SIX

The Federal Reserve took few policy actions from 1933 to 1941. The open market portfolio and the discount rate rarely changed. Changes in the monetary base during these years reflect principally changes in the gold stock and the devaluation of the dollar against gold; after the gold standard broke down the United States more closely followed gold standard rules for the money stock.

Congress and the Treasury made the important decisions about gold, silver, and banking legislation. Early in the administration, President Roosevelt took an active part in setting gold policy and making decisions about gold and silver purchases and exchange rates. The Federal Reserve had a subsidiary role—the backseat. New York transacted for the Treasury, as fiscal agent, but the Board had little influence on the decisions and was often uninformed about Treasury actions and plans.

The Banking Act of 1935 permanently changed the Federal Reserve’s structure and laid the foundation for the postwar Federal Reserve System. Out went the legal basis for semiautonomous, regional banks, each controlling its own portfolio. Reorganization shifted power and authority over the reserve banks to the Federal Reserve Board in Washington, where it remained. Although the Treasury controlled most decisions until after World War II, the 1935 act made possible the centralized system that developed once the Federal Reserve became free to pursue an independent policy.

Reorganization was mainly the work of Marriner S. Eccles, a Utah banker, aided by Lauchlin Currie, a young economist at the Treasury and later at the Board and in the White House as a presidential adviser. Eccles became governor of the Federal Reserve Board in November 1934 and, after reorganization, the first chairman of the Board of Governors in 1936. He was a strong proponent of government investment spending as a countercyclical policy and believed that the Federal Reserve should keep market rates low to facilitate private spending and government finance during a depression. He called his program “controlled inflation.”

Despite these strongly held views, Eccles and the Board became convinced after 1935 that the growing volume of reserves at member banks posed the threat of future inflation. The Board’s principal policy action in these years increased reserve requirement ratios as a preemptive act against inflation. Between August 1936 and May 1937, the Board doubled these ratios, thereby contributing to a steep recession in 1937–38.

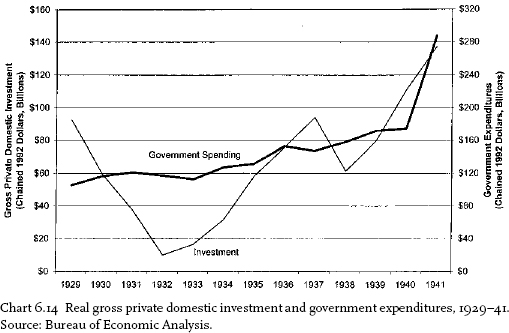

Until 1937, recovery from the depression proceeded rapidly. In the four years following the trough in March 1933, using Balke and Gordon’s (1986) data, real GNP rose at a compound annual rate of almost 12 percent. After a sharp decline in the 1937–38 recession, growth resumed in mid-1938. Real GDP did not reach its 1929 value until 1941, however, and per capita consumption did not regain its 1929 peak until 1942.1

Prices rose during the recovery, in part a result of deliberate policy to devalue the dollar so as to raise agricultural and commodity prices. The GNP deflator and the consumer price index remained below their 1929 levels, however, when the United States entered World War II.

Despite the strong recovery, many contemporary observers, including prominent administration officials, regarded President Roosevelt’s New Deal as unsuccessful. The principal reason is that 8 million people, more than 14 percent of the labor force, were unemployed in 1940. In fact, the number employed in 1940 was the same as in 1929, and hours worked were lower. Viewed one way, there was a substantial increase in productivity, but part of the measured increase was a substitution of capital for labor to avoid costly New Deal legislation. These measures sought to raise wages, reduce hours of work, and encourage the growth of trade unions. Militant unionism, particularly in manufacturing industries such as autos, steel, and rubber, reduced current and expected profits in those industries and deterred investment.

Labor legislation was one part of President Roosevelt’s New Deal. The period 1933–41, particularly the early years, was a time of intense legislative activity. The New Deal restructured society, permanently changing the role of government and the public’s attitude toward the responsibilities of government. Lasting changes were made in the financial system and the Federal Reserve.

Much of the period’s financial legislation reflected the judgments reached by the authors of the new legislation, often shared by much of society at the time, that speculation was responsible for financial collapse and the Great Depression. Taken as a whole or separately, much of the new financial legislation sought to prevent or limit speculation in common stocks, restrict banks from financing securities, and centralize authority and responsibility for monetary policy2. The Securities Exchange Act (1934) gave the Federal Reserve Board authority to set margin requirements in the belief that general monetary powers, such as open market operations or discount rate changes, cannot prevent a speculative boom in stock prices without harming the so-called legitimate needs of trade.3 Parts of the Banking Act of 1933, generally referred to as the Glass-Steagall Act, separated commercial banking from investment banking. This section of the Banking Act was mainly the work of Senator Carter Glass. A leading proponent of the real bills doctrine, Glass was convinced that the boom and bust had been caused by commercial bankers’ financing investment banking activities and other nonreal bills.4

In retrospect, the period marks the beginning of the decline in the importance of the real bills doctrine at the Federal Reserve. The 1932 Glass-Steagall Act permitted government securities to serve as backing for the note issue. Conceived as a temporary step, lack of discounts during the depression required renewal of temporary authority, later made permanent. At the end of the period, the beginning of wartime expansion restructured the Federal Reserve’s balance sheet. Government securities became the principal source of reserve bank credit. Growth in the size of the balance sheet and wartime inflation made it less costly to reduce, and later eliminate, reserve requirements behind the note issue and the monetary base than to shrink the base and force postwar deflation.

Other legislative changes reshaped the Federal Reserve by reducing the power of the New York Federal Reserve bank domestically and internationally. Glass and others believed that Benjamin Strong’s assistance to Britain in 1924 and, even more, in 1927 initiated the speculative boom that ended in the collapse. A widely shared view held that the collapse was an inevitable consequence of previous speculative excesses and departures from real bills principles. Unorthodox policies, such as the Hoover budget deficits and Britain’s departure from gold, sustained and deepened the collapse. Hence the remedy was to reduce the influence of those like Strong whose ideas, they believed, had failed.

None of this was lost on Adolph Miller. Miller, a friend of both Glass and Roosevelt, saw the Banking Acts of 1933 and 1935 as a vindication of his views (Miller 1935). He believed that by centralizing power in the Board, and eventually restoring the gold standard, the Federal Reserve would return to its original conception. In this he was mistaken.

A contemporary reader finds it difficult to reconstruct the prevailing orthodoxies of the past or to see events as they were seen at the time. Bernard Baruch, a financier who advised many presidents, perhaps typifies the views of the more articulate and influential bankers and financiers of the period. In testimony before the Senate Finance Committee in February 1933, Baruch blamed the depression on four factors, all the effects of war: inflation, debt and taxes, national self-containment, and excess productive capacity (Baruch 1933, 1). The “chief barrier” was wartime inflation. Only in 1933 could prices be said to have fallen to the 1913 level. Reflation by monetary means to restore prices to the 1929 level was the wrong policy. Prices could not be raised by increasing money: “If there is no confidence, no amount of tinkering with the currency can raise the price level… . Deficits and the finance of them by ‘bank money’ inflation … impair confidence and drive money deeper into hiding” (9). A main task of government was to reduce public spending. Although he favored relief of human suffering, he believed that “reduction in public expense is indispensable for recovery” (2). Reductions in spending and the budget deficit instill confidence and “the working of natural processes” (4). Baruch’s views are similar to the views of the Economists’ National Committee on Monetary Policy, a group that included prominent academic economists.

Views like these were not just wrong, they were influential. They appealed to beliefs that were widely shared. They called for more deflation and contraction in the mistaken belief that the 1913 price level (or some other) was correct. Restoration of that price level would somehow right whatever was wrong, but the proponents could not say how or why that would happen.

