THREE

On December 23, 1913, Congress approved the Federal Reserve Act. Final passage came after several lengthy disputes and many pages of testimony favoring and opposing a central bank. More than thirty volumes of research reported on the findings of the National Monetary Commission.1 Despite the intense discussions, detailed investigation of financial systems that preceded the act, and the number of alternative bills drafted, considered, and dismissed, the act says very little about the broader purposes of the legislation. The title talks of furnishing an elastic currency, affording means of rediscounting commercial paper, and improving the supervision of banking; the act speaks of setting discount rates “with a view of accommodating commerce and business” but mentions no other objectives.

Omission of a broad statement of purpose or policy objective was not an oversight. The act represented a compromise between many different groups that had very different purposes in mind. At one extreme were the proponents of a single central bank, owned by the commercial banks and run by bankers. The group favoring this alternative looked to the European central banks as a model, particularly the Bank of England. Many of the group’s members were bankers or “practical” men, which often meant in the context of the time that they had some idea of the services that central banks rendered to banks but less understanding of the longer-run consequences of central bank operations. They wanted the central bank to damp fluctuations in market interest rates, particularly those caused by the seasonal demand for currency and the financing of crop harvests, and to encourage the development of a broad national market in commercial paper and bills of exchange patterned on the London market. One of their principal aims was to increase the seasonal response, or elasticity, of the note issue by eliminating the provisions of the National Banking Act that tied the amount of currency to the stock of government bonds.2 They believed firmly that a central bank could reduce panics by serving as lender of last resort in periods of distress. The record of the Bank of England in the previous fifty years reassured them that their beliefs were well founded.

At the opposite extreme were those who opposed a central bank of any kind. The main economic content of their argument was that a central bank is a monopoly, but they did not oppose monopoly as such. They feared or claimed that the monopoly would be run for the benefit of the bankers, particularly J. P. Morgan and other New York bankers. Instead of proposals to avoid a “bankers’ monopoly” they produced evidence of concentration, interlocking directorates, and control of financial institutions, railroads, and other enterprises in hearings before the Pujo Committee and in that committee’s final report.3 However, the Pujo report made few recommendations, was silent on the main issues involved in the discussions of banking reform, and had greater influence on the designers of the Federal Trade Commission than on the designers of the Federal Reserve System.

Proponents and opponents of a central bank clashed over the recommendations of the National Monetary Commission. Legislation drafted at the end of the Taft administration in 1912 embodied many of the principles proposed by the commission. The chairman of the commission, Senator Nelson Aldrich, was a New York Republican. His plan, the Aldrich plan, was unacceptable to the Democrats and opposed in their platform for the 1912 election. They objected much more to the organization of the system and the centralization of power in the hands of the larger banks than to the chartering of a bank to discount commercial paper and issue currency not tied to government securities.

The 1912 election shifted control of Congress to the Democrats. Many Democrats were willing to accept a central bank only if it was under political control. Some members wanted semi-independent regional banks. A month after his election, President-Elect Wilson met with Carter Glass, the new chairman of the House Committee on Banking and Currency. Wilson proposed a mixture of private and public control (Glass 1927, 81–82).4 His legislative proposal to Congress, on June 23, 1913, included that recommendation and urged that control “be vested in the Government itself, so that the banks may be the instruments not the masters of business and of individual enterprise and initiative.” The final structure included Wilson’s compromise—a politically appointed Federal Reserve Board in Washington and regional banks in principal centers, run by bankers, with no clear division of authority between the two. As part of the compromise, Wilson proposed a Federal Advisory Council consisting of bankers, appointed by the reserve banks, to serve as advisers to the Board. As with the First Bank and Second Bank of the United States, Congress did not want to grant a permanent charter, so the initial charter was for twenty years. Permanence was not granted until the McFadden Act of 1927.

In its early years the Federal Reserve faced three major challenges. First, an unanticipated war brought a large increase in gold and removed the gold standard as the monetary system of the developed world. The Federal Reserve had a small portfolio, so it had no means of controlling the resulting inflation, even if it wished to sterilize the inflow. Second, the compromises that enabled a majority to support passage of the act shifted the argument over government or private control without resolving it. In the System’s early years, frequent conflicts broke out between the reserve banks and the Board as both sides struggled to gain control. Third, the intent of the principal proponents was not realized. They expected to create an institution capable of preventing inflation, responding to banking crises, and financing exports of grain, cotton, and other primary products. Instead they created a largely passive bank, dependent on revenues from member bank discounts but with limited influence over the volume of discounts. The real bills doctrine left the initiative to commercial banks. The Federal Reserve’s main channel of influence—the discount rate—was a penalty rate. But raising interest rates was unpopular and provoked concerns about bankers’ domination of the economy.

The early experience of the Federal Reserve induced it to abandon, or modify, the principles underlying the act. As noted, the international gold standard ended when the war started. War finance conflicted with the penalty rate, so the Federal Reserve abandoned it. Political concerns and mistaken policies prevented return to a penalty rate. And the more thoughtful among the early leaders began to question the central tenets of the real bills doctrine.

Wartime experience and the postwar boom, recession, inflation, and deflation convinced many that a passive strategy was inappropriate. Less than a decade after it was established, the Federal Reserve began to search for a more active approach.

THE FOUNDERS’ RATIONALE

The House report on the Glass bill accepted that centralization of banking resources is the “root of the central banking argument” but concluded that in a country as large as the United States “equally good results can be obtained” by several federations.5 The report makes it clear that the House Banking Committee expected the regional reserve banks to function cooperatively but independently and to achieve the advantages of central banking without acquiring the monopoly powers of a single central bank. The striking feature of the report, however, is the extent to which the congressmen who approved it viewed the proposed system as a large association of banks able by pooling gold reserves to take better advantage than the individual national banks of the note issuing and discounting privileges that the national banks possessed. In addition to providing a new bank of issue, Congress made sure that the act improved the procedures for issuing notes by both broadening the definition of acceptable collateral and removing government bonds from the list of acceptable collateral.

Virtually every discussion of banking reform commented on the frequency and severity of United States banking crises. The desire to reduce the frequency and severity of crises—five in the previous thirty years—is a main point of agreement in all the reform plans. All proposals recognized that a central bank could serve as lender of last resort in a banking crisis.

Since there was no established lender of last resort under the National Banking Act, banks attempted to protect themselves against runs or currency demands by holding gold or currency reserves.6 If all banks sought to increase their gold holdings simultaneously, short-term interest rose as high as 100 percent annually. To reduce the demand for gold, clearinghouse associations or groups of bankers pooled resources to provide payment facilities during periods of stress. Such private facilities had to assume the risk of defaults. A central bank that pooled reserves and lent during a panic would provide “elasticity” at lower cost. Hence bankers were eager to shift responsibility for maintaining the payments and clearing mechanism to a central bank, and there was wide support for this reform.

A second meaning of elasticity referred to seasonal fluctuations. Proponents expected a central bank to reduce seasonal fluctuations in interest rates, principally during the autumn marketing of the harvest. Under the prevailing system, interest rates rose and the dollar appreciated within the gold points when foreigners borrowed and purchased dollars to buy grain. New York banks sold holdings of British bills to smooth the seasonal fluctuation in exchange rates, but large seasonal swings remained until after the Federal Reserve was established (Warburg 1930; Myers 1931; Miron 1986).

