SEVEN

The period from 1942 to March 1951 divides almost equally into years of war and years of peacetime expansion. For Federal Reserve policy, the period can be treated as a whole, a repeat with different details and a different outcome of the experience during and after World War I. Once again the Federal Reserve put itself at the service of the wartime Treasury, and once again it had difficulty extricating itself from the Treasury’s grasp after the war. And again it took almost as much time to free postwar monetary policy as to fight the war.

The Federal Reserve summarized its “primary duty” in wartime as “the financing of military requirements and of production for war purposes” (Board of Governors of the Federal Reserve System 1947). In practice, this meant continuation of the historically low interest rates carried over from the 1930s. Principal efforts to control spending and inflation fell to administration tax policy and, during wartime, to price and wage controls and the rationing of several commodities. The Federal Reserve supplemented these policies mainly by regulating credit used to purchase consumer durable goods. Wartime allocation of materials and conversion of factories to military production restricted the supply of durable goods; consumer credit controls aimed to restrict demand at the controlled prices. After the war, Congress removed controls (1947), but it soon restored them (1948). In the early postwar years, the Federal Reserve used margin requirements to limit securities purchases. Credit controls proved difficult to administer and ineffective against inflation.

Eccles described his work in wartime as “a routine administrative job… . [T]he Federal Reserve merely executed Treasury decisions” (Eccles 1951, 382). When his term ended in February 1944, he offered to resign but agreed to remain if the president would commit to consolidation of banking regulation and supervision under a single agency. His reappointment as a member of the Board ran to 1958, as chairman to 1948.1

The Treasury relied more heavily on taxation than in World War I. Tax receipts rose from less than $9 billion (7 percent of GNP) in the 1941 fiscal year to more than $45 billion (21 percent of GNP) in 1945, but expenditures rose more. Public debt increased by $200 billion in the same four-year period (approximately 25 percent of GNP). Secretary Morgenthau’s passionate attachment to low interest rates meant that in practice the Federal Reserve’s “primary duty” was to market the debt at prevailing interest rates and, as in World War I, assist in the periodic war loan drives.2 To carry out this policy, beginning in April 1942, the System fixed ceiling rates on government securities at 0.375 percent for Treasury bills and 2.5 percent for long-term bonds, with intermediate rates on intermediate maturities. This pattern of rates became a main source of difficulty. With all rates expected to remain fixed, banks, financial institutions, and the public increased profits by buying higher-yielding long-term bonds and selling short-term bills in the market, where they were acquired by the System.

The war ended with wartime rates still in place. As in 1919, the Treasury was reluctant to let rates change, first because it wanted to float a Victory Loan, later because it was unwilling to increase the cost of debt service. Unlike 1919–20, no one at the Federal Reserve was willing to challenge the Treasury’s position. Eccles gave three reasons. First, like the Treasury, he was concerned about the budgetary cost. Economists in and outside government cited the large outstanding debt, the higher cost to the Treasury, and potential losses to bondholders from higher interest rates as impediments to the use of orthodox policies. Eccles shared this view. Second, higher interest rates would increase bank earnings, an outcome considered politically unacceptable. Third, Eccles believed there was no political support for higher interest rates. He was unwilling to make the case, certain he would lose to the Treasury, and skeptical that inflation could be controlled without raising interest rates so high that a postwar depression would be likely.3

An unspoken fourth reason was also present. The dominant view of professional economists at the time was that the task of monetary policy was to promote budgetary finance. Fiscal or budgetary policy was believed to have much more powerful effects on prices and economic activity than changes in the quantity of money or interest rates. In addition, many economists believed the war would be followed by a return to unemployment and slow growth, as in the 1930s. This view was based in part on historical precedent—most wars had been followed by recessions—but even more on Keynesian analyses showing that private spending would be too small to sustain full employment (Samuelson 1943).

Woodlief Thomas, of the Board’s senior staff, set out the prevailing view on the role of money. His essay emphasizes the role of unmeasured magnitudes such as “availability” and “turnover” as more important influences on the economy than money. Changes in money did not cause changes in output or aggregate income (Thomas 1941, 324–25). The Federal Reserve had limited influence on the stock of money (304–5), and the stock of money was less important than its rate of turnover, or velocity of circulation (330).

Nevertheless, the Federal Reserve had statutory responsibility for monetary control. Because it could be blamed for inflation, it became increasingly restive under tight Treasury control. It claimed that restrictions on interest rates converted the Federal Reserve into an “engine of inflation.” Morgenthau’s resignation in 1945 did nothing to change the Treasury’s stance. His successors, Fred M. Vinson and John W. Snyder, were no less concerned about maintaining the wartime pattern of interest rates.

Fears of a postwar depression soon disappeared as a reason for low interest rates, but other reasons remained. Although Eccles continued to oppose confrontation, he was not passive. He favored raising reserve requirements, mandating that banks must hold a secondary reserve of Treasury bills, higher tax rates to produce a budget surplus, selective credit controls, and during the transition, price and wage controls.

At first there was little opposition within the System to many of these ideas. After the transition, Allan Sproul, president of the New York Federal Reserve bank, began to advocate a more active monetary policy. Although generally reluctant to clash openly with Eccles and the Treasury or reopen the 1920s split between the New York bank and the Board, Sproul became the principal spokesman for a more independent monetary policy. When Eccles’s term as chairman ended in 1948, Sproul’s influence increased under the new chairman, Thomas B. McCabe.

Little changed until two events altered the political balance. First Congress, under the leadership of Senator Paul Douglas, opposed the Treasury’s position. Second, the start of the Korean War, in June 1950, heightened public concern about renewed inflation. The result was an agreement with the Treasury in March 1951, known as the Treasury–Federal Reserve Accord (the accord), that permitted the Federal Reserve to implement a more independent policy.

In fact, early postwar monetary policy was far from an “engine of inflation.” By the end of 1948 prices were falling, and long-term interest rates were below the Treasury–Federal Reserve maximums. The decline in prices was soon followed by a decline in output and a mild recession. Chart 7.1 shows growth of output and inflation from 1942 to 1951. The large spike in inflation in third quarter 1946 (and some of the increase in the previous two quarters) reflects the removal of wartime price and wage controls in that quarter.

Reliance on selective controls, to limit general price level increases, shows the System’s inability or unwillingness to use more general measures. But it also reflects the lingering effects of the real bills doctrine. Buyers of durables could borrow in ways other than the particular way that controls restricted, just as buyers of stock had done when the Board tried to control stock purchases by restricting credit to the stock market. Discussions at the time did not explain how inflation—a sustained rate of increase in a broad-based price index—could be controlled by limiting the use of credit to purchase particular goods and services.4 To prevent “speculative” accumulation of inventories of consumer goods, the Federal Reserve urged bankers to curtail lending to firms with rising inventories.

In June 1950 the United States went to war again. Spending to fight the Korean War brought nominal government spending back to its peak wartime level. President Truman chose to finance the war out of current revenues, so the cash budget had a surplus. After a brief spurt, inflation remained modest. Despite pegged interest rates, growth rates of the monetary base and the money stock were modest also, in part because gold outflows increased.

Korean War finance shows that wartime inflation can be avoided if policymakers choose to do so. President Truman’s budget policy did not force interest rates to rise, and it did not require the Federal Reserve to increase money growth to prevent the rise. In the two years beginning June 1950, the monetary base rose about 7 percent, a 3.5 percent annual rate. In the same period the consumer price index rose 11 percent, but by far the larger part of the rise occurred as a one-time price level change driven on one side by fear of a return to wartime shortages when the war started and on the other by the expectation that money growth always increases to finance wartime deficits. When the administration chose a balanced budget, expectations of inflation collapsed.

