GASOLINE RATIONING in the United States was lifted in August 1945, within twenty-four hours of Japan’s capitulation. And immediately, the voice of the motorist, silenced for years, was heard throughout the land, rising in a single, deafening crescendo—“Fill ’er up!” The rush was on, as drivers tossed away their rationing books and took to the streets and highways. America was in love once again with the automobile, and now consumers had the means to carry on the romance. In 1945, 26 million cars were in service; by 1950, 40 million. Virtually no one in the oil industry was prepared for the explosion of demand for all oil products. Gasoline sales in the United States were 42 percent higher in 1950 than they had been in 1945, and by 1950, oil was meeting more of America’s total energy needs than coal.

While demand was exploding far beyond expectations, the pessimistic predictions about postwar oil supplies were being eviscerated by actual experience. After controls were lifted, price proved to be a powerful stimulus to exploration. New regions were brought into production in the United States as well as in Canada, where, in 1947, Imperial, a Jersey affiliate, drilled a successful discovery well near Edmonton, in the province of Alberta, igniting the first, frenetic oil boom of the postwar years. Despite growing demand and rising production, proven United States reserves were 21 percent higher in 1950 than they had been in 1946. The United States was not, after all, running out of oil in the ground.

There was, however, a shortage of available oil in 1947–48. Crude prices rose rapidly, so that by 1948 they were more than double the 1945 level. Politicians declared that the country was in an energy crisis. The major oil companies were accused of deliberately orchestrating a squeeze play to push up prices, and suspicions of oil industry skullduggery and conspiracy launched more than twenty Congressional investigations.

But the reasons for shortage were quite obvious. Consumption rose with unexpected rapidity—“astonishingly,” said Shell—while there was the inevitable time lag in adapting to the postwar situation. It took time, money, and materials to redesign refineries to turn out the products that the civilian consumer wanted, such as gasoline and home heating oil, as opposed to 100-octane aviation fuel for fighter planes. In addition, steel was in short supply throughout the world, which slowed the conversion of refineries and the construction of tankers and pipelines, contributing to transportation bottlenecks. The tanker shortage worsened in early 1948, after several such ships broke in half while at sea, and the Coast Guard ordered 288 tankers laid up for emergency reinforcing. For the oil companies, it was a time of enormous pressure on retail supplies, and they became the leading advocates of conservation. Standard of Indiana urged motorists to cut back on their driving, avoid “jackrabbit” starts, and keep their tires properly inflated—all to reduce their consumption. “Helpful Hints” for conserving oil were promoted by Sun in its commercials on the popular daily broadcasts of newscaster Lowell Thomas.1

The shortages also drew in larger volumes of oil imports. Up through 1947, American exports of oil exceeded imports. But now the balance shifted; in 1948 imports of crude oil and products together exceeded exports for the first time. No longer could the United States continue its historical role as supplier to the rest of the world. Now it was dependent on other countries for that marginal barrel, and an ominous new phrase was being heard more often in the American vocabulary—“foreign oil.”

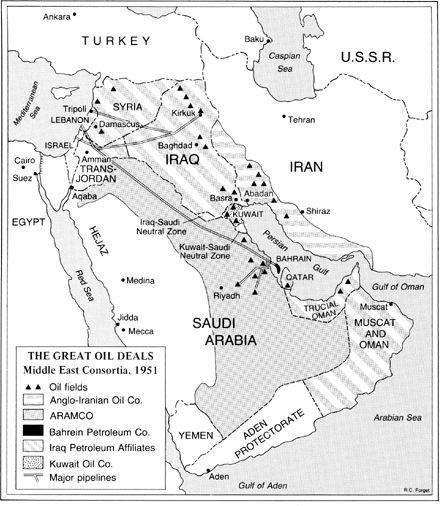

The Great Oil Deals: Aramco and the “Arabian Risk”

That shift added a new dimension to the vexing question of energy security. The lessons of World War II, the growing economic significance of oil, and the magnitude of Middle Eastern resources all served, in the context of the developing Cold War with the Soviet Union, to define the preservation of access to that oil as a prime element in American and British—and Western European—security. Oil provided the point at which foreign policy, international economic considerations, national security, and corporate interests would all converge. The Middle East would be the focus. There the companies were already rapidly building up production and fashioning new arrangements to secure their positions.

In Saudi Arabia, development was in the hands of Aramco, the Arabian-American Oil Company, the joint venture between Socal and Texaco. But Aramco was troubled. The reason was an embarrassment of riches, the very scale of the Saudi oil fields, which meant an enormous need for capital and for markets. Of the two companies in the joint venture, Socal was the more vulnerable. Texaco, the most important enterprise to have been spawned from the 1901 Spindletop discovery, was a famous American company; it sponsored the Metropolitan Opera on coast-to-coast radio, and Texaco’s service station attendant, “the man who wears the star,” was one of the familiar icons in the modern pantheon of American advertising. Socal, by contrast, was a regional company, and not very well known. Ever since World War I, it had expended millions of dollars searching for oil around the world. Yet it had nothing to show for its efforts, except for some minor production in the East Indies and Bahrain—and the massive potential of Saudi Arabia.

The Arabian concession was a grand prize that the California company could not have dared to hope for. It presented the company with a splendid opportunity—but it also meant, as Socal’s chairman Harry Collier saw it, formidable economic and political risks. By 1946, Standard of California’s investment in the Aramco concession totaled $80 million, and tens of millions more would be required. To gain access to European markets, Socal and Texaco wanted to build a pipeline across the desert from the Persian Gulf to the Mediterranean. It was essentially the same pipeline project that Harold Ickes had urged the U.S. government to finance, but now the companies themselves were going to have to come up with $100 million to pay for it. Socal faced another, even more daunting challenge. Once the oil got to Europe, how was it going to be marketed? To buy or build a refining and marketing system in Europe of sufficient size, Collier knew, would be very expensive and would commit Socal and Texaco to a deadly battle for market share against well-established competitors. The risks were further increased by the unstable political conditions. Large communist parties were represented in the coalition governments of both Italy and France, the future of occupied Germany was highly uncertain, and in Britain the Labour government was busying itself with nationalizing the “commanding heights” of the economy.

Yet Socal would have no choice but to go for higher and higher production levels, as the Saudi government recognized the potential of the reserves and would be pushing for higher output and revenues commensurate with the scale of the resources. The concession would always be in jeopardy if Aramco could not satisfy the expectations and demands of Ibn Saud and the royal family. This was the number-one consideration for Socal, and it meant that Aramco would have to move a great deal of oil, one way or another, into Europe. But before it ever got there, the Trans-Arabian Pipeline, called Tapline, would have to traverse several political entities, some of them only just moving toward statehood. A Jewish homeland might soon be established in Palestine, with possible American support, and Ibn Saud was one of the most prominent and adamant opponents of such a state. War could erupt in the region. The area also looked vulnerable to Soviet subversion and penetration in those early days of the Cold War.