The two types of inelasticity had a common source. The National Banking Act tied note issues to government bonds. Hence if banks expanded up to the limit set by the note issue, note issues could not expand further in response to seasonal or cyclical demands. A central bank empowered to discount real bills would remove this inelasticity and finance the crop movement. Currency would be more elastic.7 John U. Calkins, later governor of the Federal Reserve Bank of San Francisco, subsequently stated the contemporary view of the relation between elasticity and real bills: “Probably the most important effect of the Federal Reserve Act was to set up the machinery necessary to provide elastic currency; elastic in that it would be based on self-liquidating credit instruments arising out of the production and distribution of commodities. An obligation of the United States does not represent a transaction of this character …to the extent such obligations back the currency such currency is fiat currency” (Federal Reserve Governors Conference, May 1922, 143–44 [hereafter cited as Governors Conference]).

Authority to discount real bills was seen by many at the time as the main improvement of the new legislation.8 Many bankers shared Paul M. Warburg’s view that the Federal Reserve could prevent wide swings in interest rates without risking inflation if it purchased real bills.9 Reliance on real bills also freed the credit system from dependence on the call money market and thus on credit to stock exchange brokers and dealers who financed their positions in that market. Leading economists such as A. Piatt Andrew, H. Parker Willis, J. Laurence Laughlin, and Horace White also advocated the real bills doctrine.10 These economists believed that credit would be adjusted to the needs of trade if banks invested in commercial and agricultural loans and avoided bonds, real estate, call money, and other speculative assets (Mints 1945, 206–7).

Mints (1945, 251–53) adds three additional benefits the founders expected the Federal Reserve to bring. First, bank reserves, mainly gold reserves, would be pooled and therefore available for lending when needed. Second, a bill market would replace the call money market, as in London. The call money market provided credit based on stock exchange collateral and hence depended on a speculative asset. The bill market depended on real bills, particularly bills arising from the financing of foreign trade. Third, improvement in the check clearing system would reduce the number of banks charging fees for clearing checks. The Federal Reserve instituted collection at par at the reserve banks but did not, initially, make par collection a condition of membership.

Section 15 of the Glass bill (section 14 of the act), titled “Open Market Operations,” authorized the Federal Reserve banks to engage in such operations in any of the assets acceptable as collateral for rediscounts and to purchase and sell gold and government bonds. The House report on the Glass bill noted that the purpose of open market operations was to enable the “Federal Reserve banks to make their rate of discount effective in the general market at those times and under those conditions when rediscounts were slack and when therefore there might have been accumulation of funds in the Reserve banks without any motive on the part of member banks to apply for rediscounts or perhaps with a strong motive on their part not to do so” (Krooss 1969, 3:2317–18). The Senate report saw open market operations as a means of developing a market for bills, thereby reducing the variability of rates, the risk premium, and the average level of market rates.11

None of the reports discusses the effect of changes in money on prices or pays much attention to problems of inflation or deflation. The effects of money on prices were not unknown to Congress. Silver agitators had pressed the point during the deflation of the seventies and eighties. The lengthy report of the Jones Commission (1877) had discussed the issue and concluded that an inconvertible paper money was subject to government control and should be allowed to expand with population so as to keep the price level constant.12 The quantity of gold or convertible currency, on the other hand, could not “be greater than such an amount as may be requisite to maintain the prices …at a substantial parity with the prices of all other countries using the same kind of money” (Krooss 1969, 3:1866).13 Yet none of this found its way into the act or influenced the reports of the House or Senate committee on the amended Glass bill.14

A principal reason for the omission is the Gold Standard Act of 1900 that legally established the gold standard as the United States monetary standard. The United States was thought to be part of the international gold standard that determined the stocks of money and the price levels in all member countries. However, after the start of the European war but before the effective beginning of the Federal Reserve System, all the principal gold standard countries suspended the gold standard. It was never reestablished in its prewar form.

The intent of the legislation was very different from the way the System evolved. The original conception was of a relatively passive system. The price level would be controlled mainly by gold movements and changes in foreign exchange. Seasonal and cyclical movements in demand for credit would increase or reduce demand for rediscounts at Federal Reserve banks. Much of this activity, it was believed, would take the form of changes in the volume of rediscounts of bills of exchange or acceptances initiated by banks. The Federal Reserve would not be entirely passive, however. Its active role, like that of the Bank of England, would consist mainly of raising or lowering the discount rate in ordinary times and providing emergency credit to prevent or respond to a financial panic. The discount rate would be a penalty rate, so in ordinary times bankers would keep discounts to a minimum.

FIRST STEPS AND CONFLICTS

The new system took nearly eight months to get organized. A main reason for the delay was that members of the Board and governors of the reserve banks could not be appointed until the size and number of Federal Reserve districts had been set. The act specified that no two members should come from the same district and required that there be at least eight and not more than twelve districts, each with a Federal Reserve bank in a principal city. Decisions about size, location, number, and boundaries were left to an organizing committee consisting of the secretaries of the treasury and agriculture and the comptroller of the currency.15

These decisions were contentious, political, and time consuming.16 By April 2, 1914, the locations were decided, although appeals continued for more than a year.17 By mid-May the twelve reserve banks began to organize. Almost ninety days passed, however, before Charles S. Hamlin, Paul M. Warburg, Frederic A. Delano, W. P. G. Harding, and Adolph C. Miller took their oaths of office on August 10 as the first appointed members of the Federal Reserve Board.18 The president designated one of the members as governor and one as vice governor for renewable one-year terms. The secretary of the treasury was ex officio chairman of the Board, but the governor was the chief operating official of the Board. Hamlin served as governor until 1916, when Harding replaced him. The two remaining members of the seven-person board, Secretary of the Treasury William G. McAdoo and Comptroller of the Currency John Skelton Williams, were ex officio members who had taken office earlier.19

The twelve reserve banks opened on November 16, 1914, eleven months after passage of the act.20 Secretary McAdoo’s announcement of the opening said in part: “They will put an end to the annual anxiety from which the country has suffered and would give such stability to the banking business that the extreme fluctuations in interest rates and available credits which have characterized banking in the past will be destroyed permanently” (Board of Governors File, box 659, November 15, 1914).

Tension between the Board and the reserve banks began before the System opened for business. Two factions formed within the Board. Delano, Miller, and Warburg worried about Treasury control and loss of independence. They distrusted the Treasury group—Hamlin, McAdoo, and Williams. Harding was in the middle. Typical of the reserve banks’ concerns is a letter from a Chicago director H. B. Joy (president of Packard Motor Company), to Frederic Delano: “I have a little feeling—in fact it is growing on me—that the Federal Reserve Board in Washington is inclined toward dominating the District Banks” (Board of Governors File, box 659 October 10, 1914). Warburg described the problem. Dominance by the Board would allow political considerations to dominate decisions about interest rates. Dominance by the reserve banks “would render a concerted discount policy …an impossibility and reduce the Board to a position of impotence” (Warburg 1930, 1:473–74). To resolve some of the issues and coordinate the reserve banks’ activities, the organizing committee recommended appointment of an executive council of the banks’ governors. This is the origin of the Conference of Governors, later the Presidents Conference, that still continues (Board of Governors File, box 659, October 13, 1914).

