’s creator, each successive owner, and the dates and amounts (in cryptocurrency) of each transaction. Such transactions are immutable (once they’re confirmed on the blockchain), as is the nature of blockchain, providing an ironclad chain of title or provenance.

Permanence

The blockchain also provides permanence. Unlike physical collectibles, NFTs will not degrade over time, nor can they be accidentally damaged or destroyed. They can theoretically remain in pristine condition forever.

However, like physical art and collectibles, the owner of an NFT can intentionally and permanently destroy it. This process is known as burning in the crypto space. Why would someone burn art that they own? We don’t know, but you should be aware that it can be done.

Scarcity

It would be nice if you could copy the Bitcoin in your wallet so that you would have double the amount of Bitcoin, wouldn’t it? Well, obviously that can’t be done. Bitcoin or any other cryptocurrency, or any currency for that matter, would be meaningless if anyone could just copy it. I (Matt) remember back when at the video arcade in the mall, a kid fed photocopied dollars into the change machine to get real quarters. The Secret Service came down on him hard. Creating counterfeit currency is a serious offense, as it should be, to maintain the currency’s integrity.

Just as you can’t copy Bitcoins, or any other cryptocurrency, you can’t copy NFTs. After all, as we discussed, an NFT is a cryptocurrency, with a supply of 1. Thus, the scarcity of an NFT is ensured by the blockchain.

The scarcity, along with the authenticity of NFTs, makes it possible for artists to sell digital artwork without having to worry about unauthorized or fraudulent originals. It opens up an entire new market for digital artists and digital collectible creators—a market that never existed before—and one that is generating millions of dollars.

Ongoing Royalty for Creators

When a painter sells a painting, all the painter gets is the amount of money the painting sold for. When that painting is later sold to the next buyer, possibly for 10 times, 100 times, or even more, than the amount of the original sale, the artist receives no part of that secondary sale or any sales thereafter. There is no continuing royalty to a painter or other means for a painter to profit from the increased value of his or her work (other than to paint new paintings).

In addition to creating a whole new market for digital art and collectibles, NFTs can contain a continuing royalty, so artists and other creators can also share in future sales of their art. And artists don’t need to invoice for it, track down the purchaser, go through a third party, or wait six months to receive it. The royalty is automatically sent to the artist’s cryptocurrency wallet.

Note that ongoing royalties are guaranteed only if the NFT is sold on the same marketplace on which it was created. The ongoing royalty may not be paid if the NFT is sold on a different marketplace.

Advantages of a Decentralized System

NFTs, with their foundation on blockchain technology, benefit from the advantages inherent in a decentralized system.

No Single Point of Failure.

Centralized transaction systems consist of a database and verification process that runs through one single location or central authority. For example, even though banks have several locations, they are centralized systems. A bank controls its own database and verifies all transactions in and out of the accounts held at the bank.

The problem with a centralized system occurs when there is a breach or hack. In such a case, the hacker is able to gain access to all of the records in the database and either steal sensitive data or even potentially alter data records. For example, in 2019, someone hacked into the Capital One database and obtained the personal data of more than 100 million people. The main problem here is that there was only one place that the hacker needed to attack to get into the database.

With a decentralized system, there isn’t one point of failure that will allow an attacker access to alter the database. If an attacker is able to access one of the Bitcoin nodes and attempts to alter previous transactions or add new fake transactions to the blockchain, the other nodes will recognize these as aberrant, and they will be rejected by the remainder of the network.

No Single Controlling Authority.

With a single controlling authority, again such as a bank, the bank (subject to certain government regulations) has full control of the database and how it’s managed. Additionally, the bank has full control (once again, subject to certain government regulations) of how it conducts transactions. For example, you may have a check that you deposit put on hold for a period of time. The bank determines the length of the hold, and it can even extend that hold. Good luck trying to get those funds sooner.

As mentioned, with a decentralized system, no centralized authority controls it. In addition to all transactions being verified and processed in the same manner, you are not subject to the vagaries and whims of a controlling authority. More importantly, without a controlling authority, you actually have 100 percent total control of your funds. Only you, and no one else, can do anything with your funds (assuming that you have securely protected your password and private key, so your wallet does not get hacked).

Trustless Transactions.

In the “old days,” transactions were conducted in person by barter—I will exchange these goods with you for those goods. We really don’t need to trust each other, as it’s a simultaneous exchange, and we each have a chance to inspect the other’s goods prior to the exchange.

Later, when currency was developed, trust entered the picture. When purchasing goods with currency, the exchange is pretty much the same. I give you cash (or whatever is the pertinent currency) for goods. Now the seller has to be concerned that the currency is real (not counterfeit), that it has value, and that it will maintain its value (at least until the time the seller uses it to purchase some other goods or service).

Regarding whether the currency is real, the seller needs to trust me. To a greater extent, however, the seller must have the ability to detect whether the currency is counterfeit, as well as trust the government or other authority to enforce the counterfeiting laws vigorously in order to discourage attempts to pass counterfeit currency. Thus enters a third party into the transaction as far as trust is concerned: the governing body.

As commerce increased, people began transacting remotely, which required one or more trusted intermediaries to make payments. At first, it was a courier who would personally deliver funds. Now we have an advanced banking system. For example, if you wrote a check and mailed it to me, I would present it to my bank, which would then present it to your bank to see if the funds in your account are sufficient to cover the check. If yes, the funds would be sent from your bank to my bank, which would then credit my account. Obviously, in this scenario, the banks are acting as trusted intermediaries.