The principal international financial event of the period was the attempt to reconstruct the international monetary system as a fixed exchange rate system and, at the end of the period, the start of the gold outflow from the United States. At first the Federal Reserve and the administration welcomed the loss of gold as a necessary step in the reconstruction of a more viable international monetary framework. A decade later, concerns about the United States gold loss became the subject of an increasingly active discussion about the viability of the monetary standard based on gold and the dollar.5

The architects of the early postwar international monetary standard, the Bretton Woods system, believed that the failure of surplus countries to adjust was one of two major flaws in the interwar gold standard of the 1920s. The other was competitive devaluation, or beggar-thy-neighbor policies. The Bretton Woods Agreement established the International Monetary Fund as a public intermediary in the international monetary system. The fund’s key features were (1) an agreement to lend and borrow to adjust “temporary” imbalances in international payments and (2) a structural adjustment arrangement to correct “permanent” imbalances by changing exchange rates while preventing competitive devaluations.

Countries with a “temporary” current account deficit could use the fund to borrow from countries in surplus. This provision sought to avoid the problem that the United States and France created by failing to expand and inflate in response to gold inflows at the end of the 1920s. Their decisions forced deficit countries to contract without triggering an equilibrating expansion in the surplus countries. Under Bretton Woods rules, deficit countries did not have to contract. They could borrow the funds accumulated by the surplus countries.

The structural adjustment provisions permitted countries to correct persistent or permanent imbalances by adjusting exchange rates. A major problem with this provision was that central banks and governments could not distinguish temporary from persistent imbalances ex ante or even for some time after deficits appeared. A related problem was that fund rules did not make it clear what should happen when the principal reserve currency country—the United States—ran persistent trade or current account deficits.

Reliance on gold as a principal reserve asset of the fund and the member countries gave the appearance of a gold-based system. This appearance probably strengthened the belief that inflation would remain modest and thus contributed to the slow adjustment of inflationary anticipations in the 1960s. In practice the system was based mainly on the dollar, and there proved to be no binding restrictions on the supply of dollars under the Bretton Woods system.

The principal designers of the International Monetary Fund were John Maynard Keynes of Great Britain and Harry Dexter White of the United States. Keynes spent the war years, until his death in 1946, at the British Treasury. White was an economist at the United States Treasury. In contrast to the 1920s, when Governors Benjamin Strong and Montagu Norman were the principal architects of the postwar international monetary arrangements, power and influence over international monetary arrangements rested firmly in the two treasuries. Here, too, central banks had a subsidiary role.

At the New York bank, John H. Williams became one of the principal opponents, so he was kept from membership on the United States delegation. The Federal Reserve never formally considered the Bretton Woods Agreement and was not asked to do so. As the system developed, however, Williams’s proposal for an international system, based on the dollar, soon supplanted many of the features of the Keynes-White plan.

THE ADMINISTRATION’S WARTIME PROGRAM

There are both similarities and differences in the financing programs for the two world wars. Table 7.1 shows that interest rates remained lower and rose less in World War II, and the measured rate of inflation was lower also. Price controls distort the timing of price changes for the period. When controls were removed, in third quarter 1946, the deflator rose at a 45 percent annual rate, releasing most of the changes suppressed by wartime controls.

The first observation for each war is for the quarter in which the United States entered the war—second quarter 1917 and fourth quarter 1941. Second is the observation for the quarter in which the war ended—fourth quarter 1918 and third quarter 1945. Third is the observation for the postwar quarter in which wartime inflationary pressures began to recede, as measured by the rate of growth of the monetary base. Annualized rates of change for money and prices are computed from the first to the third date shown in the table.

Financing World War II was a much larger task. The cost of the war was substantially larger both absolutely and relative to GNP.6 Real GNP was approximately two and a half times greater in the later war, and the level of the deflator was similar in both periods, but government debt increased nearly ten times as much, as the table shows. The larger increase in debt occurred despite the larger share of taxes and faster growth of base money in World War II. Also, the Federal Reserve chose a different method of supplying reserves and supporting the Treasury market. In World War I, the Federal Reserve System did not have an open market policy. Banks obtained reserves by borrowing at the discount window using Treasury securities as collateral. In World War II, the System supplied reserves principally by open market purchases. Since the Federal Reserve supported a pattern of rates, it became the residual buyer. This left control of reserve changes to the banks’ decisions, much the same as in World War I.

With long- and short-term interest rates comparatively lower in the 1940s, the demand for real money balances was higher. In World War I, base money, money, and prices rose at about the same rate, 10 to 12 percent. Real balances declined slightly. In World War II, base money and money rose at about the same rate (16 percent), but prices rose at less than half that rate, reflecting the rising demand for cash balances. The rise in real cash balances financed spending and inflation at the end of the war and therefore became a cause for concern.

Beginning in 1942, the government severely curtailed automobile production and took all residual production. Production of other durables was curtailed also; spending declined and saving increased. Part of the saving was held as money because higher mobility of the population increased the demand for currency (Cagan 1965).

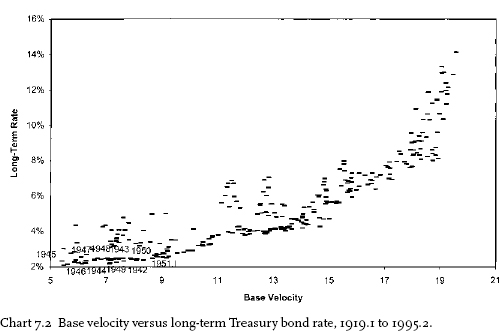

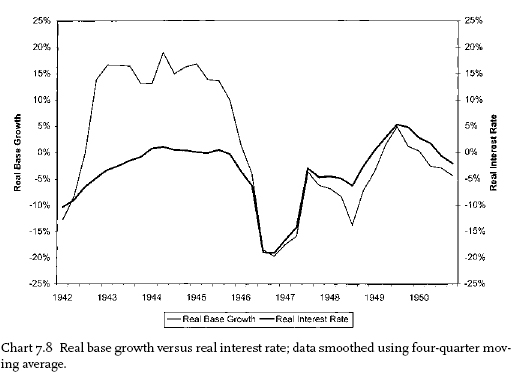

Chart 7.2 shows the relation of base velocity to a long-term interest rate and highlights quarterly data from 1942 to first quarter 1951. The chart suggests that much of the quarterly movement in wartime and postwar velocity (the reciprocal of average cash balances) is consistent with the long-term relationship. Velocity was historically low, and average cash balances were correspondingly high, principally because long-term interest rates remained close to the 2.5 percent maximum.

Chart 7.3 looks at the war and postwar period on a finer scale. The positive relation remains, but the effect of the 2.5 percent interest rate ceiling is now visible. Observations at the ceiling rate, mainly in 1943 and 1944, suggest that the ceiling was binding in these years. Extrapolating from the linear relationship, the data suggest that without the ceiling, interest rates and velocity would have been higher and average cash balances correspondingly lower during part of the war years. For much of the period, however, the ceiling rate seems not to have affected money holding.7

The opposite side of the much larger rise in cash balances was the much smaller increase in the public’s share of the debt. Morgenthau’s Treasury urged individuals to purchase debt, but he was unwilling to pay them to do so. The Treasury issued series E war bonds at prices as low as $18.75 per bond and war savings stamps for as little as 10 cents, which could cumulate to a bond purchase. The Treasury encouraged corporations, schools, and other institutions to sell bonds and stamps through payroll deduction and appeals to patriotism. These actions were not enough to offset the low interest rates paid on the debt. The nonbank public acquired a smaller portion of the debt in World War II than in World War I. Commercial banks acquired 40 percent of debt held outside the government and the reserve banks. Although many citizens and corporations pledged to buy bonds during bond drives, they sold many of the bonds to banks after the bond drive ended.

