FOUR

The years 1923 to 1929 are often described as one of the best periods in Federal Reserve history. Inflation, though highly variable from quarter to quarter, averaged close to zero for the period as a whole. Economic growth was variable but robust. The economy grew at a 3.3 percent average rate, despite two recessions in six years.1 Labor productivity in manufacturing rose 4 percent a year, and the index of stock prices rose 20 percent a year.

Whether judged by money growth or by interest rates, Federal Reserve policy avoided the sharply inflationary and deflationary actions of earlier and later years. Interest rates on both long-term Treasury bonds and commercial paper averaged about 4.5 percent. The monetary base rose about 1.5 percent a year. Although the United States was on the gold standard for the period as a whole, variations in money growth were not much affected by gold movements.

Membership in the Federal Reserve System was far from complete. Fewer than 10 percent of state banks were members. The number of state member banks declined, but deposits of member banks increased both absolutely and relative to deposits of nonmember banks.

The Federal Reserve developed much more activist procedures than envisaged by the authors of the Federal Reserve Act or practiced in earlier years, and policy actions became more centralized. The reserve banks, particularly New York, gained more control over decisions, but disputes about the locus of power continued and at times became intense.

The problem was partly personal, partly substantive. Adolph Miller, the dominant personality at the Board, was indecisive, inclined to shift his position in debate, and unwilling to take responsibility. Miller envied the power and influence of Benjamin Strong and the New York reserve bank that Strong headed. As the only economist in a decision-making position, he expected Strong and others to defer to him on economic issues. Strong was decisive, commanding, and eager to exercise leadership. Intended ambiguity in the Federal Reserve Act, a result of the compromise President Wilson crafted, heightened the personal controversy. To Strong and other bank governors, the System was an association of reserve banks supervised by the Board. To Miller and others in Washington, the Board was responsible for directing the System to a common policy goal and steering away from bankers’ interests. As open market operations increased in importance and discount policy declined, Miller tried repeatedly to shift control of open market policy from Strong and his colleagues to the Board. He was unsuccessful while Strong was alive.

Substantive differences also reflected problems in the Federal Reserve Act. Miller and the Board emphasized control of the quality of credit by discounting real bills. The act supported their position; this was the intent of Carter Glass and others who drafted the act. Strong held this view before the 1920–21 recession, but the policy failures of that period and the political response to interest rate increases changed his mind. Further, unlike Miller and the Board, he recognized that the type of credit instrument discounted by the borrowing bank did not restrict the volume of borrowing or give information about the use of new loans. He saw that under the real bills doctrine, money and credit would expand as long as banks had eligible paper and could discount profitably. To be effective, the System had to control the quantity of credit.

Initially, policy action responded to the gold reserve ratio. A decline in the ratio signaled that interest rates should rise, a rise that rates should decline. With few countries on the gold standard during and after the war, the signal was less reliable.

What should replace it? The Board’s annual report for 1923 set out the new operating framework. By carefully sifting through the responses to open market purchases and sales, economists at the New York bank and the Board developed a new set of signals to guide operations. I call this analysis the Riefler-Burgess doctrine. The doctrine played a major role in the 1920s and beyond.

Governor Strong’s efforts to support the British by easing policy in the summer and fall of 1927 brought differences between New York and the Board into sharp focus. Under Strong’s leadership, the open market committee lowered United States interest rates by buying government securities after member bank borrowing declined. Advocates of real bills, such as Miller, criticized the action as inflationary, by which they meant that the increased credit was not backed by productive assets. They, and most others, believed that inflationary credit expansion, like wartime expansion, must inevitably be followed by contraction and deflation. For the real bills advocates, the deflation and depression that started in 1929 were the inevitable consequence of Strong’s policies in 1927.

Conflict between New York and the Board reached new heights in 1928 and 1929. New York, operating on Riefler-Burgess rules, favored a higher discount rate to reduce member bank borrowing and the quantity of credit. On their interpretation, reduced borrowing would indicate greater ease. The Board, fearful of a return to the high discount rates at the start of the decade and wanting to limit credit to stock market speculators, favored controlling the quality of credit by moral suasion, direct pressure, and exhortation against speculation. It opposed increases in discount rates. The result was delay and inaction; the more serious problem on both sides was failure to recognize that monetary policy was deflationary.

The Federal Reserve had three principal aims during the 1920s: to reestablish the gold standard as an international exchange system; to maintain price stability at least as well as if the country remained on the prewar gold standard; and to prevent or slow the growth of speculative credit, particularly credit used to carry securities traded on the New York Stock Exchange. A fourth aim, though rarely stated, was present also: the Federal Reserve wanted to avoid a return to the level of interest rates and deflationary policies of 1920–21 that had damaged agriculture and commerce and heightened criticism of the System.

The different aims often gave conflicting signals. Higher interest rates to prevent growth of stock exchange lending exposed the System to renewed criticism and attracted gold. Mindful of those criticisms, some officials preferred to rely on exhortation or qualitative control instead of quantitative control. This produced conflict within the System.

At a more basic level was the conflict between price stability and restoration of the world gold standard. In part to maintain price stability, the Federal Reserve System sterilized gold inflows and, reversing its earlier policy, put gold and gold certificates into circulation. This policy reduced the monetary expansion resulting from gold inflows, thereby shifting more of the burden of adjustment to Britain and other countries seeking to reestablish and sustain a type of gold standard. Once Britain returned to the gold standard, it had to raise interest rates and deflate to defend its exchange rate. A more classical gold standard policy of lowering United States interest rates and allowing the country’s prices to rise in response to gold inflows would have reversed some of the gold flows and reduced the need for deflationary policies abroad, at the cost of higher inflation in the United States.2

French policy added to the problems faced by Britain and others. France returned to the gold standard in 1927 at a rate that undervalued the franc; Britain returned in 1925 at an exchange rate that overvalued the pound. Under the rules of a full gold standard, gold would have flowed from Britain to France, the United States, and perhaps elsewhere. The countries receiving gold would have allowed prices to rise, and British prices would have fallen. But France and the United States were as reluctant to permit prices to rise as Britain was to let them fall. Without this mechanism, or a substitute, the gold standard could not work to adjust gold stocks and prices.

In practice, after 1927 the United States and France pursued mildly deflationary policies that drained gold from Britain, Latin America, and elsewhere. The collapse of the gold standard came in the 1930s, foreshadowed by the policies of the 1920s.

The result was failure to achieve three of the four aims. Qualitative controls failed to prevent a rise in stock prices and brokers’ loans. The international gold (or gold exchange) standard collapsed, never to be restored. And the relative stability of the 1920s was followed by severe deflation and economic depression throughout the world.

NEW PROCEDURES

A more activist policy required more and better information, new procedures, and a new framework for deciding on policy actions. The procedures began to take shape after 1921, and though they evolved through the first half of the decade, the System had the main outlines in place by the end of 1923.

The prewar gold reserve had served as a signal for timing changes in the thrust of policy. That signal was now muted. During the first part of the decade, the United States was the only major country on the gold standard. The governors agreed that they could not rely on the gold standard mechanism to maintain price stability until currencies became convertible and countries restored the international standard. They favored restoration and worked toward that end, but until countries readopted the gold standard, they needed a new guide for policy. Hence they developed the research function, first in New York and later at the Board, to provide indexes of industrial production, prices, interest rates, credit, and other measures of current and prospective economic activity.3 These measures, and the volume of discounts, replaced the gold reserve ratio as guides to policy action.

Development of Open Market Policy

Section 14 of the Federal Reserve Act authorized open market operations to make discount rates effective. The section reflected the belief that if banks were out of debt to the reserve banks, changes in discount rates would be ineffective.4 By selling in the open market, the reserve banks could reduce bank reserves and force banks to borrow, thereby restoring the effectiveness of discount policy.