Then there was the matter of the King himself, the same concern that had helped bring the chairmen of Socal and Texaco rushing to Washington in 1943. Ibn Saud was now in his mid-sixties, blind in one eye, and failing in health. His personal force and drive had created and held together the kingdom. But what would happen when that force was gone? He had sired upwards of forty-five sons, of whom thirty-seven were thought to be living, but would that be a factor for stability or for conflict and disorder? And, in the event of political problems, what kind of support from the American government could Socal count on? When all the risks were added up, it was clear that Socal would have to pursue its own policy of “solidification” and its drive to assure markets in other ways. The answer to Aramco’s many problems was a broader joint venture. Spread the risk. Tie in other oil companies, whose presence would add to the political density, and which could deliver capital, international expertise, and, especially, markets. One other qualification was also essential; Ibn Saud insisted that Aramco had to remain 100 percent American, in which case only two companies qualified: Standard Oil of New Jersey and Socony-Vacuum. In the Eastern Hemisphere, they could offer, recalled Gwin Follis, who handled the matter for Socal, “markets that we could hardly touch.”

The logic of wider involvement had been evident for some time, and not only to Collier and other oil men. Various State Department and United States Navy officials had encouraged Aramco to bring in additional partners who would “have sufficient markets to handle the concession” and thus help preserve it. Socal was struck by “the surprising enthusiasm in which the State Department received our notification that such a deal was being contemplated.” Whether or not Washington actually acted as an overt marriage broker, it was clear that enlarging the participation would further the fundamental goals of American strategy: to increase Middle Eastern production, thus conserving Western Hemisphere resources, and to enhance the revenues going to Ibn Saud, thus ensuring that the concession remained in American hands. As Navy Secretary James Forrestal put it in 1945, he did not “care which American company or companies developed the Arabian reserves” so long as they were “American.” In the spring of 1946, Socal opened talks with Standard Oil of New Jersey.

To say that Jersey was receptive would be an understatement. The company was facing a shortage of oil, and Europe was its most vulnerable market. How was Jersey going to get the oil it needed? Despite all the Sturm und Drang that had gone into setting up the Iraq Petroleum Company in the 1920s, Jersey’s share of Iraqi production in 1946 totaled a decidedly insignificant 9,300 barrels per day. Meanwhile, there would be more oil coming from Kuwait, further strengthening competitors, and Jersey greatly feared that Socal and Texaco would thrust into European markets on their own, challenging Jersey’s marketing system with limitless quantities of cheap Arabian oil. Socal’s overture presented Jersey with an opportunity to be passed up on no account.

While the two sides were haggling about the price of admission, Harry Collier, Socal’s chairman, found himself challenged by his own people, who rose up in rebellion against the very thought of inviting Jersey into Aramco. The attack came from Socal’s production department in San Francisco, which had been in charge of making the barren desert bloom and did not want to lose control to larger and more powerful partners. For thirteen years, there had been no return to stockholders on the investment in Arabia, and only now, in 1946, was the concession starting to become profitable. Why give it away to Jersey? Even more vociferous were the men on the ground, led by James MacPherson, a Socal engineer who was in charge of field operations for Aramco in Saudi Arabia. The concession, he argued, was a “gold mine.” MacPherson was intent on building Aramco into a major independent force in world oil. He would point to a globe and tell his staff, “That is our oil market.” Aramco, he proclaimed, was destined to become “the greatest oil company in the world.” But now, he scathingly declared, Aramco—and Socal—were to turn themselves into an annex to Jersey’s production department.

Harry Collier, by contrast, believed Aramco would be able to sell so much additional oil through access to Jersey’s system that Socal would end up with much more “gold” than by going it alone with only Texaco. Moreover, the deal would enable Socal to recoup all of its direct investment. Collier was the boss, a strong-willed man—he was not called one of the “Terrible Tycoons” for nothing. Tying up with Jersey was the safer course as far as he was concerned, and Jersey would be invited in. Aramco was not, after all, destined to become the greatest oil company in the world. Argument ended.2

Erasing the Red Line

As the discussions proceeded on how Jersey would enter Aramco, Jersey was also holding side conversations with Socony about its possible participation. But both Jersey and Socony confronted two most formidable obstacles before they could enter Aramco: their own membership in the Iraq Petroleum Company—and Calouste Gulbenkian. The companies had expended six years and many, many thousands of hours of executive frustration in the 1920s to put the IPC arrangement together. One of its key provisions, of course, was the famous Red Line Agreement, which provided that the participants in the IPC could not operate independently anywhere inside the red line that Calouste Gulbenkian said he had drawn on the map in 1928. Saudi Arabia was most definitely inside the red line, and the “self-denying” clause 10 of the IPC agreement effectively prohibited Jersey and Socony from going into Aramco unless they took everyone else along with them—Shell, Anglo-Iranian, the French state company (CFP), and Mr. Gulbenkian himself.

Jersey and Socony had wanted out of the Red Line agreement for some time; it did not do them a lot of good, as it had turned out, to be straitjacketed in the most prolific oil basin in the world for a mere 11.875 percent each of an enterprise they did not control. The United States government had helped them get into the deal in the 1920s, but it was now abundantly clear that Washington was not going to do much to help get them out of it in the 1940s.

But, then, Jersey and Socony found another way to extricate themselves. A Socony executive called it a “bombshell.” The device was called the doctrine of “supervening illegality.” At the outbreak of World War II, the British government had taken control of the shares of the IPC held by CFP and Gulbenkian, who had packed up and gone off with the collaborationist French government to Vichy, where he had been accredited to the Iranian legation as commercial attaché. London’s seizure of the shares had been made on grounds that both CFP, as a company, and Gulbenkian were domiciled in territory under Nazi control and, therefore, were considered “enemy aliens.” Under the doctrine of “supervening illegality,” the entire IPC agreement was thus “frustrated”—made null and void.

At war’s end, their IPC shares reverted to both CFP and Gulbenkian. But then in late 1946, Jersey and Socony took up the concept of “supervening illegality” with what could only be called extreme enthusiasm. In their view, the whole IPC agreement was no longer in effect. A new agreement would have to be negotiated. Representatives of Jersey and Socony hurried to London to see the European members of the IPC in order to break their news: The old agreement was dissolved—Red Line and all. They would be willing to enter into a new understanding, certainly, but without the restrictive Red Line clauses, which “under present world conditions and American Law are inadvisable and illegal.” The Americans knew that they would have to persuade four distinct parties to renegotiate—Anglo-Iranian, Shell, CFP, and an enterprise called Participations and Investments (P&I), which was really nothing more than the holding company for their old nemesis, Calouste Gulbenkian.3

Anglo-Persian and Shell indicated that they thought the matter could be amiably worked out on the basis of “mutual interest.” The French, however, were in no mood to compromise. They rejected, without any qualification, the American contention that an agreement no longer existed. The Iraq Petroleum Company and the Red Line Agreement constituted their sole key to Middle Eastern oil. They were depending on this government-sanctioned allocation and would not relinquish what the French government had struggled so hard to obtain. France’s energy position was bad enough already. It was said that General Charles de Gaulle, head of the French government, had exploded in rage when he discovered what small volumes of oil CFP actually produced—though he knew that he could not dispute geology or, as one of his aides put it, “be angry with God.”