Now let’s say that you are purchasing something online. The trusted intermediaries would be your credit card company, the seller’s merchant bank (the bank that processes credit card transactions), and the seller’s bank.

The problem with trusted intermediaries is that sometimes that trust is betrayed either intentionally or unintentionally. How trustworthy are these trusted intermediaries? Let’s use banks again as an example.

Aside from all of the fees and charges, banks are capable of making errors. Such errors include processing errors resulting in an incorrect amount of funds in your account, transactions you didn’t authorize, and additional fees or charges that should not have been charged.

If you’ve ever played the game Monopoly, you may recall the Community Chest card “Bank Error in Your Favor. Collect $200.” That’s great! If this happens to you in real life, however, and you spend it, you could “Go Directly to Jail.” Seriously. If the bank error is not in your favor, you have only a certain time within which to notify the bank about it, and good luck trying to get it corrected without a major headache.

And then there’s the Wells Fargo scandal in 2016, where bank executives put pressure on their employees to increase sales and revenue to meet aggressive quotas. These Wells Fargo employees then intentionally created millions of new accounts for customers without their knowledge or consent, resulting in new fees to these customers for something they never initiated or wanted.

How safe is your money in the bank? Under a fractional reserve banking system, banks can loan out a vast majority of their depositors’ funds, keeping only a small fraction to cover customer withdrawals. This generally works, until multiple customers want to withdraw their funds simultaneously, causing a bank run. To prevent this, you may be restricted in the amount and frequency of withdrawals.

We often hear the phrase “too big to fail” when it comes to the big banks, but that’s only because the government bailed them out. There could certainly be another financial crisis like we had in the United States in 2008. Will the banks still be too big to fail? If not, luckily the Federal Deposit Insurance Corporation (FDIC) should provide you up to $250,000 in coverage. How long it may take to receive your funds, we do not know. If you have an amount greater than $250,000 in the bank, good luck with that. The amount that you have on deposit in excess of FDIC coverage may be subject to bail‐ins. Instead of receiving a government bailout, a bank may use; that is, take your money to keep itself afloat. This actually happened in Cypress in 2013. Uninsured depositors in the Bank of Cypress lost a substantial portion of their deposited funds.

The funds in your bank account can also be subject to liens and attachments and can be frozen or even seized. Banks can freeze your account even if you’ve done nothing wrong, just by declaring that your banking activity is “suspicious.”

Given this, how much control do you really have over your funds? Look, we’re not here to pooh‐pooh the banks, which provide valuable services and keep our economy in motion. We’re merely pointing out the issues relevant to centralized systems.

Now imagine remote transactions without the need for intermediaries. I can send currency on a blockchain directly to you. I don’t have to trust you, you don’t have to trust me, and more importantly, we don’t have to trust or even deal with an intermediary. It is true that miners and validators must process blockchain transactions, but the processing is done programmatically in accordance with the rules and protocols set out in the blockchain’s particular software, without human intervention. It may not seem like a big deal on the face of it, but sending funds with no courier, no bank, or no intermediary is quite a breakthrough.

Additionally, you are in full control of the funds that you hold on the blockchain in your blockchain wallet. They are not subject to onerous rules; do not incur fees; are not subject to potential error (unless it’s your own human error); are 100 percent available (not subject to fractional reserve limitations or bank runs); cannot be subject to involuntary liens, other encumbrances, or seizure; and can’t be subjected to bail‐ins. As long as you are in full control of your wallet and you secure your private key, the funds are 100 percent yours. In Chapter 6, “Creating and Minting NFTs,” we’ll go into how to obtain and secure a cryptocurrency wallet.

One caveat to the foregoing is that if you want to have 100 percent control of your cryptocurrencies and other crypto assets, such as NFTs, they must be held in an independent wallet, not a wallet on a cryptocurrency exchange. For example, if your Ethereum is in your Coinbase wallet, it’s not unlike having money in a bank. Another caveat is that crypto may be subject to government regulation, or it may even be banned. Many countries have instituted bans on various types of cryptocurrency transactions, such as China and Turkey, or have even completely banned it, such as in Bolivia and Nepal.

Speed.

Let’s say someone in Italy wanted to send money to someone in the United States. They could mail a check, which would take some time, and of course there would be the time (probably days or even weeks) it would take for the check to clear. Alternatively, a much quicker method would be to use a bank wire sent through the Society for Worldwide Interbank Financial Telecommunications (SWIFT) system, which is a network of more than 11,000 banks and financial institutions around the world. On average, international wire transfers take two or more business days to complete. Since it’s all electronic, why? Is the money taking a cruise across the Atlantic? On top of this, you’re going to be hit with a sizable international wire transfer fee.

Instead, the person in Italy can send cryptocurrency to the person in the United States virtually instantaneously. The exact amount of time can vary depending on several factors, such as the actual cryptocurrency being used, network congestion (due to transaction volume), and in some cases, such as Ethereum, the “gas” fee you pay. We’ll go more into gas fees later in this chapter.

Generally, a cryptocurrency transaction will take between a few seconds and several minutes, although it may take longer for some receiving entities to consider a transaction final. For example, Coinbase requires three confirmations before considering a Bitcoin transaction final. Confirmations are the number of blocks added to the blockchain after the transaction was initiated. The more blocks that are added, the more secure the transaction. Since Bitcoin blocks are added to the blockchain around every 10 minutes, a Bitcoin transaction sent to Coinbase will be pending for about half an hour.

