PART ONE

CHAPTER 1

ON DECEMBER 10, 1976, East German prime minister Willi Stoph was leaving Moscow disappointed and empty-handed. He had come to the Soviet capital seeking an increase in Soviet oil deliveries to the German Democratic Republic (GDR), but his Soviet counterpart, Alexei Kosygin, had roundly rejected his request. “We don’t have the resources for it,” Kosygin had said during their meeting in the Kremlin. “We have an acute energy shortage in our country. . . . You must get your mind out of the clouds.” “My mind’s not in the clouds,” Stoph shot back. “But you want us to increase our deliveries,” Kosygin responded. “We cannot meet that level of demand. No one in the world can do that.”1

Now, as the two men drove through the streets of the Soviet capital on their way to the airport for Stoph’s departure, Kosygin tried to lighten the mood by reminding his comrade of the overriding advantages of the socialist system compared to the chaos that currently prevailed in the capitalist world. “We understand that the situation in the GDR is not easy,” the Soviet premier said, but “compared with the predicament in capitalist states, all socialist states—the USSR as well as the GDR—[are] in an incomparably better situation.” To him, the advantages were clear. The socialist countries were “in a position to plan” their economies “until 1980, 1985, and beyond” as well as “agree on the course of our development.” In contrast, Kosygin said, “capitalist states couldn’t even plan for the next three months.” Perhaps shaken from his disappointment by Kosygin’s comparison, Stoph piled on the criticism of their ideological foes. “All of the planning efforts of capitalist states have only led them into crisis,” he said. Kosygin agreed and concluded, “Our situation is a thousand times better.”2

In the mid-1970s, one did not need to be a communist ideologue to share this view. Indeed, many in the West believed that the economic crises of the early 1970s had exposed fundamental flaws in both capitalism and democracy. The combination of widespread unemployment and high inflation throughout the West confounded both the professional economists who studied market economies and the democratically elected leaders who governed them. The reigning economic doctrine of Keynesianism offered few answers in this world of “stagflation,” and those it did put forth—increased government spending and accommodating monetary policy—appeared to only make the problems worse. Because democracy subjected Western governments to the demands of all their citizens, it was widely believed that Western welfare states were doomed to chronic high inflation because politicians needed to promise their citizens too much of the good life in order to get elected. In foreign policy, a new buzzword—interdependence—dominated discussions of the West’s place in the world and appeared to portend an end to Western societies’ control over their own fates. What could the developed West do in the face of dependence on oil from the Middle East? To many on both sides of the Iron Curtain, the answer appeared to be nothing at all. Could democratic leaders solve the riddle of stagflation if it meant inflicting pain on those they governed? Smart money said no.

The Eastern Bloc was thought to be different. Socialist states appeared to Western observers to be largely immune to the crises afflicting the capitalist world. As the exchange between Kosygin and Stoph shows, socialist leaders maintained a similar confidence in the superiority of their own system. Because the Soviet Union was one of the world’s largest producers of energy resources, the fourfold increase in the price of oil at the end of 1973 and early 1974 first arrived as a financial windfall rather than a structural economic challenge for the leadership in Moscow. The socialist states of Eastern Europe had little oil themselves, but under the generous patronage of the Soviet Union, they received large and growing deliveries of Soviet energy during the 1970s at highly subsidized prices. Because almost all trade and prices were fixed under five-year plans within the bloc, socialist states appeared exempt from the violent gyrations of inflation and commodity price shocks that crippled the Western world. And if democracies’ penchant for promising their citizens too much was the cause of Western inflation, then the socialist states’ authoritarian structure appeared to make them helpfully unresponsive to the demands of their populations. Taken together, these traits were enough to keep Kosygin and Stoph brimming with confidence as they drove through the Soviet capital that day in 1976.

And yet we begin with their exchange because beneath the professions of confidence, the discussion also pointed to the problems upon which state socialism itself would founder. Stoph had made the initial request for more Soviet oil for a very particular purpose: to lower the GDR’s ballooning sovereign debt to Western banks and governments. With more oil, the GDR would be able to produce more petrochemicals and export them to the West for hard currency. This, in turn, would lessen the need to take out Western loans to pay for imports and service old debts. In the first half of the 1970s, Western banks had been eager to loan money to the Socialist Bloc for the very reasons socialism appeared ascendant to all manner of Western observers in the 1970s: it had energy, authoritarianism, and no inflation. But by 1976, the first inklings of doubt had begun to bubble up in the minds of Western bankers: Would socialist states really be able to pay them back? Seen in this light, it becomes clear that Stoph’s pilgrimage to Moscow in search of oil was, in fact, an indirect effort to put the minds of Western bankers at ease and keep the flow of Western capital running smoothly.

The GDR’s predicament was far from unique; all states in the Council of Mutual Economic Assistance (CMEA or Comecon) shared the East German dependence on both Western capital and Soviet oil to varying degrees.3 Thus, Kosygin’s rejection of Stoph’s request points to the second problem lurking in the background of their discussion: after a ten-year period of dramatic growth, Soviet energy resources began to plateau in the mid-1970s and were projected to decline after 1980. The Eastern Bloc’s apparent imperviousness to the travails of the global economy rested on these two foundations: easy access to Western capital and an ever-increasing supply of Soviet energy resources. If either or both of these faltered, as they would around 1980, the entire bloc would be forced to reckon with the social, economic, and political problems that beset the West after 1973.

Thus, this chapter tracks the response of both the industrial West and the socialist East to the oil crisis to make one overriding point clear. Although the crisis at first appeared to validate the fundamental differences between democratic capitalism and state socialism, in time it demonstrated that both blocs were subject to the pressures of the same world market. It was a market neither side could fully or even partially control, so how the states within each system reacted to the whims of the global economy became the key determinant of their success and survival. The dramatic expansion of global capital markets after the crisis presented both sides with a means of softening the blow of adjustment to the new market conditions. But the fundamental challenge the crisis posed to both the democratic capitalist states of the West and the state socialist systems of the East could not be permanently avoided. The crisis challenged governments on both sides of the ideological divide to domestically distribute the economic losses caused by the oil price shock, transition their societies to more profitable and energy-efficient systems of production and consumption, and maintain access to the global capital markets that rapidly expanded after the oil shock. All these pressures, in turn, threatened the legitimacy of both the welfare states in the West and the communist states of the East. At first faintly felt and then stridently resisted, the crisis began the transition from making to breaking promises for both blocs.

![]()

On October 6, 1973, war came once again to the contested lands of Israel and its neighbors. Early that afternoon, Egyptian armed forces crossed the Suez Canal into the Israeli-occupied Sinai Peninsula, and Syrian forces pushed from their homeland to confront Israeli forces occupying the Golan Heights. Over the next three weeks, the Arab coalition and the Israeli Defense Forces fought pitched battles in what would come to be known as the Yom Kippur War. In the early days of the fighting, the Soviet Union resupplied its Arab allies, and on October 14, the United States responded with its decision to resupply Israel. For the Arab Gulf states that supported the Egyptian and Syrian campaign, the American decision demanded a response equal to the perceived injustice of supporting Israel. Thus, they unsheathed “the oil weapon” and unilaterally announced a 70 percent increase in the price of their oil to $5.11 a barrel. The next day, they committed themselves to a rolling embargo against supporters of Israel, chief among them the United States. After US president Richard Nixon announced a new aid package to Israel on October 19, King Feisal of Saudi Arabia upped the ante considerably by imposing a complete embargo on oil supplies to the United States.

