FOREWORD

Allan Meltzer, who undertakes projects that to most appear daunting, has delved deeply into the history of the Federal Reserve System, with a result that will add substantially to the discourse on the institution’s role and development. He has reviewed the records of policy discussion at an extraordinary level of detail, and his analysis illuminates the contributions of the many fascinating individuals who shaped the Federal Reserve System we know today.

Beginning with a history of developments that underlay the initiation of America’s most recent experiment in central banking, Meltzer carries the reader through the challenges of a developing institution faced with enormous economic upheaval, aptly describing the strong personalities that influenced both policy and culture in the System.

His work explores the Federal Reserve’s inadequate response to the Great Depression and the struggle for dominance in the System. According to Meltzer, the struggle did not wholly preclude agreement in times of crisis; nevertheless, the well-known exhortations of Bagehot and Thornton that a central bank must act to counter a banking crisis and currency drain without regard for the gold reserve were ignored. In Meltzer’s view, the System’s adherence to the real bills doctrine, combined with a belief that the purging of speculative excess was necessary to set the stage for price stability, led to the failure of monetary policy to lessen the decline.

The book describes in detail the roles played by Federal Reserve bank presidents, which have evolved substantially over the years, as has the relationship between the reserve banks and the Board of Governors. The early dominance of the Federal Reserve System by Benjamin Strong, governor of the Federal Reserve Bank of New York, is an interesting episode. Strong was credited more than anyone else with recognizing in the years after World War I the financial and economic impact of reserve bank purchases and sales of Treasury debt and the need to coordinate those transactions. Meltzer depicts Governor Strong’s opposition to a 1926–27 congressional proposal to amend the Federal Reserve Act to make price stability an explicit policy goal. He describes Governor Strong’s concern that the bill offered by another Mr. Strong—Kansas Republican congressman James A. Strong—would be interpreted to mandate the stability of individual prices, particularly of agricultural products. In a clear example of his willingness to take sides, Meltzer says here that had a mandate for price stability been approved, the Fed “could not have permitted the Great Depression of 1929–33 or the Great Inflation of 1965–80.”

Ultimately the Banking Act of 1935, largely adopting reforms proposed by Marriner Eccles, resulted with some subsequent refinement in the structure of the Federal Open Market Committee. Eccles had sought an FOMC wholly controlled by the Board rather than so-called private interests. However, Senator Carter Glass of Virginia and others were leery of monetary policy dominated by what they saw as “political interests.” The compromise that emerged mandated that monetary policy be conducted with a broader vision than if either Eccles or Glass had prevailed.

Meltzer’s book covers with the same methodical illumination the events of more recent years, completing a work both stimulating and provocative. Readers will have substantial material for continued reflection and discussion.

Allan Meltzer has spent a lifetime inquiring into monetary economics, and he calls the evidence as he sees it. His combination of interests and experience makes him most qualified for this undertaking, and he brings to the endeavor a closeness of analysis that makes his conclusions both fascinating and valuable. Those of us who enjoy the debates he inspires will find much satisfaction in this book, as in his other important works.

Alan Greenspan

PREFACE

The project that eventually became this book began in 1963–64, when the late Congressman Wright Patman asked me to extend a study I had done for the Joint Economic Committee. That study described operations in the dealer market for government securities—the market in which the Federal Reserve conducts its open-market operations. When I explained that the problems that concerned him arose at the Federal Reserve and not in the market, he asked me to undertake a study of the Federal Reserve.

My former teacher Karl Brunner, later my friend and lifetime collaborator, joined the project. Together we wrote a lengthy study of Federal Reserve operations, emphasizing their use of free reserves as a target and indicator of the thrust of policy. We showed that these procedures were faulty—that the Federal Reserve’s analysis did not go beyond the money market to the broader objectives required by an efficient and effective monetary policy. We proposed an alternative framework.

The late Harry G. Johnson proposed to the University of Chicago Press that it republish the study. The original studies were hastily written to meet congressional deadlines. I started to rewrite several sections but decided instead to extend the analysis. One set of questions in particular warranted attention: Why had the Federal Reserve acted as it did? Why had it failed to respond to the Great Depression or the deep recession of 1937–38? Why was monetary policy often pro-cyclical?

This book tries to answer those questions. At various times in the late 1960s and early 1970s, I began to revise the manuscript to complete the history. Karl Brunner always expressed interest, but he never devoted any time to working on the manuscript or commenting on what I had written.

In the fall of 1994 I returned to work on this book while on leave from Carnegie Mellon at Harvard University and the National Bureau of Economic Research. My thanks to Martin Feldstein for the hospitality and pleasant working conditions at the Bureau.

In the nearly thirty years since I first started on this project, both the Federal Reserve and my ideas have changed. Some of the ideas in the original study remain, but much of this material is new.