The dominant personality in the early days of the System was Benjamin Strong, first governor of the Federal Reserve Bank of New York. Strong’s early views were the views of a sophisticated banker, with little formal training, who had gained enough understanding of the functioning of the domestic and international payments mechanisms to be ahead of most of his contemporaries. He saw the Federal Reserve Act as an opportunity to expand the international operations of United States banks, particularly New York banks, and like Warburg, he believed that the development of the market for bills of exchange and acceptances was the means to accomplish this end in a manner consistent with the act. Throughout his life he remained a proponent of fixed exchange rates and the gold standard and an opponent of devaluation or revaluation of currencies and of inflation. In practice, this meant that he accepted deflation when required and came to regard it as the price of international stability.21

Strong’s mature views on the gold standard and on monetary policy reflected his experience in the twenties. His prewar policies can be described succinctly as an attempt to recreate Lombard Street on Wall Street, with the Federal Reserve System, particularly the New York bank, playing the role of the Bank of England.22 He regarded the twelve reserve banks as eleven too many. The appropriate number was one, he wrote. And he believed it was a major defect to issue Federal Reserve notes as obligations of the government. Government note issues were too reminiscent of greenbacks and other fiat money (Chandler 1958, 34–35, 37).23 Like Warburg, he accepted that real bills should be the base for expansion. To that end he worked to develop and strengthen the money market. One of his first appointees to the New York bank was an American expert on the operation of the London bill market. This effort to develop a market for banker’s acceptances and bills of exchange as the principal means of affecting money market interest rates and to replace the call money market was renewed in the 1920s but did not succeed (Warburg 1930, vol. 2, chap. 12; Burgess 1964, 219). Early in his career as governor, he favored compulsory membership of state banks as a means of centralizing reserves. His views on discount policy read very much like pages from Bagehot and are not noticeably different from British views at the time.24

The first task was to organize and begin operations. For Strong this meant not only staffing the New York bank but organizing the System. Since he regarded the Board as a political agency and saw the banks as the business end of the System, 25 Strong moved to enlist the support and cooperation of the other reserve bank governors so as to make the banks the dominant partner. His opportunity came very quickly. The Board called a meeting of the governors for December 10–12 to discuss common problems. The governors used the meeting to organize a permanent Governors Conference, with Strong as chairman.

From the start, the Governors Conference tried to control operations. At its first meeting, the governors discussed how the reserve banks would conduct open market operations.26 One of the main issues was whether each bank would operate independently, as prescribed in the law, or whether they would operate collectively, as required for centralized control. Early in 1915, at Strong’s suggestion, the banks agreed to combine operations in both the open market and acceptance accounts to avoid any effect of competitive purchases on market rates. Although effects on the market were recognized, purchases were made principally to increase the earnings of the reserve banks and were allocated to the individual banks in part based on their need for earnings. Reserve banks retained the right to purchase independently (Anderson 1965, 8; D’Arista 1994, 22). Not all the governors were satisfied. Some claimed that New York did not buy enough, so their earnings were held down.

The reserve banks also purchased the 2 percent bonds that continued to serve as collateral for national banknotes. The aim was to replace national banknotes with Federal Reserve notes. At first purchases were made by the individual reserve banks for their own accounts. By 1917 wartime expansion of the reserve banks reduced pressures to increase earnings, so the banks centralized open market purchases of the 2 percent bonds in New York. Concern for earnings returned, however, in the early 1920s and in the mid-1930s. The reserve banks again acted independently in the early 1920s until a new agreement was reached. Centralization of open market operations and the decision about participation remained as problems until the Banking Act of 1933 amended section 14.

The Board also sought control. One of its earliest acts was to rule that the reserve banks could not announce or change discount rates until they had been approved by the Board (letter of Parker Willis to all reserve banks, Board of Governors File, box 1239, November 18, 1914). The Board based its order on the provision of section 13 that gave the reserve banks power to establish rates “subject to review and determination of the Reserve Board.” The governors chose to interpret “review and determination” as pro forma but the Board insisted that discount rates were subject to the Board’s “determination.”27 Early in 1915 the Governors Conference approved a resolution giving the reserve banks sole power to initiate discount rate changes “without pressure from the Federal Reserve Board” (Chandler 1958, 71).

Initially, discount rates were set above prevailing market rates; they were penalty rates to provide discount facilities in periods of market malfunction, as proposed by Bagehot.28 This principle was in conflict both with the political desire for lower interest rates during the 1914–15 recession and with the desire of the reserve banks to increase earnings.29

Earnings depended on membership. The act required approximately 7,500 national banks to be members, but state-chartered banks had a choice. Among the obstacles to membership were requirements for par collection of checks cleared at Federal Reserve banks and for holding reserves at Federal Reserve banks without earning interest. As of June 30, 1915, only seventeen of nearly twenty thousand state banks had elected to join. A year later state bank membership had increased only to thirty-four.

Partially offsetting these increased costs of membership, the act broadened the powers and reduced the reserve requirement ratio for national banks.30 Cagan (1965, 140) estimates the reduction as 13 percent in November 1914, when the System started operations. This reduction was partially offset in subsequent years by the requirement that member banks deposit more of their required reserves at Federal Reserve banks. In June 1917, by law all required reserves were held at Federal Reserve banks; vault cash was excluded from reserve computation.31 The legislation increased gold held by the Federal Reserve in excess of requirements by $300 million.32

Strong, and also Warburg (1930, 2:150–52), regarded the centralization of reserves as critical to the success of the System. Failure to deposit reserves at the reserve banks meant that gold holdings were dispersed, as they had been before the act. Without centralization, the System would be in a weak position to respond if the gold inflow from Europe reversed at the end of the war. Even if the gold remained, Warburg believed, the System required a larger gold reserve so that it would not be forced to contract the note issue in recessions as eligible paper declined. A larger stock of gold could be used to maintain the note issue.33 After June 1917, vault cash no longer counted as part of reserves, so banks deposited more of their gold at the reserve banks.

Gold flows in 1915 reversed the direction of change in interest rates. Early in January, discount rates followed market rates down. Interest rates continued to fall slowly through the first year of operations. The Board was quick to claim credit. Governor Hamlin wrote that by merely opening the doors, the steadying effect of the act became apparent in the market (Board of Governors File, box 1239, December 17, 1915). The reserve bank governors were more skeptical. When the Board asked all reserve banks to describe the effect of the new system, most attributed the decline in interest rates to gold inflows and the increase in gold reserves. Chairman John Perrin (San Francisco) wrote that there was “very little tangible evidence that the establishment and operation of the Federal Reserve bank has influenced rates in any important way.” Pierre Jay, chairman at New York, wrote that the new system had “no effect whatever” (letters, Board of Governors File, box 1239, December 11 and 13, 1915).

Although the governors invited the Board to send representatives to their meetings, and they sent summaries to the Board, the Board regarded the Governors Conference as a rival organization that weakened its authority by operating independently. It resented decisions by the governors to meet at reserve banks instead of in Washington. It was determined to prevent the governors from meeting too frequently or acting independently.

The Board decided to take control after the Governors Conference criticized the Board for “an exercise of pressure” on the reserve banks. It sent a letter to each of the governors suggesting that the governors hold no more than three or four meetings that year. Although the Board approved $12,900 in expenses for the most recent meeting, it told the governors that their expenditures were too large. The Board did not object to informal discussions among the governors, but “a permanent organization, the appointment of an executive committee, and the election of a paid secretary, are matters …of doubtful propriety and beyond the scope and powers of the Federal Reserve banks as defined in the Federal Reserve Act” (Board Minutes, January 20, 1916, 79). The creation of a standing executive committee “might create the impression that certain banks …had delegated certain powers to a definite committee” (80). Responding to the governors’ criticism, the Board replied that the governors had “assumed powers which they do not possess …when they undertook collectively to direct or to suggest to the Federal Reserve Board the manner of its exercise of the powers conferred upon it by the Act” (81).34

The Board won the first contest, but the issues of control and power were put aside, not resolved. Late in July the secretary of the Governors Conference notified the Board that the governors planned to meet on August 15. By this time Harding had replaced the conciliatory Hamlin as governor (Katz 1992, 119). Harding responded that the Board did not want a conference held and that in the future conferences could be held only if called by the Board. The Treasury opposed a conference, Harding wrote, and, he added, “plans for the proposed meeting should be abandoned…. [I]n matters which concern interbank relations and operation of the Federal Reserve banks as a system, authority is vested by law solely in the Federal Reserve Board” (Board Minutes, July 25, 1917, 99–101). McAdoo attended the meeting and concurred in the decision. He urged the Board to keep the Federal Reserve banks in hand. To rein in the banks, he had considered appointing five additional government directors to the banks’ boards, but he postponed the decision pending a favorable resolution of the dispute.