Secretary Morgenthau set three major objectives for war finance (Blum 1967, 14–15). He wanted to finance 50 percent of the war by direct taxation, to finance most of the rest by voluntary purchases of bonds, and to maintain low interest rates. He believed that low interest rates would minimize the cost of the war. He succeeded in his third objective, came close to his first, and managed to avoid most of the pressures from Congress and other parts of the administration calling for compulsory bond purchases.8

For calendar years 1942–45, total government spending was $306 billion, revenues were $138 billion, and GNP was $740 billion. These periods correspond to the war years, with a few additional months of demobilization and reconversion to peacetime resource use at the end. Based on these data, tax collections were 45 percent of spending, only $15 billion short of Morgenthau’s goal.9

Tax Policy

Morgenthau had little success getting Congress to approve his tax policy. Despite a Democratic majority in both houses, he did not fully meet his revenue goal or get his preferred tax policy. By 1944, relations between Congress and the administration became so strained that, with large majorities, both houses of Congress overrode the president’s veto of a tax bill for the first time in United States history. The administration did not try again to change tax rates during the war.

The main sources of conflict were the level of rates and the distribution of the tax burden. Many congressmen favored a sales tax. Morgenthau opposed on equity grounds; the sales tax would put more of the burden on low-income earners, a group he tried to shelter. At the opposite end of the income distribution, Roosevelt favored a limit of $25,000 on individual after-tax income, $50,000 for families. This proposal had so little appeal that Congress did not consider it seriously.

The 1943 tax bill made a lasting change in the tax system by introducing withholding at the source. Before 1943, taxpayers paid taxes in March on the previous year’s income. Withholding shifted most tax collection to the current year, a pay-as-you-go system for wage earners and some others. Withholding greatly simplified enforcement, as the number of taxpayers expanded to include 40 million to 50 million returns on incomes as low as $600 a year.10

Morgenthau at first opposed the withholding plan because Congress proposed to forgive all 1942 tax liabilities (due in March 1943) when withholding began. His main objection was that, with progressive taxation and high wartime rates, high-income taxpayers (and wartime profiteers) would benefit most. He was able to limit tax forgiveness and introduce some progressivity. The bill forgave $50 or 75 percent of the lower of 1942 or 1943 tax liabilities. Withholding began on July 1, 1943.

Morgenthau recognized inflation as a tax on households. He claimed he preferred direct taxation to inflation, but he would not allow interest rates to rise.11 However, he proposed some fiscal changes to reduce household income. One of his proposals would have raised the Social Security tax on labor income during the war, with the proceeds returned after the war, if needed, as unemployment compensation (Blum 1965, 313). Perhaps without fully recognizing the change, Morgenthau had become a proponent of countercyclical fiscal policy.

At the Federal Reserve Marriner Eccles saw the war as a major shift in demand that had to be met by substantial tax increases. In 1940–41 he agreed with the Keynesians who argued that, given the high unemployment at the start of the war, the country could increase both “guns and butter.” By 1942 he was concerned that the administration and Congress would be slow to recognize that the problem was no longer an excess supply of goods. There was an excess supply of money and excess demand for goods (Eccles 1951, 346–47).12

Debt Finance

Morgenthau foresaw that the war would require an unprecedented volume of borrowing. The Treasury and the Federal Reserve agreed on the desirability of ceiling rates of interest, high tax rates, and selling bonds mainly to the nonbank public. Morgenthau described relations with the Federal Reserve as “more harmonious during the war than they had ever been during the years of the New Deal” Blum (1967, 15). Board members shared this view.

Differences about substance remained, however (Board Minutes, April 9, 1942, 8). Eccles and some others preferred a mandated program—forced saving—to Morgenthau’s mainly voluntary bond purchase program. The Board offered proposals in each of the eight bond drives intended to increase sales to nonbanks, restrict speculation in bonds, and limit the role of banks to short maturities. The Treasury accepted few of these suggestions.

There were other differences about debt finance. Although the Treasury agreed on the aim of selling as many bonds as possible to nonbank investors during bond drives, it was less concerned than the Federal Reserve about whether the purchasers held the bonds after the drive. Getting the bonds sold at prevailing rates was its overriding interest.

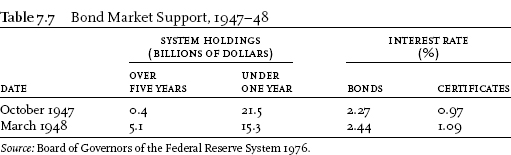

Three main problems arose. First, with interest rates lower on short-term than on long-term debt, the Treasury faced an upward-sloping yield curve. Bank and nonbank holders sold shorter-term securities and reinvested in longer-term bonds. Second, as in World War I, the Treasury permitted a “borrow and buy” policy. To ensure that bond drives were successful, banks lent money to finance bond purchases at interest rates below the bonds’ yield. Many banks agreed to buy the bonds from their customers after the drive. Since the buyers could profit by buying the bonds, they oversubscribed the new issue. This gave the appearance of public subscription but depended on bank financing. Third, Treasury certificates with one year or less to maturity were troublesome throughout. The Treasury first offered certificates in 1942 at a yield of 0.8 percent. The rate was above the rate required by the market, so prices rose to a premium. As the certificates approached maturity, they sold at a premium over Treasury bills. Banks sold them to the Federal Reserve at a profit. The Federal Reserve tried repeatedly to get the yield reduced to 0.75 percent on new issues or to shorten the maturity and lower the rate, but the Treasury would not change (Minutes, FOMC, March 1, 1944, at 11:40, 1).

Officially, the Treasury opposed the borrow and buy policy. In practice, it did little to prevent it (Eccles 1951, 361). As a result, nonbank purchasers acquired $147 billion of government securities (including nonmarketable war bonds) but held only $93 billion. Corporations subscribed to about $60 billion in bond drives but increased their holdings only $19 billion.

Commercial banks financed bond purchases by selling Treasury bills and other low-yielding securities to the Federal Reserve. With bill rates pegged and ceiling rates set on all other Treasury securities, the banks moved to the higher end of the yield curve. To limit bank purchases of long-term debt, many of the bonds were made “bank restricted.” Small and medium-sized banks complained that mutual savings banks and savings and loans could buy the restricted bonds and thus were able to offer higher returns to savers. In 1944 the rules changed to permit commercial banks to purchase restricted securities during bond drives up to 10 percent of their savings deposits (Board Minutes, December 7, 1943, 2–4). Overall, bank purchases were limited to $10 billion during all bond drives. Bank holdings increased by $57 billion, however (Eccles 1951, 362).13

As in World War I, debt finance was much less successful than claimed after the war bond drives. The monetary base doubled in the four years ending fourth quarter 1945, an 18 percent compound average annual rate of increase. Purchases of Treasury securities account for almost all of the $18 billion increase in the base.14

Eccles proposed a three-part alternative. First, he wanted more of the debt made ineligible for bank purchases. This limited the profits that nonbanks could make by buying bonds at a favorable price during bond drives and reselling them to banks after the drive. Second, Eccles thought more of the debt should be in nonmarketable securities to supplement the (nonmarketable) series E, F, and G bonds sold to individuals. The Treasury accepted part of this proposal, issuing a nonmarketable short-term bond. They did not issue a nonmarketable long-term bond, mainly because they did not want to pay the additional cost. Third, Eccles wanted to limit bank eligible issues to the residual amount required to finance the budget. He urged Morgenthau to sell banks only short-term securities with low yields. This “would have prevented the excessive profits which many banks were able to make” (Eccles (1951, 365).

To support Eccles’s suggestions, the executive committee of the FOMC voted to recommend a long-term program. On January 28, 1942, it sent a memo to the Treasury that proposed (1) tap issues (on demand) to absorb surplus funds of nonbank corporations; (2) a 2.5 percent rate on securities with fifteen or more years to maturity; and (3) flexible rates on shorter maturities, bounded between 0.25 percent and 0.5 percent for Treasury bills.