Cost.

Transaction costs for blockchain transactions are also (most likely) going to be less than an international wire transfer fee. Litecoin, a coin based on Bitcoin technology, has very low fees. On the other hand, Ethereum gas fees have been rising lately and can be excessive at times. This is a consequence of the increasing popularity and use of Ethereum (not in small part due to NFTs). The more transactions that need to be processed, the higher the demand and the higher the gas fee. Ethereum gas fees and other cryptocurrency network fees go to the validators—the ones who run the validator nodes that process transactions.

Anonymity.

Many people tout blockchain as providing anonymity. Because you transact on the blockchain with your address and not your name or other identifying information, it would seem that you’re anonymous. But is this really the case? Blockchains are public ledgers. Anyone can see any transaction or the holdings of any particular address. For example, if it’s an Ethereum address, someone could see all of the different tokens that you’re holding at that address, the amount of each token, when particular amounts of these tokens were received by or sent from that address, and in what amounts. Note that your cryptocurrency addresses are contained within a cryptocurrency wallet, which is an app that allows you to securely store, send, and receive cryptocurrency and NFTs. We’ll go more into wallets, and even guide you on how to create one, in Chapter 6.

Searching transactions and addresses can easily be done by means of a blockchain explorer, often just referred to as a block explorer, a website where you can search particular transactions and addresses, as well as view all kinds of current data pertaining to the blockchain. For example, for the Ethereum blockchain, there’s Etherscan (etherscan.io) and Ethplorer (ethplorer.io). Just enter an address or transaction hash (ID) into the search bar. So, if someone knows that a particular address is your address, then they can know what you’re holding and what transactions you’ve made, but just for that particular address.

If you purchase cryptocurrency on an exchange, such as Coinbase, the exchange knows who you are. Any transactions originating from the exchange can be traced back to you, including further transactions that you make. For example, if you buy ETH on Coinbase, send it to your MetaMask wallet, convert it to WETH, and then buy an NFT on OpenSea, all of these transactions can be traced back to your original purchase on Coinbase. Then, Coinbase (and any party with whom Coinbase shared such information, for example, the government) would know that it’s you who made all of these transactions and who owns that NFT. Not particularly anonymous, is it? Now there are ways to become more anonymous on the blockchain, but they are beyond the scope of this book. By the way, don’t worry if the previous process completely baffled you; we’ll go over it in detail in Chapter 7, “Selling NFTs.”

Limits on Inflation.

A country’s government, in conjunction with their central bank, is responsible for maintaining the value of the currency, whether the currency is backed by (exchangeable for) gold, silver, or other commodity or, as in the case of the U.S. dollar, the full faith and credit of the U.S. government. The U.S. dollar is a fiat currency, meaning that it is not backed by a commodity or precious metal. As with any fiat currency, the supply can be continuously increased (by printing more money), thus reducing the value of the dollar and, therefore, causing inflation. Throughout history, there are also examples of hyperinflation due to the excessive printing of money, such as in the Weimar Republic in Germany and in Zimbabwe, rendering the currency virtually (or completely) worthless (see Figure 3.2).

In contrast to fiat currency, the supply of most cryptocurrencies is limited. Such a limit is inscribed in the initial programming code under which the cryptocurrency was created and cannot be altered. For example, the maximum supply of Bitcoin is 21,000,000. Once that amount has been reached, no more will be minted. As of the time of this writing, the current supply of Bitcoin is approximately 18.69 million. Each time a miner successfully completes a block, they get a reward, known as a block reward, which is currently 6.25 bitcoins (BTC). Every 210,000 blocks, approximately every four years, the block reward is cut in half. Therefore, it is estimated that Bitcoin won’t reach the maximum supply until the year 2140.

FIGURE 3.2 Zimbabwe 100 trillion‐dollar bill

As mentioned, not all cryptocurrencies have a maximum supply. One example is Ethereum (ETH), the second most popular cryptocurrency. Currently, for every block, only 2 ETH are added to the circulating supply, which as of this writing is approximately 115.6 million. Given the rising demand for Ethereum, especially in connection with NFTs and other uses, any inflationary effects are minimal. The same goes for other cryptocurrencies that have not reached their maximum supply. Of course, once those cryptocurrencies achieve maximum supply, inflation will henceforth be zero. The main takeaway is that the value of a cryptocurrency can’t be inflated away by the fiat of a governing body.

As discussed, NFTs, each technically being its own cryptocurrency, have a supply of 1, which is also their maximum supply. Note that, as mentioned earlier, it’s possible for an NFT to have a supply of greater than 1.

NFTs Aren’t Perfect

Given all of the advantages of NFTs over traditional artwork, collectibles, and other assets, NFTs are here to stay. NFTs provide an excellent medium for verifying authenticity and ownership, as well as the other functionality that we discussed. However, although NFTs may be touted by some as the perfect solution, in reality, NFTs are not perfect. They have several drawbacks that need to be addressed.

Gas Fees

When we talk about gas fees with respect to NFTs, we’re not talking about the price at the pump when you fill your car. We’re talking about transaction fees on the Ethereum network, which are known as gas fees, or simply gas. Not unlike the gas at the pump, gas fees have risen recently and are starting to get out of control and become a deterrent.