As for Calouste Gulbenkian, he replied swiftly and defiantly to Jersey and Socony’s attempt to abandon the agreement: “We do not acquiesce.” The Iraq Petroleum Company, and its predecessor, the Turkish Petroleum Company, had been his life’s work, his great personal monument. He had started fashioning it forty years earlier, and he was not going to allow it to be easily dismembered. In 1946, Gulbenkian was in residence in Lisbon; he had moved there from Vichy in the middle of the war. Now, though unwilling to budge from Portugal, he would, through his lawyers and agents, do whatever was necessary to resist efforts to overturn the Red Line Agreement. The American negotiators were of a new generation, and lacking the benefit of Walter Teagle’s experience of endless exasperation, they dismissed Gulbenkian’s threats. “We have no reason to buy Gulbenkian’s signature,” Harold Sheets, the chairman of Socony, optimistically said. Confident of their legal position, they decided to go ahead and make their deal with Texaco and Socal, the two Aramco companies.

The danger of litigation over the IPC and the Red Line Agreement was not, however, the only risk with which Jersey and Socony had to wrestle. Would the new quadripartite Aramco combination violate American antitrust laws? That worry stirred the lawyers to dust off the 1911 dissolution decree. After all, three of the four would-be participants in the enlarged joint venture had been spun out of the original Rockefeller Trust. But the lawyers concluded that the proposed combination would violate neither antitrust laws, even under the new interpretations, nor the dissolution decree “because no unreasonable restraints on American commerce would be imposed.” After all, Aramco was not going to go into the oil business in the United States. The chief counsel of Socony expressed a larger worry—that seven companies would not be allowed to hold such overwhelming control of crude reserves in the Eastern Hemisphere as well as in the Western Hemisphere “for any great length of time… without some sort of regulation.” But he added, “This is a political question… within the realms of conjecture. Our job seems to be to play the game as best we can under the rules now in force.”

And the best way to play was to proceed. By December 1946, the four companies had agreed in general principle to expand Aramco. After an immediate protest from one of Gulbenkian’s representatives, a Socony executive in London sought to reassure his chairman in New York: “I have no doubt that P&I and the French may raise quite a song and dance about the matter, but I think they will be careful to wash the linen within the family circle.”4

The French were not burdened with such modesty. In January 1947 they launched a very public counterattack. Their ambassador in Washington lodged a strong protest with the State Department. Authorities in France started to make Jersey’s life, commercially uncomfortable. And in London, CFP’s solicitors brought suit, charging breach of contract and asking that any shares that Jersey and Socony acquired in Aramco be held in trust for all the members of the IPC.

The awkward situation with France, a key ally in Western Europe, combined with a continuing antitrust concern, prompted the State Department to promote an alternative to the prospective deal that would both satisfy the French and check the growth of suspiciously close arrangements among giant international oil companies. Advice on petroleum matters in the State Department was largely in the hands of Paul Nitze, head of the Office of International Trade Policy. Nitze proposed that Jersey sell its IPC shares to Socony and then go it alone into Aramco, creating two distinct groups with no overlapping membership. The French could not then charge that their rights under the Red Line Agreement were being challenged, said Nitze. Such a deal, he added, would “arrest the trend toward the multiplication of the interlocking agreements among international oil companies” and “retard the growing consolidation outside of the United States of the interests of the two largest American oil companies, Jersey and Socony.” The two companies replied that the proposal was “not a practicable plan.” And Undersecretary of State Dean Acheson scotched Nitze’s idea.5

There was someone else whose voice had yet to be heard—Ibn Saud. He, too, had to be consulted. Aramco executives went to Riyadh to see the King. They explained to him that the “marriage” of the four companies was “a natural” and would mean more royalties for the kingdom. But the King was interested in only one point, and on that he was insistent; he wanted to be positive that neither Jersey nor Socony were “British-controlled.” Firmly reassured on the purely American character of the two new companies, the King finally gave his approval to the proposal.

But what would happen if the French won in the courtroom? They could insist upon participating in Aramco. And so, for that matter, could Anglo-Iranian. The King had made absolutely clear that he would not tolerate such a situation. The deal had to be restructured to take into account this contingency. Therefore, the final arrangement provided a clever piece of flexibility just in case the American companies lost in any legal proceedings. Jersey and Socony guaranteed a loan of $102 million, which could be converted into equity valued at $102 million as soon as it was legally safe to do so. In the meantime, Jersey and Socony could start taking oil at once, as though they were already owners. In addition, Jersey and Socony would become partners in Tapline. Socal and Texaco would also get overriding payments on every barrel produced for a number of years. Thus, altogether, Socal and Texaco would receive a total of about $470 million over several years for selling 40 percent of Aramco—getting all of their original investment back and a good deal more. Moreover, as Gwin Follis of Socal later observed, the terms of the sale to Jersey and Socony took “the enormous investment” required for Tapline “off our shoulders.”

Initially, Jersey and Socony planned to split the 40 percent evenly. But Socony’s president, fretful that Middle Eastern oil “was not absolutely safe” and worried about markets, argued that the company “ought to put more money in Venezuela.” After some consideration, Socony decided that it did not need so much oil, and that a lower share would do just fine. Thus, Jersey took 30 percent, the same position to which Socal and Texaco had diluted, while Socony took only 10 percent. It would not be very long before Socony came to regret its parsimony.

There was still last-minute nervousness. Antitrust considerations continued to weigh on the minds of executives from all the companies, until they received a reassurance from the U.S. Attorney General. “Off-hand,” the Attorney General said, he saw “no legal objections to the deal. It should be a good thing for the country.” But then, in confirmation of Harry Collier’s worst fears, political troubles in the eastern Mediterranean, which could have an impact on the entire deal, came to the fore. There was a communist-led insurrection in Greece and a Soviet threat to Turkey, and it was feared that, with Britain pulling back from its traditional commitments in the Middle East, communist power might grow in the region. On March 11, 1947, Socony’s directors discussed “the problems affecting the Middle East.” But optimism prevailed and they approved the deal. The next day, March 12, 1947, officials of the four American companies met and signed the documents that put the historic transaction into force. The concession in Saudi Arabia had, at last, been “solidified.”

March 12 happened to be a historic day for another reason. On that day, President Harry Truman went before a joint session of Congress to deliver what was called the “all-out speech,” proposing special aid to Greece and Turkey to enable them to resist communist pressure. The speech, a landmark in the emerging Cold War, initiated what became known as the Truman Doctrine and launched a new era in postwar American foreign policy. While a coincidence, the Truman Doctrine and the sealing of the participation of four giants of the American oil industry in the riches of Saudi Arabia now assured a substantial American presence and interest in a vast area, stretching from the Mediterranean to the Persian Gulf.6

Gulbenkian Again

The CFP litigation was still pending. But France had many other things on its political agenda with the United States that it wanted to pursue; and by May of 1947, a deal had been worked out that improved the position of the French in the Iraq Petroleum Company. And, of course, CFP would, in exchange, withdraw its suit.