By the end of October, the guns had fallen silent, but the effects of the price increase were only beginning to ripple outward. In December, ministers from the Organization of Petroleum Exporting Countries (OPEC) met in Tehran to discuss where to peg the oil price going forward. At the urging of their host, Shah Mohammad Reza Pahlavi, the group settled on an even higher price target of $11.65, one that would have been unfathomable only months before.4 As recently as 1970, OPEC had only been able to fetch $1.80 per barrel on the world market. With the breakdown of the Bretton Woods system in 1971 and the resulting devaluation of the US dollar (in which oil was priced), some of the oil price increase could be accounted for by producers’ desire to recapture the value they had lost with the dollar’s decline. But the fourfold increase from $2.90 in mid-1973 to $11.65 at the end of the year represented more than that. Economically, it reflected the fact that the development of affluent industrial societies in the West had increased oil demand sixfold since 1950 and had pushed the United States beyond energy autonomy to dependence on foreign oil in the late 1960s.5 Politically, the price increases represented a precipitous culmination of decades of struggle on the part of developing nations to increase the value of the commodities that formed the basis of their national wealth. When they collectively called for a “New International Economic Order” at the United Nations in May 1974, they did so with the winds of long-sought wealth at their backs.

The boon for the oil producers of the world delivered a bust to the developed world on a scale unknown in the postwar years. The oil crisis arrived in a Western world already beset by a burgeoning list of economic problems. Chief among them was inflation. The rising price level had a diverse set of causes, including US president Lyndon Johnson’s attempt to fund his Great Society programs and the war in Vietnam without a tax increase, an explosion of real wage increases across the West from 1968 to 1972, and the 1971 American decision to suspend the convertibility of the dollar into gold. Washington had abandoned the Bretton Woods system of fixed exchange rates in response to the continued economic rise of Western Europe and Japan, which increased competitive pressure on US industry and decreased America’s relative standing in the world economy. The devaluation implicit in the 1971 decision, and the floating exchange rate system that soon followed, restored a measure of US competitiveness.6 But it also produced persistent monetary instability in the capitalist world and freed the United States from the nominal constraint of limiting its money supply to amounts that could be converted into gold at thirty-five dollars an ounce. In combination, these forces had pushed consumer price inflation in Organization for Economic Cooperation and Development (OECD) countries to an annual rate of 8.2 percent in 1973.7 With prices already galloping ahead at a steady pace, the fourfold increase in the price of the commodity that formed the basis of industrial society was bound to have dramatic economic effects.

In short order, in 1974–1975 the West experienced its worst economic downturn since the Great Depression.8 Unemployment across the OECD reached 5.5 percent in 1974 and peaked at 8.9 percent in the United States in May 1975.9 Under the economic conditions that had prevailed since 1945, a downturn of such scale would have nipped the problem of inflation in the bud. But the skyrocketing oil price made this contraction different, and consumer price inflation increased across the West to 14.1 percent in 1974 and 11.8 percent in 1975.10 And so, in defiance of postwar economic theory and experience, “stagflation” was born.

In the realm of public policy, the years since 1945 in the West had unfolded in the long shadow of British economist John Maynard Keynes and the body of economic theory that bore his name. During their heyday in the 1960s, Keynesian economists who populated Western governments had declared victory over the business cycle and professed the ability to prevent economic downturns through changes in monetary and fiscal policy. “Recessions are now considered fundamentally preventable, like airplane crashes and unlike hurricanes,” Arthur Okun, Lyndon Johnson’s chief economist, declared in 1970.11 On the European continent and in Japan, two decades of almost uninterrupted economic growth from 1950 to 1970 lent the credibility of lived experience to such claims. Even in the United States, where recessions had been a recurrent, if mild, part of postwar life, economists in the 1960s found reason to think that economic performance was ultimately subject to government control. The Phillips curve, named for the New Zealand economist, A. W. Phillips, who had first theorized its existence in 1958, purported to show that inflation and unemployment were inversely related—the more one went up, the more the other would go down. With this knowledge in hand, economists argued in the 1960s that governments could control the level of both inflation and unemployment through fiscal and monetary fine-tuning.

Using this line of thinking, postwar governments had based their policy and built their legitimacy on the promise of optimizing the social effects of the economy. From this, the central economic goal of the Western welfare state emerged: full employment. As Charles Maier has written, “a full employment ‘standard’” emerged after 1945 as the measuring stick by which all Western governments were judged. Under this standard, it was now the responsibility of government to ensure that everyone who wanted a job had one. This commitment was a dramatic departure from the responsibilities of democratic capitalist governments in the prewar years, when, under the gold standard, the nations of the West prioritized their international solvency over the interests of their domestic working classes. The horrid experience of the Great Depression, Europe’s descent into fascism, and the emergence of a Socialist Bloc that purported to govern in the interest of the working class all forced democratic capitalist governments after the war to adopt the interests of the working class as their own. The result of this fusion of interests between the working class and its governments was full employment. As Maier has written, “Accepting the primacy of full employment meant that a major priority of the working class had become that of society in general.”12

Stagflation, quite plainly, called into question the entire promise of Keynesian governance and, with it, the legitimacy of Western welfare states too. If the basic task of postwar government was to do something to protect the interests of the working class, it was not clear after 1973 what that should be. Inflation appeared to signal that governments and the unions they supported had already done too much. As a financial phenomenon, inflation was straightforward to understand—the price level increased when there was more money than goods in an economy. But as a social phenomenon, inflation was a signal of unresolved conflicts within a society over how wealth should be distributed. Workers believed they should get a greater share, so they demanded wage increases. Capital, unwilling to see its profits decline, responded by increasing prices, and the process continued without resolution until there was more money than goods. More than simply a monetary phenomenon, inflation appeared in societies where competing social groups had been promised more than the market could deliver.13

In Western societies, the culprit of the accumulated promises was widely believed to be the postwar welfare state and its foundational promise of full employment. Inflation was caused by “the worldwide commitment to full employment and maximum production,” the American magazine Business Week wrote in October 1974. This view was not confined to the spokesmen of the business community. Even those sympathetic to the interests of labor and the welfare state, such as Keynesian economist Paul Samuelson, agreed that the 1974–1975 crisis signaled that governments were doing too much to protect workers from market realities. Inflation “is deep in the nature of the welfare state,” he concluded, because “even when there is slack in the system, unemployment doesn’t exert the downward pressure on prices the way it did under ‘cruel capitalism.’” The problem, he wrote, was that no one wanted “to turn the clock back.”14

This is precisely what made defeating inflation so difficult. It implied someone would have to lose. The oil crisis compounded the challenge by bringing about the situation the Phillips curve had proclaimed impossible—high unemployment and inflation at the same time. Governments could fight one or the other, but not both at once. The stability of Western societies and the legitimacy of their governments depended on the restoration of economic growth, but the fight against inflation required that this restoration not add more claims on societies’ resources to those already going unfulfilled.

In Europe, this predicament threatened to destroy the fragile order that had emerged since 1945. “The postwar era is over,” the historian Fritz Stern declared in a May 1974 article. “For some twenty-five years . . . a steadily expanding economy protected Europe from major political upheavals.” In the upheavals of 1968, students and radicals may have rebelled against the conformity of bourgeois life, but the core constituents of postwar politics—the workers—had been appeased with ever-increasing promises of prosperity. “The workers of Europe found embourgeoisement a novel and, on the whole, exhilarating experience,” Stern wrote. “Each year, in every European country, more workers were able to afford cars, take vacations, dream of country bungalows, hope for a better life for their children.” That world was now gone. With Europe headed toward “‘zero growth’—at best,” Stern believed democracies on the continent would be robbed of the premise of prosperity that had underpinned them since the Second World War. Without prosperity, no one could be sure there would still be peace.15

The promise of the postwar order therefore had to be kept alive, even as its economic foundation crumbled all around it. Across the West, governments and the unions they supported ensured that the living standards of the working class were protected as the oil price shock took hold in 1974. In the United States, workers’ pay increases for the year outpaced inflation.16 In West Germany, the first public employees strike in the country’s history in May brought workers across the board a 3.4 percent real wage increase for the year.17 In Great Britain, a tense national election in February 1974 yielded a weak Labour government that immediately granted the nation’s industrial workers a 29 percent nominal wage increase.18 In Italy, where all salaries were indexed to inflation through a system called the scala mobile, workers even received a 10 percent increase in real wages in 1975.19 In Japan, where inflation ran at an astounding 24 percent in 1974, workers easily covered the increase with a 32 percent increase in wages.20 Across the West, the first reaction in every political system was to protect the nation’s workers from the changing global market.