The following week the Board formally adopted the resolution discussed in the letter to the reserve banks. There was to be no permanent organization and no Governors Conferences unless called by the Board. No further conferences were held until November 1917.35

The Board and the reserve banks also clashed over the obligation of one reserve bank to discount for another and the rate to be charged for interdistrict borrowing. The intent of the act was to pool gold reserves by permitting interdistrict borrowing, thereby smoothing regional demands for reserves and borrowing associated with crop movements. The Board had authority under the act to set the rates for interdistrict loans. Strong disliked the provision and sought to limit its scope by permitting the lending bank to set the rate on borrowings (D’Arista 1994, 19). The Board members insisted that this was their responsibility, and they prevailed.

In March 1915 the Board established interdistrict rates. No transactions were made until 1916, when rates were set by the Board on each transaction. In the fall of 1920 the Board reestablished a common rate for interbank rediscounts related to the discount rate on member bank borrowing.

POLICY PROBLEMS

Almost from its founding, the System faced a series of major policy problems. First there was an outflow of gold before the reserve banks opened, as foreigners sold dollar securities at the start of the war in August 1914. Exports declined for lack of shipping because German and British ships that had carried much of the freight withdrew. Commodity prices, particularly for exportables, fell sharply. The initial wartime problems were severe enough to send the dollar above five dollars per pound sterling, well above its intervention point. The New York Stock Exchange and most foreign stock markets closed to hinder sales of securities and demands for gold.

Soon after the reserve banks began operations in November, a gold inflow replaced the outflow and produced monetary expansion and inflation. Wartime inflation, resulting from the financing of Treasury bond sales, soon followed. After the war there was the difficult task of establishing independence from the Treasury and developing an anti-inflation policy. By 1920 the System had to deal with its first recession. The System’s response to this series of events—the discussions, the proposals for action, and the actions themselves—reveals the policy approaches and understanding of the Board members and governors at the time and the flaws in the act.

The Federal Reserve System was not fully organized when war started in Europe, so it had a minor role in responding to the gold outflow. In September the Treasury issued emergency currency, authorized under the Aldrich-Vreeland Act of 1908.36 One of the Federal Reserve’s first actions was to oppose issuance of additional Aldrich-Vreeland currency. It worked with the Treasury to organize a group of bankers that subscribed $108 million to redeem United States loans abroad. The organization of the fund may have helped to restore calm; only $10 million was drawn.

Gold Flows

Within a few months of the start of the European war, exports increased and gold flowed to the United States in payment. In 1914 the United States held 19 percent of the world’s monetary gold stock. By 1918 its monetary gold stock had increased by 65 million ounces, more than $1.3 billion at the official gold price, $20.67 per fine ounce. The increase was 88 percent of the United States monetary gold stock in 1914 and more than 16 percent of the world’s prewar monetary gold (Schwartz 1982, tables SC7 and SC10).37

The Federal Reserve followed gold standard and penalty rate rules by reducing discount rates as market rates fell. By mid-December 1914 it had lowered discount rates at all reserve banks. By February 1915, rates at most reserve banks were two percentage points lower than on opening day.38 Market rates rose briefly in the spring, perhaps in anticipation of the expiration of Aldrich-Vreeland currency issues on June 30. The Board issued a press release urging the reserve banks to “discount as liberally as prudent” (Board of Governors File, box 1239, January 21, 1915). No problems occurred, and interest rates resumed their decline.

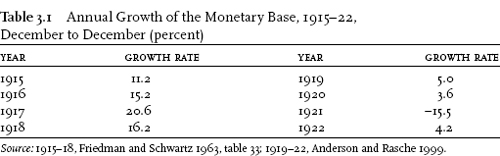

The gold inflows substantially increased the monetary base. Table 3.1 shows annual rates of increase in the base from 1915 to 1922. The Federal Reserve was at first powerless to stop or offset the increases even if it had chosen to abrogate gold standard rules by selling securities. The open market portfolio of government securities at the end of 1916 was only $55 million.39 In fact, the System made small net purchases of government securities in 1915 and 1916 and larger net purchases after the United States entered the war in April 1917.40 Many of these purchases were made to increase the reserve banks earnings.41

Alarmed at the increase in bank reserves and unable to get Congress to permit changes in reserve requirement ratios, the Board began 1917 by urging all reserve banks to let their aggregate acceptances decline by $40 million to $50 million, 20 to 25 percent of their holdings (Board of Governors File, box 1239, January 19, 1917). Several of the reserve banks ignored the request to maintain earnings.

Discount rates remained mostly unchanged until late in the year. The Board confined its activity to simplifying the rate structure. Reserve banks were requested to post no more than seven discount rates by type and maturity and to unify the rate structure across districts. The reserve banks’ responses to the request show the diversity that prevailed at the time in the United States.42

Wartime Finance

Once the United States entered the war, government spending increased. The nation advanced $7.3 billion to its allies during the war and an additional $2.2 billion after the war (Friedman and Schwartz 1963, 216). Effective income tax rates increased sixfold from 1916 to 1918, but the increased revenue was much less than the increased spending, so the Treasury had to finance relatively large deficits (Bureau of the Census 1960, 716).43 Military spending increased from less than $1 billion in fiscal 1916 to an average of $15 billion a year for the fiscal years ending June 1918 and 1919.

The war reshaped the Federal Reserve System in many ways. Most foreign governments suspended the gold standard, so it no longer served as a guide to policy. The System abandoned the penalty discount rate in the interest of war finance. The number of state member banks rose to more than a thousand by 1919, and they included the largest state-chartered banks, with 40 percent of the assets of all state-chartered banks (Bureau of the Census 1960, 633). Wartime (and prewar) changes made the System more like a central bank, as in World War II. Independence was sacrificed to maintain interest rates that lowered the Treasury’s cost of debt finance. The System became subservient to the Treasury’s perceived needs.

The Federal Reserve’s main wartime activity was selling Treasury bonds. The New York bank wanted to replace the existing Independent Treasury System, carried over from the nineteenth century, by serving as fiscal agent for the government. Its wartime activities, and those of the other reserve banks, included selling almost half of the debt issues. It succeeded in convincing the Treasury that the Independent Treasury System was redundant. In 1920 the New York bank was designated fiscal agent, and the Independent Treasury System ended.

Wartime finance consisted principally of a series of Treasury bond drives or Liberty Loans. The governors of the reserve banks served as chairmen of the committees organized in each district to sell Treasury bonds to the nonbank public. Since the amount borrowed was large relative to the size of the country or previous credit demands, the System ensured the success of the four wartime Liberty Loans by making two types of loans. Short-term loans at preferential discount rates encouraged banks to buy short-term Treasury certificates during the interval between bond drives. Initially the discount rate on these loans in New York was 3 percent for fifteen days and 3.5 percent for sixteen to ninety days. Rates rose to 3.5 and 4 percent in December 1917 and to 4 and 4.5 percent in April 1918, where they remained until November 1919.44 Loans were also made to encourage banks to stretch out the public’s payments for purchases of Liberty Loan bonds over $1,000. The latter was known as the “borrow and buy” policy. Its original intent was to avoid a short-term contractive effect on the money stock and interest rates as buyers drew down their balances to make payments to the Treasury (Governors Conference 1917, 233). Later it became a marketing device for the bonds, since buyers could defer payments for as much as a year from time of purchase.