Gas fees go to the miners (validators) who process transactions on the Ethereum network. The amount of gas required for a certain transaction is based on two main factors. First, gas is based on the type of transaction. More precisely, the gas fee is based on the amount of computational power required to execute the operation. If it’s a simple transfer of cryptocurrency, such as ETH, another token, or an NFT from one wallet to the next, the gas fee will be lower. If you’re deploying a lengthy smart contract to the network, the gas fee will be significantly higher.

The second factor affecting the gas fee is network volume (sometimes referred to as congestion). The higher the volume, the more demand is created, which drives up the price of gas. Think of it like surge pricing on the Uber app during busy times. Due to a resurgence in crypto, in no small part because of the growing interest in NFTs, the number of transactions on the Ethereum network has been rising, along with Ethereum’s popularity and price. For now, it seems that the old days of cheap gas are over.

Although rising, the volume on the Ethereum network is not continuously rising at a steady pace. The volume on the network fluctuates minute by minute, second by second, so the gas price is constantly in flux. One day the gas price for a particular transaction may be $30, while just a day later it could be $60, or more.

You may have an option, depending on from where you’re originating the transaction, to choose a level of gas. For example, if you’re sending crypto from a MetaMask wallet (we’ll get more into this in Chapter 7), you can choose a level of gas corresponding to the desired speed of the transaction: Slow, Average, or Fast (see Figure 3.3). Note that for any given type of transaction, the miners are going to prioritize the transactions depending on their respective gas fees. If you select Slow, you could be waiting for hours.

FIGURE 3.3 Choice of gas fee presented in the MetaMask wallet

Even though you may be able to make a selection, there are no guarantees on how long the transaction will take. If you select Fast, the transaction will most likely occur relatively instantaneously. If you select Average, the transaction will usually take a few to several minutes. However, gas prices may have gone up between the time you initiated the transaction and the time you confirm it. In such a case, the Average gas selected will be low and may take longer than expected—potentially a lot longer.

Hopefully soon, high gas fees will be a thing of the past. The Ethereum network is currently undergoing an upgrade, called Eth2 (or Eth 2.0). One result of this upgrade will greatly reduce gas fees, among other improvements. From the Ethereum.org website:

“Eth2 refers to a set of interconnected upgrades that will make Ethereum more scalable, more secure, and more sustainable. These upgrades are being built by multiple teams from across the Ethereum ecosystem.”

Other Blockchains.

Keep in mind that Ethereum isn’t the only blockchain that supports NFTs. As mentioned earlier, other popular blockchains that feature NFTs are WAX, FLOW, Tron, and the Binance Smart Chain, among others. These blockchains have considerably lower transaction fees compared to Ethereum’s gas fees, which is why they’re growing in popularity.

The reason why these other chains have lower transaction fees is because they use a less resource‐intensive method for determining who validates transactions. Blockchains such as Ethereum and Bitcoin use proof of work, which means that miners race to solve complex cryptographic puzzles (hence the name cryptocurrency). The miner who solves it wins the opportunity to validate the latest block of transactions and earn the block reward. Trying to solve these puzzles requires massive amounts of processing power (known as hash power), so the more hash power you have, the higher your chances are of solving the puzzle. Also, the difficulty of these puzzles increases as the total amount of hash power on the network increases, requiring even more hash power to solve. The reason why the difficulty increases is to maintain a time period between blocks of approximately 10 minutes.

The other blockchains mentioned earlier use proof of stake to determine who validates the blocks. Basically, the more of a certain coin a validator owns, WAX for example, the higher the chance the validator has of being chosen to validate a block. Since there are no cryptographic puzzles to solve, there’s no need for wasted processing power, and thus the fees are significantly lower. As part of Eth2 discussed earlier, Ethereum plans to change to proof of stake, which would drastically lower transaction fees.

Sidechains.

Another way to reduce gas fees is through the use of a sidechain, which is a separate secondary blockchain that’s connected to the main blockchain. A sidechain allows tokens to be used on the secondary blockchain (one with little or no transaction fees), with the ability to move tokens back to the main blockchain when necessary. For example, at a particular NFT marketplace, you could mint multiple NFTs gas‐free on a sidechain and only pay gas when the NFTs are sent to the Ethereum blockchain when you sell or transfer an NFT.

So, although gas fees may be an issue at present, there are measures in place to reduce gas fees, and proof‐of‐stake blockchains have significantly lower fees. When Ethereum switches to proof of stake, high gas fees may be a thing of the past.

Content Storage

Say you bought a digital art NFT that you love. The NFT’s main content, the reason why you bought the NFT, is a really cool abstract video. The blockchain confirms that the NFT was created by the artist and that you now own it. But where exactly is your NFT’s content? And more importantly, how safe is it?

We talked earlier about how the NFT is on the blockchain, but its content is not. The NFT is permanent so long as the blockchain continues to exist, but its content may not be. We touched on the two main solutions for off‐chain storage of NFT content: a trusted cloud storage provider and the IPFS.

The IPFS is the preferred storage solution because it is decentralized; content is stored across multiple locations. So long as the network continues to be supported (and there are all indications that it will be), the content should be safe. Other decentralized storage solutions, such as Arweave, have also come to the scene.

Trusted cloud storage providers, such as AWS and Google Cloud, are also exceptional solutions. However, the content will be hosted only so long as the organization paying the cloud storage fees continues to do so. If the NFT was minted on one of the major marketplaces, this probably won’t be an issue, but you never know. For whatever reason, the marketplace could go belly‐up. It could happen—then what would become of your NFT’s content?