Since the promises of postwar politics were not easily jettisoned, new sources to fund them had to be found. The oil crisis transferred roughly 2 percent of the world’s wealth to the oil-producing nations, and if life in the West was to go on as it had before, a way needed to be found to bring these funds back into Western economies.21 “Looking out to 1980 and beyond,” the US Treasury noted in August 1974, “the World’s capital requirements will be massive by historical standards.”22

The Euromarkets—the forerunners of today’s unregulated global capital markets—presented one possible avenue for distributing world savings from oil producers back to oil-consuming nations. Founded in London in 1955 using Europeans’ surplus US dollars, the Euromarkets were made up of all currency held outside its country of origin and thus subject to little regulation. Because the US dollar was the most important and widely used currency in international trade, Eurodollars represented the overwhelming majority of liquidity in the Euromarkets, though West German deutsche marks, Swiss francs, and British pounds played a role as well. Throughout the 1950s and 1960s, the United States heavily regulated the interest rates banks could apply to their deposits within the United States, so increasing numbers of companies, banks, and central banks began to keep their US dollar holdings abroad and receive a higher rate of return in the Euromarkets. Neither the US nor the British government was eager to regulate this activity, so the Euromarkets continued to grow. By 1970 the markets were valued at $80 billion, and by the time the oil crisis struck, they represented one option for mediating the world’s rapidly growing financial interdependence.

They were far from the only one, however. Many financial observers and policy makers believed that governments or the International Monetary Fund (IMF) would have to manage the recycling process rather than leave such an important element of the global economy to the volatility of the marketplace. In the first ten months of 1974, OPEC nations deposited $16.5 billion of their $45 billion surplus in the Euromarkets compared with just $10.5 billion in the United States.23 This was a strong boost for the unregulated markets, but most doubted it could last long. On June 26, 1974, West Germany’s largest private bank, Herstatt, collapsed under the pressure of speculative foreign exchange losses. Many within the financial community itself believed the crash would be just the first of many dominoes to fall if the recycling process remained the responsibility of banks and the Euromarkets. Banks were using short-term deposits from OPEC countries to make loans to oil-importing countries with maturities ranging from seven to ten years. That was, as the Wall Street Journal noted days after the Herstatt collapse, “borrowing short and lending long, the bankers’ classic formula for trouble.” Given what appeared to be an untenable situation, the Journal—not usually known for its advocacy of governmental control—concluded that governments and the IMF would have to take over the primary task of petrodollar recycling. “The only other choice is an ominous one,” it noted, “drastic reductions of imports, currency devaluations and sharp economic slowdowns at the cost of rising unemployment.”24

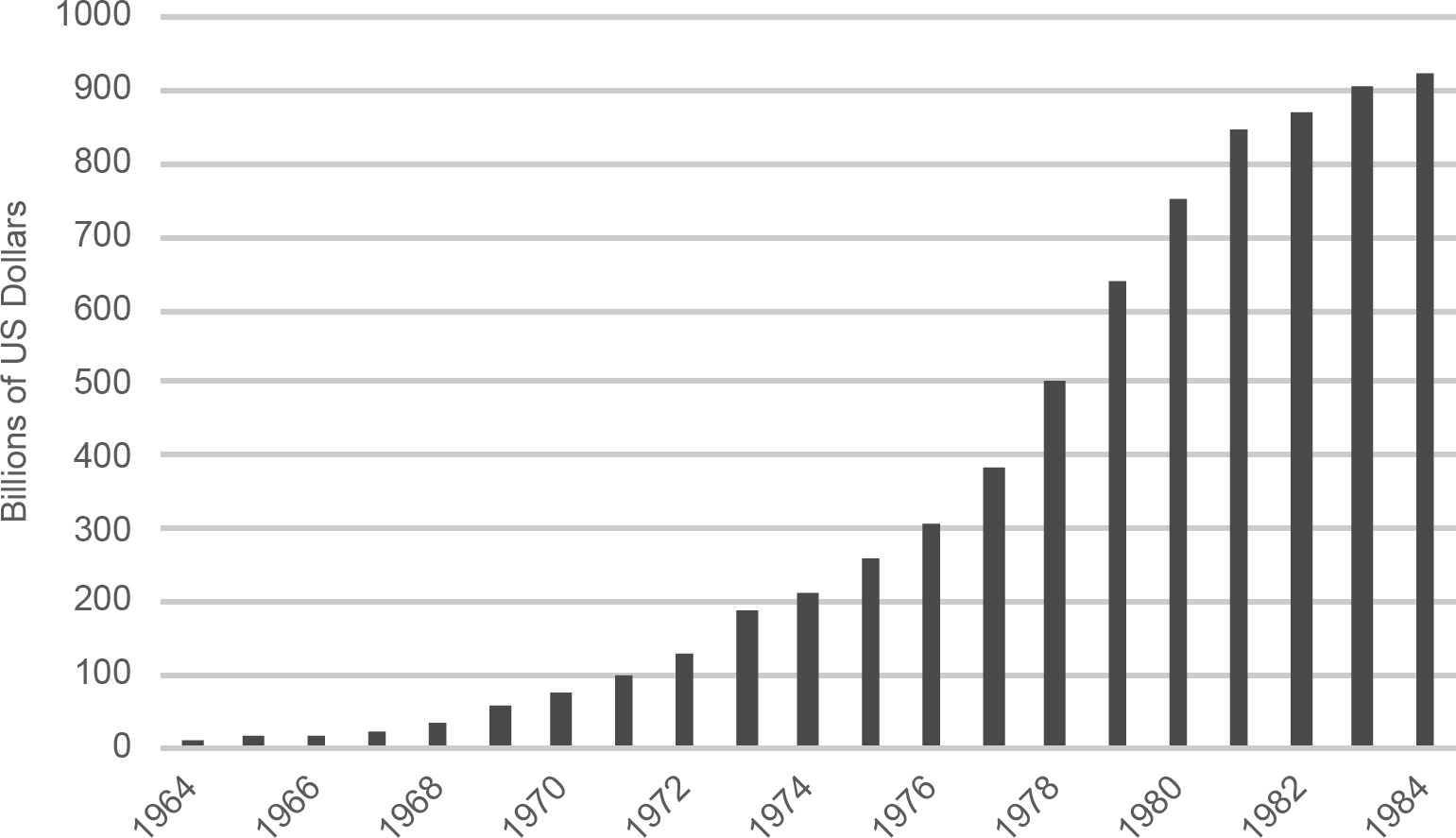

Once more, events defied expectations. By late 1974, it became clear that oil producers had no interest in using finance to destabilize the countries that purchased their oil, and they moved to secure their deposits with Western banks on a longer-term basis. Banks, in turn, found fewer reasons to worry about lending to countries. By the summer of 1975, a US Treasury official could report that “the financing problems due to the OPEC financial accumulations now are generally recognized by most banks as manageable.”25 If the private banking system could manage the recycling process, there was little role for the IMF or governments to play. From the start of 1975 onward, government efforts to control the recycling process waned, and the vast majority of sovereign borrowing stayed on the Euromarkets, which continued their skyrocketing growth for the remainder of the 1970s (Figure 1.1).