As on many subsequent occasions, the Treasury did not accept most of the FOMC’s suggestions. It was not interested in a long-term plan. Morgenthau preferred to remain opportunistic, and he was not concerned with rate flexibility or higher interest rates. He accepted only the fixed 2.5 percent maximum rate. At war’s end, he was proud of his achievement—financing more than $200 billion at an average cost of 1.94 percent. In World War I, he noted, the average interest cost was 4.22 percent (Blum 1967, 30).15

In all, there were seven war bond drives and a Victory Loan drive between November 1942 and December 1945. Judging from discussions by the New York Federal Reserve directors and the open market committee, problems with “speculators” increased in the later drives. The bank put limits on the volume of discounting and issued warnings to member banks not to participate in these activities (Minutes, New York Directors, November 16, 1944, 48; July 5, 1945, 8; October 25, 1945, 96).

The warnings did not reduce the undesired activities. The open market committee was reluctant to change course at the end of the war until the Treasury completed the last (Victory) bond drive in the fall of 1945. But it agreed unanimously to discuss with the Treasury “policies which should be adopted for the reconversion and postwar periods” (Minutes, FOMC, October 17, 1945, 5).

Price and Wage Controls

Unable to persuade the Congress to pass all its proposed tax increases, the administration turned to price and wage controls to prevent wartime inflation. In July 1941 the president asked for selective controls on prices, but the bill did not pass in the Senate. After the war started, Congress approved the Emergency Price Control Act in January 1942, authorizing selective controls.

In March the president appointed a committee to consider the inflation problem. The committee concluded that selective price controls would fail. It recommended controls on rents, profits, wage rates, and prices and a $50,000 a year limit on incomes of corporate executives and professionals.16 Workers would have an incentive to increase income by working more hours (at overtime rates). Morgenthau opposed wage controls, but he favored limiting profits to 6 percent of invested capital (Blum 1965, 314).

In April and July 1942 the administration tried selective price controls. Prices rose at a 4.8 percent annual rate in that year’s first three quarters. The administration considered that rate too high. The president requested authority to freeze prices and wages, warning Congress that if the bill was not passed by October 1, he would issue an executive order. The Stabilization Act gave the president broad authority to control prices and wages. A former senator, Justice James Byrnes resigned from the Supreme Court to administer the Office of Economic Stabilization. Controls remained until the fall of 1946, when Congress repealed the authority it granted in 1942.17

THE FEDERAL RESERVE IN WARTIME

In a prescient 1942 memo, the staff of the Philadelphia reserve bank analyzed the problem the Federal Reserve faced in wartime. Although the war was less than a year old, the bank’s staff projected that by the end of 1944 the government debt would reach $200 billion. Banks would hold between $85 billion and $100 billion; bank reserves would have to increase by $14 billion to $18 billion to support the purchases (Memo, Supply of Reserve Funds, Board of Governors File, box 1452, October 8, 1942). The memo concluded that open market purchases were the best method of supplying the reserves (ibid., 7).

With discount rates at 0.5 percent and open market rates on Treasury bills below 0.375 percent, banks preferred to sell bills rather than discount. The main wartime decision of the Federal Reserve was to keep this structure unchanged.

Pegged Rates

On April 30, 1942, the Federal Reserve announced its commitment to purchase all ninety-day Treasury bills offered “on a discount basis at the rate no higher than 0.375 percent per annum” (Board of Governors File, box 1441, April 30, 1942). It did not fix rates on other government securities explicitly, but it established a pattern of rates that it maintained throughout the war and beyond. It held one-year rates at 0.875 percent. At the longest end, it held the rate on bonds with twenty-five years or more to initial maturity to a maximum of 2.5 percent, as noted earlier. During the war and early postwar period, the duration of the longest-term bonds declined, but the maximum yield remained fixed.

The announcement put maximum Treasury bill rates above the rates prevailing at the time. During 1941 and early 1942, the Treasury bill rate had increased gradually from 0.02 percent to 0.25 percent. At the long-term end, bond yields had increased from 2 percent in much of 1941 to 2.5 percent in January 1942. The announcement had no effect on the long-term yield.18

The Federal Reserve did not vote to fix yields on all securities for the duration of the war. Memos written in early 1942 are explicit about rates on the shortest and longest maturities. Conversations with bankers and other active market participants show some concern that the 2.5 percent long-term rate might be too low; Federal Reserve officials wanted to increase the prevailing 0.25 percent rate on short-term bills. But the uniform opinion was that “the cost of war is a social cost and its risks should be borne by the public at large, not by any one group, such as those who have bought government securities” (Letter Sproul to Bell, Sproul Papers, Monetary Policy 1940–41, March 16, 1942, 2). “The Treasury, representing the public at large, should assume the risk of a change in credit conditions.”19 (ibid., March 10, 1942, 3).20

Households would get nonmarketable securities that they could redeem at the Treasury at a fixed price. This decision avoided the problem of imposing losses on the general public, a concern based on experience after World War I. Banks would be large holders of marketable debt, so it would be “necessary … for the Federal Reserve and the Treasury to protect that market, not only during the war, but during the post-war period” (ibid., March 16, 1942, 2). Sproul recognized that protecting the market meant that government debt would “have some attributes of a demand obligation.” The problem was to manage the debt “in the way least likely to contribute to … inflation” (2).21

A few days later, Sproul’s letter to Eccles summarized the agreement with the Treasury. At the short end, the Federal Reserve agreed to support the market “when the rate on Treasury bills reaches ¼ of 1 percent, and support[ing] with increasing strength as the rate approaches ![]() of 1 percent” (Sproul to Eccles, Sproul Papers, FOMC 1942, March 21, 1942). The general market would be kept “on about the present curve of rates but this … does not mean that we must hold the 2’s of 1951–55 or the 2½’s of 1967–72, or any other issue, at par, or any other fixed price” (ibid.). The System maintained this position for a time, but it was unable to get the Treasury to agree.22

of 1 percent” (Sproul to Eccles, Sproul Papers, FOMC 1942, March 21, 1942). The general market would be kept “on about the present curve of rates but this … does not mean that we must hold the 2’s of 1951–55 or the 2½’s of 1967–72, or any other issue, at par, or any other fixed price” (ibid.). The System maintained this position for a time, but it was unable to get the Treasury to agree.22

Even granting that the Federal Reserve had no choice but to finance the war at fixed rates, it was a mistake to accept the prevailing structure of interest rates. That structure reflected market anticipations in April 1942 about future economic expansion and inflation. The positive slope of the yield curve, expressing rates by maturity of the debt, suggests that the market anticipated that output, inflation, and therefore interest rates would rise over time. The fixed pattern of rates was inconsistent with this anticipation, so it invited debt holders to sell low-yield securities and buy at higher yields. Since the peg made all government securities equally liquid, or nearly so, the Federal Reserve’s decision was the cause of its principal problems for the next nine years. First, banks could lend to their customers for short periods at rates below the rates on long-term debt. As debts matured, bond prices rose to a premium. Holders sold, took capital gains, and purchased longer-term debt. Although the Treasury disliked both practices, it was unwilling to consider any changes in the structure of rates during the war. Second, banks followed the same pattern, selling bills with yields of 0.375 percent to the Federal Reserve and buying longer maturities with higher yields. By 1945 the Federal Reserve had acquired almost all of the outstanding bills: “They ceased to be a market instrument” (Eccles 1951, 359).

In the late 1930s, the Federal Reserve urged the Treasury to increase the supply of short-term debt. The Treasury refused. With the short-term rate fixed, the Treasury could now reduce interest cost by issuing a relatively large volume of short-term debt. At prevailing rates and policies, the market wanted more long-term debt. By fixing the structure of interest rates, the Federal Reserve sacrificed its ability to change the composition of the debt held by the public. Market demand dictated the amount and composition of its purchases and sales.

