“IT IS POLITICS that follows economics and not vice versa,” Gorbachev told the Lithuanian Communist Party in January 1990 during an abortive bid to keep the nation from leaving the Soviet Union.1 Evidently, the general secretary retained the foundational causal precept of Marxism, even as he jettisoned innumerable legacies of Marxism-Leninism. There was no way the Lithuanians would leave the union, he thought. It made no economic sense. The tiny Baltic state imported most of its energy from the rest of the Soviet Union, and all its economic links ran through Moscow. Nationalist pride might momentarily surge, but eventually politics would follow economics.2

It did not take long for the Lithuanians to prove him wrong. When they declared their independence three months later, they did so for a range of historical, ethnic, and nationalist reasons that belied pure economic motivation. They took only a moment’s pause when Gorbachev changed their economic calculus by imposing an oil and gas embargo in April 1990, and they persevered through violent intimidation in 1991 to achieve the independence forcibly denied them ever since the Red Army beat back Hitler’s eastward march and reoccupied the Baltic states in 1944.

Lithuania’s drive to independence is only the most proximate of countless episodes in the historical record that make a mockery of the breezy simplicity of Gorbachev’s dictum. There is, of course, no universal and ironclad relationship between economic causes and political effects, so it is incumbent upon anyone who would propose a relationship between a particular set of economic causes and a particular set of political effects to justify the reasons for doing so and specify the exact nature of the causal relation.

This book has been one such attempt at justification and specificity. It has argued that the economic forces unleashed by the 1973 oil crisis ultimately brought the Cold War to a peaceful end and gave rise to the neoliberal global economy of the late twentieth century. Those economic forces—oil, finance, and economic discipline—exerted such a profound effect because they fundamentally altered the nature of the competition between democratic capitalism and state socialism. The Cold War began as a competition between democratic capitalist and state socialist governments to harness the forces of industrial modernity to improve the economic security and well-being of their people. The two sides raced to make promises to their people and expand the social contracts that prevailed in their societies.

The economic crises of the 1970s made this politics of making promises untenable. The oil crisis of 1973 produced both the pressure to break promises and the means of avoiding that pressure. Over the long term, the industrialized economies of both East and West had to learn to produce more economic output with fewer inputs, a wrenching process of breaking promises whose true magnitude remains hidden behind the economist’s prosaic phrase “intensive growth.” But in the short term, they could avoid this challenge by seeking refuge in the global economy’s two new vast pools of wealth—global capital markets and energy resources—which vastly expanded in value after the oil crisis. As long as nation-states maintained access to either capital markets or energy resources, they could continue making promises at home and fighting the Cold War abroad. If, however, they lost access to one or both, they would have to turn to the politics of breaking promises and implement policies of economic discipline at home.

As we have seen, these moments of economic discipline abounded in the last two decades of the Cold War and ultimately decided its outcome. Though the Cold War began as a race to make promises, it ended as a race to break promises, and democratic capitalism prevailed over state socialism because it proved capable of breaking promises and imposing discipline. Neoliberalism rose as the Cold War ended because it provided ideological justification for acts of breaking promises; it made a virtue out of economic discipline. Combined with electoral democracy, it gave democratic capitalist states a political and ideological tool kit to meet the challenge of breaking promises. Lacking these tools, the states of the Eastern Bloc democratized their political systems and reformed their ideology in the 1980s as a means of imposing economic discipline. It is this process of political change and ideological reform that we now call the collapse of communism and the end of the Cold War.

Historians have traditionally identified a series of people and forces as the principle causes of the end of the Cold War: Gorbachev’s launch of glasnost and perestroika, his bold superpower diplomacy with Ronald Reagan and George H. W. Bush, the “people power” of Eastern Europeans in the streets, and the lucky confluence of a series of contingent events, like the opening of the Berlin Wall, that no one foresaw or intended. The account offered in this book does not deny the importance of any of these traditional markers of the end of the Cold War. Instead, it places these markers in a new light—one that was not ignited in the present and shone back onto the past, but rather one that once burned bright in the past and grew dim over time.