Gulbenkian, as usual, was another matter. Installed in a first-floor suite in Lisbon’s venerable Hotel Aviz, Gulbenkian kept to his flint-nosed habits. Because it was cheaper, he no longer maintained a car and chauffeur, but hired a driver to take him into the country for his daily walk, carefully checking the odometer on the car to make sure he was not being charged for someone else’s trips. “Gulbenkian may be regarded as a man of his word once this has been given,” observed a British official. “The difficulty lies in obtaining it. The ability to compromise is not one of his attributes.” The official could not help adding that “Gulbenkian’s idea of his own financial integrity takes on a peculiar form when it comes to taxation, the avoidance of which constitutes one of his major activities.” He escaped income taxes in France and Portugal by maintaining an appointment with the Iranian legation. In order to avoid property tax on his mansion in Paris, he turned a small part of it into a picture gallery. And when he sold the Ritz Hotel in Paris, he insisted on terms that provided that a suite be permanently reserved for him, so that he could always claim that he was “in transit” while in Paris—thus further avoiding French taxation.

Gulbenkian brought this same infuriating attention to detail, along with his reluctance to compromise and his intense powers of concentration, to the struggle over the Red Line Agreement. Though the French had dropped their suit, Gulbenkian was willing to wash every last piece of dirty linen in public if necessary. He filed suit in a British court. Jersey and Socony responded with counter-suits.

The case received wide publicity, which helped Gulbenkian in his counterattack against Jersey and Socony. After all, it was not he, but the American companies that had to worry about the Justice Department and public opinion. Still, there was a side effect of the notoriety that he very definitely found distasteful. Owing to his short stature, he had ordered a special platform built in the restaurant of the Hotel Aviz, so that he could eat his lunch and survey the scene at the same time. As the publicity from the case increased, “Mr. Gulbenkian at the Hotel Aviz” became one of the tourist “musts” of Lisbon, along with the bullfights. He objected, but there was nothing much he could do about it.

For well over a year, negotiators shuttled back and forth from New York to London to Lisbon, looking for a compromise. Now the next generation of oil men and lawyers had the opportunity to learn how exasperating it was to deal with Calouste Gulbenkian. “It was my father’s practice never to press any claim to a breakdown,” said his son Nubar, “but, very able negotiator that he was, to make his demands step by step, so that having obtained satisfaction on one point he would raise another and yet another, thus achieving all he wanted or, at least, much more of what he wanted than he would have obtained if he had started by putting forward all his demands at once.”

Negotiations were made even more difficult by Gulbenkian’s habitual suspicion, which had deepened into an obsession. Gulbenkian did not attend the various meetings himself. He had four different representatives at the sessions, each of whom had to report to him separately in writing, without collaborating—indeed, without even talking to the others. That way, in addition to analyzing his opponents, he could double check and second guess each of his own negotiators.

But what, in essence, did Gulbenkian want? Some suspected that he actually aimed to get a share of Aramco. That was out of the question. Ibn Saud would never allow it. To a director of Socony, Gulbenkian offered a simple explanation of his objective. He could not respect himself unless he “drove as good a bargain as possible.” In other words, he wanted as much as he could get. To another American, not an oil man at all, but one who shared his love of art, Gulbenkian could explain still more. He had made so much money that more money, in itself, did not count for very much. He thought of himself in the same terms he had used to Walter Teagle two decades before—as an architect, even as an artist, creating beautiful structures, balancing interests, harmonizing economic forces. That was what gave him his joy, he said. The artworks he had collected over his lifetime had come to compose the greatest collection ever assembled by a single person in modern times. He called them his “children,” and seemed to care more for them than for his actual son. But his masterpiece, the greatest achievement of his life, was the Iraq Petroleum Company. To him, it was as architecturally designed, as faultlessly composed, as Raphael’s The School of Athens. And if he was Raphael, Gulbenkian made clear, he regarded the executives of Jersey and Socony in much the same company as Giroloma Genga, a third-rate, mediocre, obscure imitator of the masters of the Renaissance.7

Under the pressure of the unpleasant arguments soon to begin in a London courtroom, an agreement with Gulbenkian at last seemed to take shape; and the whole “caravan,” as it was called, of oil men and their lawyers migrated to Lisbon. Finally, at the beginning of November 1948, on the Sunday before the Monday on which the court arguments were to begin, the new agreement was completed. Nubar, the dutiful and gracious son, had booked a private room in the Hotel Aviz where the signing was to take place, at 7:00P.M., to be followed by a celebratory dinner.

At five minutes to seven, Gulbenkian announced that he had found one more point that had not been covered in the new agreements. Consternation gripped the room. Telegrams were sent back to directors in London, and replies were awaited. A stunned and depressing silence descended on the Hotel Aviz. Yet the food had been ordered, it would soon be cold, and there was no point in not eating, at least so far as Nubar Gulbenkian could see. He summoned the “caravan” to the table. The dinner that ensued was very somber and funereal; only one bottle of champagne was drunk among twelve people. There was nothing to celebrate.

Around midnight, the telegrams came back from London. Gulbenkian’s final demand was acceded to. The agreements were retyped, Gulbenkian signed them at one-thirty in the morning, and they were sent by chartered plane to London. The appropriate officials were informed that the court proceedings scheduled for later that day in London should be called off, and the exhausted group in Lisbon finally adjourned to an all-night cafe to celebrate over sandwiches and cheap wine.

Thus was negotiated the Group Agreement of November 1948, which reconstituted the Iraq Petroleum Company. What Gulbenkian got, in addition to higher overall production and other advantages, was an extra allocation of oil. Mr. Five Percent was no more; he was now something greater. The agreements themselves were “monuments of complexity.” An Anglo-Iranian executive (and later a chairman of the company) declared, “We have now succeeded in making the Agreement completely unintelligible to anybody.” But there was an advantage to such complexity, for, as one of Gulbenkian’s lawyers put it, “No one will ever be able to litigate about these documents because no one will be able to understand them.”

Once the granite obduracy of Calouste Gulbenkian had been overcome and the new Group Agreement for the Iraq Petroleum Company had been signed, the Red Line Agreement was no more, and the legal threat to Jersey’s and Socony’s participation in Aramco was removed. It had been a long, tortured struggle by which the two companies won their entrée to Saudi Arabia. “If you laid all the conversations that went into this deal end to end,” said one participant, “they would reach to the moon.” In December 1948, two and a half years after the deal had first been discussed, the Jersey and Socony loans could be converted into payments, and the Aramco merger could finally be completed. A new corporate entity, more commensurate with Saudi reserves, had come into existence. With the deal done, Aramco was owned by Jersey and Socony, as well as Socal and Texaco. And it was 100 percent American.