Figure 1.1 The growth of the Euromarkets from 1964 to 1984.

Data source: Benjamin Cohen, In Whose Interest? International Banking and American Foreign Policy (New Haven, CT: Yale University Press, 1986), 23, table 2.2.

This was, for the history of both democratic capitalist and state socialist governments, a fateful development. With the world’s surplus capital now at its disposal, the international financial community became an arbiter of politics around the world. Neither bankers nor most politicians were eager to see the role of finance in these terms, but it was true nonetheless. Any nation-state, East or West, that relied on borrowed capital to fund the products of its domestic politics was now subject to the capricious confidence of capitalists. As long as markets remained convinced that borrowed capital would be repaid on time and with interest, politics within states could proceed normally. Politicians could continue to promise their people prosperity, and the legitimacy of the government could survive unquestioned. But should market confidence ever falter, the domestic politics of borrowing states would be thrown into immediate disarray. In both East and West, the temptation to use borrowed capital to support domestic living standards proved too strong to resist. This meant there was now a direct connection between the promises governments made to their citizens and the capital markets they used to fund them.

As the importance of global capital markets rose after 1975, the importance of central banks increased in equal measure. If governments could not control the capital markets to which they were now subject, central banks still could control how much liquidity pulsed through those markets on a daily basis. This made the reaction of the most important central banks in the world to the escalating economic crises of the 1970s as important as the response of governments. At the US Federal Reserve, the most important central bank in the world because of its control over the liquidity of the US currency now circulating the globe as petrodollars, the bank implemented a brief period of high interest rates in the spring of 1974 to counter the oil price shock, but it quickly returned to an accommodating policy by autumn. This left interest rates at or below the level of inflation, which, in turn, made the real cost of borrowing US dollars around the world virtually zero. With minor variations, the real cost of dollars remained close to zero until the late 1970s.26 Needless to say, this encouraged the global sovereign lending process a great deal.

Other central banks tried harder to restrict the growth of money and reduce inflation in their societies. West Germany and Japan both adopted forms of monetarism in the mid-1970s that brought them a measure of success in controlling inflation within their borders. But as long as the real engine of global liquidity, the US Federal Reserve, failed to attack inflation with all its might, governments would continue to have little trouble financing the race to make promises. Until the Federal Reserve adjusted, political systems throughout the world would not be forced to adjust either.

This made any governmental attempt to defeat inflation a political choice—and an extremely unpopular one at that. Three days after assuming the presidency in August 1974, US president Gerald Ford told the nation in a nationally televised address, “inflation is our domestic public enemy No. 1,” and proceeded to launch a campaign to WIN (Whip Inflation Now), under which he encouraged Americans to grow their own food, balance their budgets, and use credit sparingly. Doing little to halt inflation, the only real effect of the WIN campaign was to contribute to the record losses of the Republican Party in the November 1974 midterm elections. Chastened by defeat and dealing with massive Democratic majorities in both houses of Congress, Ford signed a series of simulative tax cuts in 1975 and left the challenge of government-imposed austerity to another day.27

Throughout the rest of the West, governmental attempts to prioritize fighting inflation over restoring full employment were ground to pieces by the forces of political opposition. Only in West Germany did Chancellor Helmut Schmidt, a social democrat who enjoyed strong ties with the West German trade unions, succeed in passing a contentious austerity package in 1975. He did so by leaning on his stature as a representative of the workers who was merely delivering the economic bad news the new market conditions demanded. As he told the nation the year after the austerity measures passed, “Nothing will ever be like it was before 1974.”28

Most Western politicians and the constituents they served did not want to believe Schmidt’s fatalistic conclusion. Even those who did found that their message was deeply unpopular in democracies that favored those who promised a return to the glory of the postwar golden age. Perhaps no other work captured the prevailing mood across the West like the British economist Fred Hirsch’s 1976 The Social Limits to Growth. “Economic liberalism,” Hirsch wrote, is “a victim of its own propaganda: offered to all, it has evoked demands and pressures that cannot be contained.” The promise of affluence had been extended to everyone in Western societies because of the “principle of universal participation” and “the demands of political legitimation.” Although “the spread of bourgeois objectives downward through the social scale strengthens the political legitimacy of liberal market capitalism,” Hirsch wrote, “the same process proves ultimately disruptive to economic performance.” The fundamental economic problem of “advanced societies,” he wrote, was now “a structural need to pull back the bounds of economic self-advancement.” The prospects of this occurring were dim because the “central fact of the modern situation is the need to justify” policy choices to the population. That, Hirsch wrote, was “its moral triumph and its unsolved technical problem.” The fact that resolution to the West’s economic problems needed to be “ethically defensible” imposed “drastic limits on the set of feasible solutions.” This meant the biggest challenge to industrial societies was not formulating policies to solve the crisis of stagflation but rather gaining “the public acceptance necessary to make them work.”29

Public acceptance was indeed the challenge of the hour, and few Western states appeared capable of fostering it. If social consensus would forever evade Western democracies, perhaps political systems that discarded it altogether would fare better in the post-1974 world. If nothing would ever be the same after the oil crisis, perhaps the future at last belonged to state socialism.

![]()

Quite understandably, the socialist leaders of the Eastern Bloc wanted to avoid the problems vexing their democratic capitalist counterparts at all costs. At first glance, they appeared well positioned to do so. Until the mid-1970s, prices within Comecon were fixed as part of the five-year planning process. Thus, in 1970, the USSR had set the price for its oil within Comecon for the entire period 1971–1975 at roughly 14 rubles per ton, about $2.43 per barrel.30 At the time, oil prices on the world market hovered around $2 per barrel, so Comecon states paid a slight price premium for Soviet oil. It was a premium they were happy to pay because trade with the Soviet Union was not conducted in hard currency—currencies that were freely convertible, such as the US dollar, British pound, or West German mark. Although Soviet oil was priced in rubles for accounting purposes, Comecon trade was conducted on a barter basis within the five-year plans. Before the oil crisis, planners would use the five-year planning process to determine that Soviet oil was worth a certain amount of East German television sets, Polish ships, or Czechoslovak engineering equipment, and then trade for the entire period would proceed at that price.

For Eastern Bloc countries, which generally imported raw materials and exported finished products, this arrangement had two overriding advantages compared to the trade they conducted on Western markets: their products had a guaranteed buyer and could be sold without regard for their quality. Soviet officials could (and did) protest about the quality of East European goods sent their way, but without radically altering the structure of Comecon, there was little they could do to stop the flow of inferior goods. These advantages for Eastern Europe notwithstanding, trade within Comecon before the oil crisis was not fundamentally different from trade on the world market. The barter system did not emphasize quality, but the economic value ascribed to goods (as seen in the rough parity of Comecon and world oil prices) was basically in line with world market values.

The commodity price explosion of the early 1970s fundamentally altered this dynamic. Within a matter of months from late 1973 to early 1974, the world market value of the Soviet Union’s energy resources quadrupled, and with it, the country’s dominion over the rest of the bloc became an enormous economic liability. As long as world oil prices remained above ten dollars a barrel, any deliveries of Soviet oil to Eastern Europe at two and a half dollars a barrel would represent a breathtaking loss on the sale of the country’s most valuable asset. But if the Kremlin adjusted Comecon prices to reflect the new world market prices, Eastern Bloc countries would have to dramatically increase their exports to the Soviet Union to pay the new prices. This increase in exports would have to come at the expense of domestic consumption, and thus it had the potential to disrupt the unwritten social contracts of late socialism and produce severely destabilizing social unrest. This was a prospect all Eastern Bloc leaders hoped to avoid, so they used all the tools at their disposal to insulate their domestic social contracts from changes in the world market and Comecon. After the oil crisis, a new tension defined relations among the “fraternal allies”; the economic interests of the Soviet Union now stood in stark opposition to the political, economic, and social priorities of the bloc as a whole.