It was not the present study, after all, that first identified the connection between the oil crisis, Eastern Bloc sovereign debt, and policies of economic discipline. It was instead the East German Central Committee that obsessed over this connection on November 9, 1989, just hours before the Berlin Wall opened. “In 1973 there was a very large worldwide price explosion,” financial expert Günter Ehrensperger told his comrades on that fateful day. “Because of this price explosion, the procurement of oil and other raw materials for the GDR [German Democratic Republic] became much more expensive.” Rather than adjust the domestic economy to meet this new reality, Ehrensperger said, the GDR had delayed its fate by borrowing money from the capitalist world. “If you want to characterize in one sentence why we are in this situation today,” he said in reference to the debt, “then you have to say objectively that since at least 1973 we have fooled ourselves and lived beyond our means year after year. Debts were paid with new debts.” Economic discipline was the only logical response. “If we want to get out of this situation,” Ehrensperger concluded, “we have to work hard and consume less than we produce for at least 15 years.”3 Far from drawing connections that contemporaries in the Cold War did not see, this book has merely elaborated on the dynamics that concerned the highest levels of the East German leadership on the day the foundation of their regime came crashing down.

Nor was it an interpretive invention of this book to describe the dilemmas of Soviet imperial governance and the sources of Soviet imperial collapse in primarily economic terms. It was, instead, Mikhail Gorbachev, who, when discussing the fate of Poland in the 1970s and 1980s, rhetorically asked the Politburo in March 1988, “What was it all based on? On credits from the West and on our cheap fuel. The same goes for Hungary. . . . We cannot remain a provider of cheap resources for them forever.”4 And it was Yuli Kvitsinskii, the Soviet expert on Germany, who confided to a colleague in November 1990 that “the Deutschmark decided everything” about the process of German unification and the precipitous Soviet retreat that followed.5 This book has been unable to match Gorbachev’s and Kvitsinskii’s parsimony, but it has taken inspiration from, rather than imputed motivations to, their descriptions of the reasons for the Soviet imperial collapse.

Even this book’s two most adventurous claims—that electoral democracy made governments in the West more adept at breaking promises than the authoritarian governments of the East and that the economic problems and solutions of the West and East were fundamentally similar—are not retrospective insights of the present imposed on the past but rather past observations brought forth into the present. It was a tired and defeated Mieczysław Rakowski who first noticed, in the fall of 1989, the decisive role that democratic legitimacy played in the imposition of economic discipline in Poland. As he watched Solidarity’s prime minister, Tadeusz Mazowiecki, take his first steps toward shock therapy, he committed to his diary that “in principle . . . he says the same thing that I do.” But, he lamented, if “any PZPR [Polish communist party] government implemented the policies that the Mazowiecki government does, we’d already have a civil war. Our society patiently bears constant price increases and hyperinflation because this is ‘our government.’”6 The present study has expanded the scope of Rakowski’s observation across time and beyond Poland, but it has merely followed him in arguing for the importance of democratic legitimacy to processes of breaking promises.

Similarly, though it sounds bold in retrospect to declare a fundamental similarity between the quintessential project of neoliberal reform, Thatcherism, and the seminal project of socialist renewal, perestroika, we have seen that such a conclusion was commonplace at the time. Whether it was Rakowski in Poland, Károly Grósz in Hungary, or Gorbachev in the Soviet Union, the sense among socialist reformers that they shared many of the Iron Lady’s ends and envied the effectiveness of her means lurked as an uncomfortable tenet in their thinking.

The reader can be sure, then, as this book comes to a close, that it is not so much a work of historical revision as it is a work of historical recovery. The people to whom its story would have made the most intuitive sense—indeed, the people who likely would have found this entire narrative unsurprising—were the communist leaders themselves. They knew how important subsidized Soviet oil and Western finance were to the viability of their nation-states; they understood both the economic necessity and political impossibility of revising their social contracts; and they fully believed that their governing challenge was analogous to, rather than distinct from, the one faced by the industrial nation-states of the West. But they were also the Cold War’s losers, and thus it is hardly surprising that their perspective received short shrift after the Cold War’s end. This book looks to them, the communists who lost, to justify its focus on the connection between a particular set of economic causes—oil, finance, and economic discipline—and a particular set of political effects—the collapse of communism, the end of the Cold War, and the rise of neoliberalism. To title this causal process the triumph of broken promises is, in this way, to tell its history from the losers’ point of view.

If that serves to explain the book’s subject, what then of its specific findings? How exactly does conceptualizing the end of the Cold War as a race to break promises explain its discrete events? How exactly does the race to break promises explain the broad global shift in governing ideologies in the late twentieth century that constitutes the rise of neoliberalism?