Not all financial legislation and action corrected past mistakes and alleged misdeeds. Roosevelt had campaigned as a financial conservative, critical of the Hoover administration’s deficit spending, but he also wanted to end the depression and stop the fall in prices. He promised to balance the budget, except for emergency relief, but he offered few specific proposals during the 1932 campaign and had no coherent plan for the economy when he took office.5 During the campaign, Roosevelt described himself as an advocate of experimentation: “The country needs and, unless I mistake its temper, the country demands bold, persistent experimentation. It is common sense to take a method and try it. If it fails, admit it frankly and try another. But above all, try something” (quoted in Sumner 1995, 1).

Between 1933 and the beginning of defense and war mobilization in 1940, the Roosevelt administration experimented with five main types of economic policy. The Supreme Court declared some of these actions unconstitutional. Some conflicted with others, for example, establishing cartels to fix prices and later strengthening antitrust action against price fixing. Roosevelt encouraged some advisers to advocate policies that others opposed so that he could gauge public reaction. He chose between them, tired of the policies when they did not work or were unpopular, and went to something different.

One group led by Agriculture Secretary Henry Wallace and two of Roosevelt’s campaign advisers, Rexford Tugwell and Raymond Moley, wanted national planning.6 In the administration’s first months, Congress passed the National Industrial Recovery Act (NIRA) and the Agricultural Adjustment Act. Both were declared unconstitutional within three years.7

A second group wanted reductions in government spending and a balanced budget. During the campaign Roosevelt had promised a balanced budget, except for emergency relief, in a campaign speech in Pittsburgh, and he had criticized Hoover repeatedly for running deficits. In the first one hundred days Congress passed the Economy Act, reducing government employees’ salaries by 15 percent and reducing veterans’ pensions. Balancing the budget remained an unrealized goal of the administration until the 1938 recession, when the goal changed. Prominent advocates of balanced budgets, as a means of restoring confidence, included many economists and businessmen. Within the administration, the leaders of this group were Henry Morgenthau, who followed William Woodin as secretary of the treasury, serving from late 1933 to 1946, and Lewis Douglas, the first budget director.

A third group took the opposite position. This group included Marriner Eccles, Lauchlin Currie, Harold Ickes, and Harry Hopkins. Eccles and Currie, separately, developed the idea of countercyclical fiscal policy that later became identified with Keynes’s General Theory8. Eccles, like Keynes, wanted not just spending but government investment to replace private investment during recessions. Roosevelt took this approach in 1938, but his change of view was partly, possibly mainly, a political decision about the 1938 election.

The fourth group wanted antitrust policy to break monopolies. Adolph Berle, an early adviser, was the leading proponent for many years, but he was supported in 1938 by the staff of the antitrust division of the Justice Department led by Thurman Arnold. As part of this policy, the Temporary National Economic Committee conducted a massive study of monopolies, trusts, and business practices beginning in 1938.

Fifth was the concerted effort to supplement NIRA codes of fair pricing by increasing the gold price and buying silver. These monetary operations to raise the price level are discussed more fully below.

Both the Democratic and Republican platforms, prepared for the 1932 campaign, called for an international conference to consider monetary questions. Both platforms mentioned silver explicitly, in deference to political pressures from western states. Both urged reform of bank supervision and action to prevent the use of credit for speculation (Krooss 1969, 4:2692–93). Both are short on specific recommendations.

The depression years were the beginning of the end of the international gold standard. Increasingly, domestic concerns dominated international concerns. Roosevelt had not committed to maintaining the gold standard during the campaign or after. He had not decided to devalue, either. In retrospect, July 1933 is the turning point, the time when the administration chose domestic recovery and an end to deflation over commitment to a fixed gold price. The Federal Reserve had sterilized gold flows in the past to achieve domestic objectives, but sterilization did not alter the commitment to a fixed exchange rate. Although the Roosevelt administration attempted to stabilize exchange rates by international agreement in 1936 and again in 1944, neither agreement required the Federal Reserve to subordinate domestic to international monetary objectives.

REOPENING THE BANKS

Most of the banks in the country had been closed before the national banking holiday in March 1933 as a defense against further bank runs. Federal Reserve staff had considered how to restore banking services. The administration, however, had no plan for reopening banks, and no program for what would come next. It had not planned whether the United States would leave the gold standard or reopen the reserve banks and pay out gold as necessary. On March 9 the Emergency Banking Act resolved the administrative issue by authorizing the secretary of the treasury and the state banking authorities to license banks. Implementing the program proved time consuming.9

The Federal Reserve had been indecisive and incompetent as the banking problem became a crisis. The Board now took a backseat.10 The Treasury and the new president made the policy decisions. Ogden Mills stayed on to assist the new secretary, William Woodin. The Board’s senior staff took a leading role in drafting proposals to reopen the banks in stages. It also drafted legislation that became the Emergency Banking Act, based on earlier work. George Harrison came to Washington on March 5 to work with Mills, Woodin, Senator Carter Glass, Congressman Henry Steagall, the acting comptroller, Francis Awalt, Adolph Berle, one of the Columbia professors advising Roosevelt, Treasury staff, and others. Later, Adolph Miller joined the group.

The group could not reach a conclusion. Some wanted to guarantee all bank deposits. Others wanted to print currency and pay it out to all depositors. Glass shifted from favoring an end to gold payments to a proposal that they pay gold on demand without regard to the statutory reserve. The proposal to issue currency is the only mention of a readily available Bagehotian solution to the currency drain. Harrison opposed the proposal as inflationary, and it did not get much consideration (Harrison Papers, Memo to the Files, file 2010.2, March 12, 1933).

The discussion went on most of Sunday without reaching a conclusion. Woodin appointed a small subset to work out a plan. On Monday, this smaller group proposed to guarantee bank deposits either up to 50 percent or on a sliding scale depending on the bank’s assets, but the administration, especially the president, opposed a guarantee.11 They agreed to open the strongest banks first but could not agree on how to open the weaker banks without renewing bank runs or offering guarantees.12 Finally Roosevelt decided to make all government bonds, $21 billion, convertible into currency on demand at par. Full conversion would have doubled the money stock, currency, and demand deposits. Mills and Harrison were aghast. Harrison regarded it as “completely destructive of government credit, such an inflation of the currency as to destroy the currency and offer no means of contraction” (ibid., 7).

The crisis got the Federal Reserve to do what it had failed to do earlier— relax its rules governing currency issues and credit expansion. To head off the president’s proposal, Mills and Harrison proposed that the administration reopen the sound banks, reorganize those that could survive and support many of them in exchange for preferred stock held by the Reconstruction Finance Corporation (RFC), and close the rest. The Federal Reserve (1) would lend to any member bank that opened based on its sound assets and weaken the links between gold and note issue by (2) issuing Federal Reserve bank notes backed only by portfolio assets (not gold), and (3) would broaden the definition of eligible paper backing the new notes to include direct obligations of individuals and firms that borrowed from Federal Reserve banks against government securities. The president accepted the proposal, and it became part of the Emergency Banking Act (Harrison Papers, file 2010.2, March 12, 1933).13

Federal Reserve banks reopened on March 10 and 11 to provide cash for payrolls and to lend on government securities. Harrison told his directors that the new law “greatly extends the powers of the Reserve banks, and adds to their responsibilities and the risks, which they may incur” (Minutes, New York Directors, March 9, 1933, 172). They could now lend more freely and greatly expand the note issue. Since the objective was to prevent reopened banks from failing, “the Federal Reserve banks become in effect guarantors of the deposits of reopened banks” (172).14

In his first “fireside chat” to the public on March 12, the president explained the plan for reopening banks. Licensed banks in Federal Reserve cities reopened on Monday, March 13. On Tuesday, licensed banks reopened in 250 cities with clearinghouses. Reopening continued for months. The Federal Reserve banks sent the Treasury lists of banks recommended for reopening, and the Treasury licensed those it approved.15 As late as October, bankers wrote to complain about the slow pace of re-openings (Board of Governors File, box 2185, October 2, 1933).