Open market operations were not new. They had been known for at least one hundred years in England. As early as 1822, the Bank of England purchased and sold government securities to assist the Treasury in refunding the public debt by maintaining a particular market rate (Wood 1939, 5).5 After 1830, the bank bought and sold Exchequer bills at its own initiative on a limited scale.6

Open market purchases and sales were also well known in the United States before 1920. A few weeks after the reserve banks began operations, the Board authorized them to purchase government securities “within the limits of prudence as they might see fit” (Board of Governors of the Federal Reserve System, Annual Report, 1914, 16). The first Governors Conference in 1915 discussed whether each reserve bank should purchase and sell independently or as part of a coordinated effort.7 The reserve banks retained the right to purchase independently but agreed to combine operations in government securities and acceptances under New York’s supervision.

The Board’s hostility to the Governors Conference and the demands of wartime finance ended the first coordination effort. Although San Francisco, Chicago, and Cleveland continued to coordinate actions with New York in the acceptance market, the System did not have a common policy (D’Arista 1994, 82). After the war, the reserve banks renewed efforts to coordinate operations at the March 1919 Governors Conference. New York proposed centralization of acceptance purchases in New York and rules for reserve bank operations. New York wanted a no resale rule for acceptances, to avoid competition with member banks, and common rules for purchases made outside a reserve bank’s home market to restrict competition. Nothing happened. A year later New York tried again, this time urging a common program in which everyone would share and all would be obligated “unreservedly.” Boston argued for developing local markets, and Chicago argued that New York held acceptance rates too low, reducing reserve bank earnings.

The governors could not agree at the time on rules for allocating acceptances purchased commonly. The main decision in 1920 was to appoint a committee to develop a basis for dividing costs and income from joint operations in the acceptance market. A year later the committee recommended a uniform purchase rate and urged that purchases be made only from dealers and only after bills had been endorsed.8

Coordinated operations in acceptances laid the groundwork for coordinated government securities purchases. Three factors worked to force the next step. First, the New York bank, as the main fiscal agent, was responsible for distributing and refunding government debt. The Treasury complained that uncoordinated market activity by the reserve banks interfered with debt management operations, and some commercial banks complained about competition from the reserve banks in the debt market. Second, the reserve banks purchased heavily in 1921–22 to replace income from discounts during the recession and recovery. The Treasury objected both to the timing of purchases and to the magnitude of the reserve banks’ holdings. Third, the New York bank observed that when the regional reserve banks purchased, New York member banks repaid some of their borrowings. The result was a transfer of earnings to the regional reserve banks at New York’s expense.

The main impetus for coordination came from the Treasury following the large-scale purchases by the reserve banks. Between October 1921 and May 1922, the reserve banks added almost $400 million to their holdings of government securities as partial replacement for the $900 million reduction in discounts during the same period. Purchases were particularly heavy in February and March, when the reserve banks purchased $200 million, doubling their holdings.9

The desire to avoid losses overcame scruples about real bills (Parthemos 1990, 12). In 1920, with high discount rates and heavy discounting, the reserve banks added $83 million to surplus after paying a franchise tax of $60.7 million and dividends of $5.6 million. In 1921 the addition to surplus fell to $16 million after similar franchise tax and dividend payments. By early 1922 all the reserve banks recognized that income would not be enough to cover their banks’ expenses, franchise tax, and dividends. The volume of acceptances had declined along with discounts and discount rates, reducing earnings. Even with the large increase in their government portfolios early in the year, some of the reserve banks had to pay dividends in 1922 from their accumulated surplus.10

Secretary Andrew Mellon asked the Federal Advisory Council in November 1921 to recommend a policy for the reserve banks. On April 29, 1922, he sent Governor Harding the council’s recommendations, opposing any use of the Federal Reserve System “for the purpose of carrying the Government’s obligations” and recommending that the reserve banks confine their purchases to bills of exchange and acceptances (Governors Conference, May 1922, 13–14). Undersecretary Parker Gilbert pursued the issue with great force in 1922 by writing and speaking to the governors, rejecting their argument about covering expenses, and repeatedly urging them to sell their holdings (Board of Governors File, box 1441, January, March, and April 1922).

Strong undertook three main tasks at the May 1922 governors’ meeting. He wanted to coordinate purchases and sales and centralize responsibility in his hands and away from the Board. He had to satisfy the Treasury that the reserve banks would not interfere with fiscal operations and would reduce their holdings. And he had to satisfy the other governors that their autonomy and earnings would be maintained. The governors regarded government securities as a substitute for discounts and acceptances, hence subject to decisions by their directors.

At the May 1922 Conference, Strong read a letter from Secretary Mellon to Governor Harding, dated April 25, objecting to reserve bank purchases. The Treasury’s policy was to not ask Federal Reserve banks for assistance. Mellon’s letter recognized the desire for earnings, but policy was more important: “I should regard it as particularly unfortunate if incidental questions of expenses and dividends were to be permitted to control on questions of major policy” (Governors Conference, May 1922, 519). He reminded the governors that the reserve banks were not created to make a profit.

Treasury Undersecretary Gilbert wanted the reserve banks to liquidate all their current holdings of governments. To partially compensate for the reduced income, he offered to pay the reserve banks for their fiscal services. And he reminded them that the attorney general had ruled that they could pay dividends out of accumulated earnings when they had insufficient current income.

Most of the governors admitted they were investing for earnings. George W. Norris (Philadelphia) favored buying longer-term bonds to increase yield. Others argued, incorrectly, that since they bought mainly from district banks, they had no effect on the national market. David C. Biggs (St. Louis) reported that one of the reasons his directors agreed to purchase Treasuries was to keep the gold reserve ratio from rising.

Although New York was by far the largest investor in Treasury debt issues, Strong used the Treasury’s complaints to advance his program. The reserve banks were fiscal agents of the Treasury. And, he insisted, the Treasury’s complaints were correct. The reserve banks had a legal right to purchase securities, but the Treasury wanted a policy of noninterference.11 Not only was it their duty to meet these demands, Strong said, but the Federal Reserve Board could require them to do so.

James McDougal (Chicago) resisted centralization as an attack on the regional character of the System. Open market purchases were local decisions to be decided locally. If the Treasury was in the market, the reserve banks would stay out if notified. He offered a resolution expressing willingness to work with the Treasury but retaining local decision making (Governors Conference, May 1922, 113, 129).

Strong had no interest in solving the problem so simply. He saw the opportunity for a coordinated policy under his guidance. He wanted to build a portfolio that they could use later to prevent a repeat of the 1919–20 (or 1915) experience: “The first thing we know we will suddenly break into a run-away market such as occurred in 1919, with no means of checking it. It is not the intention of this bank to let go its hold upon the situation at the present time, and we would regard ourselves as derelict in our duty were we to do so” (quoted in Chandler 1958, 211).12

The main concern of most governors was their banks’ earnings, not System policy. McDougal moved, and the Conference agreed, that “each governor recommend to his directors that it be the policy of the bank to invest in Government securities only to the extent it may be necessary from time to time to maintain earnings in amounts sufficient to meet expenses including dividends and necessary reserves” (Board of Governors File, box 1434, May 2–4, 1922). The governors also agreed to allow their investment accounts to decline at maturity until they had eliminated earnings in excess of expenses and dividends.