The most important influence on my thinking and conclusions has come from reading the minutes, correspondence, and other internal documents developed at the time. Records for the Federal Reserve Board and the Board of Governors became available as a result of the Freedom of Information Act in the 1970s. The cooperation of Chairman Alan Greenspan, the secretary of the Federal Open Market Committee, Normand Bernard, and the library staff went far beyond legal requirements. I am indebted to them, to Susan Vincent and Kathy Tunis at the Board of Governors library, and to Elizabeth Jones of the Board’s staff for their helpful assistance.

I began by reading all the archival material. It soon became apparent that the amount was too great for one person to summarize the material and complete the manuscript in reasonable time. Several researchers have reviewed and summarized material, collected data, and assisted in other ways. I am particularly grateful to Randolph Stempski, Sean Trende, Catherine Pharris, Matthew Korn, and Jessie Gabriel for their perseverance, diligence, and thoughtful selection of material.

To supplement their efforts, I continue to read and summarize materials at the Federal Reserve Bank of New York. The bank has collections of papers left by its governors and later presidents, Benjamin Strong, George Harrison, and Allan Sproul. These include memos, correspondence, and records of conversations. Lester Chandler used Benjamin Strong’s papers for his biography of Strong. Instead of rereading all the Strong papers, I relied on the quotations in Chandler’s biography. Where I differed on interpretation, I referred to primary sources.

The New York board of directors, or its executive committee, met weekly. The weekly minutes often have more detail than the daily minutes of the Federal Reserve Board’s meetings. The New York archives directed me to topics in the board’s records and conversely. The New York bank has been extremely helpful not only by providing access to materials but by offering pleasant working arrangements. Although not covered by the Freedom of Information Act, the bank provided materials without hesitation or restriction. I am indebted to President William McDonough for his assistance and to Rosemary Lazenby, the bank’s gracious and ever helpful archivist and her staff.

Many people read and commented on parts of the manuscript. I am grateful to all of them and particularly to Robert Aliber, Michael Bordo, Kevin Dowd, Milton Friedman, Alan Greenspan, Jerry Jordan, David Laidler, Athanasios Orphanides, Robert Rasche, and Elmus Wicker.

I owe a special debt to Anna Schwartz, who encouraged and prodded me. Anna commented fully and helpfully on each chapter from her vast store of knowledge. Bennett McCallum listened patiently at lunches over many years and commented with his usual economic insight. Alberta Ragan typed the several revisions and proofread the entire manuscript with her usual care, efficiency, and good humor.

Several readers have asked why I included the years covered in Friedman and Schwartz’s now classic monetary history. In one respect this is a strange question: in the physical sciences, replication of experiments is the norm. No one appreciates their work more than I, but its quality and importance should encourage, not deter, replication.

There are additional good reasons for revisiting the early years. First, I had unlimited access to material that they did not have. To the extent that I reach the same conclusions, as I often do, my work strengthens theirs. Where I find differences, as I sometimes do, my work supplements theirs by giving a more complete or more accurate account. Second, I am interested in some different questions, such as those listed above and others.

To answer those questions, I let the Board members, governors, presidents, and others explain their actions in their own words. Although personal animosities and indecisiveness play a role, there is a remarkable consistency in the statements and explanations. Using the earlier studies for the House Banking Committee, I develop the framework that guided many of their decisions.

The research for this book required much time in Washington, D.C., and at National Archives II in College Park, Maryland. My continuing association as a Visiting Scholar at the American Enterprise Institute was invaluable. I am greatly indebted to Christopher DeMuth for his generous hospitality and assistance and to my colleagues there, especially Douglas Besharov, for support and encouragement. I am indebted also to Dean Douglas Dunn and others at Carnegie Mellon University. They have encouraged me through more than forty years of an active life.

The Sarah Scaife Foundation, the Lynde and Harry Bradley Foundation, and the Smith Richardson Foundation have given generously to finance the project. It has taken six years to get to this point. Without their backing, it might never have happened.

My largest debt is to Marilyn, my wife, whose support, encouragement, and love have always been there during a lifetime of often hectic but always absorbing activities.

ONE

This book is the biography of an institution, the Federal Reserve System, much of it told by its principals. The Federal Reserve is now the United States’ powerful central bank. The founders did not intend to create either a central bank or a powerful institution; had they been able to foresee the future accurately, they might not have acted.

Institutions, no less than individuals, change as they mature and as the conditions that led to their creation change. In 1913 the United States was a developing country, with agriculture its largest occupation. The enormous shift in political and economic power and responsibility toward the United States that occurred in the twentieth century was at an early stage. The founders did not design or contemplate the Federal Reserve System we have today. They hoped to reduce financial instability, improve the quality of financial services, and strengthen the payments system.

The leading central banks in 1913 were privately owned institutions vested with responsibility for such public activities as providing currency, maintaining domestic payments systems and international payments, and serving as lenders of last resort in periods of financial disturbance following threat of failure by major banks or financial institutions. Depositors were not insured against these risks, so the threat of financial disruption set off a shift from bank deposits to gold or currency issued by the government. The drain of gold and currency into private hands forced multiple reductions in bank assets and liabilities and threatened additional bank failures. Interest rates on short-term loans rose with the increased demand to borrow and the reduced supply of loans.