Someone, an individual artist, for example, could also mint an NFT on their own (not on a marketplace) and store the NFT’s content on a private server. If that server goes offline permanently, your NFT content is toast.

These scenarios go against one of the major advantages of blockchains discussed earlier—no need for trusted third parties. That’s in essence the whole foundation upon which blockchain was invented—to provide trustless peer‐to‐peer transactions. Because an NFT’s content does not reside on the blockchain and a third party must be relied upon to store and preserve its content (often the main content), NFTs are not true blockchain assets. Decentralized solutions such as the IPFS are most akin to blockchains, but marketplaces may find it cheaper and easier to store files on a trusted centralized storage platform, instead of running IPFS nodes.

Content storage is particularly an issue with respect to unlockable content. As mentioned earlier, on OpenSea, for example, you can only include text as unlockable content, not image or video files. So, if an NFT minted on OpenSea has an image or video as unlockable content, then the creator has to provide a link to the image or video, which is hosted somewhere on the Internet. It’s not likely that your average typical digital artist will be using AWS or another trusted cloud storage provider or the IPFS. More likely, the image or video will be on some website or maybe on Dropbox (a more personal cloud storage provider). But what happens if the artist no longer maintains the website or continues to host it or no longer continues his or her Dropbox account? The image or video would be gone.

Imposters

Just as scammers like to imitate Telegram admins and others, scammers could also imitate a particular NFT artist or other NFT source. In a marketplace, it’s important to make sure that the collection from which you’re buying an NFT is validated, which is represented by a blue check mark or something similar. Again, the problem here is that you’re relying on a trusted third party. Actually, this isn’t necessarily a problem; it just obviates the main advantage of a blockchain as discussed earlier by having to rely on a trusted third party.

Although helpful, the validation mark is not a perfect solution. The validating marketplace could make mistakes or even be fooled into validating an imitator. Plus, how would NFT creators not on marketplaces get validated? The bottom line is, even though NFTs prove authenticity of origin, you still need to make sure that the origin is the person they claim to be.

Additional Reproductions

NFTs are unique, right? Yes, they are, and that’s a big driver of an NFT’s value. But what’s preventing the creator of an NFT from making another NFT with the same exact content: same image (or other content), name, description? Nothing, really. Let’s say that you bought an NFT, a 1 of 1, and you’re feeling good. The next day you see an identical NFT from the same creator. Now you’re not feeling so good. You thought you had a unique item and now you don’t, and you wouldn’t have paid what you did or maybe you wouldn’t have even bought the NFT at all.

Some NFTs, such as Rob Gronkowski’s “(1‐of‐1) GRONK Career Highlight Card,” say in the description that “This NFT is limited to just 1 edition and will never be minted again.” We trust Gronk and the creators of his NFTs. But what about some random artist whose NFT you like?

Claiming something is unique and then creating another identical item is fraud. Likely, the marketplace would boot an artist who did this. But you still may be stuck with an item that you thought was unique that wasn’t.

Delivery of Perks and Physical Items

As discussed earlier, an NFT’s description can contain perks, such as Rob Gronkowski’s “(1‐of‐1) GRONK Career Highlight Card” NFT. We trust that Gronk, and the company that created his NFTs, will deliver on the perks.

But what can you do if the NFT creator doesn’t deliver on the perk or physical item? You may be able to raise the issue with the marketplace on which the NFT was sold, but unfortunately there’s not much they can do, other than ban that NFT creator.

The issue here is that perks and physical items aren’t really an aspect of an NFT. Perks are more akin to a “Wait… there’s more” marketing tactic to increase the value of the NFT. And although a physical item may be the main driver of the value of the NFT, you’ll have to trust the NFT creator to deliver them, which obviates the main advantage of blockchain assets: trustless transactions.