Strong was able to gain approval for creation of a committee that would execute centrally all orders to buy or sell for the account of any of the Federal Reserve Banks. He saw this as a way of laying “a foundation for an investment policy” (ibid., 497). The banks were to draw up statements of projected earnings and expenses including dividends. All agreed to stay out of the market when the Treasury issued or redeemed securities. This was the beginning of what was later called an “even keel” policy—keeping interest rates unchanged during Treasury operations.

The agreement did not satisfy McDougal, Norris, and Charles A. Morss (Boston). Chicago had nurtured a local market for government securities. A central committee in New York would favor the New York market. Strong offered to buy and sell in all active markets and suggested that decisions to purchase and sell be controlled by a committee consisting of himself, Mc-Dougal, Norris, and Morss. The governors voted to establish the Committee of Governors on the Centralized Execution of Purchases and Sales of Government Securities with the four members Strong had proposed. In October the committee added Governor Elvadore R. Fancher (Cleveland). Governors of these banks continued to serve as the executive committee during the 1920s.

As the committee’s name suggests, its role was limited to recommendations and to execution of orders sent by the reserve banks. Responsibility for decisions remained with the individual banks and their directors, who retained the right to purchase and sell at their discretion and to buy directly from member banks in their districts.

At the first meeting, the committee elected Strong chairman, with Deputy Governor J. Herbert Case of New York as his alternate. The committee began coordinated sales of securities in response to the Treasury’s request to reduce holdings and the reserve banks’ agreement to limit holdings to cover expenses. The sales occurred at a time of recovery and expansion. The Board’s index of industrial production rose 35 percent in 1922, and GNP increased at a 13 percent average annual rate for the four quarters of 1922, despite a decline at the start of the year. In June Boston, New York, and San Francisco responded to the continuing decline in open market rates by reducing their discount rates by 0.5 percent to 4 percent despite the expansion.

Undersecretary Gilbert wrote to Strong in mid-September, again urging that the reserve banks liquidate all their government securities. Sales would permit increased member bank borrowing, he said, expressing what was soon to be the System’s policy view. The reserve banks should reduce discount rates to encourage the additional borrowing. Further, he complained that even with the Committee on Centralized Purchases and Sales, reserve banks were purchasing independently to increase earnings. Strong replied that since May the reserve banks had sold $150 million, one-third of the account. The committee had no power to do more than act as agents for the individual reserve banks. And, Strong added, he opposed a reduction in the discount rate, since additional borrowing might prove to be inflationary (Board of Governors File, box 1434, September 13 and 15, 1922).

When the governors met in October, Gilbert continued to press for reductions in reserve bank holdings to be carried out without disturbing Treasury operations (Governors Conference, October 10–12, 1922, 425). The governors recommended no further purchases and modified their objectives.13 Henceforth they would conduct open market operations with less attention to earnings and dividends and more to the effects on the money market. Governor McDougal, though a member of the Committee on Centralized Purchases and Sales, spoke against the recommendation as a radical departure from practice and from the principle that made directors responsible for portfolio decisions. George J. Seay (Richmond) also objected. He was hesitant to give any committee the power to override the judgment of the individual reserve banks. Strong replied, perhaps disingenuously, that nothing of that kind was intended. The committee would make recommendations to the individual banks. The reserve banks’ directors would make portfolio decisions. The committee had a “purely ministerial function”; it would not decide policy.14

The governors also took a major step away from the original plan for semiautonomous banks and toward a unified System. The Committee on Centralized Purchases and Sales now had responsibility for recommending to the reserve banks the advisability of purchases and sales.15 Decisions remained with the individual banks; they could refuse to participate, so centralization had not yet been realized. This is clear from the responses to a letter sent by Vice Governor Edmund Platt of the Federal Reserve Board early in February 1923.16 The letter asked each governor to explain his bank’s policy with respect to purchases of acceptances and governments.17

The question is surprising. The reserve banks, by unanimous vote, had adopted a common policy statement at the October 1922 Governors Conference. The statement said that discount policy and “open market operations should be administered in each district in such manner as to assist the system in discharging, as far as it may be able, its national responsibility to prevent credit expansion from developing into credit inflation.” The statement was included again in the minutes of the Committee on Centralized Purchases and Sales on February 5, 1923, when it decided not to make further purchases (Board of Governors File, box 1434, February 5, 1923). Except for New York, none of the responses to Platt’s letter referred to the policy statement. The eleven banks gave no recognition to systemic or market effects. There were three types of responses.

Several banks reported that they executed all their purchases through the centralized committee. There were not many discounts, so purchases were made to increase earnings. Chicago acknowledged that the System’s policy was to assist the Treasury by buying acceptances instead of governments. However, “the volume of bills …is at times inadequate to supply the Federal Reserve Banks with sufficient investments” (Board of Governors File, box 1434, February 7, 1923). Relying only on acceptances would depress rates and drive the commercial banks out of the market. A few banks wrote that they did not participate in the governors’ centralized purchases. They bought governments from district member banks, at prices quoted in New York, as an accommodation because there was no market in their district. Only New York wrote that purchases were made as part of a policy of keeping the volume of credit as stable as possible after allowing for seasonal demands.18

The Board’s Response

From the very beginning of centralized purchases, the Board tried to find ways to control operations. Soon after the Treasury began to express concern about purchases, the Board asked its general counsel for an opinion about its powers. The counsel’s report concluded that the “Board has legal right to impose any restrictions and limitations it may deem proper” (Board of Governors File, box 1434, April 14, 1922, 190). The memo left decisions to purchase and sell up to the reserve banks; the Board had general supervisory powers.

During the winter of 1923, the Board was pressed to adopt a policy from one side by Secretaries Mellon and Gilbert and from the other by Adolph Miller. The Treasury wanted the Board to stop the reserve banks’ open market purchases and get the banks to liquidate their holdings (letter Mellon to the Federal Reserve Board, Board of Governors File, box 1434, March 10, 1923). Vice Governor Platt’s response expressed general agreement with Mellon’s concerns, but he noted that the Board could coordinate actions by the reserve banks but did not have authority to stop all purchases. Mellon’s reply did not accept the Board’s argument. Under its power of general supervision (section 11[j]), he wrote, the Board had ample authority to prohibit the reserve banks from investing in government securities. Mellon sharply distinguished investments from credit market transactions. Only the former should be prohibited. Credit market transactions “should not be hampered by regulations any more than is absolutely necessary” (Mellon to Platt, Board of Governors File, box 1434, March 15, 1923).

Miller wanted open market policy to be made with regard to the general credit situation. On March 8 the Board voted to ask Miller to draft a policy statement, and meanwhile it wrote to all the reserve banks urging them to allow their certificate holdings to run off without replacement. Two weeks later the Board considered Miller’s proposed resolution. Citing its powers of general supervision of investments under sections 13 and 14 “to limit and otherwise determine the securities and investments purchased,” the need to maintain a proper relation between discount and open market operations, and the embarrassment that past operations had caused the Treasury, the Board ruled that the reserve banks should conduct open market operations “with primary regard to the accommodation of commerce and business, and to the effect of such purchases or sales on the general credit situation” (Board Minutes, March 22, 1923, 177–78). The resolution abolished the Committee on Centralized Purchases and Sales and appointed the five members of that committee as the Open Market Investment Committee (OMIC). Miller’s resolution placed the committee under the Board’s control.19

To placate the Treasury, the Board’s resolution required the committee to conduct most of its operations in the acceptance market. Reflecting the real bills view incorporated in the act, the resolution instructed the committee to take account of the effect of purchases of government securities, “especially short-dated issues, upon the market for such securities, and to restrict open market purchases to primarily commercial investments, except that Treasury certificates be dealt in, as at present, under so-called repurchase agreement” (Board Minutes, March 22, 1923, 177–78; emphasis added).

