6

In the previous chapter I explored the relation between self and others. In the present chapter, the focus is on the relation between the present and future. In some cases, and to some extent, the analogy between other selves and future states of the self can be useful.1 We may, that is, look for intrapersonal and intertemporal analogies to interpersonal relations. The questions “If not me, who?” and “If not now, when?” have a common root in magical thinking (Chapter 14). Drawing on the same analogy, La Bruyère observed that “To think only of oneself and of the present time is a source of error in politics.” The economic idea of externalities has a parallel in the idea of internalities (Chapter 17). Economists sometimes treat prudence and altruism within the same conceptual framework. The problem of time inconsistency can arise in intrapersonal as well as interpersonal contexts (see Chapter 18). Although the analogy is endlessly fascinating, it has to be handled with care. It may suggest hypotheses, but does not lend them any support.

Beyond gradient climbing

Freud's pleasure principle (Chapter 4) is the tendency to seek immediate gratification of desires. One manifestation of this tendency is the adoption of the belief one would like to be true rather than the belief that is supported by the evidence. Wishful thinking makes me feel good here and now, even if it may cause me to fall flat on my face later on. Another manifestation occurs in the choice between two actions that induce different temporal utility streams. The pleasure principle dictates the choice of the stream that has the highest utility in the first period, regardless of the shape of the streams in later periods.

More generally, a decision maker, be it an earthworm or a firm, may engage in gradient climbing. At any point in time it scans the nearby options to see whether one of them yields greater immediate benefits than the status quo. The restriction to nearby options is a form of “spatial myopia”: out of sight, out of mind. The restriction to immediate benefits is a form of temporal myopia: the pleasure principle. The earthworm scans the environment to see whether any spot nearby is more humid than the one it is currently occupying and moves to that spot if it finds one. The firm scans the “space” of routines that are close to what it is currently doing to find one that promises better short-term performance and adopts it if it finds one. After a while, the earthworm or the firm may come to rest in a place that is superior (in the short run) to all nearby positions. It has attained a local maximum.

Human beings can do better. Intentionality – the ability to re-present the absent – enables us to go beyond the pleasure principle and take account of the temporally remote consequences of present choices. Planning ahead enables us to make choices that have better consequences than those that would flow from minute-by-minute or second-by-second decisions. In some cases, such farsighted actions may be undertaken to satisfy current needs better, as when an alcoholic forgoes having a drink in a nearby restaurant so that he can buy a whole bottle in a remotely located store at the same price. In other cases, the actions are undertaken to satisfy future needs, as when I save for my old age. Whereas the former kind of foresight is also observed in non-human animals, the latter has usually been thought to be beyond their capacity. Some evidence suggests, however, that primates may be able to plan on the basis of expected rather than actual needs. Be that as it may, acting on the basis of projected needs is obviously a more sophisticated operation.

Let me give four examples of acting on the basis of temporally remote consequences. The first three examples are also discussed in later chapters.

Reculer pour mieux sauter. This French phrase, the rough equivalent of “one step backward, two steps forward,” is illustrated by the fundamental fact of economic life that to invest for greater consumption in the future one must consume less in the present. The agent accepts a state that is inferior to the status quo because it is a condition for realizing a superior alternative later on. Needless to say, this makes sense only if (1) the inferior state allows the agent to survive and (2) the present value of the gains from the superior state are large enough to justify the loss involved in moving to the inferior state.

Waiting. Many wines, although good from the time they are bottled, improve with age. To benefit from this fact, the agent has to be willing to reject an option (drinking the wine right away) that is superior to the status quo because the rejection is a condition for realizing an even better outcome later. Again, deferring consumption might not always make sense, for instance, if the agent does not expect to live long enough to enjoy the improved wine. For a more consequential example, consider the choice of spouse. Rather than proposing marriage or accepting a marriage proposal on the first occasion an acceptable candidate appears, one might wait for somebody even better suited. The risk, abundantly illustrated in world literature, is that nobody better suited might come along.