Environmental Effects

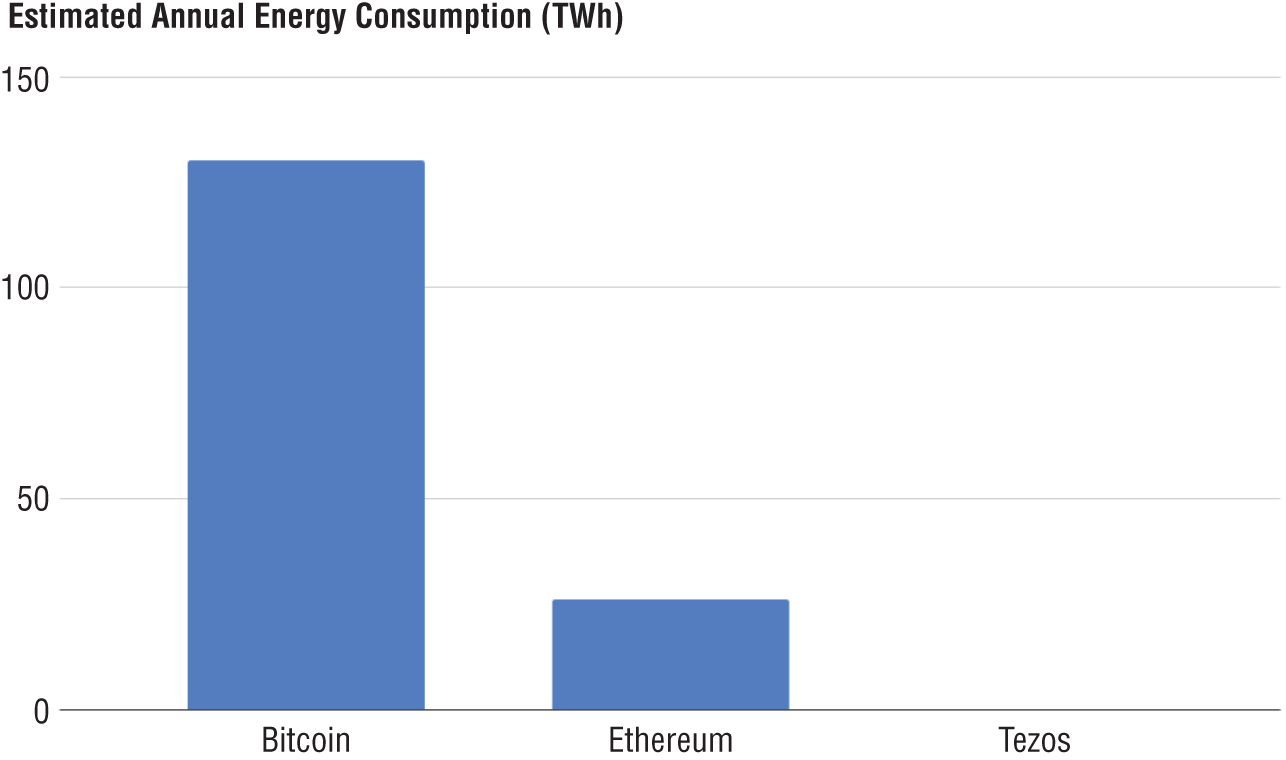

As discussed in the “Gas Fees” section, transactions on the Ethereum network, the most popular NFT blockchain, currently utilize proof of work to determine who mines a block. As mentioned, proof of work requires massive amounts of computing power, which requires immense amounts of electricity (see Figure 3.4).

If Bitcoin were a country, energy consumption‐wise it would fall between the midsize countries of Ukraine and Argentina. Ethereum would be more comparable to Ecuador. Regarding NFTs, (1) Bitcoin has nothing to do with NFTs, and (2) it is estimated that NFTs account for approximately 1 percent of the transactions on the Ethereum network. Personally, 1 percent seems a rather high estimate to us, but let’s go with it. This all boils down to an estimated average of 48 kWh per Ethereum transaction, which is less energy than the amount required to make a T‐shirt.

FIGURE 3.4 Estimated annual energy consumption of Bitcoin, Ethereum, and Tezos

Additionally, other NFT blockchains, such as WAX and Tezos, use proof of stake, which consumes 99 percent less energy than proof of work. So, although Bitcoin, Ethereum, and other proof of work blockchains on the whole consume massive amounts of energy, which may have environment effects, NFTs represent a minute portion of this energy consumption. Also, keep in mind that the Ethereum blockchain will be switching to proof of stake in the near future, so virtually all NFTs at that point will be consuming minimal amounts of energy.

Disadvantages of Blockchain

Although decentralized systems, and blockchain in particular, provide several advantages as discussed earlier, they are not perfect either. The following are the main disadvantages of Blockchain.

No Party to Which You Can Appeal.

With a decentralized system you’re pretty much on your own. If you have an issue, there’s no customer support to contact. For example, if you ordered something online with your credit card and the seller never shipped you the item, you could call your credit card company and likely get the charge reversed. Similarly, if you lose your credit card or it gets stolen, you can contact your credit card company and be protected from any fraudulent charges.

If you purchase something online with cryptocurrency and the seller doesn’t ship you the item you purchased, you’re out of luck. All cryptocurrency transfers are final and absolute. Once you send cryptocurrency, including an NFT, there’s no way to get it back, unless the person to whom you sent it sends it back to you.

This is why it’s of utmost importance only to do business with reputable parties when paying with cryptocurrency and buying NFTs. There are a lot of scammers in the crypto space, so you must be extra cautious about those to whom you send cryptocurrency and NFTs.

NFT marketplaces operate as centralized intermediaries between NFT sellers and buyers, and if an issue arises, you can reach out to them for support. However, depending on the issue, there may be little (or nothing) that they can do to help.

Personal Responsibility.

One of the trade‐offs of utilizing a system with no intermediaries is personal responsibility. You are responsible for the actions that you take on the blockchain and the resulting consequences. First, as discussed, it’s your responsibility to determine the trustworthiness of parties with whom you do business on the blockchain—do your own research (DYOR). Search for reviews, and ask questions in their telegram or other social media channels. You’re best off sticking to doing business with known, reputable companies or people. Be extremely wary of scams. If it sounds too good to be true, it probably is.

It’s incumbent upon you to keep your cryptocurrency and NFTs safe. If someone gains access to your online banking credentials and transfers money out of your account, you may be able to get that transaction reversed if you contact your bank promptly, usually within 24 hours. If someone gains access to your cryptocurrency wallet and transfers out your crypto and NFTs, you are completely out of luck. It’s your responsibility, and yours alone, to keep your wallet’s private key safe and protected so it’s much less likely to get compromised. We discuss ways to do this in Chapter 6.

Additionally, as mentioned, there are lots of scammers in the cryptocurrency world. Not only will scammers try to get you to send them cryptocurrency, but there are also ones who will ask for your private key.

Never give the private key of your wallet to anyone. Period.

There are a multitude of different kinds of cryptocurrency scams, but here are a few common ones for which you should be on the lookout:

· Imposter Websites

Scammers go to great lengths to make imposter websites look identical to the original. First, make sure that the site is secure (the address starts with https, and the lock icon appears in the address bar). Second, make sure that the domain name is exactly as it should be; no misspellings or a “0” instead of an “O.” Also, be careful when typing web addresses into a browser.