By the late nineteenth century, central bankers in principal countries understood that their responsibility to lend at times of financial panic made them unique. Their public responsibility to prevent widespread failure of banks and financial institutions that would otherwise remain solvent had to dominate the private interests of their stockholders. Private interests would lead them to contract lending, call loans, and shrink their balance sheets. Such action would force unneeded bankruptcies and increase the risks the public had to bear.

In a well-managed panic under the gold standard, the government suspended the central bank’s requirement to pay out gold or silver on demand. Relieved of the requirement to hold a fixed percentage of the note issue in metallic reserves, the central bank could expand the currency issue to satisfy any increase in the demand for currency. Privately owned banks with good collateral could borrow from the central bank instead of calling loans, reducing deposits, and forcing economic contraction and bankruptcies. When the system worked in this way, financial panics ended quickly. The additions to currency returned to the banks as deposits. Banks repaid their loans at the central bank. As the central bank’s liabilities fell, the government could restore the requirement to pay out gold on demand.

This system of public-private cooperation, combining suspension of gold payments with a lender of last resort facility, did not survive the economic, political, and financial disturbances later in the twentieth century.1 By the 1950s, privately owned central banks had disappeared. Governments looked to public institutions to manage money and credit.

Public control of money raised a new issue or, more accurately, reopened an old one—preventing governments from abusing their power to create money and credit for temporary political advantage. After a decade or more of rising inflation, central banks became more independent of political control. By the end of the twentieth century, principal countries accepted two organizing principles—public ownership and “independence.” The latter term has many different specific meanings; their common element is limitation of the government’s power to use monetary policy to gain political advantage.

The structure of the early Federal Reserve System reflected these concerns about reconciling the public nature of the central bank’s task with responsible control of money and credit. Writers and commentators at the time did not use terms like “public goods” and “central bank independence,” but they recognized the problem of designing an organization with proper incentives. Fears that a privately owned bank would place the bank’s interest above the public interest had to be reconciled with concerns about empowering the government to control money. In addition, the new institution was supposed to provide a currency with stable value, capable of expanding and contracting in response to demand; a payments system that efficiently transferred money and cleared checks in a growing national economy; and the services of a lender of last resort.2

President Woodrow Wilson offered a solution that appeared to reconcile competing public and private interests. He proposed a public-private partnership with semiautonomous, privately funded reserve banks supervised by a public board. The directors of the twelve reserve banks, representing commercial, agricultural, industrial, and financial interests within each region, controlled each bank’s portfolio. The new rules sought to pool the country’s gold reserves to strengthen the individual parts by making the total reserve available in a crisis. Reserve banks could lend gold to other reserve banks. No formal provision required coordination or cooperation of the various parts, however. In practice this meant that if the system was to serve as a lender of last resort, it would have to coordinate the actions of the semiautonomous reserve banks.

President Wilson was proud of his achievement.

It provides a currency which expands as it is needed and contracts when it is not needed, a currency which comes into existence in response to the call of every man who can show a going business and a concrete basis for extending credit to him, however obscure or prominent he may be, however big or little his business transactions. More than that, the power to direct this system of credits is put into the hands of a public board of disinterested officers of the Government itself who can make no money out of anything they do in connection with it. No group of bankers anywhere can get control; not one part of the country can concentrate the advantages and conveniences of the system upon itself for its own selfish advantage. (Wilson as quoted in Kettl 1986, 22)

LAW AND PRACTICE

President Wilson’s compromise resolved the immediate political conflicts and established an institution, but it left major economic and organizational issues unresolved. The structure of the new system did not concentrate decision-making authority and responsibility. A struggle for power and control broke out early and continued until resolved by the Banking Act of 1935.

Although the Federal Reserve was an independent agency from the start, in practice two political appointees—the secretary of the treasury and the comptroller of the currency—served as ex officio members of its board, with the secretary as board chairman.3 Before the 1930s, treasury secretaries rarely participated actively.

The 1935 act resolved this organizational anomaly by removing the secretary and the comptroller from the Federal Reserve Board. By that time the secretary took an active part in monetary policy and often influenced decisions. The legal change did not change the locus of decision-making power. The Treasury retained its strong influence until 1951.

The 1913 legislation did not ensure that the new system would respond to crises better than the old. On the recommendation of the officers, or on their own initiative, the directors of individual reserve banks could decide not to participate in System operations. The officers who headed the reserve banks were mainly bankers, the same types of individuals that had run banks or clearinghouses in the past. A change of location to the reserve banks was not enough to ensure that concern for financial stability would outweigh other interests. Some did not recognize that the lender of last resort had to place the interests of the financial system above the interests of the individual reserve banks.

Institutions both shape the society of which they are part and adapt to the dominant views in that society. Although the Federal Reserve was independent of the day-to-day political process, the public, acting through its representatives, could insist on structural changes or, without formally changing structures, demand that the Federal Reserve undertake new responsibilities or give up old ones. No institution can be independent of this pressure for change.