The governors were meeting down the hall. A joint meeting with the Board, which Burgess (1964, 221) describes as “stormy,” discussed the Board’s resolution and its claim to general powers over portfolio decisions. W. P. G. Harding had replaced Morss as governor at Boston. Perhaps because he was the former governor of the Board and Strong was on leave, Harding led the governors’ criticism of the proposed resolution. He was not opposed to selling government securities, but he opposed doing so on the Treasury’s orders. This gave the Treasury a voice in open market policy and set a bad precedent. Further, he objected to the part of the resolution that severely restricted the banks’ right to buy government securities. The Board did not have power to prevent the reserve banks from buying securities. Its power was supervisory only, and the Treasury had no power at all (Joint Meeting of Governors and Board, Governors Conference, vol. 2, March 22, 1923, 669–70).

Miller responded that the banks’ purchases in 1922 had not been coordinated by the Committee on Centralized Purchases and Sales. The banks had purchased $400 million more than needed to meet expenses and dividends. This criticism angered McDougal, who argued that the additional purchases were made because discounts had increased more than expected as the economy recovered.20

The Federal Reserve Act gave the Board general powers of supervision. None of the governors questioned the extension of these powers to open market operations. Harding, joined by Case and Norris, objected to the Board’s claim that it would “limit and otherwise determine” the amount and type of open market purchases and sales. Norris said the Board lacked general authority over a reserve bank’s portfolio decision. General authority would mean that the law created a central bank, in Washington, with the reserve banks as operating branches.

Miller’s response recognized the importance of open market operations: “The open market operations of the system are going to be the most important part of the system, largely because it is through the open market clause of the Act that the reserve banks are in a position to take the initiative” (ibid., 700).

The Board was the proper authority, Miller argued, because it had a national, not a regional, perspective. Harding replied that there was no general power in the Federal Reserve Act. The Board’s counsel could not point to any place where the Board was empowered to limit the amount of government securities that the reserve banks could purchase.

Miller’s response recognized the law’s limitations but chose to ignore them. Without intending to prophesy, he foresaw what would happen: “The powers of the Board have been challenged in this matter. I regret to say that there has even been some question in the Board itself as to whether it had the power. A Board that doubts its power doubts its responsibility, and a Board that doubts its responsibility is very apt to be charged with responsibility later…. I think we have got the power; to me it is almost as clear as though it were there” (ibid., 694).

Miller found no support for his interpretation among either the governors or his Board colleagues. The governors, on their side, did not question the Board’s supervisory role or its power to replace the Committee on Centralized Purchases and Sales with the OMIC. Hamlin proposed that the offending paragraphs claiming general authority be stricken. With that change, the Board and the banks reached agreement. On April 7 the Board approved an amended version of Miller’s resolution that omitted the offending language. The Board also issued a statement of objectives for open market policy. Open market investments were to be “governed with primary regard to the accommodation of commerce and business, and to the effect of such purchases or sales on the general credit situation.” Thus the new procedure was blended with the old and brought under the congressional mandate. The banks had thwarted the Board’s attempt to control policy operations, but the issue would return.

The compromise did not satisfy either side. Before the first meeting of the OMIC on April 13 at Philadelphia, Miller proposed that Vice Governor Platt tell the governors they must sell all their government securities before the Board would approve an increase in discount rates. Strong was annoyed repeatedly by the Board’s failure to endorse OMIC decisions and by the frequent delays and changes in the decisions reached by the committee. Miller continued to press for more control. As chairman of the Board’s Committee on Discounts and Open Market Operations, Miller was well placed to interpose his views of proper actions. Further, he tried unsuccessfully to reduce the committee’s power. Early in 1925 he proposed that the Board outlaw repurchase agreements. In 1928 he again asked the Board’s counsel to review the Board’s authority over open market operations. The resulting memo left no doubt that the Board lacked the power Miller sought. The memo also made it clear that the open market agreement was voluntary—that any bank could withdraw if it chose to do so:

The Board, under this Section [14(b)], is given the power to regulate, and probably it could prescribe, maximum and minimum amounts which could be sold during any one period, but it could not forbid sales or purchases absolutely, for the power to regulate is not the power to destroy….

The formation of the Open Market Investment Committee grew out of a voluntary agreement entered into between the Federal Reserve Board and the Federal Reserve banks. Under this agreement, the individual authority and discretion of each Federal Reserve bank to buy and sell Government securities is taken away, and the power is given to the Open Market Investment Committee and the Federal Reserve Board. I believe a Federal Reserve bank could withdraw from this agreement at any time….

In my opinion, the Federal Reserve Board has no legal right under the Federal Reserve Act to create such a Committee, or to take over to itself such functions, except by voluntary agreement. (Board of Governors File, box 1435, April 25, 1928)

What Changed?

The decision to create an open market committee did not introduce a new policy instrument. Open market operations had been used for more than a century, and it was widely believed that purchases and sales could be used to change interest rates and expand credit and money.21

The principal changes were in interpretation or beliefs about the effect of open market purchases and sales, the role of the reserve banks, and their influence on national, as opposed to regional, financial conditions. Strong’s view that the principal effect of open market operations fell on member bank borrowing, not interest rates or credit, became the foundation of a revised view of how monetary operations worked. The new view changed the role of the reserve banks in two ways. Burgess (1964, 220) reports the two conclusions drawn at the time:

First, as fast as the Reserve banks bought government securities in the market, member banks paid off more of their borrowings; and, as a result, earning assets and earnings of the Reserve bank remained unchanged. Second, they [the reserve banks] discovered that the country’s pool of credit is all one pool and money flows like water throughout the country…. These funds coming into the hands of banks enabled them to pay off their borrowings and feel able to lend more freely.

Burgess (1964) recognized that the new policy view depended on the large gold reserve. This allowed policymakers to ignore any gold movements induced by purchases or sales. Reserve banks did not have to wait for gold movements or for member banks to borrow or repay; they could take an active role, forcing borrowing or encouraging repayment by reducing or increasing bank reserves. Further, discount rates now had at best a secondary role of supporting open market policy. The System could curtail borrowing without raising rates to levels that brought political and public criticism.

The new view, developed in New York, was based partly on observation of the effects of open market purchases in 1921–22 and partly on empirical studies. At the time, Burgess summarized the empirical findings about interest rates from 1831 to 1922 as showing that the System’s main effect on rates would be less seasonal variation. He reported that

(1) there is no long-term effect of Federal Reserve operations on interest rates; in the long-run rates depend on the productivity of capital;

(2) changes in the demand for and supply of money cause fluctuations around the long-term rate;

(3) the Federal Reserve is one factor reducing interest rate variability; other factors include reduced speculation on natural resources, other improvements in money market organization, and increased wealth and saving;

(4) a main effect of the Federal Reserve was a change in the seasonal; rates were lower in October to December, and higher in April to July, after 1914. (Board of Governors File, box 1240, December 1923)

As was customary at the time, and long after, Burgess did not distinguish between real and nominal interest rates.

The Board’s Tenth Annual Report

Studies of policy actions and development of statistical series by the Board’s staff, led by Walter Stewart, complemented the findings at New York. Stewart’s work formed the basis for the most important policy statement of the period—the Board’s tenth annual report—offering substitutes for the gold reserve ratio as a guide to Federal Reserve policy (Board of Governors of the Federal Reserve System, Annual Report, 1923, 29–39).