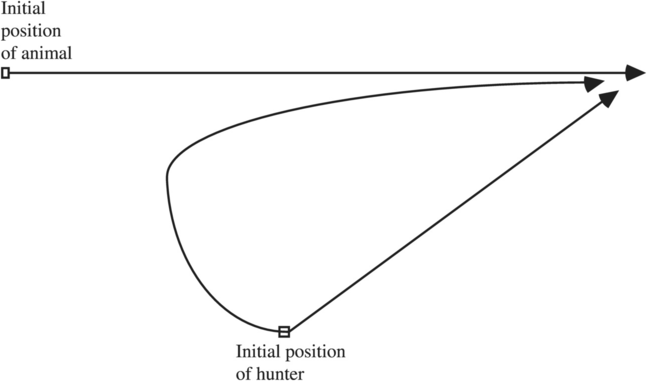

Shooting ahead of the target. To hit a moving target, one should not aim at where it is, but at where it will be at the time of encounter. Similarly, to pursue a moving target, one should aim in a straight line at where the target will be rather than follow the curved path induced by always aiming at its current position.

In Figure 6.1, the hunter, even if he is moving somewhat more slowly than the animal, can catch up with it by going in a straight line toward the point where it will be at some calculable time in the future. If, however, he always aims in the direction of the current position of the animal, following the curved path in the diagram, he will never catch up with it. As we shall see (Chapter 11), natural selection in a changing environment can be viewed in this perspective.

Figure 6.1

Figure 6.1

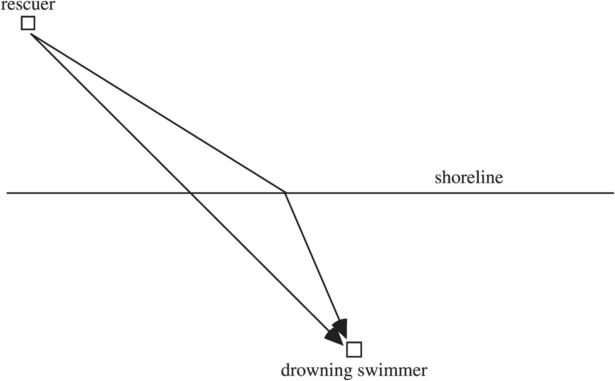

A straight line is not always the fastest way. When trying to reach a stationary target, a straight line is not always the most efficient path. In Figure 6.2, the rescuer might impulsively run straight toward the drowning swimmer until she reaches the shoreline and then swim the remaining distance. If she had paused (but not too long!) to reflect, however, she might have realized that as she can run faster than she can swim, she would reach the swimmer faster by taking an indirect path that, although longer on the whole, has a shorter stretch in the water. We behave in this way when we take a turnpike rather than the road that, on the map, seems to be the shorter. In economic planning such “turnpike behavior” is often optimal.

Figure 6.2

Figure 6.2

Time discounting

The existence of the capacity for long-term planning does not imply that it will be used. For perceived long-term consequences to make a difference for present behavior, agents must be motivated to take them into account. In the language of psychologists, they must be ready to defer gratification. In the language of economists, they must not be subject to excessive time discounting.2 The cognitive and motivational elements are both needed. If future outcomes are shrouded in uncertainty, they cannot motivate present behavior. If they involve risk, their motivating force is also attenuated. The ability of future outcomes to shape present behavior is affected both by the time at which and by the probability with which they will occur. The formal preferences by which they affect choice are, respectively, time discounting and risk attitudes.

As the phrase suggests, time discounting (or myopia) is the tendency to attach less importance to rewards in the distant future than to rewards in the near future or in the present.3 The tendency is pretty universal: “If a hangover came before we got drunk we would see that we never drank to excess” (Montaigne). If given the choice between $100 today and $110 a year from today, most people would probably, even in the absence of inflation, prefer the former. This preference could, however, have a number of sources.

Profit-seeking. Some people might prefer the early reward because they can invest the funds and withdraw more than $110 in a year's time.

Scarcity. Others might take the $100 now because they need the money to survive. Getting a bigger sum later has no value if they expect to be dead by then. Or suppose I have the choice between catching fish in the stream with my hands and making a net that will enable me to catch many more fish. Because I cannot catch fish while making the net, however, the opportunity cost of making the net may be so high that I cannot afford it.