In the 1920s the reserve banks learned to coordinate actions that affected interest rates and the stocks of money and credit. A committee, led by the New York reserve bank, took responsibility for securities purchases and sales. The reserve banks adopted a formula for allocating the System’s portfolio among the reserve banks. The reserve banks retained the right to reject participation.

The committee was an informal, extralegal arrangement. The Board, acting in its supervisory role, had to approve purchases and sales. The line between supervision and decision making was never clear, so the procedures irritated some Board members and became a source of friction. Friction increased as open market operations became the principal policy instrument.

The Banking Act of 1935 resolved this conflict also. Board members became members of the Federal Open Market Committee for the first time and held seven of the twelve seats and chairmanship of the committee. New York lost its leadership role. The New York bank did not regain a permanent seat on the committee until 1942. Since that time, the president of the New York bank has served as the committee’s vice chairman.

The 1935 act permanently shifted the locus of power to the Board. The Federal Reserve became a central bank. The twelve regional reserve banks lost their semiautonomous status and much of their original independence.

The history of the Federal Reserve is in part the story of how social, political, economic, and technological changes affected the institution. The Federal Reserve began operations not in the heyday of the gold standard but near its end. At the time, acceptance of the standard by bankers, economists, leading businessmen, and others, at home and abroad, was so great that the standard seemed to many the social manifestation of a natural order. The standard did not work in the smooth, orderly way that its proponents imagined, but it provided an internationally acceptable means of payment and store of value (Bordo and Schwartz 1984). Debts were settled and payments made without conflict. The movement of gold balances and their effect on domestic prices gave the standard the automaticity for which it is famous.

The gold standard required countries to use monetary policy to keep exchange rates fixed and thus to allow prices, output, and employment to vary as required by the movements of gold and the country’s exchange rate. Debtor countries had to pay their obligations in gold even if the price of gold rose relative to commodity prices, and creditors had to accept gold in settlement if commodity prices rose relative to the price of gold. Exporters and importers had reasonable certainty about the payments they would make or receive, since the rate of inflation remained bounded except in wartime, when the standard did not operate.

Efforts at international monetary coordination in the 1920s and 1930s foundered on the conflict between a fixed exchange rate and goals for inflation or employment. The Federal Reserve worked actively to restore the international gold standard in the 1920s, first in Germany, than in Britain, France, Holland, Poland, and elsewhere. It sought to maintain domestic price stability also. The two goals were incompatible once other countries fixed their currencies to gold. Coordination could not resolve the conflict. In the end, the Federal Reserve failed to achieve either its domestic or its international goal.

Again in the 1930s, Britain, France, and the United States renewed efforts to coordinate exchange rate policy. The new approach, known as the Tripartite Agreement, failed also. Countries would not subordinate domestic policy to the exchange rate goal.

The lesson drawn from these experiences by policymakers in Washington, London, and elsewhere was that previous attempts lacked effective mechanisms for enforcing coordination while achieving price stability. In 1944 the Bretton Woods Agreement sought to retain exchange rate stability as a goal of economic policy and to reconcile external and internal monetary stability. The agreement had fixed but adjustable rates in place of the rigid exchange rates under the gold standard. Countries did not have to reduce their price level to remove external imbalances. They could respond to permanent changes in competitive position by devaluing and could borrow from a central facility, the International Monetary Fund (IMF), when facing cyclical or temporary balance of payments deficits. The Fund would lend balance of payments surpluses to countries in deficit. In the early postwar years to 1951, the Fund did little. Most countries had wartime exchange controls and inconvertible currencies.

The Bretton Woods system of fixed but adjustable exchange rates, like the interwar gold exchange standard, tried to supplement the stock of gold by using foreign exchange—dollars and pounds—as reserve currencies. The two differed fundamentally. The stock of gold grew slowly; the stocks of dollars and pounds could grow without limit. Member countries accepted an obligation to treat the two alike. In practice this meant they had to accept inflation or appreciate their exchange rate.

The new system recognized a lasting change in beliefs about the responsibilities of government. As the population moved from rural to urban areas and from agriculture to manufacturing and service industries, governments assumed new responsibilities for social welfare and economic stabilization. The public in many countries would not accept the level of unemployment, deflation, or inflation needed to maintain the exchange rate. Adjusting the exchange rate seemed to be a less costly solution in 1944. At first the IMF had to approve exchange rate changes, but this restriction was not enforced.

President Wilson wanted the Federal Reserve to remain independent of government. Except for wartime and postwar subservience to the Treasury, independence developed in the early years and continued through the Harding, Coolidge, and Hoover administrations.

President Roosevelt and his treasury secretary, Henry Morgenthau, believed that the reserve banks represented bankers, many of whom opposed the president’s programs. Devaluation of the dollar in 1934 gave the Treasury the financial resources to affect interest rates by buying securities, and it did so. Also, the Treasury sterilized and desterilized gold, affecting the rate at which monetary aggregates rose.