· Imposter Admins

Telegram and Discord are popular social media platforms, among others, that cryptocurrencies and NFT marketplaces use to build communities and provide updates. Some cryptocurrencies and NFT marketplaces use these platforms for customer service as well, where you can ask questions. Scammers love to pose as fake admins, with the same profile pic as a particular admin, but usually with a slightly different spelling of the username or with an extra letter or period at the end. Make sure that you are conversing with a real admin, who most likely would never ask you to send crypto or an NFT anywhere or ask for your wallet’s private key.

· Fake Mobile Apps

In addition to fake websites, scammers have been creating fake mobile apps on the Apple App Store and the Google Play Store for years, and people are still falling prey. In February 2021, for example, a person downloaded a fake Trezor app from the App Store and lost nearly all of his life savings: 17.1 Bitcoins, within a second. Apple and Google are trying to crack down, but these scammers are clever. So, make absolutely sure you’re downloading the company’s (or exchange’s or NFT marketplace’s, and so on) official app, or you may lose your crypto and/or NFTs.

· Scam Emails

Scam and phishing emails can look identical to official emails. Even the “From:” can look like a legit email address. It’s imperative that you verify the authenticity of these emails. Call up someone at the company if possible or ask an admin on the company’s pertinent social media channel. And never ever click a link in any crypto or NFT‐related email unless you are 100 percent certain of its authenticity.

These scams and tips don’t just apply to crypto. It’s just that in the crypto space, if you make a mistake, it can be devastating, and there’s no way to undo it.

Potential Hacks.

Like any other system, blockchains and blockchain‐related projects are subject to hacks. According to SlowMist Hacked, more than $14.5 billion in value has been lost to blockchain‐related hacks. In 2020, hacks occurred in three main areas:

o Decentralized applications (dApps) on the Ethereum network had 47 attacks ($437 million in losses).

o Cryptocurrency exchanges had 28 attacks ($300 million in losses).

o Blockchain wallets had numerous attacks ($3 billion in losses).

Note that these amounts are based on January 2021 cryptocurrency prices.

Your blockchain wallet, where you hold your NFTs, and even an account at a marketplace, can be hacked. In March 2021, some accounts at Nifty Gateway were hacked and thousands of dollars’ worth of NFTs were stolen. Apparently, the hack was limited to certain accounts, all of which didn’t have two‐factor authentication configured. Luckily, this particular hack wasn’t more widespread.

Your blockchain wallet is also vulnerable to being hacked if you’re not careful. In Chapters 6 and 7, we’ll show you how to protect your accounts and blockchain wallet. This is imperative, because if you get hacked, there’s nothing that you can do to get your NFTs back.

Keep in mind that tokens can be hacked directly as well. In March 2021, for example, the Paid (PAID) token smart contract was compromised, and a hacker was able to mint himself or herself nearly 60 million tokens, a significant amount of which he or she dumped on the market for a haul of $3 million (see Figure 3.5).

Luckily, the Paid team did the right thing and attempted to make as many investors as whole as possible, and the token seems to have recovered. Other projects weren’t so lucky.

Potential Attacks.

Blockchains are subject to potential 51 percent attacks. This is where a group of miners (validators) controls more than 50 percent of the mining power. In such a case, this controlling group could potentially halt transactions between some or all users or, more importantly, reverse recent transactions, allowing them to double‐spend coins. In 2018, Bitcoin Gold (BTG) was hit with a 51 percent attack that resulted in double‐spending of coins to the tune of $18 million worth.

FIGURE 3.5 Paid price chart on the day it was hacked

Abandonment.

There are a slew of blockchains that have been abandoned by their founders, otherwise known as dead coins. Projects become abandoned due to lack of funding, lack of trading volume, lack of sufficient miners or validators to process transactions, being a scam in the first place, or any combination of the preceding.

Price Volatility.

The prices of cryptocurrencies are based purely on market forces, which can lead to significant price volatility. There’s no Federal Reserve or other overseeing body setting interest rates or other policies to stabilize values. There’s often a crowd mindset with cryptocurrencies, so when a particular coin or token begins to rise, perhaps based on some positive news, fear of missing out (FOMO) may kick in, and the price rockets. At other times, if the price of a coin or token declines, perhaps based on some negative news, panic selling may kick in, and you could get rekt (blockchain‐speak for “wrecked”). Additionally, for coins and tokens with lower trading volume, it doesn’t take many trades to move the price greatly in either direction. Also, there are many crypto whales (people who own extremely large amounts of a particular coin or token) who have the potential to manipulate that coin or token’s price.

Then there are classic pump‐and‐dump schemes, where a group of people conspire to buy and heavily promote (pump) a certain coin or token. FOMO takes hold causing the price to rise, and at a usually predetermined price, the group sells (dumps) their coins or tokens at a profit, leaving others holding the bag as everyone rushes for the door.

If you’re going to be creating, selling, or buying NFTs, you’re going to be in the crypto world, so just be aware that there could (most likely will) be large cryptocurrency price fluctuations.

Now that we’ve covered all the technical reasons why digital assets and NFTs have value, let’s explore the external forces that drive the value of NFTs.

External Forces That Drive Value

Let’s begin with a question: “Why did Logan Paul’s NFTs sell for $5 million?” This story begins with a YouTuber and an uncharacteristic video that spiraled into one of the biggest NFT sales.