The Treasury’s borrowing tested the System’s ability to pool reserves. By far the largest part of the Treasury’s short-term borrowing was in New York, so the New York bank was under pressure to finance the purchases. The Board urged other reserve banks to buy acceptances from New York to relieve the strain on its reserve position, and New York renewed the request at the November Governors Conference. All banks except Kansas City, Chicago, and Atlanta agreed to buy acceptances to earn interest for their banks and thereby supply additional gold reserves to New York.

The intent of the Treasury’s policy was that sales of certificates would be retired out of the proceeds of the Liberty Loans. From April 1917 to October 1919, the Treasury sold $6 billion of tax anticipation certificates and $19 billion in anticipation of bond and note sales. The intent was not realized. A large volume of certificates remained outstanding at the end of the war. The Treasury opposed raising short-term rates to refund the certificates as they came due. It expressed concern not only that higher shortterm rates on certificates would carry over to long rates, lowering bond prices, but also that an increase in rates would abrogate commitments made to purchasers of Treasury bonds under the borrow and buy policy.

By offering discounts at a preferential rate on Treasury certificates, the Federal Reserve abandoned the penalty rate, one of the main principles on which it was founded. Member banks could borrow at a preferential rate below the rate paid on the Treasury certificates or Liberty bonds, so borrowing became profitable.45 Penalty rates for other types of borrowing remained, but most borrowing was at the preferential rate, so higher rates had no effect. One consequence was that state banks membership increased, as noted earlier. Another consequence was that much of the collateral for borrowing was Treasury debt, contrary to the spirit of the Federal Reserve Act.

Table 3.2 compares the interest rates at which the Treasury sold Liberty bonds to the preferential discount rates at New York. Congress set the rate on the First Liberty Loan below the market rate on savings deposits. The intention was to avoid a drain of existing savings into war bonds (Warburg 1930, 2:12). On May 22, 1917, a week after the borrowing campaign began, New York introduced the preferential discount rate. The other banks followed within a few weeks. The decision reflected concern about the ability to sell the issue at the low interest rate Congress set (Wicker 1966, 14).46

The preferential rate enabled the Treasury to borrow on favorable terms between bond drives. The Treasury sold short-term certificates to the banks. The member banks paid by crediting the Treasury’s account at their banks and retained the deposits until the Treasury drew on its balances. Treasury balances were not subject to reserve requirements, but after they were spent, the money returned as private deposits subject to reserve requirements.47 The preferential discount rate allowed the banks to meet this obligation at low cost. The preferential rate soon became the modal borrowing rate. The Federal Reserve continued the practice until December 1919, after the war ended and the fifth and final war loan, the so-called Victory Loan, had been sold.48

The System considered direct purchases to be “inflationary.” To avoid making open market purchases, it encouraged banks to offer installment loans to nonbank purchasers on favorable terms. Most commentators point out (correctly) that it is no more inflationary for the Federal Reserve to buy the bonds directly (or in the open market) than to lend money to the banks at below market rates so that banks can either purchase the bonds or finance the public’s purchases. The increase in the monetary base is the same in both cases. However, the distinction was important to the Federal Reserve and many others who shared the real bills framework. Central bank purchases of government securities expand money (or credit) based on speculative paper. This paper would have to be eliminated after the war to restore the central bank’s reputation. Although the members recognized that it would be difficult to reduce member bank indebtedness by restoring a penalty rate in the face of almost certain Treasury opposition, far more difficult would be postwar direct sales of Treasury obligations by the reserve banks with the secretary and the comptroller on the Board. Further, currency issues had to be backed by gold and real bills. Treasury securities and commercial paper were not close substitutes for this reason.

By 1918 most of the Liberty Loans sold in the secondary market at a small discount. To raise their prices, Congress, in approving the Third Liberty Loan, permitted the Treasury to purchase not more than 5 percent of each outstanding issue in the market. Purchases were made at the market price and financed by short-term certificates subject to preferential rates for borrowing from the reserve banks. The effect was to lower the average maturity of the debt and to increase the incentive for the Treasury to maintain low interest rates on Treasury certificates and the preferential discount rate after the war. The purchase operations ended on June 30, 1920, when a sinking fund replaced the purchase program. In all, the Treasury purchased $1.7 billion under the program, with most of the purchases made after the war. The program did not succeed in bringing taxable bonds to par value.

Since the commercial banks could use the certificates at their option to borrow at preferential rates, the reserve banks were the source of the financing no more and no less than if they undertook the same volume of purchases directly. Despite a rising rate of inflation, Liberty bonds remained only slightly below par throughout the war. For example, at the time of the Third Liberty Loan, in spring 1918, the GNP deflator rose at an annual rate of about 7.5 percent. For the year 1918 as a whole, the deflator rose by 10 percent (Balke and Gordon 1986) and the consumer price index by 18 percent. Yet the Treasury was able to sell bonds at par with a 4.5 percent coupon and to keep its outstanding debt close to par by making occasional purchases. One partial explanation is that the market did not anticipate continued inflation over the life of the bonds. Although there was an embargo on sales of gold abroad, the United States remained legally on the gold standard, and the bonds contained a gold clause, permitting the holder to demand gold at redemption. Further, the common anticipation, based on experience in previous wars, was that budget deficits would end and the gold standard would be restored at the end of the war. Evidence of this disinflationary anticipation is given by the inverted yield curve: commercial paper with a maximum of 180 days maturity yielded 6 percent.49

Unlike its World War II policy, the Federal Reserve did not agree to purchase all government securities at fixed rates. In keeping with its mostly passive policy orientation, it achieved the same end by setting the discount rate on Treasury securities below the market rate on the securities. Bank reserves and the monetary base were thus set by the banks’ demand to borrow. Any bank with Treasury certificates could borrow profitably. The price of Treasury securities was kept relatively stable by this arrangement at the cost of supplying reserves and money at the market’s demand. As in World War II, the Federal Reserve became the “engine of inflation.”

The wartime policy achieved the Treasury’s objective of marketing an extraordinary increase in debt at relatively low direct cost to the Treasury.50 The public bought most of the debt, but between 1916 and 1919 commercial banks bought almost $5 billion, approximately 20 percent of the total issued. The banks financed their purchases in part by borrowing $2 billion from the Federal Reserve.

In June 1917 Congress amended section 13 of the Federal Reserve Act by reducing collateral behind the note issue. Initially, a reserve bank had to deposit with the Federal Reserve agent (at the reserve bank) 40 percent of the issue in gold and 100 percent in commercial paper and bills of exchange with less than ninety days to maturity. The new requirement reduced the total of real bills and gold to 100 percent of the note issue, 40 percent in gold. A year earlier, banker’s acceptances became eligible as collateral and, slightly altering a premise of the act, reserve banks could also use as collateral promissory notes of member banks secured by government bonds or notes.

Gold inflows slowed after 1917 (Schwartz 1982, table SC14). For the next three years Federal Reserve credit—mainly discounts—became the driving force in the expansion of the monetary base and inflation. The Federal Reserve Board’s annual report for 1918 looked forward to the time when “the invested assets of the Federal Reserve Banks have been restored to a commercial basis” (Board of Governors of the Federal Reserve System, Annual Report, 1918, 87). This appeal to the real bills standard gives a misleading impression of what had happened. From December 1916 to December 1918, Federal Reserve notes outstanding increased by $1.7 billion and bank reserves increased by $400 million. On the asset aside, discounts for member banks rose by $1.5 billion, gold by $200 million, and government securities by $180 million. Nearly all of the discounts, however, were secured by government obligations (Board of Governors of the Federal Reserve System 1943, 340).