Approximately 4,000 banks did not reopen.16 This was nearly 40 percent of the banks that closed between June 1929 and June 1933. The Midwest was hit particularly hard, losing 2,500 of the 4,000 banks. The Cleveland Federal Reserve bank sent a telegram to the Board expressing concern about “many banking institutions the present condition of which precludes their reopening with governmental support... or otherwise” (telegram, Decamp to Meyer, Board of Governors File, box 2158, March 11, 1933). Other reserve banks wired concern about too few or too many banks being opened.

The president’s announcement had assured the public that only sound banks would be reopened. Recognizing that the public would not distinguish between member and nonmember banks, Congress allowed state nonmember banks to borrow from Federal Reserve banks on acceptable collateral. This power expired after one year.17

Many of the banks that did not immediately reopen had borrowed from the Federal Reserve. Nearly nine hundred unlicensed and closed banks owed $125 million, almost 30 percent of outstanding borrowing in early April. Chicago had the largest number of such banks, 13 percent of the total, but Philadelphia, New York, and Cleveland each held about 20 percent of the now illiquid loans (Board of Governors File, box 1297, April 8, 1933).

The April meeting of the Governors Conference considered the many problems encountered in reopening and licensing banks. A week after the meeting, a committee of governors drafted a statement reporting the unanimous opinion that “if any member bank which had been licensed to reopen, is permitted to fail, it will prove a serious shock to the confidence of the public, … and may well precipitate a banking crisis even more critical than the recent one” (Governors Conference, April 19, 1933, memo dated April 26, 1933).18 The governors accepted a share of the responsibility for avoiding failures, but they were concerned that their efforts would reduce the capital and surplus of the Federal Reserve banks if banks failed while in debt to the reserve banks. The governors’ subcommittee recommended that the Federal Reserve banks “adopt a liberal loan policy and be prepared to make loans on sound assets with little or no margin in cases where it is necessary to keep a bank open.” To reduce risk to the reserve banks, the subcommittee urged that the Reconstruction Finance Corporation take over loans after an agreed period (ibid., 2–3).19

The subcommittee also suggested an alternative. The Federal Reserve could lend to the RFC, and the RFC could lend to the banks. The RFC’s debentures carried a government guarantee, so the Federal Reserve would be protected against losses. The subcommittee wanted authorization to negotiate an agreement to this effect with the Treasury.

The remarkable feature of the memo is that, except for the guarantee, it recalls a proposal made by Secretary Mellon in 1931. At that time President Hoover and Secretary Mellon sought a nongovernment solution to prevent bank failures. Large banks were asked to underwrite a new intermediary, the National Credit Commission, that would buy up some of the assets of failing banks. The effort failed in part because the Federal Reserve refused to accept obligations of the proposed intermediary as eligible paper if the subscribing banks faced insolvency or illiquidity. If the earlier proposal had been implemented, many of the bank failures and the resulting financial crisis could have been avoided.

No less remarkable is that the subcommittee recommending the financial safety net had three members, George W. Norris, George Seay, and George L. Harrison, who had served throughout the decline. Norris was an especially strong proponent of real bills and an opponent of credit expansion by the Federal Reserve. It is hard to avoid the conclusion that the governors were not just chastened by their experience but were also fearful of the legislation that the new Congress and administration would support if they failed to cooperate with the recovery program.

The proclamations and orders closing and reopening banks also changed the role of gold in the monetary system. On March 6 banks were ordered not to pay out gold or gold certificates in connection with the few transactions authorized with foreigners during the bank holiday. After March 10, reopened banks or financial institutions could not pay out gold or gold certificates without authorization by the secretary of the treasury. The Board ordered the reserve banks to compile lists of all persons who purchased gold from the reserve banks after February 1 and had not rede-posited the gold in a bank before March 13 (later extended to March 27).

The administration had not formulated a gold policy. Among those whose advice the president sought, Professors Irving Fisher, George Warren, and John R. Commons were the main proponents of devaluation or abandoning the gold standard. Roosevelt made no decision at the time, so it was not known whether the restrictions on gold payments would remain or prove temporary (Barber 1996, 24–25).

The banking position was a decisive factor in the decision to leave the gold standard. On April 5, the president forbade domestic gold holding. All gold coin, certificates, and bullion were ordered sold to the Federal Reserve banks by May 1.20 On April 18 the president announced that the Treasury would cease issuing licenses to export gold (except to settle claims of foreign governments made before the moratorium).

The April 18 order took the country off the gold standard and ended any deflationary threat from adherence to gold standard rules. The president’s announcement did not explain what would happen next. The president was no less obscure the next day, when he explained that he wanted to raise commodity prices and get the world back on the gold standard. This was followed on June 5 by a joint resolution abrogating the gold clause in all public and private contracts. Payments could be made only in legal tender.

The gold drain did not require a ban on domestic gold holding or repudiation of the gold clauses in private and public contracts. The president’s April 18 decision would have stopped the gold outflow by making the dollar inconvertible into gold, a decision President Nixon made in 1971. This would have permanently removed the deflationary pressure that the embargo had ended temporarily. Banning private gold holdings and abrogating the gold clauses transferred the profit on the devaluation to the federal government. These steps seem unnecessary interventions into private contracts and asset decisions. Their purposes were mainly political, to show that bankers and wealthy individuals would not gain from the policy.

Since the United States held about one-third of the gold in all central banks, these moves puzzled Europeans and generated suspicion and distrust of United States policy in the negotiations leading up to the London economic summit scheduled to be held that summer. The suspicions remained when the administration later changed course and sought cooperation to stabilize the dollar exchange rate against the pound and the franc.

MONETARY AND OTHER LEGISLATION, 1933

The Hoover administration had done little to correct the perceived flaws in financial regulation. The Glass-Steagall Act granted authority to use government securities as collateral for the note issue as a temporary measure, later made permanent. Likewise the Reconstruction Finance Corporation started as a rescue operation for banks, insurance companies, and railroads, but initially loans had to have full collateral backing. The RFC had very limited resources. After Congress required release of the names of banks it helped, banks hesitated to ask the RFC for assistance. Mason (1994) notes that the RFC’s constructive role in reorganization began in 1933, when it gained the power to acquire preferred stock in weak or failing banks.

Congress held hearings on reform proposals during 1931 and 1932 without reaching agreement or passing legislation.21 The information collected proved useful, however. In 1933 the banking committees could proceed without new hearings. Their major problem was to avoid some of the more populist measures such as those calling for issuing greenbacks, coining silver, devaluing the dollar, and compensating depositors for part of their losses from bank failures.22 Some of these proposals had considerable public support and support in Congress.

The Thomas Amendment

The wholesale price index, as recorded at the time, reached a low of 59.6 (base 100 in 1926) in early February and again in March. By early April the index had increased only one point. This was far too slow for many farmers and ranchers, hence for their representatives. They wanted prices for crops and livestock increased in time for the harvest.

Senator Burton Wheeler (Montana) offered an amendment requiring the Treasury to coin silver in the ratio of sixteen to one to gold. When Roosevelt threatened to veto the bill, Senator Elmer Thomas (Oklahoma) offered a substitute amendment to the Agricultural Adjustment Act (AAA) that permitted the Federal Reserve to purchase up to $3 billion of securities directly from the Treasury upon authorization by the president; gave the president discretionary authority to issue $3 billion in currency (United States notes or greenbacks) if the Federal Reserve refused to make direct purchases of Treasury securities; and permitted the president to devalue the dollar against gold and silver up to 50 percent of its value.23 The amendment also permitted the Federal Reserve Board to raise or lower required reserve ratios by declaring an emergency, on a vote of five members and with the approval of the president, and it authorized silver purchases of up to $200 million (Krooss 1969, 4:2719–22).24

Roosevelt and his advisers did not agree about the amendment. Opponents believed it was inflationary and likely to raise concerns about the administration’s direction. Roosevelt saw the issue in political terms. The amendment authorized action but did not require it. If he opposed the Thomas amendment, Congress could pass mandatory legislation to inflate. The hesitation suggests that the administration had not decided whether to return to the gold standard at the old parity, devalue, or inflate. When Roosevelt announced on April 18 that he would accept the amendment, his budget director, Lewis Douglas (a gold standard advocate), is reported to have said, “This is the end of western civilization” (Kindleberger 1986, 200).