The Federal Reserve chairman, Marriner S. Eccles, expressed concern about the Treasury’s actions but felt powerless to prevent them. And faced with relatively large gold inflows, he wanted to prevent inflation. Equally, he believed that at the interest rates prevailing during the 1930s, monetary policy could do little to stimulate expansion.

The head of the fiscal authority favored an activist monetary policy. The head of the monetary authority proposed more activist fiscal policies. Secretary Morgenthau wanted interest rates to remain low so that he could finance peacetime deficits and much larger wartime deficits. Monetary policy had the important role in his scheme of keeping market rates from rising. Eccles wanted larger budget deficits during the depression and large surpluses after the war.

Eccles, like Morgenthau, did not respect Federal Reserve independence. Although he disliked Treasury interference in monetary matters, he did little to prevent it. He advised and testified on a broad range of government policies including budget, tax, and housing policy. At times he opposed Morgenthau’s policies, and on one occasion he proposed an excess profits tax that differed from administration policy.

A most unusual breach of independence occurred in January 1951 when the entire open market committee met in President Truman’s office. The president and Secretary John Snyder wanted the Federal Reserve to maintain the long-term interest rate on Treasury bonds at the wartime peg. The president did not ask for a commitment, and the committee did not offer one. Nevertheless, meeting the president in the White House to discuss monetary policy was a long way from the tradition of independence that President Wilson had tried to foster.

IDEAS AND DECISIONS

A history of the Federal Reserve is a history of the decisions made and the ideas that prompted them. The chapters that follow allow the participants to explain their actions, and the reasons for them, in their own words. These decisions produced very different results: a steep postwar recession in 1920–21, a period of stability in the 1920s followed by the Great Depression of the 1930s and, much later, the Great Inflation of the 1970s.

The men who made these decisions were not chicane or evil. They did not directly seek the outcomes that their decisions helped to bring about. They did not fail to stop the depression because they liked the outcome and wanted it to continue. They acted as they did because of the beliefs they held about their responsibilities and about the way their actions affected the economy. Much of this history is about their reasons and their reasoning—what it was and how it changed in response to events and new ideas.

Men and women interpret events using the theories or beliefs they learned earlier. The beliefs or theories that guided the Federal Reserve were mostly mainstream beliefs at the time they were held. Individual leaders influenced decisions most effectively by introducing new or different ideas or new interpretations. Benjamin Strong in the 1920s recognized the need to replace the gold standard rules and the commercial loan theory, on which the founders based the Federal Reserve Act. Marriner Eccles believed monetary policy could do nothing in the 1930s when short-term interest rates were low, so he did nothing to lift the economy from the depression. Later he believed that the Federal Reserve did not have the political support to use general monetary policy to prevent inflation after World War II. He proposed selective credit controls to substitute for higher interest rates and slower money growth.

Individuals matter most when they are able to lead others to act in ways that do not fit comfortably within the prevailing orthodoxy. Strong led the Federal Reserve to support Britain’s return to the gold standard in 1924–25. In 1927 he lowered interest rates and expanded money to help Britain maintain the gold standard. Allan Sproul led the Federal Reserve toward independence from the Treasury in 1950–51.

These and other episodes show that leadership was important at times. Events of this kind are rare. Most policy decisions and actions apply a framework or theory based on prevailing beliefs.

This volume starts with the founding of the Federal Reserve in December 1913 and ends with the Treasury–Federal Reserve Accord in March 1951. In many respects the accord marks the beginning of a larger, and greatly changed, institution. In 1913 the United States was an emerging economy. Great Britain was the financial power and the center of the international financial system. Approximately 30 percent of the labor force worked in agriculture. By 1951 only 11 percent remained in agriculture (U.S. Department of Commerce 1966, 178–79). The United States had become the financial leader, the dominant economy, and the technological and managerial leader as well.

In 1913 the London market financed most United States exports. Since the exports included mainly agricultural products, there was a large seasonal demand for financing in the fall, so interest rates rose each fall. United States bankers wanted to replace London bankers. They believed they were at a disadvantage, since they could not discount export credits at a central bank. Politicians wanted to reduce the seasonal fluctuation in interest rates. A bank that could expand credit and reduce interest rates seasonally satisfied both groups.

Seasonal credit expansion was not the only reason for establishing the Federal Reserve. Recessions in 1893–94, 1895–97, 1899–1900, 1902–4, 1907–8, and 1910–12 averaged nineteen months, according to the National Bureau of Economic Research. In all, there were 113 months of recession from December 1895 to January 1912—55 percent of the time. Several of the recessions were severe. Financial panics, interest rates temporarily at an annual rate of 100 percent or more, financial failures, and bankruptcies were much too frequent. Other countries had a lender of last resort to ameliorate financial crises or even prevent them. The series of crises and financial panics increased support for creation of a new institution.