The report, written mainly by Stewart with Miller’s support, blends the old and the new policy views by joining the real bills doctrine underlying the Federal Reserve Act with the more activist policy of responding to current and anticipated changes in the credit market.22 Instead of waiting for member banks to borrow or repay, the reserve banks could influence the supply of real bills. Instead of a portfolio consisting of real bills and gold, the reserve banks would now choose to hold government securities as part of their portfolios.23

The report offered two “tests” of policy, qualitative and quantitative. The qualitative test, as before, was whether credit was used for productive purposes. The new quantitative test replaced the gold reserve ratio with measures showing how credit changed relative to production. The report argued that the qualitative test alone could not be sufficient. Credit is fungible. A bank could offer real bills while financing speculative activities. Or a bank could borrow on government securities to finance production.

Both tests required judgment. The assets used to support bank borrowing need have no relation to the marginal extension of credit. Judgments about quantity could be made only by looking at many indications of business conditions, including indexes of production and employment.

The report rejected both the gold reserve ratio and the price level as the principal quantitative guides. The gold reserve ratio had the benefit of tradition and wide acceptance, but its usefulness depended on the reestablishment of the international gold standard. In response to critics who urged the Federal Reserve to adopt price level stability as its main objective, the report argued that there are many causes of price level changes. Several of the causes are independent of “the credit system,” so a central bank that tried to control the price level would fail. The quantity theory of money was brushed aside: “The interrelationship of prices and credit is too complex to admit of any simple statement.” The discussion of the price level ended with the following: “Credit is an intensely human institution and as such reflects the moods and impulses of the community—its hopes, it fears, its expectations” (Board of Governors of the Federal Reserve System, Annual Report, 1923, 32). Credit administration cannot be done by “mechanical rules.” It must be done by judgment guided by the principles of the Federal Reserve Act.24

Some members of the Board, particularly Miller and Hamlin, did not accept the activist view of policy and the quantitative guides. They could accept the new policy as a means of getting banks to discount or repay, since that was consistent with the Federal Reserve Act and the real bills doctrine. Further, to satisfy proponents of real bills the report advocated a policy of qualitative control by “direct supervision” of the use of credit by member banks, contradicting the clear statement about the fungibility of credit.

These different statements became the basis later in the decade for disputes between the Board and the reserve banks. In 1924 and 1927, Miller objected to open market purchases made not to reduce discounts but to expand money and credit. In 1929, the Board and the reserve banks quarreled over reliance on direct supervision (qualitative control) to prevent increases in stock exchange credit.25

Differences of Opinion

Burgess later claimed that most of the reserve banks regarded direct supervision of the use of credit as “theoretical and impractical” (1964, 222 n. 2). Clearly there was little enthusiasm for direct controls at some of the larger reserve banks, and New York was opposed. Governors of several reserve banks held to the real bills view, however, and accepted qualitative controls. They disliked Board interference in lending as a violation of their autonomy, but their views were closer to Miller’s than to Strong’s.

Case praised the discussion in the tenth annual report, calling it “a most excellent report and a good set of principles to follow” (Governors Conference, May 6, 1924, 240).26 New York had applied the quantitative principles on April 30, lowering its discount rate in recognition of what appeared to be the start of a recession. At a joint conference of the Board and the Governors on May 7, Governor Daniel R. Crissinger27 of the Board asked New York “on what theory they acted” (Joint Conference, Governors Conference, May 7, 1924, 1).28 This question started a lengthy discussion of discount rate policy that gives insight into prevalent views. Some of the differences reflected in the discussion became central issues later in the decade and help to explain the failure to act during the depression.29

The governors had agreed at an earlier meeting that in place of a penalty discount rate, the discount rate should be held at the average of commercial paper rates and the lending rates at banks in the principal cities of the district (Governors Conference, May 6, 1924, 240). This set the level of the discount rate relative to a market rate, but it left the decision to the market, in contrast to the part of the tenth annual report that proposed activist Federal Reserve policy.

Case used this agreement to justify the New York decision. The decision was taken to align the discount rate with market rates and with the principles of the tenth annual report. Several governors, who disliked the lower discount rate, challenged the decision as an unduly activist policy out of keeping with the Federal Reserve Act. One reason for the criticism is that the lower discount rate in New York drew borrowing to New York, reducing the earnings of other reserve banks and encouraging Boston, Philadelphia, and others to lower their rates, further reducing their earnings. Governor Harding of Boston described business conditions in New England as showing “a very distinct recession,” but he did not want to lower the discount rate. A reduction would not stimulate business but would probably encourage speculation. Further, the member banks did not want a reduction because they did not want to reduce their lending rates (Joint Conference, Governors Conference, May 7, 1924, 9–11). Governor Norris supported Harding’s statement. Banks in the Philadelphia district also opposed a reduction in discount rates. Norris believed that any recession “should be allowed to run its course, provided it does not become too violent” (ibid., 19 and 20).

Neither Norris nor Harding gave either recognition or support to the new policy principles. McDougal also opposed activist policy. In an exchange with Miller, he argued that lowering the discount rate was “squarely against the policy that Federal Reserve banks should pursue.” It would lead to an “abuse of credit [and] …encourage inflation.” The discount rate reduction was wrong because “it is not reflected in the demands upon the Reserve banks.” “I think we should not lead the rates down, and that is what has been done recently by one bank” (ibid., 38–40). Although they were members of the OMIC, McDougal and Norris threatened to purchase securities for their banks to increase earnings.

John U. Calkins (San Francisco) and Fancher (Cleveland) criticized New York’s action also. Calkins took a standard real bills approach. The open market committee “has put money into the market when it is unduly easy and it will …be taking money out of the market when the market is beginning to tighten” (ibid., 19). He did not oppose Strong’s purchases in principle, but the purchases had not lowered market rates. The failure was evident in New York’s decision to lower rates by reducing its discount rate. The only reason for reducing the discount rate that he had heard from Case was that it could be raised later.

Stewart then reported on business conditions. Wholesale prices had fallen by 6 percent in three months, and employment by 2 percent, since the start of 1924. Other indicators also showed the beginning of a moderate to steep decline.30 The report had no perceptible effect on the discussion. The Board and the New York bank continued to argue for lower interest rates; the other reserve bank governors continued to oppose them. Seay (Richmond) thought 4.5 percent was attractive, since banks in his district paid 5 percent for time deposits. He challenged Miller to explain why a reserve bank should try to lead rates down (ibid., 57). Roy A. Young (Minneapolis) and David C. Biggs (St. Louis) saw no reason for lower rates. Willis J. Bailey (Kansas City) put forward an argument that some of the others may have been hesitant to make—the effect on reserve bank income: “How are we going to pay dividends and salaries?” (80).

Miller and Crissinger said that rates should have been reduced in January or February. Miller made the argument for the Board, but all the Board members concurred (ibid., 80, 83–84). Leading the market to rate reduction was the right policy unless the increase in credit was for speculation. Policy actions must be symmetrical. When the Federal Reserve “undertakes to use its rates for the purpose of restricting credit, it has got to show that it is also willing to do what it can to give the public and the borrowing community the benefit of lower rates when conditions warrant it” (59). If the recession continued or deepened, Miller said, New York should reduce its rate to 3.5 percent: “It will be very much easier for the directors of the New York reserve bank and its officers to bring the rate up if they move from 3.5 percent than if they had stuck at 4.5 and desired to raise it from 4.5 to 5” (60–61). Miller concluded: “The Federal Reserve is on trial, and I do not want to acutely attract destructive attention to us through niggardly, parsimonious or hesitant action with respect to the discount policy” (75).

Much of this argument was political, so it was unlikely to persuade the governors who thought the Board was overly responsive to political pressures. The argument hardly spoke to the main concerns felt by most of the governors—concerns about earnings and dividends and what later became known as “elasticity pessimism,” the belief that demand did not respond much to changes in interest rates. Although Miller claimed that rate reductions could have sizable effects on the amount of borrowing, many of the governors contended the opposite. This was particularly true of the governors from the agricultural regions, but the point was voiced by others, including Norris, McDougal, and Harding.31 None of the principals except Case (New York) made any reference to, or expressed support for, the principles in the tenth annual report.