For his part, Gulbenkian had once again succeeded in preserving his exquisite creation, the Iraq Petroleum Company, as well as his position in it, against the combined might of international oil. His last display of artistry was ultimately to earn hundreds of millions of dollars more for the Gulbenkian interests. Gulbenkian himself lived on for another six years in Lisbon, occupying himself by ceaselessly arguing with his IPC partners and by writing and rewriting his will. When seven years later, in 1955, he died at age eighty-five, he left behind three enduring legacies: a vast fortune, a splendid art collection and, most fittingly of all, endless litigation over his will and the terms of his estate.8

Kuwait

Another American company, Gulf Oil, faced a quandary in the Middle East. As half owner of the Kuwait Oil Company, Gulf was constrained to some degree from competing with its partner, Anglo-Iranian, particularly in India and the Middle East. Where else could Gulf dispose of its oil? It had a small system in Europe that was hardly adequate for even a fraction of the rapidly rising tide of oil that would be available from Kuwait. Gulf needed outlets, primarily in Europe. So Colonel J. F. Drake, the company’s president, went in search of them. The best answer to Gulf’s problem soon became apparent: the Royal Dutch/Shell Group. It owned one of the two largest marketing organizations in the Eastern Hemisphere, particularly in Europe. And unlike its competitors, it had access to very little Middle Eastern oil. As Drake explained to the State Department, a deal “between Gulf, which is long on crude oil and short on markets, and Shell, which is long on markets and short on crude oil,” made excellent sense.

The two companies developed a unique purchase-and-sale agreement; it was a shadow integration that would allow Gulf’s Kuwaiti oil to flow into Shell’s refining and marketing system via a long-term contract—initially a ten-year agreement, which was later extended another thirteen years. The total volumes of oil over the life of the contract were estimated to account for fully a quarter of Gulf’s proven reserves in Kuwait. In turn, Gulf would be providing Shell with 30 percent of its requirements in the Eastern Hemisphere. No one would be so foolish as to set a fixed price over such a long and uncertain duration. So the two companies came up with an innovative solution—what would become known as “netback pricing.” The contract provided for a fifty-fifty split of the profits—profit being defined as “final selling price” minus all costs along the way. The schedules and accounting formulas by which profit would ultimately be calculated were so complicated that they took up over half of the 170 printed pages of the contract.

In truth, Gulf had hardly any alternative to Shell. Kuwaiti production was going up rapidly; the Amir would insist upon such increases, especially when he saw the production curves in his neighboring countries. Very few systems could absorb so much oil. Shell’s was about the only one available. Furthermore, there was an aspect to the deal that would certainly win the approval of the State Department. It was, Colonel Drake said, the only option that Gulf could see that would leave its one-half interest in Kuwaiti oil “wholly American owned.” In short, first with Aramco, and now with the Gulf-Shell arrangement, American oil interests in the Middle East were being protected. As for Shell, the deal would give it a claim on a substantial part of Kuwait’s total output. It was more than merely a long-term buyer. As the Foreign Office put it, “in Her Majesty Government’s view,” Shell was “to all intents and purposes a partner in the Concession.”9

Iran

The third of the great postwar oil deals involved Iran. In the course of the first discussions in London on abrogating the Red Line Agreement in the late summer and early fall of 1946, the representatives of Jersey and Socony privately raised the possibility of a long-term contract for Iranian crude with Sir William Fraser, chairman of Anglo-Iranian. “Willie” was certainly receptive. Like Gulf, Anglo-Iranian did not have the wherewithal to build up quickly a large refining and marketing system of its own in Europe, and it feared that it would find itself shut out of Europe by cheap and abundant oil from Aramco.

But political considerations also provided reason for AIOC to tie up long-term relationships with American companies and thus help “solidify” its own position. For Iran was under continuing and considerable pressure from the Soviet Union. In the latter part of World War II, the Soviet Union had demanded an oil concession in Iran, and Soviet troops continued to occupy Azerbaijan in northern Iran after the war. Stalin did not withdraw until the spring of 1946, and then only in response to intense pressure by the United States and Britain. Indeed, what became known as the Iranian Crisis of 1946 was the first major East-West confrontation of the Cold War.

In early April 1946, at the same time that the Soviets were finally beginning to withdraw their troops, the American ambassador in Moscow went to the Kremlin for a private, late-night meeting with Stalin. “What does the Soviet Union want, and how far is Russia going to go?” the ambassador asked.

“We’re not going much farther,” was the not particularly reassuring reply of the Soviet dictator, who went on to describe Soviet efforts to extend influence over Iran as a defensive move to protect its own oil position. “The Baku oil fields are our major source of supply,” he said. “They are close to the Iranian border and they are very vulnerable.” Stalin, who had become a “journeyman of the Revolution” in Baku four decades earlier, added that “saboteurs—even a man with a box of matches—might cause us serious damage. We are not going to risk our oil supply.”

In fact, Stalin was interested in Iranian oil. Soviet oil production in 1945 was only 60 percent of that of 1941. The country had desperately mobilized a range of substitutes during the war—from oil imports from the United States to charcoal-burning engines for its trucks. Shortly after the war, Stalin interrogated his petroleum minister, Nikolai Baibakov (who subsequently was to be in charge of the Soviet economy for two decades—until 1985, when Mikhail Gorbachev replaced him). Mispronouncing Baibakov’s name, as he always did, Stalin demanded to know what the Soviet Union was going to do in the light of its very bad oil position. Its oil fields were seriously damaged and heavily depleted, with little promise for the future. How could the economy be reconstructed without oil? Efforts, the dictator said, would have to be redoubled.

Toward that end, the Soviet Union made its demands for a joint oil exploration company within Iran. So, certainly, oil was one Soviet objective in Iran, but not the only one, by any means, and not the most important. In 1940, in the context of the Nazi-Soviet Pact, Soviet Foreign Minister Vyacheslav Molotov had declared that “the area south of Batum and Baku in the general direction of the Persian Gulf be recognized as the center of the aspirations of the Soviet Union.” That area had a name—Iran. Stalin was seeking to build up his own sphere in bordering countries, and to expand Soviet power and influence wherever he could. In trying to reach into Iran and toward the Persian Gulf, he was also pursuing a traditional objective of Russian foreign policy, one that was almost a century and a half old. The pursuit of that same objective had, at the turn of the century, provided the motivation for the British government to support the original 1901 Iranian concession of William D’Arcy Knox, as one way to blunt the Russian advance.

After Stalin pulled back his soldiers from northern Iran in 1946, the Soviet Union continued to try to gain a favored position in that area and sought to establish a joint Soviet-Iranian oil company. Meanwhile, the communist-led Tudeh party was conducting a campaign of demonstrations and political pressure to gain greater sway over the central government—including a general strike and demonstrations at Anglo-Iranian’s Abadan refinery complex, in which a number of people were killed. Iran was unstable, the political institutions in the country were weak, and there was the grave possibility of civil war or even of the disappearance of Iran into the Soviet bloc.