Logan Paul, known by most for his high‐octane YouTube videos, known by others for his foray into celebrity boxing and his fight against Floyd Mayweather, made a video in October 2020 titled Opening the $200,000 1st Edition Pokémon Box.

As with any video on YouTube, clickbait wins. And this clickbait worked! The live‐streamed video pulled in more than 300,000 live viewers and more than 11 million total views to date. The event simultaneously raised $130,000 for mental illness.

Clearly, the title piqued people’s interest. “What could possibly be contained in a $200,000 Pokémon box, and why would anyone pay that much for some images on cardboard?”

Inside each box were 36 packs of cards with each pack containing 10 Pokémon cards. But it wasn’t the collective 360 cards that buyers wanted. It was one card, or rather, one type of card they were seeking: a holographic Pokémon. These are rarer and, therefore, more valuable than their regular counterparts (and look a lot cooler too). If you’re lucky enough to pull a holographic Charizard out of a pack, you’re looking at a potential value of $350,000. Furthermore, 1st edition boxes were created more than 20 years ago, at the very beginning of the Pokémon card game, which adds to its rarity.

Obviously, the Pokémon franchise doesn’t need any help from Logan Paul in order to make sales. Pokémon tops the list of highest‐grossing media franchises in the world at approximately $100 billion in total sales, even beating out the likes of Star Wars, Mickey Mouse, and Super Mario.

Although interest in the Pokémon franchise never faded, Logan’s video amplified interest in the collectible cards and helped fuel the rage again. His video heavily influenced the resale market of these 1st edition boxes.

Following Logan’s video, the resale market for these 1st edition boxes ballooned. Anyone lucky enough to have bought one of these boxes years (or even decades) prior and never opened it was looking at a potential price tag of $300,000–$400,000. For reference, 1st edition boxes were going for around $500 in 2007.

Naturally, Logan wanted to build further on the success of his unboxing video. He did so by creating an even bigger event around his next 1st edition box opening, incorporating a public auction and NFTs.

About four months later, in February 2021, Logan announced another upcoming 1st edition Pokémon box unboxing. But this time, others could get involved in the experience and potentially cash in on the Pokémon collectibles with him.

Logan auctioned off the 36 individual packs within the box. Winning bidders would not only get the contents of the pack, but additionally would be gifted one of Logan’s “1st Break” NFTs.

This auction went swimmingly, selling packs for an average of $38,000 for a grand total above $1 million. That’s not bad ROI on the $300,000 box.

To add an additional tier for others to get involved, he listed 3,000 editions of his “Box Breaker” NFT at the price of 1 ETH each. Buyers were entered into a lottery, whereby three winners would be chosen at random to be given one of the 36 packs along with a flight to his California studio to attend the live unboxing.

Estimates show that he sold about 2,500 of these additional “lottery ticket” NFTs, and at a price of 1 ETH, he really made out like a bandit. While it’s hard to confirm the exact haul he brought in with this entire NFT drop, most estimate it at around $5 million.

The question remains: Were people buying Logan’s NFTs because of his status as a creator, and on the basis that his value in society would continue to grow, bringing the value of his NFTs with it? Or, was the price of his “Box Breaker” NFTs justified entirely by another, more popular and existing collectible, the Pokémon cards?

One can make the argument that this wasn’t truly an NFT sale, but rather a Pokémon lottery, whereby the tickets were issued and bought in the form of NFTs. And this argument becomes even stronger by the fact that all of Logan’s NFTs have plummeted in value since the initial offering. Many of the 1 ETH “Box Breaker” NFTs are being listed and sold at a tenth, or some for even one‐hundredth, of the original price.

What can we learn from this?

· Many creators are leaning into physical experiences to enhance the value of their NFTs. As discussed in Chapter 2, most NFT marketplaces allow for unlockable content or perks, such as additional physical goods to be included in the sale of the NFT. Utilizing these features can help parlay something that others already value into NFT value.

· NFT value is volatile. The technology behind NFTs, as discussed in this chapter, prevents frauds and forgeries, as well as supply manipulation. However, the demand of individual NFTs is always subject to change. And as is the case with Logan’s NFTs, when the unlockable, physical experience was used up, the price of the digital part of the NFT dropped because the assumed value was encompassed in the physical unlockable.

We tell this story to address the cross‐pollination between the traditional collectibles market and digital collectibles. The lines are still quite blurry as to whether NFT values will continue to appreciate. And for many creators jumping into the space, they’re leaning heavily on what’s worked historically in the physical collectibles space and parlaying it into a digital collectible.

In many cases, there isn’t enough demand for a person’s NFT because who really knows whether or not that demand will increase over time. Therefore, there’s no assurance that the value of the NFT will rise. This is why Logan’s pairing with Pokémon was one part genius and one part antithetical to the purpose of NFTs, which are supposed to be digital assets.

While intrinsically the technology behind NFTs is what makes them scarce and, therefore, gives them the ability to have value, there’s still no rhyme or reason as to what NFTs or which NFT creators will continue on a trajectory of high demand. As we established, collectible value is largely dependent on the demands of the market. The more people who want something, the higher the price goes.

Ideally, Logan continues to break barriers and grow as a creator (and boxer). Theoretically, his NFT collectible cards should mirror the growth of his brand. But there are still too many unknowns in the NFT market to say for sure whether NFT values will grow in parallel to the people creating and collecting them. The market will decide.