In 1944 some members of the open market committee began to shift their position. They asked the Treasury to increase bill rates to 0.5 percent by lengthening the initial term to four months (Minutes, FOMC, March 1, 1944, 5). Eccles opposed the request on the improbable grounds that large banks would use the additional revenue to absorb exchange charges on checks. Small banks would increase these charges, weakening the banking system (Board Minutes, March 8, 1944, 2).

Despite the comments about flexibility he made in 1942, Eccles favored the fixed rate structure throughout the war to reduce financing costs and to prevent owners of Treasury securities from profiting from war finance. He opposed a proposal to extend the maturity of the debt by selling more three- to four-year securities and fewer bills because “there was no reason why they [banks] should receive 1¼ or 1½ percent” (Board Minutes, Meeting of the Federal Advisory Council, December 4, 1944, 9). “It was highly desirable that the proportion of outstanding Government debt in the form of bills and certificates (under one year) should continue” (11). He regretted only that banks did not buy more short-term securities. It was a mistake, he thought, not to restrict them to these short-term issues in 1941 (13). The banks had too much profit.23

With its chairman firmly holding views of this kind, the Federal Reserve did not seek changes in interest rates during the war. Even if it had sought higher rates, it would have faced two obstacles. Morgenthau opposed any increase. And populists in Congress claimed the interest cost was too high. Congressman Wright Patman (Texas), a member of the House Banking Committee, denied that he wanted “printing press money.” He wanted lower interest rates: “If money must be created on the government’s credit, the taxpayers should not be compelled to pay interest on it” (Board of Governors File, box 141, July 1942).24

The Board and the banks understood the inflationary consequences of pegging rates, but they did not oppose the policy during the war. Those most concerned about inflation urged higher income tax rates, sales or expenditure taxes, or compulsory savings to absorb purchasing power. To improve understanding of the problem and disseminate information more widely, Eccles urged the reserve banks to expand their research staffs and coordinate their efforts through a System committee (Board Minutes, March 2, 1943, 2–7).25

Open Market and Other Purchases

With rates fixed, the FOMC had little to do. It approved new limits on the size of the account and authorizations to purchase and sell. It spent much of its time discussing problems associated with bond drives, banks playing the pattern of rates, and the possibility of lending to banks instead of buying securities or using repurchase agreements instead of discounts and outright purchases.

Banks held more than $6.5 billion of excess reserves early in 1941. At first they purchased securities by reducing excess reserves. The decline was most rapid in New York, slowest at country banks.26 By August, New York banks had all but eliminated their excess reserves (Minutes, FOMC, August 8, 1942). To provide reserves, the Federal Reserve removed all restrictions on the amount of short-term securities (bills and certificates) in the System Open Market Account by the end of 1942. Limits on the amount of longer-term securities remained.

Table 7.2 shows the rates of purchase from 1942 to 1945. By the end of the war, short-term government securities had become the Federal Reserve’s principal asset. The pre–World War I problem of a portfolio insufficient to offset a gold inflow or, in the 1930s, excess reserves greater than the portfolio, would not return. Financing World War II left the Federal Reserve balance sheet and the monetary base dominated by the open market portfolio. This result was very different from the founders’ plan; the System had become an indirect source of government finance.

It soon became a direct source as well. On March 27, 1942, the second War Powers Act authorized Federal Reserve banks to acquire direct or guaranteed obligations of the United States by purchase from the Treasury. Eccles supported the bill enthusiastically. At one point he suggested that the FOMC should view the change as a new method of distribution: “Instead of having to … price an issue at a figure which would attract heavy oversubscriptions, the securities could be taken by the System and sold to the market as it could absorb them” (Board Minutes, February 3, 1942, 4).

Other Board members accepted the change as a wartime measure needed to ensure that Treasury issues would not fail to find buyers at established rates and to furnish funds for short periods around tax dates. Sproul, who was at the meeting, did not oppose the amendment. He criticized the Board’s failure to discuss the subject with the president before it was included in the War Powers bill, and he opposed Eccles’s suggestion that the reserve banks distribute government securities. He accepted direct purchases as a temporary measure to help the Treasury around tax dates or in an emergency.27

The change repealed a section of the Banking Act of 1935 that prohibited the System from purchasing government securities except in the open market. A few months later, the Board told the account manager to combine direct purchases from the Treasury with open market purchases in the weekly statement. The War Powers Act expired six months after the war ended; initial authority for direct purchases expired in December 1944. The Board requested renewal for two more years; later the authority became permanent.

Despite the low interest rates on short-term debt, war finance greatly increased earnings of the reserve banks. Net earnings rose from an average of $11 million for 1937–41 to more than $92 million in 1945. The Federal Reserve had been relieved of payments to the United States Treasury after 1933 in exchange for the capital provided to establish the Federal Deposit Insurance Corporation.28 By September 1942, Vice Governor Ronald Ransom anticipated that the government would reinstate the franchise tax if earnings rose (Board Minutes, September 15, 1942, 2). He was correct but premature. Congress imposed a tax equal to 90 percent of annual net earnings in 1946. The tax offset a substantial portion of the interest payments on Treasury debt held by the reserve banks.29

Reserve Requirements

With the bill rate at 0.375 percent in 1942 and income taxable at high wartime rates, banks outside New York and Chicago did not bother to invest in bills or send excess reserves to correspondent banks. The Treasury wanted to reduce reserve requirement ratios for urban banks to release reserves for purchases of Treasury securities.

The Banking Act of 1935 did not permit the Board to change reserve requirements for only one class of banks. Congress approved the additional authority on July 7, 1942. The change was contentious within the System. The Federal Advisory Council opposed the change, and initially so did the Board. Eccles described the reduction as “a grave mistake” (Board Minutes, February 16, 1942, 2–3). Prodded by the Treasury, once the legislation passed, the Federal Reserve reduced required reserve ratios at central reserve city banks in three steps, from 26 percent to 24 percent on August 19, 22 percent on September 14, and 20 percent on October 3. Together the three reductions released $1.2 billion, about 6 percent of the monetary base at the time.

The New York and Chicago banks bought Treasury bills, as expected. The principal effect of the change was not on reserves or the monetary base but on the earnings of the banks and reserve banks. With interest rates rigidly fixed, banks as a group determined the aggregate amount of reserves by buying or selling Treasury bills. Further, New York and Chicago banks could create more deposits and add more to earning assets per dollar of reserves or base money. Contrary to Eccles’s aim, the reserve banks had smaller earnings and the banks had more.30

The three changes brought required reserve ratios for the two central reserve cities to equality with reserve city banks for the first time in Federal Reserve history. There were no further changes in reserve requirement ratios during the war. The only other wartime change removed reserve requirements on war loan deposits as an inducement to banks to buy securities by increasing Treasury deposits during bond drives.

Discount and Other Rates

Discount rates ranged from 1 to 1.5 percent when the war started. After some prodding from the Board, on April 11, 1942, the reserve banks agreed to a uniform discount rate of 1 percent. In addition to the basic discount rates, the Federal Reserve set a preferential rate for loans collateralized by short-term government securities and a rate on direct loans to military contractors made under its authority to lend to individuals and businesses. The latter provision, a depression measure, was used to finance production of war materials. The amount outstanding on June and December reporting dates never exceeded $35 million (lent in 1936). During World War II, the total outstanding was about $10 million. Almost all the loans were for one year or less (Board Minutes, 1976, 492).31

Analysis at the Philadelphia reserve bank correctly noted that banks would obtain reserves at lowest cost and would hold debt with higher rates and longer terms to maturity. With discount rates above Treasury bill rates, discounting remained small. The memo criticized preferential rates for loans collateralized by government securities. Preferential rates would not affect the volume of borrowing, only the collateral used to borrow and the maturity of bank-held debt (Board of Governors File, box 1452, October 8, 1942, 7–10).