Both the American and British governments were trying to help to preserve the independence and territorial integrity of Iran. And London was categoric: Anglo-Iranian’s oil position in Iran was the company’s crown jewels, and it had to be preserved at all costs. In the face of such uncertainty and in light of the high stakes, there was some considerable value in having major American companies take a more direct interest in Iranian oil. Thus, political as well as commercial realities underlay the deal between Anglo-Iranian and the two American companies, Jersey and Socony. In September 1947, the three companies signed a twenty-year contract.10

With the completion of the three huge deals—Aramco, Gulf-Shell, and the long-term Iranian contracts—the mechanisms, capital, and marketing systems were in place to move vast quantities of Middle Eastern oil into the European market. In the postwar world, petroleum’s “center of gravity”—not only for the oil companies, but also for the nations of the West—was indeed shifting to the Middle East. The consequences would be momentous for all concerned.

Europe’s Energy Crisis

The swelling volumes of Middle Eastern oil were crucial to the postwar recovery of a devastated Europe. Destruction and disorganization were everywhere. The workshop in the heart of Europe, Germany, was hardly functioning at all. Throughout Europe, food and raw materials were in desperately short supply, established trading patterns and organizations had broken down, inflation was rampant, and there was a severe shortage of the American dollars that were required to purchase necessary imports. By 1946, Europe was already gripped by a severe energy crisis—a terrible shortage of coal. And then the weather, the longest and coldest winter of the century, brought conditions to a crisis point. In England, the River Thames froze at Windsor. Throughout Britain, coal was in such short supply that power stations had to be shut down, and electricity to industry was either reduced greatly or cut off entirely. Unemployment abruptly increased six times over, and British industrial production was virtually halted for three weeks—something German bombing had never been able to accomplish.

This unexpected shortfall of energy drove home the extent to which Britain had been impoverished by the war. Its imperial role had become an insupportable burden. During those few bleak, freezing, and pivotal weeks of February 1947, the Labour government of Clement Attlee referred its intractable Palestine problem to the United Nations and announced that it would grant independence to India. And on February 21 it told the United States that it could no longer afford to prop up the Greek economy. It asked that the United States take over that responsibility and, by implication, broader responsibilities throughout the Near and Middle East. Still, the situation worsened. Throughout Europe, the economic disarray brought on by the weather and the energy crisis in the winter of 1947 accentuated the shortfall of U.S. dollars, which constrained Europe’s ability to import vital goods and paralyzed its economy.11

The first step toward averting a massive breakdown was taken in June 1947, in Harvard Yard in Cambridge, Massachusetts. There, at the Harvard commencement, United States Secretary of State George Marshall introduced the concept of a large, broadly based foreign aid program that would help revive and reconstruct the economies of Western Europe in a continental framework and that would fill the gap created by the shortage of dollars. In addition, the European Recovery Program, or the Marshall Plan, as it was soon known, became a central element in the containment of Soviet power.

Among the first problems to be addressed was Europe’s energy crisis. There was not enough coal capacity, productivity was low, and the labor force was disorganized. Moreover, in many countries, communists occupied leading roles in the miners’unions. Oil was part of the solution; it could replace coal in industrial boilers and power plants. Oil was also, obviously, the only source of fuel for Europe’s airplanes, motorcars, and trucks. “Without petroleum the Marshall Plan could not have functioned,” said a U.S. government report at the time.

Those in Paris running the European Recovery Program did not worry much about the physical availability of oil. They simply counted on the companies to assure that supplies were there. Oil did, however, have to be imported, and that made it not only part of the solution, but also part of the problem. Approximately half of Europe’s petroleum came from American companies, which meant that it had to be paid for in dollars. For most of the European countries, oil was the largest single item in their dollar budgets. It was estimated in 1948 that upwards of 20 percent of total Marshall Plan aid over the subsequent four years would go to the imports of oil and oil equipment.12

Price became a very contentious matter. The Europeans became particularly outspoken on the subject of the dollar drain from the purchase of oil in 1948, when oil prices, rising quickly, were at their postwar peak. “How unfortunate it was,” British Foreign Secretary Ernest Bevin told the American ambassador, that “while the Americans were voting money to help Europe, the rise in oil prices nullified their efforts to a considerable extent.” The dollar drain led to a bitter argument as to how much “dollar oil” (from American companies) and how much “sterling oil” (from British companies) would come into the United Kingdom and the rest of Europe. There was also a running battle with the oil companies about cost, particularly for the growing volumes of Middle Eastern oil, and whether those prices were competitively set or could and should be lower. Eventually, after much acrimony, Middle Eastern oil was being pushed down to price levels below what had, until then, been the benchmark U.S. Gulf Coast price. This meant the end of the pricing convention that had been established two decades earlier, at Achnacarry Castle. The last vestige of the prewar “As-Is” system was now gone.13

Yet, despite all the controversies, the fundamental fact was that the Marshall Plan made possible and pushed a far-reaching transition in Europe—the change from a coal-based economy toward one based on imported oil. The short supplies of coal, compounded by labor strife and strikes in the mining industry, gave powerful impetus to that change. “It is not a joyful thing, but it is a national necessity to import more oil,” Britain’s Chancellor of the Exchequer, Hugh Dalton, told Marshall. Government policies also encouraged the conversion of power plants and industry from coal to oil. Because of the great surge of cheap production from the Middle East, oil could effectively compete against coal in price. Moreover, when industrial consumers came to make their choice, they could see a clear distinction between coal, whose tribulations and disruptions were daily fare in the press, and oil, whose supply and distribution were handled efficiently and with little friction.

Where possible, the oil companies moved to capture new markets, both in industry and in homes—in the latter case, with the revolutionary innovation of central heating. In the words of one Shell manager, “The Englishman began to realize that there was no value in being cold, and there was no reason why he should not have the amenities of his American and Canadian cousins.” Though Europe remained a coal-based economy, oil became increasingly important, especially to fuel the incremental growth in energy demand. That was where the new production of the Middle East loomed so large. In 1946, 77 percent of Europe’s oil supply came from the Western Hemisphere; by 1951, it was expected that a dramatic shift would take place—with 80 percent of supply to come from the Middle East. The synchronization of Europe’s needs and the development of Middle Eastern oil meant a powerful and timely combination.14

To Market It Goes?

There was still the problem of getting those rapidly growing volumes of oil to market. Aramco and its parent companies, now four, were continuing to battle to build Tapline, which would carry Saudi Arabian oil to the Mediterranean. But several major obstacles stood in its path. Steel, in short supply, was still under United States government controls, and yet a big share of the total steel output in the United States would have to be allocated for the pipes and tubing required for the mammoth undertaking. The independent oil men and their Congressional allies tried to block the allocation in order to prevent the buildup of large volumes of cheap foreign oil that they feared would flow into the American market. But there was significant support for Tapline in the Truman Administration, much of it based on the view that Middle Eastern oil supply was essential to the success of the Marshall Plan. Without the pipeline, warned one State Department official, “the European recovery program will be seriously handicapped.”