Mortality. Still others might take the smaller reward because they have a disease that entails a 10 percent chance of dying within a year. More generally, when planning for the future we have to take account of the fact that we know that we shall die but not when.

Risk aversion. If the future sum is an expected reward, involving a 50 percent chance of $130 and a 50 percent chance of $90, risk aversion might induce a preference for getting $100 with certainty today.

Pure time discounting. Finally, some people might prefer the early reward simply because it arrives earlier. Just as a big house seen in the distance appears to be smaller than a small house close up, a large sum in the future may appear, subjectively, as smaller than a small sum in the present. In the following, I shall consider only this case.

Is pure time discounting irrational? Suppose a person discounts future rewards very heavily. Rather than getting a college education, which involves a temporary sacrifice of income with a higher income later on, he takes a low-level job with few promotion possibilities immediately after high school. Because he ignores the long-term impact of smoking and of tasty but unhealthy food, he has a short life expectancy.4 If he does not respect the law on moral grounds, prudential considerations will not deter him from violating it. It is quite likely, in other words, that his life will be short and miserable. If this is not irrational behavior, what is?

In my view, pure time discounting, by itself, is not irrational. It may cause the agent's life to go worse than if she cared more about the future, but that may also be true of selfish motivations. Someone who only cares for herself may end up having a sad and impoverished life. As Montaigne said, “He who does not live a little for others hardly lives at all for himself.” We should not for that reason, however, say that selfishness is irrational. I pursue these questions in Chapter 13. Here, I focus on the proper way to conceptualize time discounting. Several approaches, which have radically different implications, are available.

To model time discounting, decision theorists traditionally assumed that people discount future utility exponentially. One unit of utility t periods in the future has a present value of kt, where k < 1 is the per-period discount factor. Exponential discounting has the attractive factor, from a normative point of view, that it allows consistent planning. If one stream of rewards has a greater present value than another at one point in time, it will have a greater present value at all other points in time. Hence the agent is never subject to a preference reversal, which is usually (in the absence of reasons for changing one's mind) taken as a hallmark of irrationality.

Empirically, however, the notion of consistent planning makes less sense. Casual observation shows, and systematic observation confirms, that most of us are frequently subject to preference reversal. We often fail to carry out intentions to save, do exercises in the morning, do our piano practice, keep our appointments, and so on. I may call my dentist on March 1 to make an appointment for April 1, only to call and cancel on March 30, saying (untruthfully) that I have to go to a funeral. To account for these varieties of everyday irrationality (and for a large number of other phenomena) we can replace the assumption of exponential discounting with that of hyperbolic discounting.

Suppose that the discounted present value of 1 unit of utility t periods into the future equals 1/(1 + kt). (In the example below I assume k = 1, but in the more general case, k might be any positive number: the larger it is, the less the agent cares about the future.) Suppose, moreover, that the agent at t = 0 faces the choice between a reward of 10 at t = 5 and a reward of 30 at t = 10. At t = 0 the present value of the former is 1.67 and that of the latter is 2.73. An agent that maximizes present value will form the intention of choosing the delayed reward. At t = 1 the present value of the earlier reward is 2 and that of the later is 3. At t = 2 the values are 2.5 and 3.3; at t = 3 they are 3.3 and 3.75; and at t = 4 they are 5 and 4.29. At some time between t = 3 and t = 4, that is, the earlier reward ceases to be the least and becomes the most preferred option as the result of nothing but the sheer passage of time. It is easy to see, in fact, that the switch occurs at t = 3.5, which is when I call my dentist to cancel the appointment.