The Federal Reserve did not participate in discussions with the president about the Thomas amendment (Todd 1995, 26). Nor did it raise objections or point out that prices of most agricultural products were set in world markets, so that any benefit to farmers resulting from inflation would be temporary, reversed by devaluation of the dollar and a rise in the prices farmers paid.

Meyer did not approve of the administration’s direction and had limited contact with its officials. On May 10, he resigned. His replacement as governor was Eugene R. Black, governor of the Federal Reserve Bank of Atlanta since early 1928. Black had the shortest tenure as governor of the Board to date; he served only fifteen months before returning to the Atlanta bank. He died in December 1934, four months after his return.25 Roosevelt also appointed J. F. T. O’Connor as comptroller and, ex officio, a member of the Board.

The Banking Act of 1933

As a senior member of Congress, Carter Glass had his choice of the chairmanship of two Senate committees—Appropriations and Banking. If Glass chose Banking, Kenneth McKellar (Tennessee) would be chairman of Appropriations. McKellar was a machine politician and, for this and other reasons, unattractive to the incoming administration as chairman of a key committee. The president prevailed on Glass to take the Appropriations post but, de facto, he retained control of banking legislation (Hyman 1976, 162).26

The 1933 act was the first major revision of the Federal Reserve Act. Glass submitted his first bill in December 1930. Shortly after, he appointed H. Parker Willis as technical adviser to the committee.27 Willis had worked with Glass in 1913 and shared his views about the real bills doctrine, speculation, and decentralization. Hearings began in January 1931. Glass and Willis used the hearings to question Harrison, Case, Miller, and others about what had gone wrong, whether speculation and the power of the New York bank in dealings with foreign central banks had contributed to bank failures, deflation, and depression, and whether the Board should have more control of open market operations.28

A second attempt to write a bill, in 1932, strengthened the Board’s power over open market operations. All operations had to have the approval of the open market committee and the Board. The Board argued that that was too rigid.29

The 1933 act established a deposit insurance fund that became the Federal Deposit Insurance Corporation (FDIC), separated deposit and investment banking, restricted member banks from dealing in investment securities, and placed supervision of bank holding companies under the Board.30 The act also lengthened the terms of the six appointed Board members to twelve years, increased the Board’s power to remove bank officers or directors who violated banking laws, prohibited interest payments on demand deposits, and gave the Board power to set ceiling rates on time deposits.31

The Federal Open Market Committee, with all twelve banks as members, acquired legal status. Reserve banks could engage in open market operations only under Board regulations (Krooss (1969, 4:2725–69). To retain local directors’ authority, the act permitted a reserve bank to refuse to participate in an open market operation on thirty days’ notice to the Board and the committee (Kennedy 1973, 210). This was a step away from the idea of semiautonomous reserve banks, but it did not abandon local option.

Glass believed the New York bank and the secretary of the treasury had too much power. He blamed New York, particularly Strong, for the expansion of speculative credit after 1927. He was suspicious of the relation between the New York bank and the Bank of England and determined to prevent relations of this kind from affecting the growth of credit. The act reduced New York’s role in foreign transactions by shifting control to the Board. Glass also wanted to remove the treasury secretary from the Board, but the secretary objected strongly, and Glass did not prevail.

The act also eliminated the double liability of directors of national banks, specified in the National Banking Act.32 Despite much testimony arguing that reserve banks could not control the use of credit, Glass inserted a provision that the banks must keep informed about “whether undue use is being made of bank credit for the speculative carrying or trading in securities, real estate or commodities” (Krooss 1969, 4:2726). The intent was to limit discounting and prevent financial speculation. Since discounts remained low in the 1930s, the provision had no effect. Glass also included a provision making the System’s goal the accommodation of commerce, industry, and agriculture.

Writing at the time, Westerfield (1933, 727) reports that Glass believed the Federal Reserve had been dominated by the Treasury and had permitted securities speculation. The Board had been timid and vacillating. Power had shifted to New York. The Board, on its side, considered most of the legislation unnecessary. It wanted only an amendment clarifying its power of supervision over open market operations and relations with foreign banks (732).

Glass had larger plans. He wanted most of all to strengthen commercial lending by separating commercial and investment banking. Some bankers supported this change, among them Winthrop Aldrich, chairman of the Chase National Bank (Harrison Papers, Conversations, file 2500.1, March 8, 1933).33 He wanted banks to retain powers to underwrite only municipal, state, and federal government bonds. After the Pecora investigation of investment banking exposed the alleged misdeeds of banks’ investment affiliates, other bankers wrote to Roosevelt or Glass supporting separation (Kennedy 1973, 222–23).34

Section 20 of the Banking Act, known as the Glass-Steagall Act, gave banks one year to choose between commercial and investment banking, prohibited investment banks from taking deposits, and banned interlocking directorates for commercial and investment banks. Glass regarded this as the most important feature of the 1933 act. It took more than sixty years to reverse the mistake.

Henry Steagall (Alabama) had proposed some type of deposit insurance or guarantee for several years. The insurance provisions were his main contribution to the Banking Act.35 Public pressure to get partial recompense for banking losses helped to move the legislation toward passage.

Opposition to deposit insurance came from two sources. First, past attempts by states had produced mixed results, in part because of problems of moral hazard, in part because local banks were not diversified. Second, many small banks wanted insurance, but large banks believed they would be forced to pay most of the cost and thus subsidize small, weak banks. The history of failures before the depression supported this argument. Opponents favored liberalized branching to produce more diversified financial institutions (White 1997, 3).

The 1933 provision started as a proposal to deal with the liquidation of failed member banks. The Federal Advisory Council argued that the government should pay the liquidation costs for member banks just as the RFC paid for nonmember banks. The compromise proposal took $150 million from the RFC and half the surplus of the reserve banks on January 1, 1933—$138 million—to establish the Temporary Deposit Insurance Fund, which opened in January 1934 (Todd 1995, 28). Insurance was limited to $2,500 of deposits. Large bankers wanted any fund restricted to member banks, but the legislation admitted nonmembers if they undertook to join the System within two years. This provision was unpopular with small banks, and it was removed in the Banking Act of 1935.36 The latter act changed the fund’s name to the Federal Deposit Insurance Corporation (FDIC), made it a permanent agency, and raised maximum insurance to $5,000 (White 1997, 4–5). By 1980 the government insured deposits up to $100,000, the equivalent of $16,000 at 1934 prices.

The Federal Reserve’s failure to serve as lender of last resort, principally from 1931 to 1933, is the main reason for deposit insurance. Deposit insurance, however, is not a substitute for the lender of last resort; the insurance fund cannot protect against systemic or widespread failure. For that, the financial system required improvements in monetary policy that the 1930s legislation did not address. Without the many bank failures, the many depositors who lost money in failed banks, and others who feared such losses in the future, political pressure for deposit insurance most likely would have remained weak. Glass and Roosevelt would most likely have prevailed.

There is no record of the Federal Reserve’s opinion about deposit insurance, but there is some evidence in the minutes of the executive committee of the New York directors for April 10, which Secretary Woodin attended. The dominant view was opposition, but some directors accepted insurance for national banks. Harrison opposed the plan and criticized the proposal to use the Federal Reserve banks’ surplus to finance the insurance fund.37

Roosevelt had opposed guarantees and insurance in discussions about the bank holiday, and he did not quickly change his position. Glass opposed insurance, as he had earlier. The Senate bill provided only for a sinking fund limited to member banks. Change began after Senator Arthur Vandenberg (a Michigan Republican) offered a substitute amendment authorizing $2,500 of insurance. Most midwestern senators voted for the bill, urged on by thousands of telegrams and letters from citizens with deposits in failed banks.38 At its start, on January 1, 1934, 13,201 institutions joined the new system. Only 1 percent of state banks that applied did not qualify at the opening (Patrick 1993, 179–81).