This tension first appeared in 1974 after the Soviet leadership proposed a new Comecon pricing system that would dramatically increase the price of Soviet energy resources in order to bring them more in line with the new world market prices. The Soviet Politburo debated the issue on numerous occasions that year, and Soviet general secretary Leonid Brezhnev “personally attache[d] great importance to this question,” Gosplan chairman Nikolai Baibakov told his East German counterpart, Gerhard Schürer, in December that year. The Soviet leader believed “that no socialist country, nor the Soviet Union, should have a setback in national economic development due to price regulation.” For the leadership, the issue of oil prices was “fundamentally a political question, not just a purely economic problem,” Baibakov said. Soviet leaders knew that a transition to current world market prices “could lead to the emergence of chaos in the economies of the socialist countries, as is currently the case in capitalist countries.” At the same time, however, they believed the socialist countries could not “completely separate themselves from the development on the world market” because the price changes were “an objective [and] irreversible process.” This meant that the Socialist Bloc could not “escape the prevailing price increase on the world market.”31

Escape was precisely what Eastern European leaders believed the bloc should do. For them, the oil crisis was the clearest sign yet that capitalism was prone to crisis and doomed to failure. Official East German policy maintained that the oil price shock was “influenced to a large degree by speculative and inflationary factors” that arose “out of the intensification of the general crisis of the capitalist system, especially from the chronic energy, currency, and financial crisis.”32 Similarly, the Hungarian Socialist Workers’ Party concluded that “manipulations of international capitalist monopolies” had produced the commodity price shock. “The general crisis of capitalism deepens,” party documents declared.33

Faced with capitalism’s evident failures, Eastern European leaders thought it foolish to willingly import the effects of capitalism’s crisis through changes to Comecon prices. As GDR policy makers told their Soviet comrades, the bloc “should under no circumstances” incorporate price increases into the Comecon price system based “on speculative . . . factors of the imperialist system.” Such a move would only “transmit the effects of capitalist inflation into our economic relations.” This would not only have “economic effects,” they warned. “We must also recognize that political problems could arise if price increases for raw materials trigger a general price increase within our community of states.”34

Soviet leaders understood the explosive social potential of price changes, but they remained firmly convinced the oil price increase was something to be celebrated, not admonished. Far from signaling the power of monopolies and speculators in the capitalist world, the commodity price shocks represented a resounding victory for the global forces arrayed against Western imperialism. “Something fundamental has happened in the world,” Nikolai Patolichev, the Soviet minister of foreign trade, told his East German colleagues. “Developing countries have achieved their economic independence in recent years. 1973 was the conclusion of this struggle. This is not an imperialist process but an anti-imperialist development.” The socialist community had “supported developing countries in their political struggle, and now they have triumphed,” Patolichev said. This meant that “by their very nature, the new commodity prices are the result of the anti-imperialist struggle.”35

The differences in ideological interpretation between the Kremlin and its allies reflected differences in national self-interest and domestic politics exposed by the oil crisis. As the Soviet foreign trade minister Patolichev rhetorically presented it to GDR officials, “How are we to explain to our people that we are selling our oil 30 rubles below the world market price?” The allies needed to understand, Patolichev said, “what it would cost the Soviet side to sell the raw materials so cheaply.” The Soviets could not go on providing such a subsidy because they could no longer “explain it to the Soviet people.” This made it “absurd to reject” the Soviet Union’s “authority (Berechtigung)” to revise the Comecon price structure.36

Bloc governments equally felt the pressure to please their people. As East German leader Erich Honecker wrote in a 1974 letter to Brezhnev, the GDR leadership felt it could not allow “a reduction of the population’s standard of living” because the state’s “class enemies” in the West led “a daily ideological diversion against the people of the GDR.” To counter this threat, the East German leadership thought it “necessary to solve a series of social questions (increases in pensions, the minimum wage, support for young families, aid for children, [and] acceleration in the construction of housing, hospitals, and schools, etc.).”37 The same governing strategy defined the regimes of János Kádár in Hungary, Edward Gierek in Poland, Gustáv Husák Czechoslovakia, Todor Zhivkov in Bulgaria, and Nicolae Ceauşescu in Romania. Higher Soviet energy prices would mean fewer houses in Leipzig, lower wages in Gdánsk, emptier shelves in Sofia, and more political instability everywhere.

Ultimately, it was the Soviet Union that had the oil, so it was the Kremlin that set the policy. At first, the Politburo decided that energy prices within Comecon for 1975 should be set based on an average of the world market price in 1973 and 1974. Because these two years contained the dramatic price increases, this would have served Soviet economic interests handsomely. But after hearing loud protestations from their allies, the Politburo decided that the two-year price average would be “too difficult for the socialist countries.” Instead, they chose to base the 1975 price on an average of 1972, 1973, and 1974 in order to include “one year each with low, medium, and high price[s].” After 1975, Soviet officials decreed, the Comecon price system would adjust based on a rolling average of the previous five years of world market prices.

It was a decision worth billions of rubles—and, by extension, billions of dollars. As Baibakov explained, if Comecon had moved immediately to world market prices, the socialist countries would have had to export an extra 16 billion rubles worth of goods to the Soviet Union during the 1976–1980 Five-Year Plan. Under the system of flexible prices, the 16-billion-ruble burden on Eastern Europe would fall to 7 or 8 billion rubles.38 Patolichev described the new sliding price system as “an optimal compromise, which splits the necessary strains between the USSR and the other CMEA countries.” Optimal did not mean easy, however. Everyone involved in the negotiations throughout the bloc knew that the consequences of their decisions would be vast and long lasting. As Patolichev told Honecker in the midst of a particularly testy exchange, “The current change in Comecon prices is the most difficult task of my life. . . . The system of sliding prices is not only a question for the USSR, but also politically and economically important for the entire socialist community.”39

What appeared difficult to Soviet officials appeared life threatening to Eastern European officials. Even under the sliding price system, it was now clear the price of energy for bloc countries would dramatically increase in the years ahead. Upon hearing of Moscow’s move to change the pricing system, Erich Honecker called an emergency meeting of the East German leadership to formulate a response. There were domestic and international dimensions to the Soviet decision that needed to be discussed. Internationally, the general secretary observed that the oil crisis had fundamentally, and perhaps permanently, changed Eastern Europe’s economic value to the Soviet Union. “Until now,” he said, “we have paid more for a ton of oil from the USSR than the FRG [Federal Republic of Germany]. That may have changed as a result of the price increases in the West.”40 For the foreseeable future, Eastern Europe would now be an economic burden on Moscow.