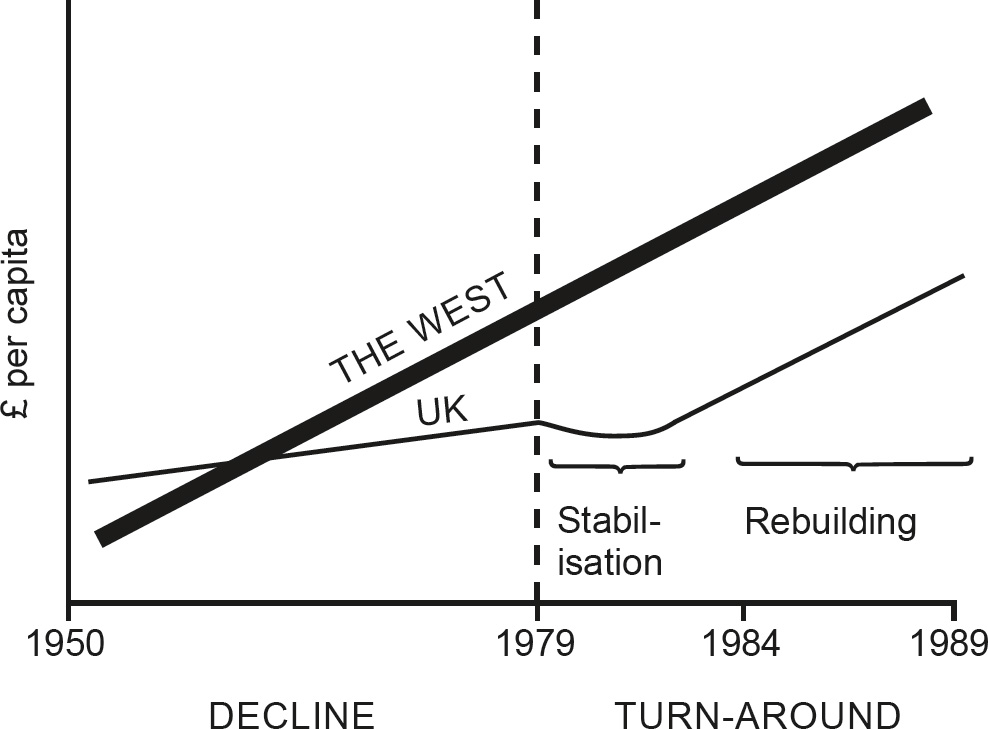

Here, again, we need not conceive of an answer in the present and project it onto the past. The past already holds the answer, and we need only bring it forward. Recall Margaret Thatcher’s chief strategist, John Hoskyns. On June 12, 1979, one month after Thatcher became prime minister, he laid out the coming challenge of transforming Britain’s economy in an internal memo. In this document, we can see the origins, challenges, and consequences of the politics of breaking promises. “We can represent the whole process as follows,” he wrote, before taping a graph to the memo (Figure C.1).

Figure c.1 John Hoskyns’s vision of the politics of breaking promises.

Reformatted from John Hoskyns, “Government Strategy,” June 12, 1979, PREM 19/24 f11, Margaret Thatcher Foundation, Thatcher MSS (digital collection), accessed December 14, 2017, https://www.margaretthatcher.org/document/115016.

What, exactly, do we have here? We have a country in stagnant decline relative to “the West,” which is itself defined as a relentlessly upward sloping line of increasing individual wealth and well-being that proceeds without setback infinitely into the future. To reverse its fall behind the West, this country’s government must confront a seeming paradox and explain it to its people: as a means of reversing its decline vis-à-vis “the West,” the government must first implement a period of “stabilisation” in which living standards would decline and the country would fall further behind the West for years on end. “Stabilisation is the difficult bit,” Hoskyns wrote, unknowingly summarizing the entirety of this book in one short sentence. “There is likely to be a noticeable J-curve effect over the first 2 or 3 years, when economic deterioration, as judged by the traditional indicators—growth, unemployment, inflation—will all look worse than they did in 1978/9.” This would make the politics of implementing stabilization treacherous, but if the country wanted to remain a significant force in the world, it could not be avoided. “The alternative,” he concluded, “is to continue to drop slowly out of the Western world in political, social, and military terms.”7

This was the politics of breaking promises in a single graph, and now that we have reached the end of this study, we can see that its dynamics were hardly confined to Thatcherite Britain. We need only change the years along Hoskyns’s x-axis, the currency along his y-axis, and the country of his concern to describe the central dilemmas of many governments in the late Cold War. This was the situation Paul Volcker faced when he put millions of Americans out of work and caused thousands of bankruptcies in a bid to revive the US economy and renew the United States’ preeminent position in the world. This was the situation Edward Gierek faced in 1980 when his attempted price increases spurred the formation of Solidarity. And this was the situation Polish and Hungarian leaders faced in 1987 and 1988 when they decided to liberalize their political systems as a means of gaining their societies’ acceptance of austerity.