Deposit insurance seemed a great success until the banking failures of the 1980s once again highlighted the problems of moral hazard and adverse selection that were recognized at the time of passage.39 Almost all banks have chosen to be insured, and insurance of savings and loans, credit unions, and stock market accounts followed. Most mutual savings banks stayed out of the federal system.

White (1997, 35) concludes that the FDIC did not reduce costs of bank failures from 1945 to 1994 and may have raised them. He places the cost of resolving bank failures in these years at $39 billion, with a present value of $7.8 billion. His estimates exclude the much larger costs of savings and loan failures in the 1980s and do not include the benefit of avoiding bank runs. Bank runs almost disappeared under the FDIC, in part because the FDIC absorbed part of the losses and encouraged mergers of failing banks into stronger banks. Instead of a run to currency, depositors in banks and savings and loans, with very few exceptions, held their insured deposits or moved them to another insured bank.

Although deposit insurance appears less successful now than before the 1980s, it retains broad public support. The failures of the 1980s convinced Congress that moral hazard was a real problem. Legislation strengthened capital requirements and required banks with less than minimum capital to close. After 1980, national and regional banking, proposed in the 1930s as an alternative to insurance, increased diversification of portfolios and the banks’ average size.

Contemporary beliefs that speculation had caused financial collapse, and Senator Glass’s powerful role in the Banking Act of 1933, greatly enhanced the Federal Reserve’s ability to respond to speculation. The new legislation included the power to fix the percentage of a bank’s capital and surplus invested in loans secured by stocks or bonds, restrict discount privileges by banks ordered to stop lending to customers using stock as collateral, warn banks not to lend to stock exchanges or loans from the Federal Reserve would come due immediately, and suspend a bank using its facilities for purposes not related to sound credit (“Power of the Federal Reserve System to Restrain Speculation in Stocks and Bonds,” Board of Governors File, box 1297, July 6, 1933). Most of these powers were rarely, if ever, used. Their presence after 1933 shows that Congress accepted Glass’s explanation of the financial collapse.40

Operations of the Reconstruction Finance Corporation

Nonmember banks that failed or required capital infusion to survive became the responsibility of the RFC. After the Emergency Banking Act authorized banks to issue preferred stock, the RFC assisted banks by buying their preferred stock or debentures. During its twenty-five years of operation, the RFC made 15,400 loans, totaling more than $2 billion, to more than 7,300 banks and trust companies. It ended operations in 1957 (Beckhart 1972, 273).

Beginning in June 1934, Congress authorized the RFC to lend to business enterprises. The same statute added section 13b to the Federal Reserve Act authorizing commercial and industrial loans in cooperation with financial institutions or on its own. The volume of such loans outstanding and authorized was never large. It varied between $35 million and $60 million. The number of applications ranged from eight thousand to ten thousand a year (Board of Governors of the Federal Reserve System (1943, 345). Discussion of section 13b loans absorbed a considerable amount of time at directors’ meetings.

OPEN MARKET POLICY IN 1933–34

The New York reserve bank closed with its gold reserve ratio about 25 percent, far below requirements. Although the Board had been unwilling to require Boston and Chicago to participate in open market operations, it now instructed five reserve banks to rediscount $245 million for New York at 3.5 percent. This was the first use of interdistrict lending since 1922 and the last use to date.41 New York repaid its borrowings in mid-April.

The monetary base and the money stock continued to fall in March and April as banks repaid discounts made during the emergency. The Federal Reserve was busy reopening banks and preparing legislative proposals, so the Open Market Policy Conference did not meet. Early in April, New York lowered its discount rate by 0.5 percent to 3 percent. Late in May, it reduced the rate again to 2.5 percent, where it remained until October. Other banks followed, but Richmond, Minneapolis, and Dallas kept their rates at 3.5 percent until February 1934.

The Open Market Policy Conference met on April 21 and 22 and voted to purchase up to $1 billion in securities over time “to meet Treasury requirements.” Harrison told his directors that the Governors Conference was not in favor of purchases, but referring to the Thomas bill, he was afraid of “undesirable legislation coming out of Congress” (Harrison Papers, Directors’ Meeting, April 27, 1933). The Board deferred action and made no purchases. This was Meyer’s last meeting. On May 12, with Meyer gone, the Board approved purchases of up to $1 billion. The amount was 60 percent of the portfolio held at the time.42

Governor Black first met with the executive committee on May 23. Under pressure from the administration, Black urged the members to purchase $100 million to $200 million. The OMPC favored $25 million. Before Black agreed to the lower amount, he obtained agreement that the committee would make heavy purchases if business activity and prices fell off. The committee agreed, subject to approval by a majority of the OMPC. Fears of a renewed decline did not materialize, but the purchases continued. In the next two months, the Federal Reserve purchased $200 million, at the rate of $20 million to $25 million per week.43

Most of the purchases were Treasury notes with up to five years maturity. Between May and December, note holdings increased by $700 million. The System sold shorter-term securities, mainly certificates (under one year), lengthening the portfolio’s maturity. The increased risk alarmed some of the governors, who pointed out that a rise in interest rates could wipe out the reserve banks’ capital.44

With the passage of the Banking Act of 1933, the Open Market Policy Conference became the Federal Open Market Committee (FOMC). At its first meeting on July 20, the FOMC chose an executive committee consisting of the same five members as before to carry out its instructions— Boston, New York, Philadelphia, Cleveland, and Chicago. Harrison remained as chairman. The committee voted unanimously to continue purchases and renewed the authority to purchase up to $1 billion.45

As excess reserves rose, some members of the FOMC became more reluctant to continue purchases. The System continued purchases, however, to avoid displeasing the administration and from fear of new legislation. On June 8, W. Randolph Burgess used Riefler-Burgess reasoning at the New York directors’ meeting to argue that there was not much reason, other than the psychological reaction, to continue purchases. On July 6 Harrison told his directors that Governor Black believed purchases should stop but that the president had said publicly that he wanted higher commodity prices, so this was a poor time to stop purchases. Oliver M. W. Sprague talked about the need to assist the Treasury in debt finance (Board Minutes, July 21, 1933, 1). On August 10 Harrison reported he had told Secretary Woodin that, with excess reserves at $500 million, the FOMC saw no reason for additional purchases. The Treasury responded that the president wanted purchases to continue.

Oliver Sprague was again present at the August 10 meeting. Sprague was working at the Treasury and served as an intermediary with the Federal Reserve. Asked to describe the administration’s monetary policy, Sprague replied that he could not because no particular policy had been adopted. Various policies had adherents in the administration. He warned that some wanted more radical approaches, so they hoped Federal Reserve policies would fail. Harrison complained again that it was difficult to know what to do, since he didn’t know what the administration’s policy was. One of his directors disagreed: the Federal Reserve, he said, should pursue its own correct policy.

The following week, Harrison reported that the president wanted purchases of up to $50 million. After an initial recovery, the economy was slowing down and commodity prices had fallen. The directors were reluctant to approve large purchases. They authorized only $25 million.46 A week later, Governor Black and Secretary Woodin came to New York. Black told the executive committee of the New York directors that purchases of $10 million or even $25 million a week would achieve little. He wanted purchases of $50 million a week. This was a relatively large rate of purchase, and Black would not say how long he thought it should continue. Much of the discussion at the meeting was not about the economy but about the risk of legislation to force inflation. The directors approved purchases of $50 million for that week with only one director voting against. Woodin urged that the vote be unanimous so he could tell that to the president; the recalcitrant director reluctantly changed his vote.

The president knew how to keep the Federal Reserve under his control. He agreed not to issue greenbacks during September, but he did not offer a longer-term commitment. The New York directors’ meeting of August 25 was reluctant to approve the $50 million rate of purchase agreed to by its executive committee. Owen Young of General Electric voiced the sentiment of many. He was opposed to directives from the government. If there was to be a policy of inflation, it should be a consistent policy, not one that changed every week.