THE POSTWAR STRUGGLE FOR INDEPENDENCE

The history of the early postwar years is principally the story of the Federal Reserve’s struggle for independence from the Treasury and the deflationary consequences of its policies after it obtained independence. This was the System’s first opportunity to take independent policy action. It made several mistakes, some avoidable, some unavoidable in the circumstances. By promising not to raise interest rates during the last wartime bond drive, the System relinquished a chance to moderate the postwar inflation. By raising discount rates from 4 percent to 6 percent and then to 7 percent in the space of a few months, it contributed to the postwar contraction.51 By failing to lower discount rates for more than a year after the cyclic peak, the System prolonged the recession and contributed to its severity.

In the first four years of Federal Reserve operations, the compound average rate of inflation was 12 to 13 percent, using consumer prices and the GNP deflator. Table 3.3 shows the annual data. The peak in the quarterly rate of inflation is in third quarter 1918, at the end of the war, but the price level did not reach a peak until second quarter 1920. For the first two quarters of the latter year, the deflator rose at a 20 percent annual rate. For the last two quarters, it fell at a 15 percent annual rate. The price level continued to fall throughout 1921, although the rate of decline slowed after midyear.

The inflation period has two phases. At first the Treasury dominated the Federal Reserve, aided by the System’s commitment to assist in war finance and, after the war, commitments under the borrow and buy policy. In the second phase, the commitments had expired. The System was free to act but uncertain about what to do.

The Inflation Phase, Part 1

The Board’s annual report for 1920 blamed the inflation on “an unprecedented orgy of extravagance, a mania for speculation, overextended business in nearly all lines and in every section of the country” (Board of Governors of the Federal Reserve System, Annual Report, 1920, 1). At best this was disingenuous, as the Board had recognized in its annual report for 1919. The Board wrote there that the absence of a penalty rate “is enough to prevent a normal functioning of a Federal Reserve Bank, whose rates should be so fixed that resort thereto is unprofitable …and thus has a tendency to check expansion” (Board of Governors of the Federal Reserve System, Annual Report, 1919, 2).

In fact, the Federal Reserve lacked any consensus on a policy regarding rates. A return to penalty rates might be sufficient to stop the inflation but was likely to conflict with accommodating the needs of trade and commerce. This was a principal concern for several governors. Others viewed the wartime policy as a violation of the real bills basis for credit expansion, hence inflationary. Insisting on a return to a real bills policy meant that the preferential discount rate on Treasury securities had to be raised. As long as the preferential rate remained in effect, the discount rate would be controlled by the Treasury when it set the rate on Treasury issues.52 Thus there was an issue of control or independence as well as a policy issue about rates. Members were aware, however, that the president could invoke the Overman Act and assign their responsibilities to another agency. This act did not expire until six months after the end of the war, in April 1919.

The division of opinion remained throughout the war and beyond. In February 1918 Governor Harding suggested an increase to 4 percent on commercial discounts with less than fifteen days to maturity. Opinion was mixed, and the rate remained unchanged. In June Adolph Miller wrote a long memo pointing out that the government had spent less than planned in fiscal 1918 but would increase spending to $24 billion in fiscal 1919. He estimated that this would be half of current GNP, and he urged an immediate increase in rates to curtail commercial lending. He included an increase in rates on loans secured by Treasury certificates. Hamlin replied in a letter to Harding, opposing Miller’s proposal and recommending “rationing credit as we now ration food.” Raising rates would be “bad faith” with the banks that bought certificates (Board of Governors File, box 1239, February 21 and 25, June 27 and 28, 1918).53 The only action was a decision by the Cleveland and Richmond banks to raise the discount rate from 4 to 4.25 percent in April. Kansas City followed in May, raising its rate to 4.5 percent. The others remained at 4 percent.

Government spending continued to exceed revenues at the end of the war, so the Treasury’s problem of financing the deficit continued through the winter and spring of 1919. This was one source, but not the only source, of contention between the Treasury and the Federal Reserve and within the Federal Reserve. Carter Glass, who replaced McAdoo as treasury secretary in January 1919, preferred qualitative controls and moral suasion to rate increases as a means of controlling credit. In the first of many differences about qualitative controls, governors of many of the Federal Reserve banks argued that exhortation or moral suasion would work, if at all, only if rates increased.54 Missing from the discussion of qualitative controls, as from Hamlin’s proposal to ration credit, was the role of interest rates in resource allocation. Wartime expenditures required a shift of real resources equal to almost 20 percent of GNP. Several Board members and Treasury officials seem unaware that their proposals raised the cost of the transfer and added to the burden of financing the war.

In addition to deficit finance, the Treasury faced the problem of rolling over the outstanding stock of short-term certificates. Before leaving office, McAdoo had sent a letter to all banks urging them to purchase short-term Treasury certificates. Glass continued this policy of moral suasion. Moreover, to sell the Fourth Liberty Loan (in September and October 1918), national banks had promised as part of the borrow and buy program to lend at 4.25 percent for ninety days with renewal guaranteed for a year at the 4.25 percent rate. These commitments did not expire until the end of October 1919. And to sell the Victory Loan, in April–May 1919, banks had offered customers installment loans at a 4.25 percent rate for six months.

The shorter period for financing the Victory Loan reflected a telegram from the Board to the reserve banks on April 16 suggesting that member banks be discouraged from “leaving the situation with respect to loans secured by Government bonds entirely clear after November” (Board Minutes, April 16, 1919, 297).

The Board and the reserve banks were parties to the borrow and buy policy. As heads of the Liberty and Victory Loan committees, the governors had wanted this commitment to make the bond drives successful and to avoid large changes in money and interest rates following Treasury bond drives. Treasury took the position that honoring the commitments took precedence over credit and monetary control (Board Minutes, April 16, 1919). With this stance, the Treasury also hoped to fund its outstanding short-term debt at the prevailing interest rate.

Behind the subsequent struggle lay the governors’ concern about independence. Wartime policy had prevented Strong and other governors from establishing an independent institution that was free of political control. A strong Board subject to political pressures, or dominated by the Treasury, was a long-standing concern.

In January Strong took another leave to rest and recuperate from tuberculosis. The Board approved a three-month leave with full pay. Strong was away from the bank during January and February and in Europe from mid-July to late September. He participated in the discussion only by letter. Early in February he wrote to Adolph Miller and to Russell Leffingwell, the undersecretary of the treasury, about the need to liquidate the banks’ borrowings secured by Treasury certificates. In his letter to Miller he is undecided about the speed with which the Federal Reserve should act and the consequences of a rapid liquidation. The letter to Leffingwell is more decisive about the need to deflate, although he recognized that “the process of deflation is a painful one, involving loss, unemployment, bankruptcy, and social and political disorders” (Chandler 1958, 138–39).

When the Governors Conference met with the Federal Reserve Board on March 20–22, three main considerations were the forthcoming sale of the Victory Loan, the French and British decisions to allow their currencies to depreciate against gold and the dollar, and the end of the gold embargo with the expiration of the Trading with the Enemy Act in June.55 Discussion of the size and pricing of the Victory Loan presumed that discount rates would remain unchanged. Large foreign balances had built up during the war, currency exports had increased, and there was concern that a higher discount rate would be needed to slow the gold export.

Leffingwell argued that Europe lacked effective demand. Although the gold reserve ratio had fallen from 61 percent to 49 percent in the year to March and seven reserve banks including New York and Philadelphia had recourse to interbank loans to supplement their reserves, he did not “see anything in the international situation to justify an apprehension about the protection of our gold reserves” (Governors Conference, March 20, 1919, 156). He would soon reverse that forecast. Strong responded that British and French devaluations effectively raised prices in the United States, so it was equivalent in its effect on spending to an increase in the discount rate. He feared that raising the discount rate would cause too rapid liquidation of inventories (162).