Most of all, this was the situation Mikhail Gorbachev faced when he walked into the Kremlin on March 11, 1985, as the new general secretary of the Communist Party of the Soviet Union. What was perestroika if not an economic reform program that aimed to reverse the Soviet Union’s relative decline vis-à-vis “the West” in order to avoid the alternative of continuing “to drop slowly out of [or, in Gorbachev’s case, behind] the Western world in political, social, and military terms”? Gorbachev did not need to attempt reform in the Soviet Union. As many historians have stressed, the country could have gone on for many years persisting in stagnation. But once he did initiate reforms, Gorbachev’s ultimate failure—and the source of the Soviet Union’s economic and geopolitical collapse—lay precisely in the fact that he was never willing to tolerate a J curve in the Soviet Union’s fortunes. First for reasons of ideology and domestic politics, he was unable to carry out the politics of breaking promises at home and instead lost control of the Soviet economy. Then, by 1990, when he recognized that a substantial J curve was unavoidable, he surrendered the Soviet Union’s military position on German soil to save hard currency, gain access to Western capital, and soften the domestic blow of the J curve to come.

Indeed, in Gorbachev’s story, we can see that the pressure to break promises drove political and ideological change in the late Cold War in two distinct ways. First, a series of political and diplomatic events that were vital developments in the end of the Cold War were by-products of communist leaders’ desire to lessen the severity of breaking promises at home or avoid breaking promises altogether.

The changes in Soviet foreign policy that contributed to the end of the Cold War should be understood in these terms. The Kremlin’s desire after the oil crisis to lessen the material burden of its empire and its growing desire to lessen the burden of the arms race were both born of this inclination and reached their zenith under Gorbachev. His bold nuclear arms diplomacy and repeal of the Brezhnev Doctrine in 1986, his willingness to accept the highly asymmetric Intermediate-Range Nuclear Forces (INF) Treaty in 1987, his announcement of a unilateral withdrawal of Soviet forces from Eastern Europe at the United Nations in 1988, his acceptance of noncommunist governments in Eastern Europe in 1989, and his agreement to German unification on Western terms in 1990 were all attempts to cut back Soviet guns (and subsidized energy deliveries) to give the Soviet people more butter. Gorbachev thought that if he could free the Soviet Union from the burden of arms and allies, perhaps he would not have to break promises to his people. His success in breaking free from these burdens was at best partial (as one would expect in the face of the formidable entrenched interests confronting him), but it was the desire to break free of the material burden of arms and allies that motivated the signature developments in Soviet foreign policy on the road to the end of the Cold War.

The political side effects of efforts to avoid broken promises were hardly confined to the Kremlin. The desire to avoid or lessen economic discipline also contributed, in fundamental ways, to the shape of events in Eastern Europe. Most fundamentally, of course, Eastern European leaders’ steadfast determination to avoid breaking promises was the original source of the bloc’s financial dependence on Western governments and global capital markets after the 1973 oil crisis. We have seen how this dependence produced specific and decisive political changes during the Cold War’s endgame. It was Wojciech Jaruzelski’s desire to regain access to hard currency that contributed to his decision to declare a general amnesty and set Solidarity’s leadership free in September 1986. It was Miklós Németh’s desire in late 1988 to find cuts in the Hungarian budget that would not harm living standards that drove him to order the removal of the “Iron Curtain” fence separating Hungary from Austria. It was Egon Krenz’s desire to avoid domestic austerity that contributed to his reluctance to use violence against the East German people and drove his attempt to exchange the opening of the Berlin Wall for West German hard currency. And it was Gorbachev’s desire to lessen the hardship of the Soviet Union’s coming transition to a market economy that drove him to accede to German unification on Western terms and ask for billions of dollars and deutsche marks in return. Thus, out of a fear of implementing Hoskyns’s J curve or a desire to lessen the dip of the J, communist leaders of the Eastern Bloc slowly relinquished their coercive hold on the populations of Eastern Europe and, bit by bit, set the stage for the stunning events of 1989 and 1990.