Late in August, Governor John U. Calkins (San Francisco) wrote to Black suggesting larger purchases, up to $100 million a week. But he added that he did not expect them to be effective: “It is my view that the Federal Reserve System should do its full part [to encourage expansion], even at the risk of subsequently having to realize that its efforts were ineffective.” Black replied that he agreed “with the expressions in your letter” (Calkins to Black and Black to Calkins, Board of Governors File, box 1449, August 23 and 31, 1933).

The FOMC continued to authorize purchases in September and October. Member bank borrowing declined to about $125 million, and excess reserves rose to between $700 million and $800 million. By Federal Reserve standards, policy was easy and there was no reason for further purchases. Harrison’s memo for the September FOMC meeting referred to the volume of excess reserves as evidence of an easy money market position. The governors agreed that further purchases were unnecessary from a banking and credit perspective, but they feared an issue of greenbacks and for that reason wanted the Board to indicate that it favored further purchases. Governor Black gave that assurance, and the executive committee of the FOMC voted to maintain the $36 million per week rate of purchase for another week.47

Opposition to Purchases

Between the July and October meetings, the Federal Reserve purchased almost $300 million, bringing total purchases to $500 million of the $1 billion authorized in April. Prime commercial rates fell to 1.25 percent and acceptance rates to 0.25 percent, far below the discount rates at Federal Reserve banks.

Opposition to the purchase program increased. Disturbed by the decline in rates and loss of revenues and by the volume of government securities, the executive committee of the Chicago bank unanimously approved a resolution on September 29 calling for reduction in its share of open market purchases. Chicago continued to adhere to the real bills doctrine, citing not only the $700 million of excess reserves but the need to be in position to rediscount paper for commercial, agricultural, and industrial borrowers. Further, the directors saw “no need for further purchases” (Letter C. R. McKay to Eugene Black, Board of Governors File, box 1449, October 4, 1933). Since Chicago took the largest share of new purchases, its decision threatened the purchase program.48

The background memo for the October 10 meeting showed that “basic commodity prices” reached a peak in July, then fell back. By early October, the index was above April but substantially below mid-July. Governors Roy A. Young (Boston) and George W. Norris (Philadelphia) argued that market rates were so low that they deterred lending. Banks incurred costs with very little return. All the governors agreed that the credit and banking position gave no reason for purchases. The committee voted to continue purchases, however, to avoid political confrontation.

The minutes of the meeting give the governors’ view of how open market operations work and why they had not worked on this occasion. Open market operations force funds into the short-term market and, as short-term rates decline, into the longer-term markets. The focus is on interest rates, not on the broader interplay of relative prices of assets and output. Some governors reported that banks were reluctant to lend because of their recent experience and concerns about some (inflationary) provisions of the Securities Act and the Banking Act. Borrowers were reluctant to take on debt. The governors believed that the inflationary program deterred lending and investment. They favored an administration program to strengthen confidence. The latter is probably a reference to the budget deficit and the uncertainty surrounding the administration’s policy of buying gold to raise the price level and devalue the dollar (FOMC Minutes, Board of Governors File, box 1449, October 10, 1933).

Harrison described the committee’s position when presenting the recommendation to the Board. The committee found “little or no reason for further purchases.” A reduction in purchases should be made if it could be carried out without harming the recovery program (Board Minutes, October 12, 1933, 3–4).

Chicago’s directors voted to participate in 12 percent of the purchases, based on the allocation formula in effect before May 1933, instead of 36 percent under the new formula. This was a modest concession to the Board, since the directors had voted to participate only on the written request of the Federal Reserve Board (Letter McKay to Black, Board of Governors File, box 1449, October 16, 1933). The main reason for the concession was that the Banking Act of 1933 required a month’s notice by reserve banks withdrawing from the purchase program (Letter Young to the Board, Board of Governors File, box 1449, November 6, 1933).

Chicago was not the only recalcitrant bank. After the FOMC voted to reduce the rate of purchase to $18 million on October 25, Boston voted on November 1 not to participate in the purchase. It cited the Chicago decision, the large amount ($581 million) remaining from the $1 billion commitment, and uncertainty about what its share would be. The formal rules required prior notification. The bank was willing to consider purchases weekly (ibid., 2).

In October and November the System purchased $55 million, then purchases stopped. The committee did not meet again until March 1934, when it voted to reduce the authorization to purchase from $1 billion to $100 million. Between November 1933 and April 1937, the open market portfolio remained at about $2.43 billion. Changes represent expiring maturities not immediately replaced.

The System’s discussion of interest rates and credit conditions ignored the sustained upward movement of stock prices. During the spring and early summer of 1933, the Standard and Poor’s index of stock prices nearly doubled, rising from 45 in March to 85 in July. Thereafter the index declined slightly to the end of the year. By July 1933 the index of industrial production reached the highest level in three years, more than 50 percent above its trough; the Board’s index, available at the time, shows a larger increase, 70 percent above its trough, back to the level last experienced in May 1930. The index declined in the fall. By December much of the increase had reversed.

Just as in 1932, open market purchases stopped as the economy began to expand. Although the circumstances differed, the reasoning was much the same. Harrison explained the prevailing view in a memo to his files on November 20. Acting Treasury Secretary Henry Morgenthau wanted the reserve banks to purchase $25 million a week in advance of the December Treasury financing.49 All the governors opposed. Harrison told Morgenthau that “it would not only do no good, but it might do some harm; it would be only another factor of uncertainty, tending toward inflation” (Harrison Papers, November 20, 1933). According to Harrison, Morgenthau agreed.50

Federal Reserve officials appear to have learned nothing from the experience of 1929–33. They continued to operate in established ways and to interpret events as they had in the past. The principal reason for large-scale purchases was fear—fear of legislation or of action by the new administration. Balancing this fear was fear of inflation, a concern more closely related to the real bills doctrine than to the fact that the price level was 25 percent below its 1929 level.

In 1920–21, gold movements and a falling price level raised real balances and ended the recession despite high real interest rates. The pattern was very different in 1933. The economy recovered strongly beginning in the second quarter, as banks reopened and the financial crisis ended. The deflator rose at an 11 percent average annual rate for the last three quarters of the year, mainly the effect of NRA codes approved in July. Growth of the monetary base remained negative throughout the spring and early summer, and real balances fell. The ex post real interest rate was negative. In the fourth quarter output fell, and the risk premium in interest rates rose by 0.75 percent from the low reached in May.51

Unlike Hoover, Roosevelt did not intend to be the victim of Federal Reserve inaction. He began buying gold and silver to raise their prices and the general price level. Although Federal Reserve credit declined slightly in 1934 as discounts and acceptances fell to insignificant levels, gold and silver purchases increased the monetary base. The base and the money stock resumed their increase, and recovery also resumed.

GOLD AND SILVER POLICY, 1933–34

From the banking holiday to April 11, the gold price remained within 15 cents (0.7 percent) of its par value, $20.67 an ounce. There is no sign of anticipated devaluation in either the gold price or the forward market. The Treasury granted export licenses without hindrance. Gold returned to the Federal Reserve banks.52 These and other available data suggest that the markets regarded the suspension of convertibility as a temporary move. The relatively large United States gold holdings at the time gave no reason for permanent devaluation under “rules of the game.”

Sentiment began to change in April. Discussions leading to the Thomas amendment and pressure for inflation or reflation increased requests for licenses to export gold. In mid-April, gold outflows increased. The liberal gold export policy ended abruptly on April 18, when Secretary Woodin refused to issue new export licenses. The following day, the president prohibited gold exports except for gold previously earmarked, and hence owned, by foreign governments.53 The United States was no longer on the gold standard.54

Business and the public supported the decision. The stock market response was euphoric. The Dow Jones index of industrial stock prices rose 14 percent in the next two days and 55 percent in the next three months (Sumner 1995, 12). A daily index of the wholesale prices of seventeen commodities rose 76 percent, and the gold price rose to $30.18 in the next three months (Pearson, Myers, and Gans 1957, 5613).55 J. P. Morgan praised the decision as an end to the deflationary policy (quoted in Crabbe 1989, 436). Proponents of devaluation within the administration were delighted, as was the Committee for the Nation, a group of prominent citizens who favored reflation as a cure for depression (Pearson, Myers, and Gans 1957, 5610).56

Suspension of the gold standard was a decision to favor domestic over international considerations in the recovery. Most observers at the time presumed this was a temporary move, not a decision to float the dollar permanently. Roosevelt had not yet made a firm decision about either gold or the dollar.