The Philadelphia bank’s memo was critical of preferential discount rates on other grounds also. The memo rejected the real bills doctrine: “The experience with preferential rates in the last war and the postwar period on the whole was not satisfactory. The general conclusion of Reserve officials and analysts is that the particular paper used to secure an advance has no relation at all to the use that the bank will make of the funds it secures” (ibid., 9).

Despite this correct analysis, the Board adopted a preferential discount rate of 0.5 percent for discounts secured by short-term governments. The main argument for the preferential rate was that it would induce banks to hold more short-term bills instead of higher-yielding bonds. George L. Harrison said that it would be easier to eliminate the preferential rate, when it was time to reverse policy, than to increase the general discount rate (Board Minutes, October 7, 1942, 9).32

Harrison underestimated the Treasury. In June 1945 Sproul proposed an increase in the preferential rate to 0.75 percent. All the presidents concurred, but the rate remained at 0.5 percent (Minutes, FOMC, June 20, 1945, 9). The following month, the New York bank directors asked to eliminate the preferential discount rate. The Treasury remained unwilling, so the rate stayed (Minutes, New York Directors, July 19, 1945, 20).

Bankers grumbled occasionally about Treasury tax and interest rate policies. When the opportunity arose, members of the Federal Advisory Council argued for higher rates on short-term securities to get banks to hold more of them. The most strenuous plea came from a member who argued that banks could not be expected to finance the war if they were “‘bled white’ through the maintenance of low interest rates and application of high taxes” (Board Minutes, April 9, 1942, 13).33

Selective Credit Controls

Unable to control money or interest rates, the Board turned first to controls on consumer credit and later to controls on real estate, stock market, and other forms of lending and borrowing. Some of these actions were taken to show that it was “doing something” to control inflation, some in the belief that it had to use existing authority before Congress would grant additional powers, and some at the urging of other agencies.

The Board adopted regulation W to reduce the demand for durable goods. The original order required a 20 percent down payment and limited loans to a maximum of eighteen months. Wartime revisions and amendments extended the range of goods covered, raised the required down payment, and reduced the maximum term.34 Experience with regulation established once again that efforts to control a complex economy produce unforeseen consequences leading to both extensions and exclusions from earlier regulations.35 Since credit is fungible, restrictions on one type of credit shifted demand to less regulated forms and encouraged innovation to circumvent regulations.36

By 1943 the Board began to discuss extending credit regulation to include real estate, securities, and traded commodities. Eccles explained to the reserve bank presidents that “the Board was not seeking the authority … but was willing to accept it” (Board Minutes, June 29, 1943, 21). Eccles preferred to increase taxes and forgo additional regulation, but he accepted the new responsibility to retain credit control under the Federal Reserve System: “Some of the Presidents indicated agreement with Chairman Eccles’s attitude and expressed doubt as to the ability of any agency successfully to discharge the responsibility” (22).

Enforcement differed across the country because each reserve bank chose the extent of enforcement. Vice Chairman Ransom complained at one point that the Board had chosen a middle course between strict and lax enforcement. Strict enforcement “would antagonize the people whose support was necessary,” and lax enforcement would foster the “impression that the System did not care whether the provisions of the regulation were observed” (ibid., 23).

Years later, W. Randolph Burgess summarized matters: “Looking back at the experience with the control of consumer credit, it would be very hard to make a case that what was done … was useful, and it certainly made a great deal of work for a great many people, at a time when there was a shortage of manpower and a heavy surplus of irritating red-tape and procedures to interfere with essential war work” (Letter Burgess to Sproul, Sproul Papers, Board of Governors, Joint Committee on Economic Report, October 7, 1949, 2).

Common stock prices had fallen a total of more than 20 percent from 1939 to 1941. Stock prices rose 20 percent in 1942 but remained below their 1938 value (Ibbotson and Sinquefeld 1989). In March 1943 the Board began discussing increases in margin requirements on securities. The volume of trading had increased to about one million shares a day, making some of the staff uneasy. Earlier, the Board had issued regulations T and U to set margin requirements as authorized by the 1934 Securities Exchange Act. Some staff members urged a preemptive strike against speculation, but the Board decided not to act (Board Minutes, March 15, 1943, 2–4). Prices continued to rise. By the end of 1944, the stock price index was almost 40 percent above the 1936 peak.

On February 5, 1945, the Board increased margin requirements to 50 percent. Eccles argued that there was no evidence of excessive use of credit in the stock market, but the Board approved the increase to show that it was concerned about future inflation (Board Minutes, February 2, 1945, 3–9).

Three weeks later, Eccles reported that the Economic Stabilization Board had suggested a 100 percent margin requirement. Eccles saw no need for the change, but Chairman Vinson of the Stabilization Board thought that Congress would not authorize new powers to control inflation until existing powers had been used. Eccles suggested that Vinson send a letter to the Federal Reserve asking for the increase in margin requirements (Board Minutes, February 23, 1945, 7–8). Vinson sent the letter, but the Board delayed a decision.

By a vote of five to one, the Board agreed to let Eccles tell the Economic Stabilization Board that the System favored an increase only to 70 percent. Governor John K. McKee opposed because the government’s anti-inflation program was incomplete, and not much credit had been used for purchasing and carrying securities (Board Minutes, May 3, 1945, 7–8).37

The Federal Advisory Council agreed unanimously that speculation in real estate and stocks should be discouraged, but it saw little evidence of inflationary pressure in asset markets: “Farm lands are about where they were in 1913… . There has been a good deal of speculation in the larger apartment buildings and hotels and in some kinds of commercial buildings, but even there the prices are below the cost of reproduction. Stock prices are not above the 1936–37 levels, in spite of the fact that in the interim most corporations have added very materially to their assets” (Board Minutes, May 14, 1945, 2).

By late June 1945, with the war almost over, the Economic Stabilization Board agreed to recommend credit controls on real estate, higher margin requirements on stock transactions, and a longer holding period for capital gains. It considered an increase in the capital gains tax rate. It could not decide whether new construction should be exempt from real estate controls. Eccles believed that the new credit controls would be ineffective and should not be used unless Congress passed a tax increase (Board Minutes, June 21, 1945, 18–19).

Pressed by the administration, the Board voted to increase margin requirements on new purchases of securities to 75 percent effective July 5. The Board also required that the proceeds of security sales be used to bring the margin on the whole portfolio toward the new requirements before cash could be distributed to the owner. Governor McKee again opposed the increase.

The new requirements were unpopular with the public and with many bankers and securities dealers. In September the Federal Advisory Council urged the Board to consider returning to a 50 percent margin. Eccles thought it was premature to consider a reduction. Effective January 2, 1946, the Board increased the margin requirement to 100 percent; all transactions had to be for cash.

Other Wartime Changes

Rapid growth of the Federal Reserve’s portfolio and the monetary base, and a small gold outflow, lowered the System’s gold reserve ratio toward the legal limit—40 percent of notes in circulation and 35 percent of deposits at Federal Reserve banks. By mid-1944 the System’s gold reserve ratio had fallen to 55 percent (from 91 percent in November 1941).

The FOMC minutes first mention the problem in May 1944. The committee voted to reallocate Treasury bills in the System account to prevent the ratio at any reserve bank from falling below 45 percent. Members agreed to buy Treasury bills from the reserve banks with low ratios and to change the allocation of open market purchases (Minutes, FOMC, May 4, 1944, 14–15). Several banks sold Treasury bills to other reserve banks for gold certificates, and the Federal Open Market Committee revised the securities allocation formula to adjust for differences in gold reserves.

The System’s gold reserve ratio continued to fall. In July the executive committee considered asking Congress to reduce the ratio to a uniform 25 percent against notes and deposits. Eccles favored eliminating the requirement, but the committee thought the public was not ready to remove all ties to gold. The executive committee voted to put off any decision until after the election.