Second, if attempts to avoid the politics of breaking promises drove important political and diplomatic change in the late Cold War, attempts to confront the politics of breaking promises drove political and ideological change of an even greater magnitude. Confronting the challenge of breaking promises meant actually revising the postwar social contract, and such revisions needed to be justified in ideological terms to domestic political constituencies. Breaking promises therefore required ideological and domestic political change. As Hoskyns wrote to Thatcher, “We are dealing with social systems, not mechanical ones. . . . Government therefore has to persuade people to think and feel differently, before the behavior of the system can change.”8 Gorbachev would have agreed with that sentence verbatim (with perhaps, in his early years as general secretary, the single change of “government” to “the party”), and he expressed much the same sentiment in regard to perestroika on numerous occasions. Paul Volcker also would have agreed that Hoskyns’s sentiment precisely described the nature of his quest to use monetarism to defeat Americans’ inflationary expectations, and Ronald Reagan would have concurred that it summarized quite nicely the goals of his bid to revive American economic growth through supply-side economics and launch a revolution in Americans’ views of the role of government. Finally, Wojciech Jaruzelski would have agreed that “changing the behavior of the system” was precisely his goal when he launched the Polish roundtable. All these efforts were attempts to change a prevailing political or ideological system in order to justify and rationalize broken promises. Therefore, even as important political change emerged from attempts to avoid the politics of breaking promises, the most fundamental and lasting changes in the political and ideological currents of democratic capitalism and state socialism emerged from attempts to confront it.

Hoskyns’s J curve also allows us to specify the exact ways three very important groups of actors—Western governments and international institutions, global capital holders, and the people of the Eastern Bloc—influenced the end of the Cold War. This book made clear at its outset that the last two decades of the Cold War really operated as a privatized Cold War in which both state and nonstate actors controlled nation-states’ access to energy and finance. Over the subsequent pages, we saw that Western governments and international institutions like the International Monetary Fund (IMF) had no influence over communist countries as long as global capital holders maintained confidence in those countries. Only when communist governments faced the imminent threat of losing access to private capital, or had already lost it completely, were Western governments and international institutions able to wield power and influence.

This is what made the capitalist perestroika so important. Throughout the 1970s, global capital holders were willing, indeed eager, to provide virtually limitless amounts of capital to the Eastern Bloc, leaving Western governments and international institutions with little power in the region. Only the potent combination of the Volcker Shock, the Reagan financial buildup, and the Polish Crisis caused global capital holders to question their lending to sovereign borrowers in general and to the communist world in particular. And after Western policy makers unwound the East-West interdependence of the 1970s, the potential for Western leverage over the Eastern Bloc emerged. The communist world did not permanently lose access to global capital markets after the early 1980s, but never again did it receive the unquestioning allegiance of global capital holders. This made future losses of market confidence, and thus future moments of leverage for Western governments and international institutions, inevitable.

The same forces that weakened the Communist Bloc’s standing on global capital markets renewed the United States’ preeminent position in the international system. Paul Volcker’s choice to impose Hoskyns’s J curve on the American population was the key act of renewal for the structural power of the United States in the international system in the postwar period. Volcker’s willingness to impose unprecedented economic discipline on the American people showed global capital holders that American policy makers could and would ultimately protect the interests of capital over the interests of labor. In return, they rewarded American policy makers and citizens with a deluge of capital inflows that erased the United States’ choice between guns and butter, renewed American prosperity, worsened inequality, and underwrote the projection of American power abroad. The two facts that have allowed the United States to remain hegemonic in the international system since 1980—the US dollar’s undiminished role as the world’s reserve currency and the United States’ ability to run virtually continuous budget and current account deficits for forty years—are both results of the confidence Volcker gave global capital holders that their money was safe in American hands.

Ronald Reagan was the inaugural beneficiary of this new and unforeseen configuration of American global power. The combination of Volcker and Reagan’s policies had enormously detrimental consequences for many groups both within the United States and abroad, most significantly American workers and the nations of the Global South. But they served three constituencies in the United States enormously well: consumers, the wealthy, and the government. The financial buildup that began under Reagan’s tenure funded both the largest tax cuts and the largest peacetime military buildup in the nation’s history. Given the complex interplay of economic, political, and ideological forces discussed in this book, it would be both absurd and highly simplistic to suggest, as some popular lore has it, that the Reagan military buildup ended the Cold War by bankrupting the Soviet Union. But we can also see that Reagan’s renewal of American military power in the 1980s produced its intended effect: to make clear to Soviet leaders that they could not match the bountiful material resources at Washington’s disposal for pursuit of the arms race and would be better off seeking its end.