Congress took a longer view. On June 5 the president signed legislation abrogating the gold clause in all contracts. The action redistributed wealth from creditors to debtors, including the government as a principal debtor. The clause applied to about $100 billion of public and private debt and to $1.6 billion of currency—gold certificates. Holders of mortgages, bonds, notes, and currency calling for payment in gold at 23.22 grains per dollar could not insist that their claims be enforced by the courts. Creditors challenged the action, but the Supreme Court upheld the government’s action five to four in February 1935 (Pearson, Myers, and Gans 1957, 5598).57

The London Monetary and Economic Conference

Events soon forced President Roosevelt to choose between stabilization and devaluation. An international conference at Lausanne, Switzerland, in July 1932 agreed to call another conference to consider international capital movements, currency stabilization, tariffs, and trade policy.58 London was chosen as the site and June 12 as the date. As the conference date approached, Roosevelt became active. Between April 22 and June 3, he met with ten prime ministers or presidents and cabled fifty-four others. His statements supported the aims of the London conference and an international solution, as pledged in the 1932 party platform (Pearson, Myers, and Gans 1957, 5617). In a fireside chat on May 7, he told the public that the conference “must succeed. The future of the world demands it” (quoted in Beckhart 1972, 306).

Roosevelt’s advisers were divided. George Warren was the leading advocate of devaluation within the administration. Outside, Irving Fisher favored devaluation based on his proposal for a compensated dollar and his belief that the rise in the real value of debt was a main obstacle to recovery. Both wanted the price level restored to the 1926 level.59 Morgenthau supported Warren’s views and used his charts comparing weekly changes in agricultural prices to changes in the world price of gold to convince Roosevelt. The president “was impressed” (Blum 1959, 64).

Conservatives within the administration opposed devaluation. Dean Acheson, later secretary of state in the Truman administration, was undersecretary of the treasury under Woodin. Woodin appointed Oliver Sprague of Harvard as his adviser on international economic policy. Sprague held traditional views; he favored deflation to reduce the price level as required under gold standard rules. Government could help by reducing “sticky” prices—wages, freight rates, and telephone charges.60

Secretary of State Cordell Hull headed the delegation to the London Monetary and Economic Conference. Hull’s concern was multilateral tariff reduction, and he does not seem to have taken much interest in monetary or financial issues. Drafting the United States position on these issues was left to Sprague and James Warburg, who favored a return to a gold standard after a 15 to 25 percent devaluation of the dollar. This plan was unacceptable to the British and the French (Kindleberger 1986, 205–6).61

Harrison was the principal Federal Reserve official involved in the discussions. In May he talked to Montagu Norman about a French proposal to stabilize the dollar, franc, and pound. Norman suggested that the franc and the dollar could remain at their current values but said the pound was likely to depreciate. He proposed that France and the United States accumulate sterling balances in London, to be paid in gold when the stabilization agreement ended. He doubted that the plan would work or would be helpful to Britain, but he promised to send a member of his staff to Paris to discuss the proposal (Harrison Papers, Memo, file 3115.4, May 18, 1933).

Four days later, Norman told Harrison that the Bank of England and the Bank of France had agreed on a joint reply to the United States. They favored a return to gold. In an indirect reference to uncertainty about United States monetary policy, he urged that the three governments “should make each other aware as to what policy they intended to follow in monetary matters” before agreement could be reached (Harrison Papers, Memo, Crane to Files, file 3115.4, May 22, 1933, 1). Norman insisted there was no point discussing Warburg’s proposal or any other technical details until the three countries agreed on a policy.62

The problem for the United States delegation was that Roosevelt had not yet decided what to do. Devaluation and rising prices were politically popular. By June 2 the Board’s weekly wholesale price index was five points higher (8.5 percent) than when the administration took office. The weekly price memo referred to “substantial increases” in several prices and no large declines.63 Wallace, Tugwell, and the planners claimed credit for the price increases, as did the proponents of devaluation. Under the Agricultural Adjustment Act, approved on May 12, the Agriculture Department paid farmers to reduce supply by plowing under cotton and wheat and slaughtering pigs. Slaughtering little pigs proved politically unpopular, strengthening the proponents of devaluation as a means of raising prices (Pearson, Myers, and Gans 1957, 5623).

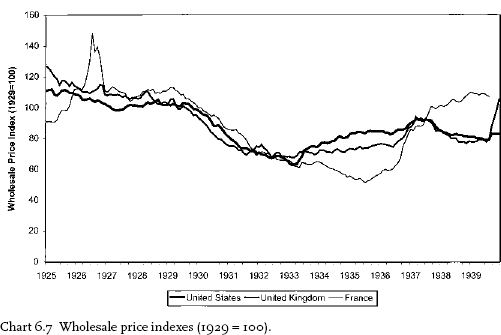

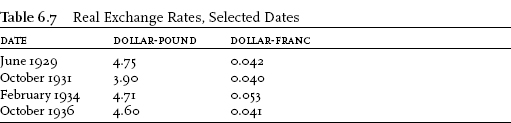

Roosevelt is often accused of scuttling the London conference and ending monetary cooperation working toward currency stabilization (Kindleberger 1986, 220–21; Beckhart 1972, 306). The truth to this charge is that Roosevelt’s message to the conference, on July 3, rejected an agreement to return to an international gold standard. The agreement specified neither the time nor the parity at which countries would rejoin because the conference could not agree on exchange rates. Chart 6.1 suggests the principal difficulty—the depreciation of the real dollar exchange rates for the pound and the French franc in 1933. France and Britain would not accept the 1933 rate; Roosevelt would not restore the earlier nominal rate and accept the implied deflation that would follow.64

In April, after floating the dollar, Roosevelt had offered to stabilize at a 15 percent devaluation against gold provided Britain and France would agree to a stabilization fund to keep exchange rates at the proposed levels. They refused. The British and French had been favorable to stabilization in the winter of 1933, before devaluation of the dollar brought the franc to a peak and the pound back to its traditional range, $4.86 per pound. By the time of the conference, the principal concern for Britain and France was that the dollar would continue to depreciate against the pound and the franc.

Harrison’s notes record the jockeying for relative advantage of the British, French, and United States delegations to a conference called from June 9 to June 16 at the Bank of England to resolve trilateral issues outside the main London conference. James Warburg, representing the State Department, Oliver Sprague, representing the Treasury, and Harrison were members of the United States delegation. All three favored a return to the gold standard, and two of them resigned later in the year when Roosevelt forced further dollar devaluation. This agreement aside, the United States delegation did not have a common viewpoint. Harrison favored “de facto stabilization as soon as possible” but does not mention an exchange rate (Harrison Papers, Diary of Trip to London, file 3010.2, June 1933, 1). He reports Sprague as not favoring any definite arrangement until exchange rates stabilized, perhaps in three months, but willing to consider an interim agreement. Warburg worried about the domestic political consequences of stabilization, almost certainly a reference to congressional and agricultural interests and perhaps to Warren and Morgenthau also. By June 10 Warburg had changed his mind, at least to the extent of tactically favoring stabilization. He cabled the president that he would support gold exports to make stabilization effective, but he did not expect the British to agree. The onus for failure would then be on them (ibid., 2).

Norman refused to negotiate any agreements until Treasury and government officials agreed on the policies of the respective governments.65 The governments agreed on the desirability of fixed exchange rates, but they could not agree on a policy. The French wanted a permanent agreement, based on gold. They considered an interim agreement useless or worse. Speculators would bet on the next step. Sprague said that “a permanent stabilization commitment was now entirely out of the question so far as the United States is concerned” (ibid., 3). The question to be considered was whether there should be a temporary agreement. He offered to forgo use of the Thomas amendment during the period of the agreement if the United States recovery continued. He favored stabilization but argued that it was impossible as long as unstable economic conditions persisted. Norman agreed with Sprague, but he viewed the pound as the weak currency. The United States and France had large stocks of gold; Britain did not: “He foresaw great difficulties and many quarrels” in a tripartite agreement (ibid., 7).