Another obstacle was the stubbornness of the countries the pipeline had to cross, particularly Syria, all of which were demanding what seemed to be exorbitant transit fees. It was also the time when the partition of Palestine and the establishment of the state of Israel were aggravating American relations with the Arab countries. But the emergence of a Jewish state, along with the American recognition that followed, threatened more than transit rights for the pipeline. Ibn Saud was as outspoken and adamant against Zionism and Israel as any Arab leader. He said that Jews had been the enemies of Arabs since the seventh century. American support of a Jewish state, he told Truman, would be a death blow to American interests in the Arab world, and should a Jewish state come into existence, the Arabs “will lay siege to it until it dies of famine.” When Ibn Saud paid a visit to Aramco’s Dhahran headquarters in 1947, he praised the oranges he was served but then pointedly asked if they were from Palestine—that is, from a Jewish kibbutz. He was reassured; the oranges were from California. In his opposition to a Jewish state, Ibn Saud held what a British official called a “trump card”: He could punish the United States by canceling the Aramco concession. That possibility greatly alarmed not only the interested companies, but also, of course, the U.S. State and Defense departments.

Yet the creation of Israel had its own momentum. In 1947, the United Nations Special Committee on Palestine recommended the partition of Palestine, which was accepted by the General Assembly and by the Jewish Agency, but rejected by the Arabs. An Arab “Liberation Army” seized the Galilee and attacked the Jewish section of Jerusalem. Violence gripped Palestine. In 1948, Britain, at wit’s end, gave up its mandate and withdrew its Army and administration, plunging Palestine into anarchy. On May 14, 1948, the Jewish National Council proclaimed the state of Israel. It was recognized almost instantly by the Soviet Union, followed quickly by the United States. The Arab League launched a full-scale attack. The first Arab-Israeli war had begun.

A few days after Israel’s proclamation of statehood, James Terry Duce of Aramco passed word to Secretary of State Marshall that Ibn Saud had indicated that “he may be compelled, in certain circumstances, to apply sanctions against the American oil concessions… not because of his desire to do so but because the pressure upon him of Arab public opinion was so great that he could no longer resist it.” A hurriedly done State Department study, however, found that, despite the large reserves, the Middle East, excluding Iran, provided only 6 percent of free world oil supplies and that such a cut in consumption of that oil “could be achieved without substantial hardship to any group of consumers.”15

Ibn Saud could certainly have canceled the concession, but at considerable risk. For Aramco was the sole source of his rapidly rising wealth, and the broader relationship with the United States provided the basic guarantee of Saudi Arabia’s territorial integrity and independence. Ever suspicious of the British, the King feared that London might be sponsoring a new coalition to champion the Hashemites, as it had done after World War I, enabling the Hashemites—whom Ibn Saud had driven from Mecca only two decades earlier—to recapture the western part of his country. His apprehension mounted when Abdullah, the Hashemite King of Jordan, was said to have “likened the Saudi regime to the Jewish occupation of Palestine.” And the Hashemites constituted, to Ibn Saud, an even greater enemy than the Jews. The Soviet Union and communists, too, were a more dangerous threat, in terms of Soviet pressure to the north and the impact of communist activity within the Arab world.

Indeed, in the face of the Hashemite and communist threats, Ibn Saud pressed the Americans and even the British in late 1948 and 1949 for a tripartite defensive treaty. The British minister to Saudi Arabia observed in his annual review to London, “As Israel became, and was seen by most Arabs to become, a reality which could not be wished away, the Saudi Arabian Government resigned themselves to its existence in practice while maintaining their formal hostility to Zionism.” Ibn Saud found he could distinguish between Aramco, a purely commercial enterprise owned by four private companies, and the policy of the U.S. government elsewhere in the region. When other Arab countries declared that Saudi Arabia should cancel the concession to retaliate against the United States and prove its allegiance to the Arab cause, Ibn Saud replied that oil royalties helped to make Saudi Arabia “a stronger and more powerful nation, better to assist her neighboring Arab states in resisting Jewish pretensions.”

And so, even while Jew and Arab were at war in Palestine, the feverish oil development continued within Saudi Arabia, and construction proceeded on Tapline. It was finished in September 1950. Two more months were required to fill the line, and in November, the oil began to arrive at Sidon in Lebanon, the terminus on the Mediterranean, where it was picked up by tankers for the last leg of the journey to Europe. Tapline’s 1,040 miles would replace 7,200 miles of sea journey from the Persian Gulf through the Suez Canal. Its annual throughput was the equivalent of sixty tankers in continuous operation from the Persian Gulf, via the Suez Canal, to the Mediterranean. The oil it carried would fuel the recovery of Europe.16

No Longer “Far Afield”: The New Dimension of Security

The overlapping of politics and economics had, in the second half of the 1940s, created a new strategic focus for both the British and the American governments. In the case of the British, even as they withdrew from the far reaches of empire, they could not turn their backs on the Middle East. The Soviets were putting pressure on the “northern tier”—Greece, Turkey, and in particular, Iran. And Iran, plus Kuwait and Iraq, were Britain’s major sources of oil. Continued access was required for military security, and the dividends from Anglo-Iranian were a major revenue generator for the Exchequer. “Without the Middle East and its oil,” Foreign Secretary Bevin told the Cabinet Defense Committee, he saw “no hope of our being able to achieve the standard of living at which we are aiming in Great Britain.”

If the British focus narrowed, the shift in outlook and commitments greatly expanded for the United States. No longer would an American President say, as Franklin Roosevelt had said in 1941, that Saudi Arabia was a little far afield. The United States was becoming an ever more petroleum-based society, which could no longer supply its own needs with domestic production. The world war, just over, had proved how central and critical oil was to national power. American leaders and policymakers were also moving toward a much wider definition of national security—one that reflected the realities of the postwar balance of power, the growing clash with the Soviet Union, and the evident fact that the mantle was passing from Britain to the United States, which was now by far the preeminent power in the world.

Soviet expansionism—as it was, and as it might be—brought the Middle East to center stage. To the United States, the oil resources of the region constituted an interest no less vital, in its own way, than the independence of Western Europe; and the Middle Eastern oil fields had to be preserved and protected on the Western side of the Iron Curtain to assure the economic survival of the entire Western world. Military planners did have considerable doubt about whether the oil fields could actually be defended in an extended “hot war,” and they gave at least as much thought to how to destroy them as to how to defend them. But in the Cold War, this oil would be of great value, and everything possible should be done to prevent its loss.

Saudi Arabia became the dominant focus of American policymakers. Here was, said one American official in 1948, “what is probably the richest economic prize in the world in the field of foreign investment.” And here the United States and Saudi Arabia were forging a unique new relationship. In October 1950 President Harry Truman wrote a letter to King Ibn Saud. “I wish to renew to Your Majesty the assurances which have been made to you several times in the past, that the United States is interested in the preservation of the independence and territorial integrity of Saudi Arabia. No threat to your Kingdom could occur which would not be a matter of immediate concern to the United States.” That sounded very much like a guarantee.