Domestically, the sliding price system presented the prospect of social and political disruption. The first estimate of the economic losses for the GDR under the new price system projected an additional cost of 7–8 billion marks in 1975 and 8–9 billion marks per year during the period 1976–1980. To put the scale of these costs in perspective, state planners warned the Politburo that the new annual costs for Soviet oil were “more than the annual increase in national income.” Günter Mittag, Honecker’s deputy and the chief economic official in the GDR, understood immediately what this would mean for the country: “an absolute fall in living standards in the GDR.” He was furious. If prices were not fixed, then insulating the GDR from world market volatility would be impossible and the inflation pervading the capitalist world would creep into the Eastern Bloc. For Honecker, preventing this from happening was a top priority. “We have no intention of letting inflation penetrate the socialist camp,” he told the group. Budget subsidies were the only way to turn flexible and rising import prices into stable and cheap domestic prices, so the fight against world inflation would come at the expense of the state budget.41 Honecker gave the new marching orders to his state planning commissioner, Gerhard Schürer, in early 1975. “The main task,” he said, was to achieve economic growth “by means of intensification”—the socialist term for increases in productivity—and to ensure that “social security is placed at the center of the development of working and living conditions.” Social security meant, “above all, stability of prices . . . implementation of the housing program, preservation and expansion of health care capacities, and safeguarding of the school program.”42 Progress in the land of real existing socialism would go on, Honecker had decided, no matter the consequences.

Progress would also go on in Hungary. In 1972, the Hungarian Politburo had decided on the need to further improve the position of the working class and increase real wages. A capitalist crisis like the oil price shock was not going to stand in the way of this goal. János Kádár told the country in his speech to Eleventh Party Congress in 1975, “Despite the external difficulties it is possible for our national economy to develop in the coming years at approximately the same rate as it has in recent years and for living standards to continue to rise.”43 The party program adopted at the 1975 congress still insisted the final stage of communism could arrive in Hungary in the next fifteen to twenty years.44

The bloc governments’ decisions to leave the social contract untouched in the face of the oil crisis was born of searing historical memories. Gerhard Schürer, the head of the East German State Planning Commission, wrote of the East German leadership, “Since the sugar price increase of June 17th, 1953,”—when price increases had sparked an uprising that was violently suppressed by the Soviet Army—“the fear of price increases on basic goods sat so deep in the bones of policymakers that no one achieved a change.”45 In Poland, dangerous history was much closer at hand—Edward Gierek owed his ascension to the pinnacle of the country to the repeal of the 1970 price increases and the start of his “New Development Program,” which promised workers a better life. In Hungary, Kádár had secured the political acquiescence of the population after the national trauma of 1956 with a single promise: ever-increasing living standards. Gustáv Husák was detested in Czechoslovakia, but after 1968 he drove a similar bargain. Throughout the bloc, higher living standards were the price of social peace.

But if history and politics provided the impetus for stabilizing the social contracts of late socialism, they were not what made it possible. For that, the particular configuration of the global capitalist economy that emerged after the oil crisis was required. In a supreme irony, it was only the development of global finance capitalism that allowed late socialism to exist. Without the explosive growth of global capital markets after 1970, and particularly after 1974, the governing model of late socialism would have been impossible. Had there been no transnational pools of capital on the Euromarkets in the 1970s, or had those pools been more highly regulated and thus less easily accessed, the entire time line of socialism’s denouement would almost certainly have looked completely different. Rather than speaking of the rise of Solidarity in the Polish Crisis of 1980 and 1981, we might instead be writing about a Polish, Hungarian, or East German Crisis of 1974 or 1975.

Günter Mittag, the East German party leader for economic policy, admitted as much in his memoirs. In his words, because in the 1970s “it was regarded as an indisputable axiom that the standard of living should increase, loans were taken out to bridge supply shortages.” Had these loans not been available, the Unity of Economic and Social Policy—the East German name for their policy of raising living standards and expanding social welfare—would have quickly become untenable. Abandoning this policy, Mittag wrote, would have “been a funeral for the GDR in the 1970s.” Upending the social contract would have produced “social conflicts with political consequences, which would probably have affected more than just the former GDR.” In the 1970s, “a possible political destabilization in the GDR through a restriction of social policy was connected with an incalculable political risk. In this respect, the guarantee of economic and social stability was a basic premise of all political action.”46

In the same way, a basic yet unexamined premise of our histories of the last period of the Cold War is the intimate relationship between the globalizing financial capitalism of the 1970s and the fragile stability of late socialism. It was a relationship that quietly underwrote everything from the daily lives of Eastern Europeans, who unknowingly depended on it to put food on their tables and goods in their stores, to the high politics of the Cold War, where it was the prerequisite for détente on the European continent. Its power was really only apparent once it was gone, as it would be in 1980, at which point the broken connection between finance capitalism and late socialism would produce a crisis in Poland that would disrupt both the daily lives of Eastern Europeans and the high politics of the Cold War.

A closer look at the situation of the GDR at the moment the oil crisis struck illustrates this interdependence. Just as the oil crisis was beginning to unfold in November 1973, members of the East German Ministry of Finance produced a projection of the GDR’s sovereign debt out to 1980 if the country maintained its trajectory under the rapidly rising world prices. The results were frightening. The GDR’s debt to the West at the end of 1974 was projected to be 8.7 billion “valuta marks” (VM), the East German accounting unit used for foreign trade and finance and pegged at roughly the value of a West German deutsche mark (DM). This converted to roughly $3.5 billion.47 Even under optimistic hard currency export assumptions, the projection anticipated the hard currency debt growing from VM 12.1 billion in 1975 to VM 25.5 billion, or roughly $10 billion, in 1980. Officials believed such a level of debt would simply not be possible to attain. They estimated that over the entire period of 1974–1980, VM 18 billion of planned borrowing on global capital markets was simply “not financeable.” As they wrote, “All calculations show” that the nation’s economic trajectory “is not viable” because “of the development of the debt and the impossible financing [requirements].” If the debt was to be controlled, they wrote, the social contract would have to be disciplined.48

In its first months, the oil crisis only seemed to make the prospects for substantial Eastern Bloc borrowing worse. As discussed previously, many Western observers did not think the Euromarkets could sustainably manage the process of petrodollar recycling for any period longer than a couple of months.49 This sentiment was immediately and urgently echoed within the East German leadership. In March 1974, there were “fundamental differences of opinion” among the economic leadership on the question of whether “the necessary sources of credit for financing the planned imports of 1975–1980” could be found. It remained an open question because East German bankers had recently been forced to meet existing debt payments by taking out new loans. This was “already a tense goal because the existing sources of credit [were] largely exhausted.” Foreign banks were “increasingly questioning the liquidity of the GDR.” The first months of higher commodity prices had made the availability of credit worse, not better. Markets, it seemed, might force a change in Eastern Bloc domestic policy whether communist leaders wanted one or not.50

Throughout the tumultuous summer of 1974 in the West, the debate over the sustainability of the bloc’s access to global capital markets continued. As the Soviet Union worked to change Comecon oil prices in September, a newly formed group of top economic officials in the GDR discussed a Marxist-Leninist analysis of the Euromarkets that was designated “Top Secret.” In the first section, titled “The Nature of the Eurocurrency Market and Its Risks,” the author detailed how the markets had begun in the late 1950s when surpluses of US dollars ended up in Europe due to the “unrestricted political and economic predominance of US imperialism on the world capitalist market.” Then, in the late 1960s, “objectively acting laws of the capitalist mode of production” such as the “uneven economic development of capitalist industrial states” and “the excessive expenditure of US imperialism on financing its aggressive global strategy” led to a breakup of the Bretton Woods system in 1971. The report reminded the working group that the party had recently decided that “the general crisis of capitalism has reached a new stage” and declared that this conclusion was “fully applicable to the development of the Eurocurrency market.” The upshot was clear: “With its inherent risks, the Eurocurrency market does not provide a long-term basis for financing balance of payments deficits.”51 If this was true, then all bloc states would confront a highly precarious situation. As 1975 approached with Eastern European leaders determined not to let increases in Soviet energy prices lead to a fall in domestic living standards, bankers throughout the bloc had no choice but to test how much money Western capital markets would let them borrow.