In the 1920s the Federal Reserve received credit for improving economic performance. It eliminated both the seasonal and the extreme changes in interest rates characteristic of financial panics. Although the economy continued to experience relatively large cyclical fluctuations and many banks failed, old-style financial panics did not return in the three recessions from 1920 through 1927.

THE ECONOMY 1913–51

In first quarter 1951, real GNP was nearly three times greater than at the start of System operations in 1914, a compound annual growth rate of 2.8 percent. Growth was far from uniform. Chart 1.1 shows the many cyclical swings. Quarterly values of annual GNP growth range from 20 percent to –20 percent, associated with war and the Great Depression, but many years show changes of 10 percent or more.

Stable growth was not part of the Federal Reserve’s formal mandate in the early years. Most of the System’s leadership would have denied any responsibility for economic activity or employment.

Chart 1.1 shows the main events and experiences that shaped the Federal Reserve and were shaped by it. Two postwar contractions followed the two wartime expansions. The three and a half years of contraction from 1929 to 1933 stand out, as do the recovery following devaluation of the dollar against gold in 1933–34 and the wartime expansions from 1941 to 1945.

Also, the price level in first quarter 1951 was approximately three times its early 1914 value. Prices rose at a compound annual rate of 2.8 percent a year. As chart 1.2 shows, wartime inflations contributed greatly to the average rate of change, so the average for the period is misleading. In both world wars, the Federal Reserve issued money, as required to support the Treasury’s interest rate policy. After increasing in response to gold inflows from 1914 to 1917, the price level fluctuated widely from 1917 to 1939 around a constant value. The price level was approximately the same in 1939 as in 1917, before the United States participated as a combatant in World War I. The price level then doubled between 1940 and 1951, a more than 6 percent annual rate of increase. Most of the increase occurred during World War II, but part of it appears after the war, when price controls ended.

In the early years, 1914–16, the Federal Reserve’s portfolio remained small. The Federal Reserve’s nongold assets were too small to offset gold inflows. Since the United States was on the gold standard the rules required higher prices, so it is not clear that a larger portfolio would have been used at the time to cancel the effect of gold flows on money and prices. Principal gold standard countries had suspended the standard during wartime, but the belligerents and others used gold to pay for imports, and some foreigners sought safety in dollar securities.

Putting aside these early years, table 1.1 summarizes outcomes in the years 1917 to 1951. The table shows that in this period the country rarely experienced price and output stability. The Treasury dominated the Federal Reserve more than half the time. The seven years of stability, 1922–29, are exceptional, not the rule.

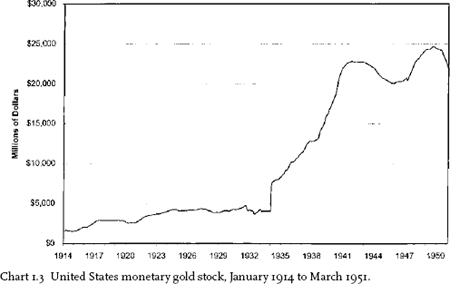

The founders of the Federal Reserve expected the new institution to follow gold standard rules. Gold movements would determine long-run price changes. Chart 1.3 shows that the stock of monetary gold rose in the 1920s, particularly from 1920 to 1925, when the dollar was the only major currency convertible into gold. Restoration of the international gold standard increased the demand for gold, contributing to the gradual fall in the United States price level after 1926. Federal Reserve officials worried that the gold flow would reverse. They were reluctant to monetize inflows or permit prices to rise. Despite the gold inflow, prices fell in the 1920s.

Chart 1.3 shows the dollar value of the monetary gold stock. The vertical line at the beginning of 1934 shows the revaluation of gold to $35 an ounce (devaluation of the dollar against gold). At the $35 price, gold flowed to the United States at a rapid rate that slowed during the 1937–38 recession but accelerated after the recession as Europe moved toward war.

The monetary gold stock increased nearly eightfold during the thirtyseven-year period, using troy ounces to abstract from the 1934 revaluation. At its start in late 1914, the Federal Reserve held 74 million ounces of gold, valued at $1.5 billion. After 1934 United States citizens and corporations could not own gold. Only the Treasury held gold. At the peak in 1949 the Treasury held more than 700 million troy ounces, valued at over $24 billion.

The main contribution to this growth came between 1934 and 1939, following the revaluation. The rising gold stock was the dominant force increasing money and credit, keeping nominal interest rates low, and promoting economic expansion with modest inflation. Rising income, rising stock prices, low inflation, and concerns about a European war sustained the gold inflow until 1941.