The next day the Conference voted to maintain the discount rate until after the Victory Loan was placed and “for such reasonable period thereafter as will permit a considerable liquidation of such borrowing [to buy the bonds] without imposing undue penalties upon the banks” (Governors Conference, March 21, 1919, 354–55). It would soon regret this decision. The Conference also voted to recommend a 5 percent interest rate on the Victory Loan.56 The Treasury set the rate at 4.75 percent.

The inflation rate increased sharply during the summer and fall of 1919. Part of the increase is mainly measurement, the release of prices that had been controlled in wartime, but this explains only a small part of the surge in the inflation rate. Balke and Gordon’s (1986) estimate of the deflator rose from 4.3 percent annual rate in first quarter 1919 to 15.8 percent for the last two quarters. The consumer price index shows an even larger increase.

Interest rates on government bonds and commercial paper remained steady through the spring and summer. The Treasury continued to support the bond price by purchasing in the open market. From June to year end, the Treasury purchased $500 million, with more than half the purchases in late November and early December (Wicker 1966, 35).

By June, an outflow of gold and rising inflation revived interest in eliminating the preferential rate for Treasury securities and raising the discount rate. On June 9 the Treasury removed the embargo on gold exports. Despite the subsequent gold outflow, bank reserves and currency continued to rise in response to member bank borrowing. Rising monetary liabilities and falling gold stock reduced the ratio of gold to monetary liabilities from 50.6 percent in June to 47.3 percent in September. The fall in the gold reserve ratio was the traditional signal to raise interest rates. The Federal Reserve had urged an end to the wartime embargo so that the United States would lose gold. Adolph Miller describes the decision as helping “to bring nearer the day when the Federal Reserve must be permitted to resume their normal relations to the money market and to exercise control through discount rates” (1921, 182).

The Treasury was in charge, and it continued to oppose a rate increase. In July, Boston requested a general increase in its discount rates. The Board rejected the request as “inadvisable from the point of view of Treasury plans.” Government debt outstanding reached a peak in August, but the Treasury was not yet ready to raise rates. At a September 4 meeting with the Board, Leffingwell explained that he shared the view that rates must rise. He was not primarily interested in borrowing money cheaply for the government. His purpose, he said, was to refund the debt and eliminate the Treasury certificates that were subject to the preferential discount rate. He thought that higher rates would make that task more difficult in two ways. First, Liberty and Victory bonds would fall below 90, and if this occurred, Congress might require the Treasury to refund the entire debt and absorb the loss. Second, banks were obligated to renew loans to carry securities at unchanged rates. A rise in rates would put more of the debt into the banking system, so speculative credit expansion would increase at the expense of commercial and agricultural credit. This he viewed as contrary to real bills principles, hence inflationary.

In response to a question from Governor Harding, Leffingwell indicated that the Treasury did not oppose an increase in rates on commercial loans: “I ask that you do not increase your rates on paper secured by Government obligations” (Board Minutes, September 4, 1919).

Despite Leffingwell’s comment, some of the differences at the meeting reflected the commitment to keep rates unchanged at least until November. A second issue concerned debt management. Strong wanted the Treasury to borrow at market rates, in smaller amounts, more frequently. His reasoning was that Treasury borrowing created a large volume of Treasury deposits not subject to reserve requirements. When the Treasury spent the proceeds, private deposits increased. Banks borrowed at the prevailing preferential discount rate to meet the reserve requirement. The Treasury’s view was that the reserve banks should discourage borrowing by the banks without raising rates. Strong, supported by several of the reserve banks, argued that inflation could not be controlled as long as borrowing at the preferential discount rate remained profitable.57

At an October 28 meeting, Strong urged the Board to approve an increase in the minimum discount rate to 4.5 percent. Leffingwell objected that such a move would hurt the Treasury’s planned refunding. He again favored higher rates for commercial and agricultural borrowers and greater use of moral suasion to prevent “speculation.” Secretary Glass strongly favored moral suasion and opposed rate increases.58

Glass, and others, argued as if demand were completely inelastic. By raising rates, the reserve banks would encourage commercial banks to raise their rates with no effect on the amount borrowed. He agreed, however, to increase the rate for borrowing against Treasury certificates to 4.25 percent and voted for the increase at the November 1 Board meeting.

Table 3.4 shows the interest rates prevailing during the years 1919 and 1920. In October 1919, just before the first increase in discount rates, short-term rates were above long-term rates. Both had changed little during the year; bond prices, on average, had remained in a narrow range below par, 91.3 to 92.9, sustained in part by Treasury purchases.

At the end of October 1919 the outstanding debt was $26 billion, with $3.7 billion in certificates of indebtedness subject to a preferential rate. At the nearest call date, November 17, member banks held $3.5 billion in United States government obligations, mainly Treasury certificates, and had borrowed $2.2 billion from Federal Reserve banks, mainly at preferential rates (Board of Governors of the Federal Reserve System 1943).59 An important change had occurred, however. Commercial bank commitments to lend at a fixed rate on the Fourth Liberty Loan and the Victory Loan issues had expired.

On November 3 the directors of the New York bank voted to increase the discount rate by 0.25 percent, putting the discount rate for borrowing on certificates (4.25 percent) equal to the rate on the certificates. The discount rate on commercial paper increased by 0.75 percent to 4.75 percent and to 4.5 percent on paper secured by Liberty Loans. However, the Bank retained the preferential rate for borrowing collateralized by Treasury certificates, so the new minimum effective rate was 4.25 percent for up to fifteen days maturity.60 This was the first increase in the discount rate for more than a year. The Board immediately approved increases at New York, Boston, and Chicago and, on the next day, at Kansas City. Other banks followed later.

Member bank borrowing continued to increase, but government bond yields rose and stock prices fell. The monthly index of common stock prices, at 80.5, was close to a peak in October. It did not pass the monthly October level in the next five years. Loans to brokers and dealers on the New York Stock Exchange declined, suggesting reduced demand for “speculative” credit. The rate of inflation increased, however.

Although Glass voted for the increase in rates, he was far from enthusiastic about the decision. He had always favored the real bills doctrine, and he now forcefully urged the reserve banks to rely on qualitative control. On November 5 he wrote a five-page letter to Governor Harding arguing that the Federal Reserve could not rely on interest rates alone. In principle he accepted that discount rates should be above commercial rates, but these were difficult times. A rise in Federal Reserve rates would only raise other rates. Wartime embargoes remained, so gold would not be imported. Higher rates would curtail domestic production, raise prices, and stimulate speculation. Then he added:

We cannot trust to copybook texts. Making credit more expensive will not suffice…. The Reserve Bank Governor must raise his mind above the language of the textbooks and face the situation which exists….

Speculation in stocks on the New York Stock Exchange is no more vicious in its effect upon the welfare of the people and upon our credit structure than speculation in cotton or in land or in commodities generally. But the New York Stock Exchange is the greatest single organized user of credit for speculative purposes.” (Board of Governors File, box 1239, November 5, 1919)

Glass praised the Federal Reserve for accepting Treasury leadership during the war. Now the Board must provide the leadership. Governor Harding replied that he was “in hearty agreement” with the letter. The Board sent a copy to each of the reserve banks “with the injunction that the policy outlined be carried into effect” with reliance on direct action to prevent excessive borrowing and improper use of “bank credit.”61 The emphasis on direct action continued. As late as April 1920, the Board commented on the use of credit for speculation.62

A new element now entered. Inflation reduced the real value of cash balances, inducing conversion of dollars to gold. The continuing fall in the gold reserve threatened to force suspension. The problem was most acute in New York, where most foreign balances were held. New York’s reserve ratio fell to 40.2 percent.