The special relationship that was emerging represented an interweaving of public and private interests, of the commercial and the strategic. It was effected both at the governmental level and through Aramco, which became a mechanism not just for oil development, but also for the overall development of Saudi Arabia—though insulated from the wide range of Arabian society and always within the limits prescribed by the Saudi state. It was an unlikely union—Bedouin Arabs and Texas oil men, a traditional Islamic autocracy allied with modern American capitalism. Yet it was one that was destined to endure.17

The End of Energy Independence

Since Middle Eastern oil could not, in the event of war, be very easily protected and was, in the words of the United States Joint Chiefs of Staff, “very susceptible to enemy interference,” how could overall security of supply be assured in a future conflict? This question became a major topic of discussion both in Washington and in the oil industry. Some argued for importing more oil in peacetime in order to preserve domestic resources for wartime. Such was the call in A National Policy for the Oil Industry, a controversial book by Eugene V. Rostow, a Yale Law School professor. A new Federal agency, the National Security Resources Board, made a similar argument in a major policy review in 1948; importing large amounts of Middle Eastern oil would allow a million barrels per day of Western Hemisphere production to be shut in, in effect creating a military stockpile in the ground—“the ideal storage place for petroleum.”

Many advocated that the United States do what Germany had done during the war—build a synthetic fuels industry, extracting liquids not only from coal, but also from the oil shale in the mountains of Colorado and from abundant natural gas. Some were confident that synthetic fuels could soon be a major source of energy. “The United States is on the threshold of a profound chemical revolution,” said the New York Times in 1948. “The next ten years will see the rise of a massive new industry which will free us from dependence on foreign sources of oil. Gasoline will be produced from coal, air, and water.” The Interior Department optimistically declared that gasoline could be made from either coal or shale, for eleven cents a gallon—at a time when the wholesale price of gasoline was twelve cents a gallon!

The more realistic and widespread view in the oil industry was that synthetic fuels were, at best, on the horizon. Still, in late 1947, as the Cold War intensified, the Interior Department called for another Manhattan Project: a huge, crash $10 billion program that would be capable, within four or five years, of producing two million barrels per day of synthetic fuels. As it was, a total of only $85 million was authorized under the Truman Administration for such research. And as time went on, the cost projections became higher and higher, until it was estimated, in 1951, that gasoline from coal would cost three and a half times the market price for conventional gasoline. In the end, it was the ever-growing availability of cheap foreign oil that made synthetic fuels irrelevant and uneconomical. Imported petroleum killed synthetic fuels. And they would remain dead for three decades, until hastily resurrected in response to an interruption in the flow of imported oil.18

In the immediate postwar years, technology was opening new domestic frontiers for exploration and development. Much greater depth was attained in drilling, which increased production. And even more innovative was the development of offshore production. As far back as the mid-1890s, operators were drilling off piers near Santa Barbara, but the wells produced no more than one or two barrels per day. In the first decades of the twentieth century, wells were drilled from fixed platforms in lakes in Louisiana and Venezuela. In the 1930s, drillers had walked into the shallow waters immediately off the beaches of Texas and Louisiana, though with little success. They were only wading distance from land. It was quite another thing to go offshore altogether, into deeper waters of the Gulf of Mexico, out of sight of land. That would require the creation of a new industry. Kerr-McGee, an Oklahoma independent, took the gamble. And a very big gamble it was. The technology and know-how did not exist for building a platform, getting it into position, drilling into the ocean floor—or even for servicing the operation. Moreover, essential knowledge about such important matters as weather (including hurricanes), tides, and currents was either rudimentary or almost nonexistent.

Because of its size, the management of Kerr-McGee reasoned that it did not have much chance to win attractive, “real class-one” onshore acreage against the larger companies. But, when it came to offshore sites in the Gulf of Mexico, there was hardly any competition. Indeed, many other companies thought that offshore development was simply impossible. Kerr-McGee put the pieces together, and on a clear Sunday morning in October 1947, on Block 32, ten and a half miles off the Louisiana coast, its drillers struck oil.

The well on Block 32 was a landmark event, and other companies followed Kerr-McGee’s lead. Yet the buildup of offshore exploration was not as fast as it might have been, partly because of the expense. An offshore well could cost as much as five times more than a well of similar depth onshore. Development was also slowed by an intense struggle between the Federal government and the states over who actually owned the continental shelf. Of course, what they were really fighting about was who would get the tax revenues, and that matter would not be resolved until 1953.19

Given that synthetic fuels would be very expensive and offshore development was only just beginning, was there any other alternative to imported oil? There was. The answer could be seen at night, along the endless highways of Texas, in the bright spears of light that shot up from the flat plains. It was natural gas, considered a useless, inconvenient by-product of oil production and thus burned off—since there was nothing else to do with it. Natural gas was the orphan of the oil industry. Only a fraction of natural gas production was used, mostly in the Southwest. Yet the country appeared to have huge reserves of gas, which could well substitute for oil—or, for that matter, for coal—in residential heating and in industry. But it so lacked in markets that it was sold, on an energy basis, for only a fifth of what oil from the same well would cost.

Natural gas required no complex engineering processes in order to be used. The problem was transmission: how to get it to the markets in the Northeast and the Midwest, where both the large populations and the major industries of the country were to be found. That meant long-distance pipelines, halfway across the country, in an industry for which long distance had heretofore meant 150 miles. But the commercial arguments, compounded by the concerns about national security and dependence on foreign oil, were very compelling. In a judgment that found favor with Defense Secretary Forrestal, the House Armed Services Committee declared that increasing the use of natural gas was “the quickest and cheapest method immediately available to reduce domestic consumption of petroleum” and that, therefore, steel should “be made available for natural gas pipelines in advance of any other use now proposed.”

In 1947, both Big Inch and Little Inch—the pipelines hurriedly built in wartime to bring oil from the Southwest to the Northeast—were sold to the Texas Eastern Transmission Company and turned into natural gas pipelines. The same year, in a project championed by Pacific Lighting, the parent of Southern California Gas, Los Angeles was hooked up by large-diameter pipe to the gas fields of New Mexico and West Texas. That pipeline itself, owned by El Paso Natural Gas, was dubbed “Biggest Inch.” By 1950, the interstate movement of natural gas reached 2.5 trillion cubic feet—almost two and a half times the level of 1946. Without the additional natural gas use, American oil demand would have been seven hundred thousand barrels per day higher.

By then the new petroleum order had been established, centered in the Middle East, and within it, the oil companies were moving at a feverish pace to satisfy the rapidly rising demand in the marketplace—consumption in the United States jumped 12 percent in 1950 over 1949. Oil would prove to be the favored fuel, not only in the United States, but also in Western Europe and later Japan, providing the energy to power two decades of remarkable economic growth. Forged to meet new political and economic realities, the postwar petroleum order was a great success—in fact, it was, in some ways, far too successful. Already, by 1950, it was clear that the problem now facing the industry was not the immediate postwar anxiety of being unable to keep up with demand. On the contrary, as a Jersey analysis in July of that year described the situation, “It appears that in the future, Mid-East crudes available to Jersey may exceed requirements substantially.” What was true for Jersey would be true for the other majors. The Jersey forecast was only a hint of the massive surplus that would confront the industry in the years ahead. In the meantime, even as the new petroleum order was beginning to generate massive profits, bitter battles were already erupting over how these profits were to be divided.20