At the central bankers’ meeting, Norman suggested an interim program under which the pound and dollar would be fixed to gold with settlement in gold. The commitment would be limited to the specific amount of gold committed. If a country paid out its entire commitment, a new agreement could be reached at adjusted gold parities. This process could continue until the countries reached stable parities.66 Émile Moret preferred this plan to Harrison’s proposal to stabilize exchange rates, because the franc remained convertible into gold and the Bank of France was not allowed to buy foreign exchange. Harrison was skeptical because Washington favored stabilizing exchange rates, not the gold price. He considered daily or weekly announcements of gold movements a source of instability, so he wanted to avoid them. Exchange rate stabilization with gold settlement would show only net movements over a period. Further, he explained, the United States Treasury was unwilling to promise not to devalue after the London conference ended.

Moret rejected Harrison’s proposal. Central banks could stabilize exchange rates without an agreement. What was needed was a statement about monetary policy, current and future. Announcing and maintaining a gold price would provide the information.

On June 15 the central bankers’ meeting reached a modest, partial agreement to fix the dollar-pound rate within a 3 percent (12 cent) band around $4 per pound for a two-week period. The British government reserved the right to change the rate after two weeks, and the United States reserved the right to reject any British devaluation. Otherwise the contract would remain in force. The French would continue pegging to gold at a rate that equaled $0.04662 per franc. The United States promised not to invoke the Thomas amendment.

Financial markets greeted the announcements as a halt to reflation and recovery. Stock and commodity prices began to fall on June 12 as rumors of an agreement spread. Between June 12 and June 17 commodity and stock prices fell 3.5 and 8 percent, and the dollar appreciated against gold. Burgess told Harrison that even temporary stabilization was unacceptable. The delegation to the main London conference announced that “measures of temporary stabilization now would be untimely” (State Department files, quoted in Eichengreen 1992, 333). Roosevelt went on a sailing trip. The dollar fell, and commodity and stock prices resumed their rise.

That seemed to put an end to the main business of the London conference, but the conference continued. Roosevelt seems not yet to have made a final decision. Instead he sent one of his principal advisers, Raymond Moley, to London with instructions calling for a return to “stability in the international monetary field ... as quickly as practicable,” with gold “reestablished as the international measure of exchange values” (Moley 1939, app. F). Gold would not circulate but would be held by central banks or governments. Currencies would be subject to a uniform minimum gold reserve ratio. Silver could substitute partially for gold as a central bank reserve.

Based on these instructions, Moley negotiated a new agreement with Britain and France to limit speculation and restore the gold standard, but the agreement did not specify either the date or the gold price at which countries would return to gold. This was left to the future.

The June experience helped to convince Roosevelt about the difficulty of reaching a meaningful agreement. The market response to the June 15 agreement seemed to confirm Warren’s view that stabilization would bring back deflation. Morgenthau, who joined the president on his vacation, reinforced the latter view by showing Roosevelt Warren’s charts of weekly changes in gold and commodity prices.67

On July 3 Roosevelt reversed direction, threw out the instructions given to Moley, and rejected Moley’s agreement. In a strongly worded message to the conference favoring domestic over international action, the president said:

The world will not long be lulled by a specious fallacy of achieving a temporary and probably an artificial stability in foreign exchange on the part of a few countries only. The sound internal economic system of a nation is a greater factor in its well-being than the price of its currency in terms of the currencies of other nations… . Our broad purpose is permanent stabilization of every nation’s currency. Gold or gold and silver can well continue to be a metallic reserve behind currencies, but this is not the time to dissipate gold reserves. When the world works out concerted policies in the majority of nations to produce balanced budgets and living within their means, then we can properly discuss a better distribution of the world’s gold and silver supply to act as a reserve base of national currencies. (Quoted in Crabbe 1989, 437–38)

Roosevelt had at last made up his mind to emphasize domestic over international considerations as many in Congress wanted. Reflation of the domestic commodity price level became a key element in a policy of domestic recovery.

The world, Roosevelt said, faced catastrophe if the conference limited its concerns to exchange rate stabilization. There was no visible prospect of successful international cooperation to restore prosperity. The British hesitated to enter more than a temporary agreement that gave them a temporary advantage. The Harrison diaries make clear that agreement with the French was possible only on their terms. By law France could not engage in expansive open market operations. By choice they would not do so, because French officials continued to believe that the only proper solution was for each country to force its prices down to the level implied by its gold holdings. If this policy forced deflation on other countries, they must restrict money growth and deflate also. Harrison, Black, Miller, and others at the Federal Reserve, and Acheson, Warburg, and Sprague at the Treasury, favored a gold standard policy for the United States. The Federal Reserve made open market purchases at the time, but mainly out of fear of the administration and congressional “inflationists.” A commitment to restore the gold standard would soon end these purchases and restore deflationary policy.

By rejecting the London agreement, Roosevelt freed policy from the gold standard and kept the Federal Reserve in the backseat. He had moved, hesitantly, toward the policy of reflation advocated by Warren, Fisher, and Morgenthau. He did not decide to forever abandon the gold standard, as Fisher and Warren proposed. Long-term commitments had no special attraction and surely were not his concern at the time. The decision was to raise agricultural and commodity prices, to experiment, and to see where the experiment led.

Roosevelt’s decision to choose domestic expansion over stabilization of the gold price was correct in the circumstances. Starting from the low levels of 1933, the income effect of domestic United States expansion would more than offset any effect on foreigners of a United States devaluation. Further, a return to the gold standard would have brought back deflation in those countries that lost gold. Even if the technicians could have adjusted exchange rates appropriately—an unlikely event—fixed exchange rates would again be misaligned as countries moved toward full employment at different rates and with different price changes. The London meetings show that policymakers could not agree on exchange rate changes. They were unlikely to pay the costs of maintaining fixed rates during the long period of adjustment that lay ahead.

Unilateral Action

Markets greeted Roosevelt’s “bombshell,” as it is often called, enthusiastically. They anticipated reflation, rising output, and a vigorous policy of domestic expansion. On July 3 the daily indexes of commodity and stock prices rose 2 and 3 percent respectively, and the dollar depreciated against the pound. The daily price indexes continued to rise until July 18, when the NIRA announced its first codes. The following day, the Dow Jones industrial average fell almost 5 percent. The cumulative decline in the next few days reached 18 percent for stocks and 10 percent for Moody’s daily index of commodity prices. The dollar appreciated.

The president did not want the dollar to go above $4.86 per pound, the nominal rate prevailing before the 1931 British devaluation. On July 11 he asked the Federal Reserve to earmark $20 million in gold for the Bank of England, to be released two weeks later. Harrison explained to Norman that the intervention was intended to slow the dollar’s appreciation; it was not an attempt to fix the dollar at the old rate. As chart 6.1 above suggests, the dollar had appreciated strongly in real terms since April; it reached a peak in July, then declined (Board Minutes, July 13, 1933, 1–3; Harrison Papers, file 2210.3, July, 14, 1933).68

A week after his July 3 message to London, Roosevelt asked Morgenthau to invite Warren, Fisher, and Professor James Rogers of Yale for tea. Warren and Fisher met with Roosevelt at his home in Hyde Park, New York, on August 8. Roosevelt asked whether he should increase the price of gold to $29 an ounce. Warren urged at least $32 to $37. He showed Roosevelt charts showing the recent increases in prices of commodities, stocks, and gold and the level of employment (Pearson, Myers, and Gans 1957, 5626–27). Fisher, of course, agreed with Warren that buying gold would raise the price level (Barber 1996, 47, paraphrasing a letter from Fisher to his wife). Roosevelt was convinced and apparently pleased. He called a news conference the next day to show the press some of Warren’s charts.