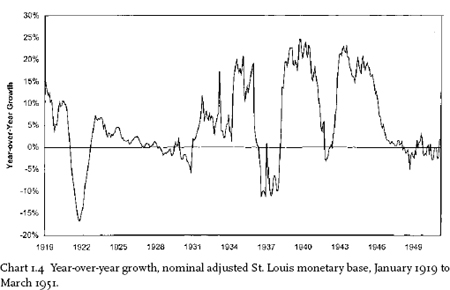

Potential inflation, driven by gold inflows, was the Federal Reserve’s main concern in the 1930s. Gold certificates representing the monetary gold stock became the largest asset on the System’s balance sheet. Bank reserves rose rapidly; banks held large stocks of excess reserves. As in 1914–17, the Federal Reserve was concerned that its nongold assets were too small to counter the inflationary effects of the gold inflow. In 1936 it persuaded the Treasury to sterilize the gold inflow, ending the increase in reserves. And at about the same time, it used its newly acquired power to double reserve requirement ratios over a nine-month period in 1936–37. These actions contributed to a new, severe recession in 1937–38.

Chart 1.4 shows the sudden reduction in monetary base growth in 1936–37 resulting from these policy errors. The rate of base growth fell from 19 percent in December 1935 to –11 percent a year later. As Chart 1.4 shows, the reversal, when it came, was just as sudden and sharp. The Federal Reserve reversed part of the increase in reserve requirement ratios, and the Treasury stopped sterilizing gold inflows. The only declines comparable to the 1937 experience came in 1920–21 and in 1946. Both contributed to severe postwar recessions.

The monetary base is the amount of reserves and currency supplied by the Federal Reserve.4 The principal counterparts or sources of the base are gold and Federal Reserve credit, the latter consisting mainly of member bank discounts and Federal Reserve purchases of government securities. Growth of the monetary base shows the monetary actions that the Federal Reserve permits or takes.

The data in chart 1.4 suggest the central role of monetary actions in this period. As noted, the economic contractions of 1920–21 and 1937–38 followed monetary contractions. Although committed to restoration of the gold standard in the 1920s, the Federal Reserve followed a deflationary policy that drained gold from other gold standard countries. In the first half of the 1940s, the Federal Reserve helped to finance World War II by purchasing government securities at fixed interest rates. It continued this policy after the war ended. Although the Federal Reserve complained that it had become an “engine of inflation,” the monetary base fell in the early postwar years. By late 1948 the economy was in recession with falling prices, as shown in earlier charts.

Interest rates are the more conventional way to describe monetary policy actions. Chart 1.5 shows short- and long-term interest rates for most of the period. Long-term rates decline over the entire period with brief interruptions, notably in 1931, following Britain’s departure from the gold standard. Most subsequent movements are relatively small.

Both short- and long-term rates are highest in 1920–21. This was the Federal Reserve’s first attempt to use monetary policy to control inflation. High interest rates were very unpopular with Congress and large parts of the public. The Federal Reserve did not raise rates to this level again for a generation.

Changes in short-term rates from 1922 to 1930 show the beginning of active monetary policy. Short-term rates are highest at the peak of expansions in 1923, 1926, and 1929 and lowest near business cycle troughs in 1924 and 1927. The modest reductions in interest rates in 1927 took on importance well beyond the size of the change. Under the influence of Benjamin Strong, the Federal Reserve lowered interest rates, in part to help Britain remain on the gold standard. Critics within and outside the System blamed the reduction for the subsequent stock market boom and the depression that followed.

Policy changed after 1932. With interest rates near zero, Federal Reserve officials believed that policy was “easy” and that additional monetary ease would not contribute to expansion. During World War II the short-term interest rate remained at 0.375 percent until November 1947. The Federal Reserve would not change rates without Treasury approval until the March 1951 accord.

The Treasury’s reluctance to let interest rates rise after World War II was the traditional reluctance of a large borrower to experience an increase in interest cost. The Federal Reserve had the same problem after World War I. To the treasury secretaries in both periods the debt seemed very large, and it was compared to their previous experience.

Andrew Mellon became treasury secretary after the 1920 election. During his term of office, he retired debt and reduced tax rates. Government debt declined from 34 percent to 16 percent of GNP and from $25 million to $16 million. By 1932 the debt to GNP ratio was above its wartime peak, mainly the result of a decline in GNP. Chart 1.6 shows these data.

New Deal deficits seemed large to contemporaries accustomed to Mellon’s policy and earlier peacetime policies. The chart shows that the debt to GNP ratio was approximately constant from 1933 to 1941 at about 40 percent. Wartime finance brought the debt to nearly $300 billion by the end of 1946, a peak of 129 percent of GNP. The large outstanding stock of debt raised new fears about the operation of monetary policy. A large literature claimed that higher interest rates would cause losses to creditors (debt owners) and that such losses would have severe negative effects on the economy. Arguments of this kind became popular in government, but not just in government. This literature neglected to mention either the gains that debtors received or the losses that creditors would experience if inflation resulted. The argument became part of the case against higher interest rates and an end to the wartime pegging policy.

PLAN OF THE VOLUME

Central banking institutions developed and spread in the nineteenth century. Understanding of the role of money and monetary institutions followed. Chapter 2 traces major developments in central banking and monetary theory using the work of Henry Thornton, Walter Bagehot, and Irving Fisher. If the Federal Reserve had followed the policies these authors advocated, it would have avoided the most serious and socially costly errors.