The fact that the immense resources at Reagan’s disposal were not, as he liked to conclude, the product of a newly entrepreneurial American capitalism reinvigorated by supply-side incentives, but were instead the result of an increasingly globalized capitalism supercharged by the free flow of capital around the world, took nothing away from their potency. Indeed, by getting Japanese, West German, and Arab investors to pay for the development of the next generation of American military power indirectly through debt markets, Volcker and Reagan unwittingly accomplished a feat Soviet leaders were never able to achieve: getting their empire to pay for itself. After 1980, the American empire became an enormous material asset to Washington, while the Soviet empire remained an enormous material burden on Moscow. This disparity created a gaping imbalance of power between Washington and Moscow that was not just a matter of scale but also of form. Washington not only had more hard economic and military power than Moscow, but it also had allies that were materially integral to sustaining the projection of that power. A great deal about the subsequent collapse of the Soviet empire and the persistence of the American empire stems from this foundational difference in imperial form.

For a time, communist countries also benefited from the free flow of surplus capital around the world in the 1980s. The unexpected connection unearthed in these pages between the goulash of János Kádár’s communism in Hungary and the yen of Japanese investment houses in Tokyo bears witness to this fact. But communist states eventually lost access to global capital markets, and in these moments, Western governments and international institutions gained the power to influence their fate. This power came in two forms. First, through what I have called “the power of omission,” Western governments and international institutions withheld money from communist governments to force them to undertake domestic economic or political reforms. This was the essence of the power of the US government and the IMF in Poland and Hungary beginning in 1986 and 1987, the nature of the West German government’s power over the GDR beginning in October 1989, and the motivation behind the US government’s refusal to grant the Soviet Union large-scale financial aid in the spring and summer of 1990. By withholding communist states’ access to both public and private capital, Western governments and the IMF forced them to confront Hoskyns’s J curve and the treacherous political and ideological questions that came with that confrontation.

Second, through a form of power that is something closer to rewarding good behavior, Western governments granted communist governments money that allowed them to avoid or soften the blow of breaking promises in return for political and diplomatic concessions. This was, in fact, a tool that only the West Germans used on two important occasions. First, in August 1989 they granted Miklós Németh a DM 500 million loan and gave him broader assurances of economic support in return for his decision to let East German refugees amassed in Hungary leave for the West through Austria, striking a fatal blow to the viability of the GDR. And second, they offered Gorbachev a DM 5 billion loan and broader economic assurances in 1990 in return for his cooperation on German unification and accession to NATO, sealing the fate of German unity on Western terms. The evidence suggests that both Németh and Gorbachev made their decisions before reaching out to the West Germans. But it also makes clear that both governments stood on the precipice of losing access to global capital markets. Each man’s primary concern was softening the coming blow of Hoskyns’s J curve on their own population, and they knew that West German financial support could play a crucial role. Bonn, in turn, recognized the decisiveness of its financial support and was happy to help both leaders ease their domestic troubles if they granted significant political concessions in return.

In sum, we can see that a broad array of Western actors—governments, international institutions, and global capital holders—had a profound causal influence on the end of the Cold War. Scholars have long been reluctant to identify any significant Western role in bringing about the collapse of communism and the Cold War’s end, usually because those who did claim a decisive Western role used that version of history to pernicious ends in the post–Cold War world. But identifying instances of decisive Western power need not equal endorsement of that power’s use. Indeed, the most strident critiques of American, Western, or capitalist power are built on an understanding that Americans, Westerners, and capitalists are all too capable of producing results in foreign countries, not that they are more impotent than commonly thought. In addition to enhancing our empirical understanding of how the Cold War actually ended, this book allows us to make such an analytical move. We can identify the full scale, scope, and nature of American, Western, and capitalist power in the international system during this period without automatically endorsing it.

It should also be made clear, however, that there were no straight lines of influence from the halls of Western power to events in the Eastern Bloc. This book is emphatically not a story of how a quiet cabal of Wall Street financiers, secretive international institutions, and Western finance ministries magically and purposefully brought communism to its knees, nor is it a recommendation that financial coercion works at all times and in all places. Like the idea that the Reagan military buildup single-handedly ended the Cold War, we can see that the complex interplay of economic, political, and ideological forces at play in both the East and the West would make such claims highly simplistic and absurd. But this is a story of how a conjuncture of pressures—sometimes purposeful, sometimes not; sometimes coordinated, sometimes not—emanated from Western governments, international institutions, and global capital holders to slowly winnow the choices available to Eastern Bloc leaders. And through their incomplete patchwork of intentions, purposes, and coordination, Western actors played a substantial part in ending the Cold War.