Legislation introduced in January, and passed in June, lowered the gold reserve requirement to 25 percent and extended the “temporary” authority, first granted in 1932, to use government securities as collateral for Federal Reserve notes.38 The FOMC responded by lowering from 45 percent to 35 percent the gold reserve ratio at which the individual reserve banks would cease to participate in open market purchases. Table 7.3 shows that even after the legal change, several of the reserve banks did not meet the requirement.

Eccles attempted to coordinate the research functions at the reserve banks under the direction of the Board’s research division. The issue had arisen first in 1936, after the Banking Act of 1935 became law. It arose again in 1943, under the guise of having a “steering committee” to give direction to research work. The reserve banks resisted and, on both occasions, prevented the Board’s staff from acquiring authority over the banks’ staffs (Sproul Papers, Memorandums and Drafts, December 17, 1943). Eccles tried again, claiming that the Board had the right to approve persons appointed to supervisory positions in the banks’ research departments, but he did not prevail over the protests of the banks’ officers and directors (Minutes, New York Directors, August 17, 1944, 267).

To supplement wartime price controls, the government ordered coupon rationing of gasoline, food, shoes, and other consumer goods. Purchasers presented coupons along with cash to complete transactions. Processing ration coupons became the responsibility of commercial banks and Federal Reserve banks beginning in January 1943.

The army decided early in 1942 to move Japanese and Nisei living in the western states into camps. After the administration approved the order, Japanese and Nisei had to leave their homes and businesses. The Treasury had responsibility for protecting the property they left behind. The Federal Reserve banks administered the program for the Treasury (Blum 1967, 3–4).39

POSTWAR PLANNING

Planning postwar economic policies began long before the war ended. Interwar experience convinced many businessmen, economists, and others that it would be unwise, and probably unacceptable, to return to the high unemployment rates and instability that characterized the interwar period. Keynes’s General Theory (1936) seemed to provide an economic rationale for activist government policies to expand or slow domestic economic activity.40 His plan for international monetary cooperation, prepared during the war, made a major contribution to the development of the postwar Bretton Woods institutions. Earlier, in his Treatise on Money (1930), he had made the case for international monetary reform, based on a more flexible gold standard. These topics moved to the forefront in planning for the postwar world.

Discussion of postwar planning shows significant changes in policy views since the 1920s. Two changes eventually altered the role of United States monetary policy. First was the commitment to economic stabilization. This commitment was a long step away from the Federal Reserve’s denial in the 1920s that its actions affected the price level or the pace of economic activity. Second was the primacy given to domestic over international considerations. The proponents of these changes assigned a very modest role to monetary policy and the Federal Reserve. As the perceived influence of monetary policy changed in the 1950s and 1960s, full employment and domestic stability became dominant policy concerns by the 1960s. Although not fully recognized at the time, the heightened emphasis given to domestic concerns in many countries was incompatible with plans for an international monetary system based on gold and fixed exchange rates.

Domestic Plans

In spring 1943 the System began to study postwar reconversion. One set of issues was transitional. For example, when the military canceled contracts, small and medium-sized firms would need loans to convert to peacetime production just as regulation V loans to finance military procurement ended. The System appointed a committee to study transitional lending (Board Minutes, April 29, 1943, 5–7; June 20, 1943, 5–7). In May 1944 the Board authorized a series of studies of postwar policies. A sample of the ideas gives the flavor of many economists’ opinions at the time.

The Board’s economic adviser, Emanuel A. Goldenweiser, recommended the “continuation of wage and price controls, rationing and allocation, as well as licensing exports … [as] a prime condition of a successful transition from a war to a peace economy” (Board of Governors of the Federal Reserve System 1945, 1:3). Goldenweiser proposed that the government offer employment to any unemployed worker to sustain consumption. He favored keeping selective credit controls, margin requirements, and “all the powers over the general volume and cost of money that they have had in the past, and they should have additional authority over member bank reserves” (1:15). The “additional authority” is probably a reference to a secondary reserve requirement of securities to prevent banks from selling Treasury bills to the reserve banks.

Unemployment was a main concern. The second study in the Board’s series warned of another 1929 collapse and unemployment of 6 to 8 million during reconversion to peacetime (ibid., 1:18–49).41 Postwar experience turned out very differently. Reconversion occurred quickly. After a brief adjustment, economic activity rose rapidly. Unemployment remained low.

Like Goldenweiser, Eccles believed that price controls should be retained until postwar output increased enough to satisfy demand. He testified that “price controls, rationing, curbs on consumer credit or stock market credit, and similar devices, admittedly deal only with effects and not with basic causes of inflationary pressures” (House Committee on Banking and Currency 1946, 171).42 Nevertheless, he believed that an opportunity to control inflation was lost with repeal of the excess profits tax in 1945, termination of the War Labor Board, and failure to increase the capital gains tax at the end of the war (Board Minutes, November 19, 1945, 10–11). He did not mention that these wartime measures distorted allocation and slowed investment. Nor did he recognize that price and wage controls caused many low-priced goods to disappear and encouraged producers to lower quality as a substitute for raising prices. Similarly, wage controls encouraged both labor “hoarding” and shortages and the substitution of noncash benefits for cash payments.43 Neither he nor his staff recognized that deregulation and correct price signals would speed the transition and reduce waste.44

Congress did not concur. It responded to the general dissatisfaction with wartime controls, rationing, and black markets by removing most controls by fall 1946. The immediate effect was a short-lived surge in the reported price index, as reported prices adjusted to reflect hidden or deferred changes (see chart 7.1 above). Consumer prices rose at a 29 percent annual rate between June and November, with the largest rise in July. By January 1947 the monthly increase had fallen to zero.45 After these adjustments, price levels were 33 percent above the level at the start of the war, a 6.5 percent annual rate of increase.

Lauchlin Currie, on the White House staff, and Keynesian economists at Commerce, Treasury, and other agencies believed that a severe postwar depression was likely. They bolstered their argument by showing that private spending would not expand enough to replace military spending as a source of employment. Much of the shortfall was a consumption “gap”—the difference between predicted consumption spending and spending consistent with full employment. And because the consumption gap would be large, private investment would remain low and unemployment high.46 Beginning in 1944, Keynesian economists urged gradual release of materials from military use to smooth postwar readjustment. The military opposed the change while the war continued, and nothing was done. Interest in peacetime conversion rose when the European war ended in April 1945. The National Resources Planning Board advocated a comprehensive social welfare program, pollution abatement, public transport systems, and other government programs.

Nothing in Keynesian analysis favored government spending instead of tax reduction as a way for government to influence the transition from war to peace. Largely as a matter of belief, administration economists and their outside advisers favored government spending.47 System economists were divided.48

President Roosevelt adopted part of the Keynesian program. His last State of the Union message to Congress set a goal of 60 million postwar jobs. At the time, there were 55 million people in the civilian labor force and an additional 11.4 million in the armed forces, but some of these were women who were expected to leave the labor force after the war. The statement was seen as a loose commitment to “full employment.”

Roosevelt’s statement was soon followed by a proposed Full Employment Act that became the Employment Act of 1946.49 The original proposal recognized a person’s right to employment and the government’s responsibility to provide full employment. To achieve this end, the proposal called for some national planning: a National Production and Employment Budget would forecast the state of the economy and the levels of employment and output consistent with full employment. The president would recommend actions needed to close any “gap” between expected and full employment.

Discussion of the bill shows the large shift in opinion that had occurred in a decade. The bill had three Republican senators as sponsors and more than one hundred sponsors in the House, including Congresswoman Clare Booth Luce, a prominent conservative and the wife of a prominent publisher. Few in Congress criticized the commitment to an expanding economy or the idea that government spending could affect the economy. The right to a job and a commitment to full employment were more contentious. Opponents pointed to the risk of inflation, the possibility of continuous budget deficits, and the possible use of the act to promote “national planning,” price controls, or other restrictions on freedom.