The rest of the volume divides the thirty-seven-year history into five chapters. Each chapter covers a major event and the environment in which it occurred. Chapter 3 treats the founding of the System and the early years. The conflict over political versus financial control that delayed the Federal Reserve’s founding began almost immediately. Problems of war finance soon took precedence. During the war, the Treasury’s financial demands controlled monetary policy. After the war, the Federal Reserve faced the problem of freeing itself from Treasury control. Once freed, the System raised interest rates to end inflation. It was more than successful, but at a high cost. Prices and output fell sharply in the 1920–21 recession.

The 1920–21 recession and deflation constituted an important milestone. The severe contraction was costly economically and politically. The severity of the decline raised doubts about the applicability of the operating principles in the Federal Reserve Act. Chapter 4 traces the development of a new framework and the beginning of a more activist role. Instead of depending on banks’ decisions to discount or repay borrowings, the new approach used open market operations to force banks to borrow or repay.

Open market operations required the reserve banks to work together. Portfolio decisions remained with the directors of the individual reserve banks, but the New York reserve bank, aided by a System committee, guided and implemented System decisions to purchase and sell. The Federal Reserve Board had supervisory responsibility only.

The new procedures radically changed the System’s original structure. The reserve banks sacrificed part of their autonomy to the System committee. Control of operations shifted toward the New York bank. Members of the Board resented New York’s increased authority, but they were powerless to combat it. These substantive differences combined with personal antipathies to heighten conflict between Benjamin Strong of the New York bank and members of the Board, particularly Adolph C. Miller. After Strong died, the conflict contributed to the delay in responding to the rapid expansion in the first half of 1929.

Chapter 4 ends at the start of the Great Depression. Chapter 5 follows the decisions and reasoning from meeting to meeting during the depression. It shows why the Federal Reserve remained passive through most of the decline and why it undertook major purchases in 1932 but stopped purchases before recovery was under way. The chapter ends with the financial collapse in March 1933.

President Franklin Roosevelt took office at the climax of the financial collapse. The new administration transformed many institutions, including the Federal Reserve. At the time, the dominant explanation regarded the depression as an inevitable consequence of speculation financed by speculators’ easy access to credit. Legislation separated commercial and investment banking and gave the Federal Reserve authority to set stock market margin requirements. In these and other ways, Congress absolved the Federal Reserve of responsibility for the debacle.

Legislation also corrected deficiencies in the 1913 Federal Reserve Act. That act barred the use of government securities as collateral for the currency. In 1932 the Glass-Steagall Act ended the prohibition as a temporary measure that later became permanent. The Banking Act of 1935 settled the long dispute over the locus of power by greatly increasing the Board’s power and by giving the Board a majority on the open market committee. The act ended the reserve banks’ ability to control their portfolios independently, creating the structure we know today.

Treasury requirements and gold inflows were major influences on money growth and interest rates from 1933 to 1941. The Federal Reserve’s main decision was to double reserve requirement ratios in three steps between August 1936 and March 1937. These actions, along with the Treasury’s decision to sterilize gold inflows, produced a steep monetary contraction. The 1937–38 recession followed.

Chapter 6 reports these events and the reasoning that produced them. The chapter also develops the attempts to reestablish an international financial system at the London Monetary and Economic Conference in 1933 and in the Tripartite Agreement of 1936 to limit exchange rate changes.

President Roosevelt called his programs the New Deal. Economic policy did not follow a consistent strategy. Before World War II, New Deal programs and actions had not restored prosperity or ended high unemployment. Wartime expansion achieved what New Deal policies did not.

The war and early postwar years (chapter 7) bring the volume to 1951. As in World War I, the Federal Reserve took an active part in administering wartime regulations and selling bonds. Its pledge to maintain a “pattern of rates” in effect fixed maximum rates at all maturities. The pledge ended any possibility of using monetary policy to control wartime or postwar inflation. In the postwar years to 1951, Federal Reserve officials became increasingly unhappy with the fixed pattern of interest rates, but they did not believe they could change policy without Treasury consent or support in Congress.

Chapter 7 also traces the development of postwar domestic and international legislation such as the Full Employment Act of 1946, the Bretton Woods Agreement establishing the International Monetary Fund and the World Bank, and the United States decision to finance European recovery. The chapter ends with the financing of the Korean War and the threat of renewed inflation that pushed the Federal Reserve into open conflict with the Treasury and brought about the March 1951 accord.

The concluding chapter summarizes the main findings and the lessons for monetary theory and policy.

1. Reasons other than effectiveness played a role in this transformation.

2. Wicker (2000) shows that perceptive writers understood the need for a lender of last resort by the 1860s, but attempts by the New York clearinghouse to provide the service often failed because of the conflict between the collective interest in system stability and the members’ individual concerns for the safety of their own institutions.

3. The comptroller is a Treasury official responsible for regulating banks with national charters.

4. Reserves are adjusted for changes in reserve requirement ratios.