But only a part. Western actors could force communist leaders to confront the politics of breaking promises, but only the people of the Eastern Bloc could make that confrontation a torturous, and ultimately fatal, political process for them. If the Soviet, Polish, Hungarian, and East German people had accepted economic discipline as passively (relatively speaking) as the American or British people did, there would be no collapse of communism and end of the Cold War to speak of. Once again, Hoskyns’s J curve helps us pinpoint exactly when and why popular resistance proved decisive. Hoskyns wrote in his memo that implementing his period of stabilization would depend on the population having “confidence about the future” so they would be willing “to make present sacrifices for future benefits.”9

This confidence—not just in the future but also in their government—was precisely what was lacking among the populations of the Eastern Bloc. It is why their moments of mass activism began exactly when their governments asked them to “make present sacrifices” in return for “future benefits.” The Polish working class, of course, set the standard for the whole bloc, and its revolts against austerity in 1970, 1976, 1980, and 1988 were the principal reason communist governments were never able to successfully implement the politics of broken promises. Solidarity’s bold emergence and brave persistence sent a message far beyond Poland’s borders about the political consequences of economic discipline. Working-class resistance was not as strident in other Eastern Bloc countries, but it did not need to be. Communist leaders in other countries feared that their own version of the Polish Crisis lurked behind any attempt to impose austerity at home.

Ultimately, Eastern Bloc peoples would not accept economic discipline unless it came from “their” government, as Rakowski concluded in 1989, and both the people and the communist leaders knew that whatever bond they might once have shared had long since been lost. Reestablishing that bond so that the state could implement the politics of breaking promises was the reason communist governments democratized themselves in the late 1980s. Thus, we can conclude that the peoples of the bloc played an essential and—given the formidable forces of violent repression arrayed against them—heroic role in creating their own future.

That conclusion coexists uneasily, however, with another one we must draw. It was common, in the euphoric moments of 1989 and its immediate afterglow, to think that the fall of communism and the birth of electoral democracy in the former Eastern Bloc signaled the dawn of a new era of popular sovereignty and self-determination for the peoples of the region. Rakowski’s diary entry about the Polish people’s feeling that at last they had “their” government in Warsaw attests to this sentiment. But this book has shown in detail that the government the Polish people thought was theirs was not theirs alone. It was, instead, a servant of two masters: the people and the market, or, if you like, capital and labor. From the preceding pages, we can see that one of the central contradictions—perhaps the central contradiction—of the collapse of communism was that the seat of government was returned to the people only so that their power to resist the government could be transcended. The end of the Cold War, we must conclude, was the moment in which the people’s power peaked and the moment in which it was overcome.

This contradiction was hardly confined to the collapsing states of the Eastern Bloc. Every government that lived on credit after the oil crisis—which, as we have seen, was most of them—was beholden to the twin masters of global capital and their own people, and this set distinct limits on the domestic policies they could pursue. Britain’s IMF crisis in 1976, the Federal Reserve’s fight to save the US dollar from 1978 onward, Mitterrand’s U-turn in France in 1982, and the countless structural adjustment programs imposed on the debtor countries of the Global South throughout the 1980s testify to these limits.

At its foundation, this book offers a structural explanation for the growing dependence of governments across the Global North on finance after the oil crisis of 1973: even though the world economy stopped growing at its exceptional postwar rate around 1970, people’s expectations of social and material progress did not. The politics of making promises remained far more popular and easy than the politics of breaking them, and governments found in finance capital a lifeline that made making promises still possible. The impulse to continue making promises was a perfectly natural, even noble, inclination on the part of governments, but it inevitably added a new counterparty—global capital holders—to the social contract between citizens and their states. As the relationship between citizen and state increasingly became mediated by borrowed capital, it is hardly surprising that it also morphed over time into a relationship between debtors and creditors, with the state—democratic or otherwise—mediating the relationship between the two. Nor is it surprising that the state slowly dropped its commitments to protecting the interests of labor and replaced them with commitments to protect the interests of capital. Neoliberalism—the governing ideology of capital, if nothing else—rose in the late twentieth century because nation-states’ dependence on finance capital to fulfill their social contracts rose as well.

It would be a mistake, however, to leave our explanation of the rise of neoliberalism there, as a story of capitalists accumulating more capital on account of the oil crisis and using that capital to impose their interests on the rest of the world. This book has also shown that neoliberalism rose because it proposed a relatively attractive ideological vision that promised to meet the governing challenge posed to both East and West by the oil crisis: how to justify in political terms and achieve in economic terms the transition from industrial stagnation to postindustrial modernity.