Meeting in conference without the Board, the governors discussed whether to continue centralized purchases through the OMIC and, if so, the principles that should guide the OMIC. Calkins argued that reserve bank earnings were an inappropriate guide. Earnings would be low when borrowing and interest rates had fallen. If earnings were the guide, the reserve banks would purchase and ease the money market when the market was “easy” and conversely. Policy would be countercyclical. This, he said, is “exactly the reverse of what is desired” (Governors Conference, May 1924, 17). The reserve banks were supposed to take money out of the market in recession when the market was “unduly easy” because the supply of real bills had declined (19). This policy was procyclical.

McDougal, Fancher, and others criticized earlier decisions, taken in response to Treasury pressure, requiring reserve banks to sell all government securities. McDougal wanted to purchase long-term bonds to increase earnings (ibid., 20). Case acknowledged that selling off most of the portfolio in 1923 was a mistake, but recently the Open Market Investment Committee had bought back $235 million. The purchases had not increased reserve bank credit as Calkins implied. Reserve bank credit declined as purchases were made in recession. The effect of purchases, he said, was much more on the volume of discounts than on the aggregate portfolio.

The discussion turned again to earnings. The governors discussed three options: If earnings fell below expenses plus dividends, the reserve banks could curtail check processing, currency deliveries, and other services, purchase securities, or pay dividends from their accumulated surpluses. Three governors favored curtailing services. Nine favored paying dividends from surplus. The consensus was that open market operations should be conducted independently of earnings and dividend requirements and that the OMIC should continue. The governors retained the right to purchase or sell independently of the OMIC if their directors decided to do so.

Economists’ Views

The tenth annual report marks a turning point in Federal Reserve policy and, later, in the policies of other monetary authorities. Leading economists commented on the development of more activist policy and the use of open market operations to adjust bank borrowing.

The British economist Ralph Hawtrey found the new view of open market operations “highly encouraging to those who hope for enlightened management of credit with a view to the stabilization of prices” (1924, 284). He praised the report for its contribution to solving some of the practical problems of monetary control. He found the analysis flawed in two respects, however. First was the continued reliance on real bills and the qualitative test. These are “time-honored fallacies from which practical bankers seem to be quite incapable of emancipating themselves.” (285) Second was the “delusion” that the United States received gold because of its balance of payments: “Apparently they have not yet learnt that they receive all this gold simply because they offer a higher price for it” (286). However, Hawtrey did not go on to say that, at the current gold price, the Federal Reserve’s aims of achieving price stability and restoring the international gold standard required continued deflation abroad or changes in exchange rates.

John Maynard Keynes (1930, 2:225–21) accepted the new role for open market operations but thought that Federal Reserve officials underestimated their effectiveness (2:231). He praised the Federal Reserve for its policy from 1923 to 1928. It had shown “that currency management is feasible in conditions which are virtually independent of the movement of gold” (2:231). Although he recognized that the policy failed after 1929, he did not relate the failure to the previous policy.32

Charles O. Hardy (1932, 27, 273) was more representative of contemporary views. He argued that the new approach missed an important difference between discounts and open market operations. Control of discounts provided quantitative and qualitative control, whereas open market operations controlled only the quantity of credit. Like many of his contemporaries, he accepted the central idea of the real bills doctrine.

THE RIEFLER-BURGESS DOCTRINE

The tenth annual report does little more than sketch a new framework for monetary policy.33 During the 1920s, many people contributed to filling in the details. The best of this work was contained in two remarkable books by Winfield Riefler, an economist at the Board, and W. Randolph Burgess at the New York bank (Riefler 1930; Burgess 1936). I refer to the framework they developed as the Riefler-Burgess doctrine.34

The central relation was the member bank borrowing function. Although the reserve banks had tried in the early years to operate an English system with a penalty rate, Riefler and Burgess discarded that approach; they explained that banks were reluctant to borrow, borrowed only if reserves were deficient, and repaid promptly.35 To repay borrowing, banks called loans, raised lending rates, and sold government securities.36 Discount rate policy reinforced open market policy. A rise in the discount rate lowered the level of member bank borrowing, reduced credit and money, and raised market interest rates; a reduction in discount rates lowered market rates. Thus policy actions influenced market rates by changing the level of member bank borrowing and the discount rate.

Riefler presented the reluctance view as a central element of his theory. The importance of bank indebtedness in the transmission of policy reflected the banks’ inability to control borrowing and their unwillingness to remain in debt.

The most obvious theory is that member banks, on the whole, borrow at the reserve banks when it is profitable to do so and repay their indebtedness as soon as the operation proves costly. The cost of borrowing at the reserve banks, accordingly, is held to be the determining factor in the relation between the reserve bank operations to money rates, and the discount policy adopted by the reserve banks to be the most important factor in making reserve bank policy effective in the money markets. At the other extreme, there is the theory that member banks borrow at reserve banks only in case of necessity and endeavor to repay their borrowing as soon as possible. According to this theory the fact of borrowing in and of itself—the necessity imposed by circumstances on member banks for resorting to the resources of the reserve banks—is a more important factor in the money market than the discount rate …open market operations …contribute more directly to the effectiveness of the reserve bank credit policy than changes in discount rate. (Riefler 1930, 19–20)37

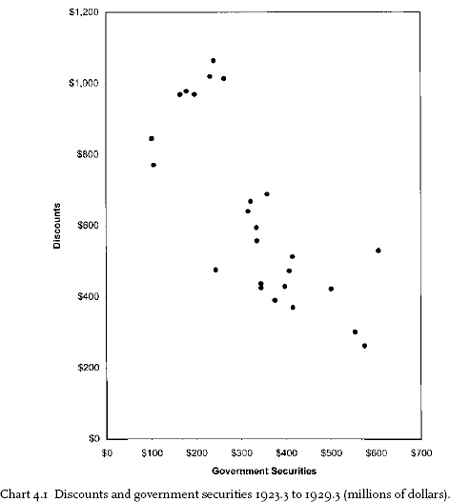

Chart 4.1 shows that the relation between discounts and government securities is negative in the 1920s. The bivariate relation is much less than one-to-one, however. On average, open market purchases reduce discounts by less than the amount of the purchase. A more complete analysis in appendix A allows for other relevant factors and casts doubt on the posited relationship.38

The discount rate has an ambiguous role in Riefler-Burgess. At times its role is modest; open market operations drive banks to borrow and repay at the prevailing rate. More often, open market operations prepare the way for discount rate changes. Strong testified in 1926 that the Federal Reserve continued to study and learn but had reached some preliminary conclusions:

If speculation arises, prices are rising, and possibly other considerations move the Reserve banks to tighten up a bit on the use of their credit, and we own a large amount of Government securities, it is a more effective program, we find by actual experience, to begin to sell our Government securities. It lays a foundation for an advance in our discount rate.

If the reverse condition appears, …then the purchase of securities eases the money market and permits the reduction of our discount rate. (House Committee on Banking and Currency 1926, 332–33)

The Riefler-Burgess doctrine was compatible with the real bills doctrine and the Federal Reserve Act, but it permitted activist policymaking. Open market operations could be conducted so as to accommodate agriculture and commerce, as the act prescribed, but they could also be used for other purposes. However, nothing in either the Riefler-Burgess or real bills doctrine distinguished between real and nominal interest rates, a major reason for later misinterpretation of policy.