To universal surprise, it turned out to be a great deal. Once it became clear that private banks could manage petrodollar recycling on a permanent basis, economic plans across the world that had been deemed “not financeable” in 1973 became eminently so by 1975. The rapid expansion of the Euromarkets that began in 1974 pushed the horizon for living on credit to a level that would have been deemed dangerous and impractical just one year earlier. OPEC nations accumulated a $60 billion current account surplus in 1974. Of this $60 billion, $21 billion was deposited with Eurocurrency banks, and the total assets of the five largest US banks grew at an unprecedented annual rate of 40 percent in 1974.52 Western banks were, in short, flush with cash and eager to find places to put it. The time was ripe for a marriage of convenience, and in 1975, the Eastern Bloc as a whole borrowed more money than they ever had before. Eurocurrency loans to the bloc—the type East German officials had feared would suddenly become scarce—more than doubled from 1974 to 1975, rising from $1 billion to $2.4 billion. Quite literally, the surplus capital generated by a global crisis in capitalism was now funding state socialism’s defense against the global capitalist system.53

Indeed, by the beginning of 1976, the growth of socialist borrowing was so notable that Euromoney magazine, the publication of record for the Euromarkets in the 1970s, put the Eastern Bloc on the cover of its January issue. “It is customary to begin the new year with a backward look,” the lead article noted, “and if we focus on the Euromarkets, the number and nature of Comecon borrowings in 1975 are striking.”54

There was so much Comecon borrowing in 1975 that by early 1976, Western financial and political leaders were beginning to question the bloc’s creditworthiness. The January 1976 Euromoney article noted it was “inevitable” that “the magic” would eventually “go out of lending to Comecon countries.”55 In May, a widely discussed article in Business Week quoted Zbigniew Brzezinski, soon to become Jimmy Carter’s national security advisor, on the political dimensions of the increase in the Eastern Bloc’s debt. “We are dealing with both an opportunity and a threat,” Brzezinski told the magazine in a quintessential expression of the logic of interdependence. “Indebtedness often increases the leverage of the debtor and decreases the leverage of the creditor,” he said. “If a Comecon country defaulted, it could create considerable problems” for Western European banks that had lent out the most money.56 This threat of interdependence was the concern of US secretary of state Henry Kissinger, who warned a gathering of OECD officials in June 1976 of “possible efforts” by socialist states “to misuse economic relations for political purposes inimical” to the West.57

The flurry of commentary in the West caught the ear of officials in the East who were now highly sensitive to changes in global market sentiment. “The capitalist national and international banks,” East German officials wrote in early 1976, “have recently expressed doubts about the creditworthiness of the socialist countries. That was not always so. A few years ago . . . insolvency from a borrower in a socialist country was as unthinkable, for example, as an insolvency from the American automaker General Motors.”58

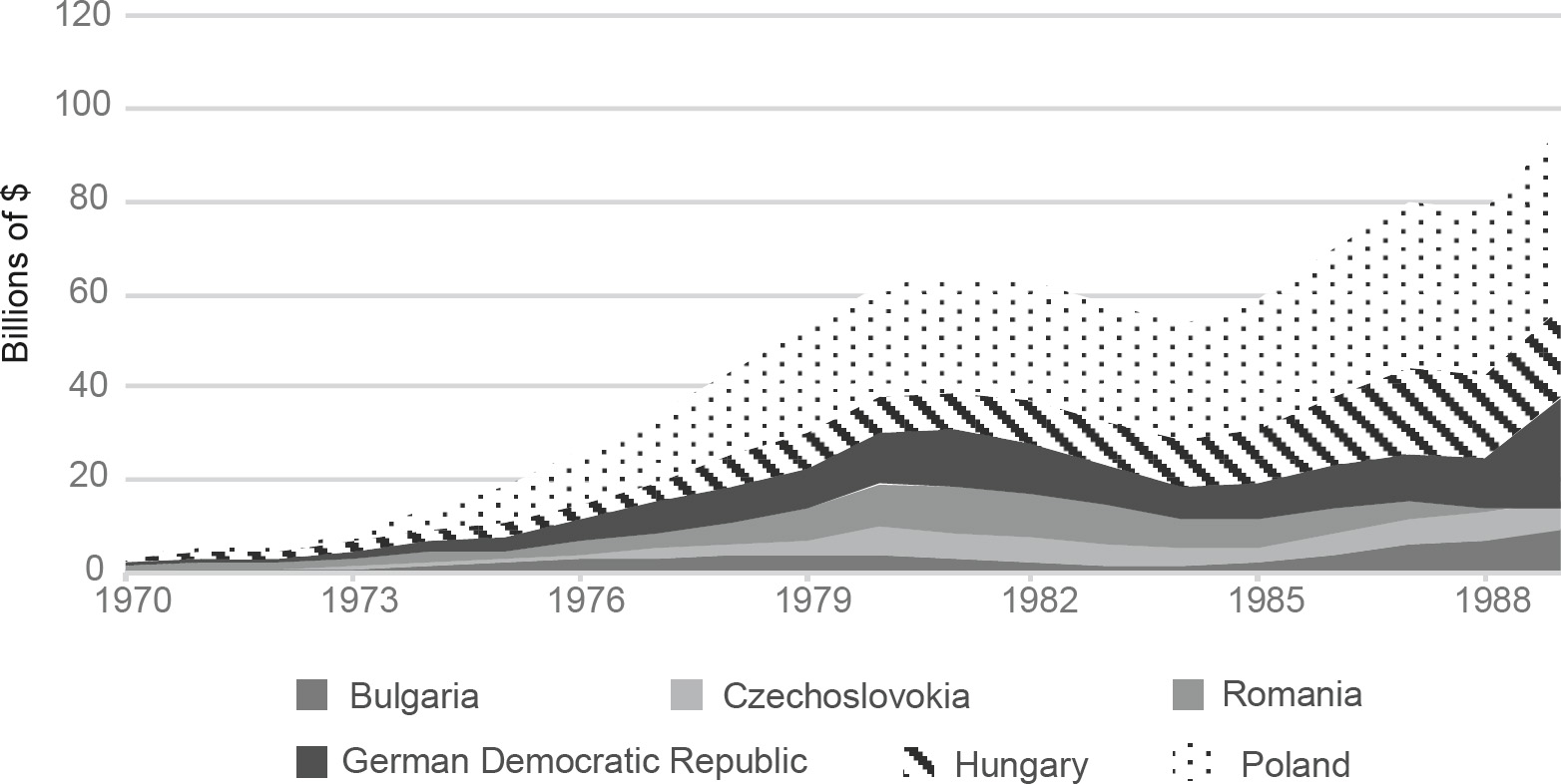

But if the dangers of a Comecon default had become thinkable for both sides by the spring of 1976, that did not stop the banks from lending.59 By the start of 1977, the bloc was once more the star of the Euromarkets and reappeared on the cover of Euromoney. “Any concern over the rapid increase in the level of indebtedness of the CMEA countries has not restricted the volume of lending,” journalists for the magazine wrote. “On the contrary, 1976 was a vintage year.” Banks seemed to agree they had lent Comecon too much, but they couldn’t help themselves from lending more. Eurocurrency credits to the communist world had increased 33 percent in 1976 to $3.2 billion, and there was no end in sight.60 As Figure 1.2 makes clear, the debt burden of the Socialist Bloc would continue to rise through the end of the 1970s and would remain onerous for the rest of the Cold War.