What was that vision? Hoskyns, again, put it right down on his page in words that shock our retrospective eyes. “Everyone knows that the UK economic problem is one of structural fatigue,” he wrote. “What is really needed is 10 years of vulgarly pro-business and pro-industry policies.” Those policies would include “zero, or near-zero inflation,” “reductions in Government’s % of GNP,” “the restoration of personal incentives,” “freeing up the labour market,” and, perhaps most importantly, “a profound cultural change” in attitudes toward wealth. “Fashion follows money,” he told the cabinet. “As the American academic said at the end of his lecture, ‘Don’t clap. Throw dollars!’” Previous governments, Hoskyns maintained, had been “constrained by union power in industry and the prevailing egalitarian mood.” Only if the government broke the unions’ grip and made the private sector “a better way of accumulating personal capital” would the country’s economic fortunes turn around. He hoped such a change in cultural sentiments could happen quickly but admitted that “it probably won’t happen until managers [in the private sector] are so prosperous and so lightly taxed that they begin to attract the attention of other parts of the population.” Changing the public’s negative perceptions of vast wealth and high inequality was the key. Once the country overcame its “traditional British hang up—the lurking fear that a few individuals might make a lot of money,” Hoskyns assured the cabinet, “a lot of good things will start happening.”10

The reason we know that the global spread of this vision—as neoliberal as any ever put to paper in a practical governing document—was not only the result of capitalists’ pressure on societies is that similar sentiments were soon being expressed on the other side of the Iron Curtain. Until the late 1980s, the Soviet Union had no significant dependency on Western capital and remained the bastion of Marxist-Leninist resistance to capitalist exploitation. And yet, as this book has shown, Soviet officials often lamented the “structural fatigue” of their industrial economy and the “egalitarian mood” of their population. They too wrestled with how to restore personal incentives to work, reduce the state’s role in the economy, free up the labor market, and close down unprofitable enterprises. They too settled on a form of “Don’t clap. Throw rubles!” as their motto and increasing inequality as their method. And they were not alone. It was the Hungarian communist leader Károly Grósz, an admirer of Thatcher, who put the prevailing view most bluntly. “Marxism has never accepted egalitarianism, but rather the postulate of equal opportunity,” he said in 1986. “This postulate takes into account, in all respects, the possibility of considerable inequality. . . . Equality has never been and cannot be a feature of socialism.”11

This turned the race to make promises that started the Cold War on its head. Far from debating how much economic equality and security would produce the most social progress, the countries of the East and West now found themselves debating how much economic inequality and insecurity would launch a new golden era. Just as in the race to make promises, their differences of degree were substantial, but they were not differences in kind. Far from racing to make promises, the two sides were now racing to break them.

Communism, however, made no sense in an era of breaking promises. The party could claim no special right to rule if it was just going to be any empty vessel for the allocation of the market’s punishments and rewards. Neoliberalism suffered from no such quandary. Not only did it seek to turn the state into as much of an empty vessel as possible for the market’s provision of luxury and anguish, but it went further. As Hoskyns’s words make clear, neoliberals sought to use the state to actively advance the interests of the wealthy few, all while justifying this pursuit in a lexicon of political and economic freedom. The collapse of communism and the rise of neoliberalism were thus two sides of the same ideological coin, the coin that governments use to justify the role they choose in mediating the relationship between their citizens and the economy.

We can close this book with one final observation about the legacy of broken promises for the world we currently inhabit. It comes in the form of yet another comment on Hoskyns’s graph. A keen observer will have noticed that the countries that go through his J curve of broken promises do not actually catch back up to the skyrocketing trajectory set by the postwar West. Their wealth and well-being slowly increase, but they forever remain in the shadow of that postwar Western line, which sprints off inexorably into a future of ever-increasing material and social progress.

That disparity is an apt indication of both the exceptional nature of the postwar period through the early 1970s and the mounting challenges of political and economic life in our own time. There is, in the end, no actual place called “the West.” It is, instead, the term used to signify expectations of eternal progress. The uniqueness of the postwar period until 1973—indeed, the uniqueness of the race between democratic capitalism and state socialism to make promises in the first half of the Cold War—was that for a brief moment in both East and West, there was no disparity between their line on Hoskyns’s graph and the Western one, no daylight between many of their citizens’ expectations and lived experience. At the significant price of racial and gender hierarchy in the West and authoritarian rule in the East, governments were able to promise at least their white men a better life and deliver on that promise almost as fast as those men could imagine what a better life was.

The economic turmoil of the 1970s swept away that neat alignment between promises and expectations, and we now live in a world forever in its shadow. In the wake of the wave of broken promises that swept the world in the late 20th century, economic growth continues. But it is accompanied by vast wealth inequality that destabilizes our politics and environmental exploitation that destroys our planet. How we can achieve a world in which states sustainably keep their promises to all their citizens is the vital question that arises after broken promises have triumphed. They are the questions that define our time.