The “reluctance” view of borrowing is the weak link in the Riefler-Burgess doctrine. Banks borrowed heavily in 1920–21, when it was profitable. The Board’s annual reports and statements of members during the next few years seem intended to inform banks of the “tradition” against borrowing or to impose it on them through the administration of the discount window.39

Being able to control borrowing without large changes in discount rates had strong appeal. If interest rates could be held in a narrow range without jeopardizing control of inflation, System policy would be effective and criticism would be muted. Until the end of the decade, discount rates stayed within a narrow range, 3.5 percent to 4.5 percent at New York.

Neither Riefler nor Burgess completed the framework to link money, credit, interest rates, and borrowing to income and the price level. Instead, they relied on the real bills notion that if productive lending expanded at about the same rate as production, prices would be stable. It was an easy, but invalid, inference to rely on member banks’ borrowing or a market interest rate as the proper measure of the thrust of monetary policy. If borrowing and interest rates were low, policy was easy; if the two were high, policy was tight. By the mid-1920s, high and low borrowing were defined as member banks’ borrowing above and below $500 million.

The System had adopted measures of tightness and ease that misled them at critical times. A principal problem was the failure to distinguish between an individual bank and the banking system. An open market sale removed reserves, but if banks were induced to borrow, reserve bank credit and the monetary base remained unchanged. The increase in borrowing may have induced some banks to repay, as Riefler-Burgess claimed. But unless all banks behaved that way, others borrowed at the unchanged discount rate.

During many of the cycles in Federal Reserve history, both member bank borrowing and the monetary base moved procyclically, rising relative to trend in expansions and falling relative to trend in contractions. The Federal Reserve interpreted increased (reduced) aggregate borrowing as evidence of restrictive (expansive) policy even if the monetary base and the money stock accelerated (decelerated).

Differences in regional discount rates and in the reserve position of member banks produced a market innovation. In 1921 banks with surplus reserves—reserves above current and near-term requirements—began to sell reserves to banks with deficient reserves. These sales (or loans) and purchases made better use of existing reserve balances and supplemented the correspondent banking system as a means of putting idle balances to work. The market also supplemented the discount facilities.

The new market was known as the federal funds market (Board of Governors of the Federal Reserve System 1959). Banks with surplus reserves exchanged checks drawn on their accounts at a reserve bank for checks drawn on the purchasing bank payable through the clearinghouse the following day (or later). The difference between the two checks included interest for the term of the sale. Most transactions were made in New York, and transfers occurred on the books of the New York Federal Reserve bank.

Once the banks established the market, its convenience attracted other users. Acceptance dealers, commercial paper dealers, and others settled transactions in federal funds—reserve balances at Federal Reserve banks. Brokers began to canvass regularly.

The market languished in the 1930s. Early in the decade, risk increased as bank failures rose, so far fewer banks were willing to accept the default risk. Later, gold flowed in and excess reserves accumulated. The market disappeared until after World War II (ibid., 29–30).

GOLD POLICY

Although the United States remained on the gold standard, Riefler and Burgess did not dwell on the role of gold and did not state a policy with respect to gold. The explanation may be that both authors sought to develop policy guidelines in place of the gold reserve ratio. Nevertheless, gold policy played a secondary, but important, role in the 1920s.

A contemporary reader has difficulty comprehending the strength of commitment to the gold standard by bankers, officials, and many economists. Federal Reserve officials were unanimous in their commitment to restore some form of gold standard. Strong and others took many trips abroad, motivated in part by efforts to restore fixed parities tied to gold.

Montagu Norman, governor of the Bank of England, expressed an opinion representative of the ideas of informed central bankers. Failure to restore the gold standard would mean “violent fluctuations in the exchanges, with probably progressive deterioration of the values of foreign currencies vis-avis the dollar; it would prove an incentive to all of those who were advancing novel ideas for nostrums and expedients other than the gold standard to sell their wares; and incentives to governments at times to undertake various types of paper money expedients and inflation” (Chandler 1958, 311).

The ruling orthodoxy of the period sharply separated governments and central banks. The decision to fix the exchange rate was typically taken by the government. Central bankers negotiated support operations among themselves, usually keeping their governments informed about their progress. Continuing prewar practice, Strong was the principal negotiator of these agreements for the United States.

It is convenient to treat gold policy in the 1920 as three separate topics: the monetary response to changes in gold; circulation of gold and gold certificates; and actions to foster or sustain the gold standard. The last of these raises the issue of international cooperation, about which much has been written (Nurkse 1944; Clarke 1967; Eichengreen 1992).

Gold and Money

The Federal Reserve has been both criticized and praised for not following gold standard rules during the 1920s (Brown 1940; Keynes 1930). To contemporary observers at the Federal Reserve, the rules did not apply in the circumstances of the period. These officials believed that the gold reserve ratio was not an adequate policy indicator as long as no international gold standard existed. New procedures had to be found while they waited for, and worked toward, convertibility of the principal European currencies into gold and elimination of embargoes and other impediments to gold flows.

The problem, as seen in the early 1920s, was that the United States gold stock had increased much more than expected. By the end of 1921, the System’s gold reserve ratio reached 72 percent; it continued to rise in 1922, and by midyear it had nearly doubled from its low point in 1920. The Federal Reserve did not want to monetize the entire increase, as required under gold standard rules, both from fear of a new inflation and from concern about subsequent deflation if gold should leave when foreign governments restored an international gold standard. The Federal Reserve had used the fall in the gold reserve ratio as a main reason for raising interest rates in 1920. Many in Congress and the public interpreted the rising gold ratio as a signal that the Federal Reserve banks should lower interest rates in 1922.

At the beginning of 1923, discount rates at New York, Boston, and San Francisco were 4 percent, 0.5 percent below the rates at other banks. Concerns about inflation prompted these banks to consider raising the discount rate, as they subsequently did, despite their gold reserves. Concerns about public interpretations of the gold reserve ratio prompted the Governors Conference to approve a resolution urging the Board to issue a statement about the diminished importance of the gold reserve ratio (Governors Conference, March 28, 1923, 379). Case (New York) expressed the dominant view: “The average person cannot understand why we should be thinking of high rates with that reserve ratio” (ibid., 768).40

Contemporary observers report a difference in the Federal Reserve’s response to gold movements before and after 1925 (Hardy 1932, 148). Table 4.1 divides the period 1923–29 at the second quarter of 1925, the date at which Britain returned to the gold standard. These data support Hardy; the monetary base more fully reflected the gold flow in the earlier period, before the Europeans returned to the standard. Chart 4.2 gives more detail, using quarterly data for the period.41

If the Federal Reserve had followed strict gold standard rules, gold movements would be fully reflected as changes in the base, and changes in the base would reflect only changes in gold. All points in chart 4.2 would lie on a straight line through the origin with a unit slope. We know that the Federal Reserve allowed discounts and open market operations to change the base. The points in the upper left quadrant suggest that large gold inflows were more than offset at times; the lower right quadrant shows that the base could rise while gold flowed out, contrary to gold standard rules. Nevertheless, there is a weak but clear positive relation between current quarterly gold movements and current quarterly changes in the base for the period as a whole. The Federal Reserve did not follow gold standard rules, but it did not ignore them entirely in the short run.

Together the data in chart 4.2 and table 4.1 suggest that gold flows often affected the base on arrival. In this sense the Federal Reserve “followed the rules” to a degree, most likely as a result of fixing the interest rate on discounts and acceptances and allowing reserves to respond to unanticipated gold flows. After Britain returned to the gold standard, the long-term change in the base was independent of gold flows.42

Gold as Currency

One aim of the Federal Reserve Act was to pool reserves by centralizing gold holdings in the reserve banks. In its first decade, the System worked to achieve this objective by replacing gold certificates with Federal Reserve notes.