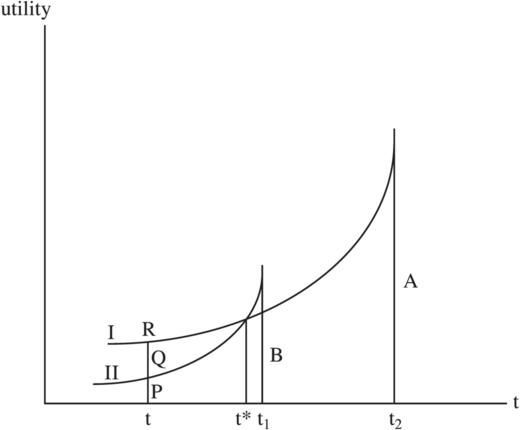

This pattern is even easier to see in a diagram. In Figure 6.3, the agent can either choose the small reward B at t1 or wait until t2 and get the larger reward A. The hyperbolic curves I and II represent the present values of these rewards as evaluated at various earlier times. They are in fact indifference curves (Chapter 10) that represent the trade-off between the time a reward becomes available and the size of the reward. At time t, for instance, the agent is indifferent between getting reward PQ immediately and getting the small reward at t1, and also indifferent between getting PR immediately and getting the large reward at t2. Since at time t the present value of A is larger than that of B, she will form the intention to choose A. Yet because the hyperbolic curves cross one another at t*, a preference reversal occurs at that time and she chooses B instead.5

Figure 6.3

Figure 6.3

Pascal's wager

We can use Pascal's wager to illustrate the relation between exponential and hyperbolic time discounting. Pascal wanted to persuade the freethinking gamblers among his friends that they should bet on the existence of God, since even the smallest chance of eternal bliss would offset the greatest possible earthly pleasures. Pascal's argument harbors many complexities, some of which will concern us in the next chapter. Here I only want to draw attention to a question that Pascal does not mention: does the present (discounted) value of eternal bliss have a finite or an infinite value? If it is finite, the gambler might prefer to take his pleasures on earth rather than wait for the afterlife.

Suppose for simplicity that each period in the afterlife provides 1 unit of experienced utility; that the person expects to die in n years from the present; and, finally, that he discounts future welfare exponentially by a factor of k (0 < k < 1). If God exists and grants him salvation on the basis of his faith, the present value of bliss in the first year after he dies is kn units of utility, that of the second year kn + 1, and so on. As a matter of elementary algebra, this infinite sum (kn + kn + 1 + kn + 2 …) adds up to a finite sum kn/(1+k). Conceivably, at least, this sum might be inferior to the present value of n years of hedonistic living on Earth. By contrast, if the agent is subject to hyperbolic discounting the infinite sum 1/(n + 1) + 1/(n + 2) + 1/(n + 3) … increases beyond any given finite value, implying that if we compare present values any earthly pleasure will ultimately be overtaken by the bliss of salvation. Even if the latter is multiplied by a small probability (as small as you wish) that God exists, the product will still increase beyond any finite number.

Suppose, however, that Pascal's interlocutor is regularly exposed to opportunities to gamble. When considered ahead of time, he prefers to attend mass rather than gamble, because the former will ultimately make him believe and assure him an expectation of infinite bliss. By the logic of hyperbolic discounting, however, the imminence of the opportunity to gamble will induce a preference reversal. He will form the intention to gamble just one more time and then start going to mass. With St. Augustine, he will say, “Give me chastity and continence, but not yet.” Next week, the same reasoning will apply. Thus the very structure of time discounting that ensures that eternal bliss has the greater present value will also prevent the gambler from taking the steps to achieve it.

Weakness of will

As this example shows, hyperbolic discounting may illuminate the problem of weakness of will. With the problem of self-deception (see next chapter), it constitutes a classical instance of paradoxical irrationality. Both weakness of will and self-deception are forms of motivated irrationality, but that feature does not in itself make them paradoxical. Wishful thinking, too, is irrational, but hardly paradoxical. What lends an air of paradox to weakness of will and self-deception is that the person subject to them appears to want and not want, believe and not believe, the same thing at the same time. The paradox has led some thinkers and scholars to deny that these states can exist. Others have argued for their existence, and tried to specify mechanisms that can bring them about. My own view is agnostic, and somewhat skeptical.

A weak-willed (or akratic) person is characterized as follows:

1.The person has a reason for doing X.

2.The person has a reason for doing Y.

3.In the person's own judgment, the reason for doing X is weightier than the reason for doing Y.

4.The person does Y.

Emotions, in particular, are often held to have the capacity for inducing action against the better judgment of the agent. When Medea in Euripides’ play is about to kill her children, she says, “I know indeed what evil I intend to do. But stronger than all my after thoughts is my fury.” In Ovid's version of the play, she says, “An unknown compulsion bears me, all reluctant down. Urged this way or that … I see the better and approve it, but I follow the worse.”