The act that emerged was a compromise, but it gave more to the opponents than to the original proponents.50 Gone were the commitments to full employment and mandatory computation of the “gap.” The legislation called only for “maximum employment, production, and purchasing power,” a phrase that was undefined, therefore open to whatever interpretation an administration or Congress might put on it. Gone also was a legislated commitment to forecasts of economic activity, although forecasting became standard procedure in all administrations.51

The act created a Council of Economic Advisers in the Office of the President to help the president decide on economic policy. The intention may have been to keep the council as a professional body, free of politics. In practice the council, as a staff agency, had a weaker position than many of the current and future line agencies representing business, labor, environmental, educational, consumer, and other interest groups. The role of the council has varied with the president’s interest in receiving its advice and the relationship between the council’s chairman and the president.52

The Board’s reaction was generally positive and supportive of the original bill. Woodlief Thomas, assistant director of research at the Board, read the bill as an attempt to “legislate the Keynes-Eccles-Hansen-Beveridge theory of economic stabilization” (Memo Thomas to Ransom, Board of Governors File, box 198, February 12 and 4, 1945). Thomas saw enactment of a particular economic theory as a danger, but the act did not do that. The bill, he said, was “a statement of goals, not an outline of policies” (ibid.).

Eccles had favored countercyclical use of fiscal policy since the early 1930s. He came to Washington early in the New Deal to promote that policy. In a letter to Senator Robert Wagner, he accepted the objectives of the bill but emphasized the primary role of the private sector in providing employment. He urged Wagner to substitute for full employment “maintaining economic stability at as high a level of employment and production as can be continuously maintained” (Eccles to Wagner, Board of Governors File, box 198, June 16, 1945). Although he discussed the Federal Reserve, he did not mention monetary policy as a tool for reaching the objectives of the act.

Neglect of monetary policy was not an oversight. The conventional view among economists at the time was that monetary policy had, at most, modest effects on output and prices.53 These beliefs justified the passive monetary policy that the System chose mainly for political reasons. When conventional views changed in later years, the Federal Reserve accepted major responsibility for moderating recessions and controlling inflation.

International Plans

Planning for postwar international monetary cooperation began before the United States entered the war. Section 7 of the lend-lease agreement, under which Britain and others obtained military supplies and equipment “on credit,” provided that the United States could waive postwar repayment if the British agreed to eliminate trade “discrimination” and reduce tariffs. Discrimination was not further defined, but the objectives it expressed included elimination of the prewar system of imperial preference that bound Britain to its empire and favored British exports.

Avoidance of bilateral agreements and imperial preference was a major goal of the State Department. Secretary of State Cordell Hull favored a multilateral system centered on “most favored nation” clauses that gave each signatory the lowest tariff rate agreed with any other country. The British accepted section 7 out of wartime desperation. They did not like it (Presnell 1997).

In the course of negotiations leading to the lend-lease agreement, Keynes broadened the terms of reference to include finance and exchange rates. The two treasuries then took the lead in negotiations, shifting emphasis from trade issues to finance. By September 1941 Keynes had developed a proposal for an international clearing union that could create a currency for member central banks to use in settling payments imbalances. After adjustment, Keynes’s proposal became the British government proposal in April 1943, when formal bilateral discussions began.

Keynes (1924) had developed the basic analysis much earlier. Each country acting alone can achieve either stable prices or a fixed exchange rate but not both. To achieve both, there must be international cooperation or agreement. The gold standard is one type of agreement; each country accepts the rules of the standard, defining currency value in grams of gold, agreeing to buy and sell gold at a fixed price, and allowing money and prices to rise or fall with gold movements. If member countries followed these rules, exchange rates would remain fixed and inflation or deflation would be limited to changes around the world price level, the latter set by world demand for and output of gold. Large productivity shocks might disrupt countries’ efforts to maintain employment and stable prices, but prices and output would eventually adjust as required by the fixed exchange rate.

The rules, however, required procyclical policies—allowing gold inflows to inflate the economy during expansions and to accept contraction, unemployment, and deflation when gold flowed out. With the growth of industrialization, labor unions, and the spread of the voting franchise, voters and governments were less willing to follow such rules in the 1920s. Many proposals to eliminate or reduce procyclicality had been made, but none had been adopted.54

In December, a week after the United States entered the war, Morgenthau asked Harry Dexter White to “prepare a memorandum on the establishment of an inter-Allied stabilization fund” as the basis for postwar international monetary arrangements (Blum 1967, 228–29).55 Morgenthau’s diary suggests that, although the United States had insisted on title 7, he had no more than a vague idea about expanding the prewar Tripartite Agreement to avoid competitive devaluation.56

The British were particularly interested in preventing a return of their interwar problem, when efforts to expand their economy by lowering interest rates were followed by a current account deficit and an outflow of gold that reduced the money stock and forced contraction and deflation.57 White, and others at the United States Treasury, also favored a more flexible system. He too proposed a middle way between fixed and fluctuating rates with rules for lending and borrowing. Exchange rates would be fixed but adjustable; countries with a balance of payments surplus (like the United States in the 1920s) would lend to countries with deficits (like Britain in the 1920s). Unlike Keynes’s plan, the new international institution could not create money.

The plan envisaged that deficit countries would not be forced to contract and deflate for balance of payments purposes. They would maintain imports from the rest of the world instead of reducing purchases and spreading contraction. To enforce lending, member countries agreed to impose costs on surplus countries that would neither expand imports nor lend to countries in deficit. Thus deficit and surplus countries alike would benefit from increased flexibility.58 Both Keynes and White limited their proposals to financing trade and current account deficits. To the extent that they considered lending and borrowing on capital account, it was the responsibility of the proposed International Bank for Reconstruction and Development, later called the World Bank.59

Countries could pursue the domestic policies of their choice, a main British aim and another major departure from classical gold standard rules. Countries could correct policy errors by changing the exchange rate, with the consent of the new agency, the International Monetary Fund. The fund would also prevent multiple currency practices, discriminatory bilateral arrangements, and competitive devaluations. Eventually countries would maintain current account convertibility, a main aim of the United States.

Many in the banking community and the Federal Reserve wanted to return to the gold standard. White dismissed these proposals: “There isn’t the slightest chance of getting other countries to return to the gold standard” (White to the Board and Reserve Bank Presidents, Minutes, FOMC, March 2, 1945, 20). The only chance for agreement was to combine stability of exchange rates with the flexibility to change them with the fund’s approval. Other countries would agree to this mixture of stability and flexibility if it was part of an agreement that gave each country some assurance that it could borrow in an emergency: “We must give them time to balance their payments in such a way that they will not hurt the rest of the world” (25). Adjustment might take two, three, five, or even ten years.

The Reserve Board began to consider the Keynes and White plans in May–June 1943. Their first concern was the amount of new bank reserves that the United States would have to create. To eliminate all restrictions on current account financing, as Keynes proposed, required an expansion of $25 billion to $30 billion of United States base money. An expansion of this magnitude would double the amount of base money then outstanding. Board members wanted either power to control the domestic effect of such a large increase or a limit on the size of the increase (Board Minutes, May 29 and June 1, 1943). The Board also favored a provision, suggested by the Canadian representatives, that if the amount of foreign exchange balances at the fund increased beyond a preset limit, the member would gain voting power (ibid., June 1, 1943, 4). This would permit a surplus country to eventually limit borrowing and expansion of its money stock. The British would not accept this proposal. They remembered the policies of surplus countries (the United States and France) in the 1920s and did not intend to repeat the experience.

As the plan developed, the Board’s discussion of substantive issues ceased. Board staff participated actively in meetings organized by the Treasury, but few of the issues they raised came before the Board. The Board never considered the merits of alternative proposals and objections to the plan by leading bankers and the New York reserve bank.