Policy changed in the 1920s. Unwilling to allow prices to rise and concerned about the political pressures to expand as a consequence of a high reserve ratio, the governors looked for ways to reduce the reserve ratio without inflating. Early in 1922 Secretary Mellon proposed to substitute gold certificates for Federal Reserve notes. Gold certificates had 100 percent gold backing instead of the 40 percent behind Federal Reserve notes, so they reduced the gold reserve but had no effect on money or inflation.

The Federal Reserve was at first reluctant to change its policy of centralizing the gold reserve. Miller proposed instead raising the 40 percent gold reserve behind currency issues. This proposal, like Mellon’s, seemed too transparent to defuse political pressure. A second alternative kept the gold in Europe on “earmark” and, by ruling of the Board, excluded from reported gold reserves. At first the amount earmarked was relatively small, $20 million or less. Earmarked gold rose to $50 million in 1924–25 and again in the first half of 1926. The maximum during the decade was $200 million, about 5 percent of the monetary gold stock.

Despite Mellon’s request, in May 1922 the Governors Conference approved a proposal that made issuing gold certificates to the public a last resort. Gold inflows continued. In August, New York began issuing gold certificates and sent a letter to the Board asking all reserve banks to do the same. The other large bank, Chicago, did not accept the policy until February 1924, after repeated requests from Undersecretary Gilbert at the 1923 Governors Conference and by letters. The two banks had issued over $700 million in certificates by the end of 1924. The gold flow then reversed, so after discussion with the Treasury, Strong changed policy. The new policy kept total gold certificates equal to $1 billion, the amount outstanding in 1925. This policy remained in effect until mid-1928 (Governors Conference, March 1926, 126–29).43

In testimony before the Royal Commission on Indian Currency and Finance in 1926, Strong gave four reasons for changing gold certificate policy in 1922. First, the amount of gold certificates in circulation had fallen to $170 million; continued reduction might give gold certificates a scarcity value relative to Federal Reserve notes. Second, although the economy was recovering from the 1920–21 recession, “there was prevalent, especially in the agricultural sections, a feeling that possibly it would be a good thing for the country to have some expansion of credit” (Strong 1930, 301). Third, to restore the working of the gold standard, a country like the United States could fix the amount of gold in domestic circulation and permit inflows and outflows to be reflected in the monetary base. Fourth, he feared that the high reserve ratio would become the norm, so that a reduction from 85 percent to 65 percent would be considered serious (301–2).

Strong gave greatest weight to his third reason, letting the monetary base respond to gold movements, although the Federal Reserve did not follow this policy subsequently. His reasoning probably reflects the period in which he spoke, after Britain had returned to gold. Initially, the principal concern was the pressure from agricultural representatives to expand credit.44

The net new issues of gold certificates, about $800 million from 1922 to 1926, equaled about 20 percent of the gold reserve. Together, the policies of earmarking gold and issuing certificates reduced the gold reserve by about 25 percent at peak issuance.

Restoring the Gold Standard

The Federal Reserve consistently favored restoration of the gold standard in the principal countries, and it worked toward that end as long as it was consistent with domestic policy.45 At the end of the war, this meant that foreign governments had to either deflate or devalue prewar parities. Britain chose deflation; France, Germany (and others) chose devaluation.

Wholesale prices in Britain had increased 115 percent from the beginning of the war (August 1914) to March 1919, when the pound was allowed to float. In the following year, the pound declined 30 percent against the dollar. Devaluation and the effect of removing wartime price controls contributed an additional 40 percent price increase. From this inauspicious starting point, the Bank of England began to reestablish the prewar parity at $4.86 per pound by deflating rapidly. By the end of 1922 the Sauerbeck index (1867–77 = 100) had fallen almost 50 percent, from 251 to 131. At the 1922 level, the index was lower than in 1925, when Britain restored convertibility. The dollar exchange rate reached $4.61 per pound.

Achieving the remaining 5 percent appreciation took more than two additional years. Political and economic tension over reparations, including occupation of the Ruhr by French and Belgian troops, contributed to the fluctuation in the European exchange rates against the dollar during this period. The Dawes Plan of 1924 rescheduled reparations payments and provided loans to Germany that removed a major source of instability, at least for a time, by ensuring prompt payment of reparations and wartime debts.46

Germany’s return to the gold standard, or more accurately, the gold exchange standard, put pressure on Britain.47 Further, the British embargo on gold exports expired at the end of 1925. Aided by lower rates in the United States and speculation that the embargo would not be renewed, the pound rose toward its prewar parity (Howson 1975). On April 28 Winston Churchill, chancellor of the Exchequer, announced that Britain would not extend the embargo. This decision made the pound convertible de facto. Two weeks later Parliament passed the Gold Standard Act of 1925, restoring the prewar parity de jure.48

To achieve and maintain the $4.86 parity, the Federal Reserve offered the Bank of England a two-year standby loan of $200 million. On two occasions, 1924 and 1927, to help Britain it encouraged gold exports from the United States by lowering interest rates.49

The financial press and Congress criticized the loan as beyond the authority of the New York Federal Reserve bank.50 Strong responded at length in congressional hearings (House Committee on Banking and Currency 1926). The loan was secured by British Treasury obligations, payable in dollars. Governor Crissinger of the Federal Reserve Board had been present when it was discussed, and he had asked for and received approval from all members of the Board. The Open Market Investment Committee approved the loan unanimously, with Secretary Mellon present: “Mr. Mellon asked specifically if there were any objections to the arrangement …and the making of the commitment, and no objection being made, he stated it was understood that I was to go ahead” (Chandler 1958, 315).51

International Cooperation

As part of its policy to help countries return to the gold standard, the Federal Reserve lowered discount rates in August 1924. The United States was in recession, so the System had a domestic as well as an international reason for acting. Wicker (1966, 77) claimed that “the desire of the Federal Reserve Bank of New York to establish a rate spread between New York and London to encourage capital outflows and reduce gold imports was indeed the chief determinant of policy. It was not, however, the only one.”52 Chandler (1958, 241) was at the opposite pole, claiming that the policy was mainly an anticyclical policy that also was expected to encourage a capital outflow. This was also the view of Hardy (1932, 108), who found “a great deal of exaggeration” about the attention given to international considerations in setting Federal Reserve policy. Hardy recognized that Strong held such views, and stated them often, but he noted correctly that there was little evidence that other members of the OMIC shared them. They agreed on the desirability of reestablishing the gold standard but were more skeptical about using policy actions to help the British. Friedman and Schwartz (1963, 269) agreed with Hardy.

Chart 4.3 leaves no doubt that the spread between short-term rates in London and New York turned sharply in favor of capital flows to London during the summer and fall of 1924. The spread again moved in favor of Britain in the summer of 1927, the second occasion that some observers cite as evidence that international considerations had an important influence on United States policy. The covered interest parity shows the same general pattern, though the changes are smaller (Clarke 1967, 129). The difficult problem for an international explanation of policy action is that the spread reversed early in 1925, just as Britain was about to restore the gold standard. The reason for the reversal was a rise in the discount rate in New York on February 27, two months before the British decision. The reversal came for domestic reasons. The trough of the recession had occurred the previous July. By early 1925, recovery and expansion were well under way and the price level was rising. Despite the emphasis Strong gave to capital movements and restoration of the gold standard, he did not hesitate to raise the New York discount rate. This action required Norman to raise rates in London by 1 percent in early March to keep the spread in favor of London. Strong was fully aware that the British decision on gold was imminent; he was negotiating the standby credit at the time.