These utterances, like the four statements used to characterize weakness of will, are all ambiguous or underspecified in that there is no mention of when they are supposed to be true. Let us define a strict conception of weakness of will as follows:

1.The person has a reason for doing X.

2.The person has a reason for doing Y.

3.The person does Y, judging at the moment of action that the reason for doing X is weightier than the reason for doing Y.

Imagine a person who has resolved to quit smoking and goes to a party where she is offered a cigarette. She accepts the offer, knowing as she does so that she should not. A person on a diet may accept an offering of dessert knowing as he does so that it is not a good idea. Although there is nothing impossible about this conception of weakness of will, it runs into two empirical problems. It would be hard to establish that the action and the “better judgment” coexisted at the very same moment, rather than that the judgment changed a split second before the action. Also, nobody to my knowledge has specified the causal mechanism by which the desire to do Y acquires greater causal efficacy than the desire to do X.

To bypass these problems we may define a broad conception of weakness of will, which allows the agent's judgment that he should do X and the choice of Y to occur at different moments:

1.The person has a reason for doing X.

2.The person has a reason for doing Y.

3.In the person's own calm and reflective judgment, the reason for doing X is weightier than the reason for doing Y.

4.The person does Y.

Socrates denied that weakness of will in the strict sense was possible. Aristotle, too, came close to suggesting the same thing. He allowed for WW in the broad sense, citing as an example a person whose judgment at the time of action is under the influence of alcohol. Suppose I go to the office party, have too many drinks, offend my boss, and make amorous advances to his wife. At the time, these actions seem the perfectly natural thing to do. Yet ahead of time, had anyone suggested I might act in this way, I would have rejected it as inconsistent with my calm, reflective judgment. If I had been persuaded that my judgment might dissolve in alcohol, I would have stayed away. After the fact, I might bitterly regret my behavior.

This case, shown in Figure 6.4, is a case of temporary preference reversal, not of weakness of will in the strict sense. There are at least three mechanisms that may bring about such changes. One is temporal proximity, as explained in the discussion of hyperbolic discounting. Another is spatial proximity, as illustrated by the phenomenon of cue dependence. This mechanism explains, for instance, many cases of relapse among addicts. Even after years of abstinence, an environmental cue traditionally associated with drug use may trigger relapse. Merely seeing drug paraphernalia on TV may be sufficient. The resolve to go on a diet may be undermined by the sight of the dessert trolley coming around. In these cases, too, the agent chooses according to her conception at the moment of choice of what she most prefers, all things considered. Finally, passions are capable of inducing temporary preference change, by virtue of the fact that they usually have a short half-life (Chapter 8). They may also induce preference reversal by causing the agent to pay less attention to the remote future.6

Figure 6.4

Figure 6.4

We may extend this idea to include temporary (and motivated) changes in the agent's beliefs. On this very broad conception, weakness of will can also result from self-deception (or wishful thinking). Having decided ahead of a party to have only two drinks in order to be able to drive home safely, a person might, under the influence of his desire for a third drink, tell himself, against the weight of the evidence, that it will not make a difference to his driving skills.7 His preference for safe driving remains unchanged, but his belief about the conditions under which he can drive safely has changed. He might also, of course, undergo a temporary preference change, if he decides that having a good time at the party is so important that it offsets the risks (which he may perceive accurately) of drunk driving.

Discounting the past

The impact of expected future events on present choices may depend, as we have seen, on the time at which the agent believes they will occur. The impact of remembered past events on present choice can depend on the time at which they did occur. Some past events, to be sure, fade from memory, but what is the impact of those that do not? Intuitively, we tend to think that recent events have a greater impact, partly but not only because they are more easily remembered. The intuition is confirmed by evidence that in presidential elections, American voters take account of changes in the nation's economic situation under the incumbent government mainly if they occur relatively close to election day, and are little affected by what happened in the first years of the administration.8 They may be said to suffer from “backward-looking myopia.”