On November 7 the Board voted to suspend for ten days, if necessary, the reserve requirement against deposits at the New York bank.63 Adolph Miller opposed the action, arguing that New York had available $150 million in gold from the other reserve banks. Further, Miller noted, New York had allowed its credit facilities to be used for speculative borrowing. The Board was reluctant to let New York borrow gold by rediscounting in other districts. It had to be punished for permitting the increase in speculative credit.

The Federal Advisory Council met on November 19. A majority favored a rate increase, but Leffingwell convinced the members that a rate increase would be harmful. Their report to the Governors Conference the following day recommended no change. Many of the governors disagreed. They wanted a prompt increase in rates. Governor Charles A. Morss (Boston) expressed concern about speculative activity. The gold reserve ratio was approaching 40 percent. He “strongly advocated higher rates, even for commercial paper.” Governor Maximillian B. Wellborn (Atlanta) saw the credit situation in the country as more important than Treasury borrowing rates. But others were hesitant and preferred to hear the Treasury’s arguments before deciding (Governors Conference, November 19, 1919, 59–71).

When the governors meeting resumed after hearing Glass and Leffingwell, Strong asked each of the governors whether control could be achieved by moral suasion and admonition and what would happen to market rates if moral suasion succeeded in controlling credit. Although Strong was a proponent of the real bills view at the time, he did not believe that qualitative controls and moral suasion could replace quantitative controls. He believed that direct action to control the quality of credit would not work without an increase in rates. Even if the New York bank succeeded in getting its members to withdraw loans for stock exchange credit, loans would be available from banks in other districts. Many of the lending banks did not borrow from their reserve banks, so they were not subject to direct pressure. Several governors accepted that direct pressure could have an effect but doubted that it would work without an increase in rates. Governor Roy Young (Minneapolis), in particular, recognized that money and credit are fungible; the lender does not truly know what is financed at the margin. Governors who took this position argued that substituting one type of credit for another undermined the effects of direct action. These governors concluded that, if effective, moral suasion would raise interest rates.64

The conclusion was not unanimous, however. Governor George Seay (Richmond) claimed that moral suasion had a “very widespread effect.” A concerted effort would, he claimed, reduce credit demand and interest rates. Some shared this view, at least in part, qualifying their answers in various ways (Federal Reserve Governors Conference, November 19, 1919, 74–88).

The Board wanted to avoid harming the Treasury’s January refunding of $1.5 billion in certificates. Leffingwell agreed that rates should rise, but not until after the refunding. Miller expressed a common concern about the effects on the prices of government bonds. He favored an increase in rates only after the Treasury refunding.65 Strong argued that it was wrong to follow certificate sales with an increase in rates and compared this proposal to a “sharp” commercial practice. Strong’s position was weakened, however, by his own and the New York directors’ concern, earlier in the month, about the effect of a discount rate increase on bond prices and by his apparent ambivalence on the issue of a preferential rate.66

Strong recognized, correctly, that banks would borrow at the lowest rate available. He weakened his argument for higher rates, however, by buying banker’s acceptances at a 4 percent rate even after the discount rate on Treasury certificates was raised to 4.25 percent. Strong considered this preferential rate necessary to encourage the market for banker’s acceptances, one of his main aims. He wrote to Governor Harding that it was

essential to the Federal Reserve System and, particularly, to the financing of the foreign commerce of the United States by American banks instead of, as heretofore, by foreign banks. But this preferential rate was also established in recognition of the fact that a bill drawn against an actual shipment of commodities and accepted by the largest and richest bankers of the country was a credit instrument of greater value commanding a lower rate than the average of the commercial paper which would reach us. (Chandler 1958, 160)

This argument for a preferential rate has some similarities to the Treasury’s argument. The principal difference is that Strong wanted a preferential rate for a particular type of real bill. The Treasury wanted the preferential rate for itself, based on its claim that its debt had lower risk because the government would not default. A central issue was whether the rate structure should give preference to real (commercial) or speculative (government) borrowers. Beneath the surface was the continuing struggle over the control of policy and the requirements of Treasury finance.

The November Governors Conference made no decision.67 On November 24 New York and Boston voted to increase their discount rates. When the Board met two days later to consider the request, Leffingwell attacked Strong both personally and for several of his actions and policies.68 He accused Strong of making “a direct attempt to punish the Treasury of the United States for not submitting to dictation on the part of the Governor of the Federal Reserve Bank of New York even though it be at the cost of a shortage of funds of the Treasury to meet its outstanding obligations.” Treasury had consented to a rate increase early in November because Governor Strong had agreed to do three things: insist that stock exchange accounts be adequately covered; prevent a scramble for deposits (higher rates on deposits) by New York banks; and raise the buying rate on acceptances. Strong had done none of the three. Further, he said, Strong had made an agreement with the governor of the Bank of England to increase rates for Treasury borrowing. The Bank of England had forced the British Treasury to raise rates, thus encouraging a gold outflow and the fall in the gold reserve. The United States Treasury had to borrow $500 million every two weeks until January 15. Leffingwell urged the Board to wait until January 15, when Treasury borrowing would be completed.

The Board disapproved the increases by New York and Boston. Miller said that he believed rates should rise, but he would not vote against the Treasury. Albert Strauss, a New York investment banker who had replaced Warburg, saw “no occasion for an increase in rates” that would only add to the cost of credit with no effect on the credit situation. Williams opposed a rate increase because of heavy borrowing by banks that lent to Wall Street. The Board rejected the increase in discount rates and voted to advise Boston and New York that acceptance rates were too low (Board Minutes, November 26, 1919).69

The criticism found its mark. Strong at last fulfilled his commitment by raising buying rates on acceptances to 4.375 percent on November 26 and to 4.5 percent on December 4.70 Within a month, the rate was 4.75 percent. At a meeting in Secretary Glass’s office, Strong threatened to increase the discount rate without Board approval, claiming that section 14 of the Federal Reserve Act gave power over discount rates to the reserve banks. This was too much for Glass. He threatened to have the president remove Strong, and in a lengthy letter to the attorney general that left no doubt about his view, he requested an interpretation of section 14.71

On December 9, the Justice Department responded: “I am of the opinion that the Federal Reserve Board has the right, under the powers conferred by the Federal Reserve Act, to determine what rates of discount should be charged from time to time by a Federal Reserve bank, and under their powers of review and supervision, to require such rates to be put into effect by such bank” (quoted in Warburg 1930, 2:822).

The Treasury won the point, and the Board won another round in the continuing dispute about the locus of power in the System.72 The Federal Reserve System had shown itself divided, hesitant, and unable to move promptly against inflation in the face of Treasury opposition, a situation that was repeated in different circumstances after World War II.

The Inflation Phase, Part 2

The attorney general’s opinion came just as the Treasury’s cash position improved. On December 9 Leffingwell wrote to Glass: “I do not think that a moderate further increase in rates at the present time would have a disastrous effect upon the Treasury’s position” (quoted in Wicker 1966, 42). On the following day he gave a similar message to the Board, offering several reasons for the change in position. Recent Treasury issues had been successful; the chance of a coal strike had diminished; and he was concerned about renewed speculation. He no longer objected to an increase in rates or the elimination of the preferential rate for debt secured by Liberty and Victory bonds. The preference for certificates should remain (Board of Governors File, box 1239, December 10, 1919).

The Board immediately sent a telegram to the reserve banks informing them that they could now propose a rate increase. New York and Richmond responded at once, raising rates on paper collateralized by Treasury certificates and Liberty bonds by 0.25 percent to 4.5 percent and 4.75 percent, respectively. The minimum discount rate, 4.5 percent, was now above the rate on the Treasury’s latest certificates. Most other banks followed within the week. On December 30 New York voted to increase the rate on certificates to 4.75 percent. Despite the Treasury’s sale of certificates on the same day, Leffingwell permitted the increase, although he described the change as unwise.73 Other banks followed.