Other facts suggest that the impact of the past is more ambiguous. When speaking before a jury, the prosecutor and the defense attorney have to decide whether to place their stronger arguments at the beginning of the presentation or at the end. Although the intuition just cited suggests that they should exploit “the recency effect” and place them at the end, there is also evidence for a “primacy effect” that would support the opposite strategy.9 Since both effects have been demonstrated, what should the speaker do? The so-called “Nestorian strategy” is to place the second-best argument at the beginning and the best at the end, with the least persuasive arguments in the middle.

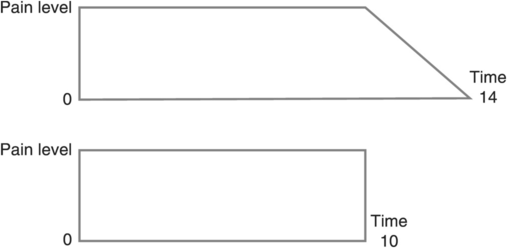

Experiments suggest that we sometimes assess the past using a “peak-end” heuristic. In one experiment, each subject was exposed to a continuous loud and unpleasant sound in two conditions. In the condition shown in the top diagram of Figure 6.5, the sound was consistently loud for ten seconds and then tapered off for four seconds. In the second, the sound was cut off abruptly after ten seconds. When they were asked to choose which sequence they would prefer to experience again, about two-thirds chose the first – objectively more unpleasant – experience. A study where patients were assigned to two colonoscopy procedures that differed in the same way gave a similar result. The proposed explanation for these counterhedonic choices is that the subjects judged their experience (i) by how good or bad it was at its best or worst and (ii) how good or bad it was when it ended. Other experiments also showed “duration neglect”: the duration of the experiences had little effect on how the subjects retrospectively assessed their pleasantness.

Figure 6.5

Figure 6.5

The peak-end effect and duration neglect have also been observed in the recollection of musical emotion, with an additional slope effect. According to the authors of this study, “The duration of … episodes contributes minimally to remembered affect (duration neglect). Listeners rely on the peak of affective intensity during a selection, the last moment, and moments that are more emotionally intense than immediately previous moments to determine post-performance ratings.” This may well be true in general, but some pieces of music, such as Beethoven's Fifth Symphony, certainly illustrate the primacy effect. Another question concerns the lessons that a composer might draw from these findings, assuming that they are robust. Should he maximize the experienced affect of the listeners or their remembered affect? If he chooses the latter, members of the audience may be more likely to listen to the piece again, although their experience may be inferior. If he chooses the former, may we charge him with paternalism?

Motivational versus cognitive myopia

In the last section I made the obvious observation that agents cannot be influenced by their memory of the past if they do not have any memory of it. A similar point applies to the future. For future consequences of present choices to affect these choices, the agent must not only be motivated to take account of them, but also have the cognitive capacity to determine what those consequences will be.10 Thus behavior that appears to be shaped by “motivational myopia” may, in reality, be shaped by a “cognitive myopia.” Commenting on the suppression of the English monasteries under Henry VIII, Hume observed that “there is no abuse so great in civil society, as not to be attended with a variety of beneficial consequences; and in the beginnings of reformation, the loss of these advantages is always felt very sensibly, while the benefit, resulting from the change, is the slow effect of time, and is seldom perceived by the bulk of a nation.”

Tocqueville argued that people in democratic societies are naturally myopic, in the sense of being unable to delay gratification. At the same time, he argued for the existence of a cognitive deficit: “what democracy often lacks is a clear perception of the future, based on enlightenment and experience.” This argument applies with particular force to the benefits to be derived from liberty and the dangers that equality might bring.

Political liberty, if carried to excess, can endanger the tranquility, property, and lives of private individuals, and no one is so blind or frivolous as to be unaware of this. By contrast, it is only the attentive and clear-sighted who perceive the perils with which equality threatens us, and they usually avoid pointing them out. They know that the miseries are remote and are pleased to think that they will afflict only future generations, for which the present generation evinces little concern. The ills that liberty sometimes brings on are immediate. They are visible to everyone, and to one degree or another everyone feels them. The ills that extreme equality can produce reveal themselves only a little at a time … The goods that liberty yields reveal themselves only in the long run, and it is always easy to mistake their cause. The advantages of equality are felt immediately and can be seen daily to flow from their source.

The first phrase I italicize refers to a cognitive deficit in all citizens except for the “attentive and clear sighted.” The second refers to a motivational deficit in (it would seem) all citizens. Even though the temporally distant effects of their present choices appear on the mental screen of members of the intellectual elite, they are not motivated to lend them any weight in their decisions. As for members of the majority, they lack foresight as well as prudence: the two deficits converge.

I argue in Chapter 8 that cognitive myopia can be induced by the urgency of emotion. It can also, however, simply be due to the increased thickness of the fog of uncertainty when we try to peer into the future. In such circumstances, decision makers are often tempted to base their choices on the short-term consequences they can foresee. The 2011 military intervention of Libya was motivated by the clear short-term benefits of getting rid of a dictator, with little thought about who or what would replace him. Similarly, an historian of the Vietnam War writes that “Fixated on short-term expedients and lacking a comprehensive estimate of what the war might cost the United States in the long term, [President Lyndon B. Johnson] focused on the more easily discernible price of withdrawal.”

Many economic models assume that people have “rational expectations,” in the strong sense that agents actually use the models to form their expectations. More weakly, the models assume that agents are not systematically wrong in forming their expectations. The strong version imputes to agents cognitive capacities that they demonstrably do not have. The weak version ignores the fact that some agents may not form any expectations at all, but recognize the pervasive uncertainty about what will happen a few years hence. It also ignores the fact that some agents may form adaptive expectations, as in the cobweb model further discussed in Chapter 17. These expectations can indeed be systematically wrong, but the agents may not be in a situation to learn from their mistakes. People also make other systematic predictive errors that are not corrected by experience. According to one analysis, the best strategy for goal keepers in face of a penalty kick is to stay in the center of the goal, yet in about 94 percent of the cases they throw themselves to one side or the other, perhaps because of “inaction-aversion” (Chapter 8).

Bibliographical note

Rational-choice explanations of time discounting and altruism are offered by G. Becker and C. Mulligan, “The endogenous determination of time preference,” Quarterly Journal of Economics 112 (1997), 729–58, and in C. Mulligan, Parental Priorities and Economic Inequality (University of Chicago Press, 1997). For evidence that primates may be able to plan for future (not currently experienced) needs, see N. Mulcahy and J. Call, “Apes save tools for future use,” Science 312 (2006), 1038–40. Two source books on time discounting and other aspects of intertemporal choice are G. Loewenstein and J. Elster (eds.), Choice over Time (New York: Russell Sage Foundation, 1992), and G. Loewenstein, D. Read, and R. Baumeister (eds.), Time and Decision (New York: Russell Sage Foundation, 2003). I discuss Pascal's wager at greater length in “Pascal and decision theory,” in N. Hammond (ed.), The Cambridge Companion to Pascal (Cambridge University Press, 2004). The neurophysiological evidence for quasi-hyperbolic time discounting is in S. McClure et al., “Separate neural systems evaluate immediate and delayed monetary rewards,” Science 306 (2004), 503–7. Modern discussions of weakness of will take off from D. Davidson, “How is weakness of the will possible?” in his Essays on Action and Events (Oxford University Press, 1980). I comment on his ideas in “Davidson on weakness of will and self-deception,” in L. Hahn (ed.), The Philosophy of Donald Davidson (Chicago: Open Court, 1999). Motivated belief formation is discussed in D. Pears, Motivated Irrationality (Oxford University Press, 1984). I discuss the link between weakness of will and preference reversal at greater length in “Weakness of will and preference reversal,” in J. Elster et al. (eds.), Understanding Choice, Explaining Behavior: Essays in Honour of Ole-Jørgen Skog (Oslo Academic Press, 2006). The evidence for “backward-looking myopia” in American politics is in L. Bartels, Unequal Democracy (Princeton University Press, 2010). Doubts about the political business cycle are expressed in A. Drazen, “The political business cycle after 25 years,” in B. Bernanke and K. Rogoff (eds.), NBER Macroeconomics Annual 15 (2000), 75–137. The cited studies of the peak-end heuristic are D. Kahneman. P. Wakker, and R. Sarin, “Back to Bentham? Memories of experienced utility,” Quarterly Journal of Economics 112 (1997), 375–406, and D. Redelmeier, J. Kart, and D, Kahneman, “Memories of colonoscopy: a randomized trial,” Pain 104 (2003), 187–94. The study of the memory of music is A. Rozin. P. Rozin, and E. Goldberg, “The feeling of music past: how listeners remember musical affect,” Music Perception 22 (2004), 15–39. The comment on Lyndon B. Johnson is from H. McMaster, Dereliction of Duty (New York: Harper, 1997), p. 297. The analysis of the actual and optimal behavior of goal keepers is in M. Bar-Eli et al., “Action bias among elite goalkeepers: the case of penalty kicks,” Journal of Economic Psychology, 28 (2007), 606–21. Other studies yield different conclusions.

1 The phrase “future selves” is acceptable only as a metaphor. The phrase “multiple selves” does not even have that value (in non-pathological cases).

2 In this book, the phrase “a high rate of time discounting” shall mean that future rewards have a small present value. The phrase “a high discount factor” shall mean that they have a large present value. To illustrate and motivate this seemingly strange terminology, assume that the agent is indifferent between three units of reward tomorrow and two units today. The future reward is discounted (reduced) by one-third. The discount factor (the number by which we have to multiply the future reward to get its present value) is two-thirds.

3 Some individuals, such as pathological misers, may attach more importance to future than to present utility. For them, the time to consume is never quite ripe.

4 Fifty years ago many people might have “ignored” these consequences in the sense of being unaware of them. While this is less likely today, they may still “ignore” them in the sense of attaching less importance to them in their decisions. Not infrequently, they may also be in a state of “motivated ignorance” (a form of wishful thinking) about the consequences.

5 There is an alternative, slightly different way of representing hyperbolic discounting. It rests on the intuitive idea that people make a radical distinction between the present and all other times, by attaching more importance to welfare in the current period than to welfare in all later periods. In addition, they differentiate among later periods. In a three-period example, writing ui for experienced welfare in period i, the present value or discounted sum of utility is u1 + b(du2 + d2u3). There are two discount factors involved. Compared to the present, all future utility, regardless of when it is experienced, is discounted by a factor b. In addition, all future utilities are discounted exponentially by a factor d. The present moment has a visceral salience that makes it stand out compared to all others, whereas later periods gradually lose their motivating power by something more akin to an optical illusion. This pattern, called “quasi-hyperbolic discounting,” has in common with hyperbolic discounting proper that it can induce preference reversals. It differs in that the present value of an infinite stream of equal rewards (as in Pascal's wager) has a finite sum. There is some evidence from neurophysiology that quasi-hyperbolic discounting, although introduced only as a useful approximation to hyperbolic discounting, is in fact the more accurate representation.

6 In fact, the preference reversal caused by hyperbolic time preferences may be mimicked by emotionally induced changes in the discounting factor associated with exponential time preferences. Suppose the agent faces the choice between two options, A and B, which offer the respective rewards (2, 5, 6) and (5, 4, 1) in three successive periods. With a one-period discounting rate of 0.8 (and a two-period rate of 0.64), the present values of the two options (as assessed in the first period) are respectively, 9.84 and 8.84. With a one-period discounting rate of 0.6 (and a two-period rate of 0.36), the values are 7.16 and 7.96. Not surprisingly, the agent ceases to prefer the option with the better long-term consequences when emotions cause him to pay less attention to the future.

7 By contrast, if he is concerned with being stopped by the police rather than with having an accident, it is harder to make himself believe that the third drink will not cause the blood alcohol content to go beyond the legal limit. As I argue in the next chapter, even wishful thinking is (somewhat) subject to reality constraints.

8 One would expect a rational and self-interested executive to exploit this fact, by boosting economic growth in election years. The evidence for the existence of a “political business cycle” remains ambiguous, however.

9 Pride and Prejudice, whose draft title was First Impressions, testifies to the force of the primacy effect.

10 Laboratory experiments rarely capture this fact, since subjects are told what the consequences of their choices will be, rather than having to determine them for themselves. Similarly, in experiments designed to capture risk attitudes, subjects are told the likelihood of the various outcomes. As a consequence, experiments may not allow us to distinguish between “motivational pessimism” (risk aversion) and “cognitive pessimism” (counterwishful thinking).