Why did the banks continue to lend? The potent combination of surplus capital and erroneous assumptions pushed their enthusiasm beyond rationality. “On any normal criteria,” one London banker told Euromoney, the Eastern Bloc was “certainly overborrowed.” But banks were not holding the bloc to high standards of creditworthiness “because they’re so flush with funds,” another said.61 Bankers’ confidence in the wisdom of their own cause compounded the enticements of easy liquidity. Citibank CEO Walter Wriston, the leading proponent of the global movement toward sovereign lending in the 1970s, notoriously proclaimed, “Countries don’t go bankrupt.”62

Figure 1.2 Eastern European sovereign debt (net of hard currency reserves) from 1970 to 1990.

Data source: United Nations, Economic Commission for Europe, Economic Survey of Europe in 1990–1991 (Geneva: United Nations, 1991), 250, appendix table C.11.

Above and beyond “normal” capitalist countries, bankers believed socialist countries had three other advantages. First, they had a pristine record of timely payment and had never defaulted on their debts. Second, bankers assumed that socialist states’ authoritarian structure meant they had the “ability to control domestic consumption and investment,” which would put them “in a better position” to exercise “restraint.”63 Unlike capitalist democracies, which promised their citizens too much, socialist authoritarianism was assumed to be adept at implementing austerity. Should that fail, however, bankers saw a strategic reserve behind the Eastern Bloc unparalleled throughout the rest of the global economy—the Soviet Union. Over the course of the decade, they came to believe in what was termed “the umbrella theory,” whereby they anticipated that the USSR would “come to the rescue” of its allies if they ran into financial trouble.64 Under the Soviet umbrella, Eastern Europe seemed safe from financial harm.

On top of favorable ideological and financial structures, a group of very talented communist bankers represented their countries on Western financial markets with aplomb. To read the Western press coverage of these men is to sense the potent mix of intrigue and respect with which Western bankers looked upon their communist counterparts at the time. Standing at the head of this group, and on par with any financial official in the West, was János Fekete, the deputy vice president of the Hungarian National Bank. Fekete had earned his venerable reputation in Western financial circles for accurately predicting a devaluation of the US dollar in 1971 and the global recession of 1974–1975. By the time he was profiled in Euromoney in 1977, the magazine treated his opinions with what verged on oracle-like reverence. There was an entire separate article on the topic of “What Fekete Says About the West,” presumably to help the magazine’s readers glean insight into the future of capitalism from this astute “Marxist economist.” Described as “bespectacled and ebullient,” Fekete told Euromoney that the Eastern Bloc was vastly underborrowed, not overly indebted. “If you take the economic potential of these countries, their debts are ridiculously low,” he said. Playing on the Western notion of an umbrella theory, he seamlessly shifted questions about Eastern Europe’s problems to a discussion of the Soviet Union’s material strength. “In a year, [the Soviet Union] is producing 480 million tons of petrol, it is producing about 300 billion cubic metres of gas, and 700 million tons of coal. It is an enormously strong economy.”65 With such strength in Soviet natural resources, it was implied that the debt of the rest of the bloc hardly mattered. For the time being, Western banks couldn’t help but agree.

If Fekete projected self-confidence, Poland’s Jan Wołoszyn, the first deputy president of Bank Handlowy, the Polish foreign trade bank, projected stately elegance. The same 1977 Euromoney issue described him as a “distinguished, elder statesman of Polish banking who would look equally at home in the boardroom of any bank in the West.”66 Bankers had nothing to fear with “Mr. Poland,” a later profile concluded. Wołoszyn was “credible, knowledgeable, and . . . impressive,” had never joined the Polish communist party, and had thought more than once about leaving banking for more leisurely bourgeois pursuits, gardening foremost among them. “This is a people business,” bankers reported to Euromoney, and Wołoszyn was “the one who, through his own charisma, standing, and personality, persuades many banks to lend to Poland.”67

In East Germany, two men, Werner Polze and Horst Kaminsky, ran the country’s public financing efforts on the Euromarkets. Both men went about their business in the West without the fanfare of Fekete or Wołoszyn. After the Cold War, their actions receded further into the background in Germany after the revelation that another man—Alexander Schalck-Golodkowski, known simply as Schalck—had been running an organization within the East German government called Kommerzielle Koordinierung. KoKo, as it was referred to, was charged with creating hard currency for the East German state using any means available. From the late 1960s to the collapse of the state in 1989, this mission led KoKo into all manner of activities, including currency and commodity speculation, hotel management, consumer goods stores, garbage disposal services for West Berlin, and weapons sales to developing countries. Along the way, Schalck became one of the most important people within the East German leadership because he was the state’s chief negotiator with West Germany on all financial matters.

And there was a great deal to negotiate. After the launch of Willy Brandt’s Ostpolitik in the late 1960s and the signing of the Basic Treaty normalizing relations between the two German states in 1972, the West German government began to use its financial resources as a tool of its détente policy. East Germany was granted access to a “swing” credit with West German banks, under which it could borrow deutsche marks without interest up to a negotiated limit, which ranged from DM 500 million to DM 800 million in the 1970s and 1980s. Bonn also made an annual transportation payment to the GDR that was ostensibly for the maintenance of the roads running between the Federal Republic and West Berlin but was, in fact, free for the East Germans to use as they pleased. Most spectacularly of all, the Federal Republic began buying East Germans’ freedom, transferring increasing sums of money to the East German government in exchange for the release of dissidents (and eventually many others) to the West. Schalck played a role in all these negotiations while still organizing KoKo’s varied commercial activities, so his influence within the East German hierarchy steadily grew over the last two decades of the Cold War. Once the Berlin Wall fell, the public revelations of KoKo’s dubious activities led many in the newly reunited Germany to label Schalck “public enemy #1.”68

The East German situation was an especially vibrant example of how the politics of détente further eased the reigns on sovereign lending beyond their already lax hold. Gierek’s regime in Poland proved particularly adept at using Western governments’ interest in better relations with the Eastern Bloc to unlock Western state coffers. Each US president in the 1970s—Nixon, Ford, and Carter—visited Poland under the banner of détente, and each time they landed in Warsaw, they brought with them increases in US government loan guarantees as a sign of goodwill and a means of boosting US exports.69 In 1975, on the sidelines of the meetings to sign the Helsinki Accords, Gierek and West German chancellor Helmut Schmidt signed an agreement granting Warsaw a “jumbo credit” of DM 500 million in exchange for the Polish government’s willingness to let its German minority emigrate to the Federal Republic.70 In Romania, Nicolae Ceauşescu parlayed his reputation for independence from Moscow into membership in the International Monetary Fund in 1972, which, in turn, helped his country gain broader and cheaper access to Euromarket credit. The Kádár government in Hungary generally refrained from using détente to gain politically motivated credits from Western governments, but it nevertheless used its reputation in the West as the most liberal and reform-minded country in the bloc to great financial effect.

Even if the question of access to Western credit markets turned out to be surprisingly easy for Eastern Bloc states to solve, the question of how to use the borrowed capital proved infinitely vexing. Every foreign borrowing strategy in the Eastern Bloc was at least officially premised on a single idea: using the hard currency to import Western technology, modernize domestic production, and develop industries capable of producing exports to the world market that would earn enough hard currency to pay off the loans.71 In Poland, for instance, Gierek’s New Development Strategy had augmented the country’s traditional export strengths in copper and coal with new hard currency investments in heavy industry, chemicals, aircraft, construction equipment, and auto parts on the assumption that these industries would produce exportable goods by the end of the decade. In East Germany, planners had funded a massive expansion of the petrochemicals industry in the late 1960s and early 1970s to take advantage of growing Soviet energy supplies to produce more exports of refined petroleum products to the West. In each case, some of the imported capital made it all the way to improving the quality of Eastern European factories and production processes, but much of the rest merely presented rampant opportunities to expand domestic corruption and patronage networks.

More importantly, the decision to base long-term development on future exports to the world market broke an important barrier between Comecon and the rest of the world economy. In order to win in global export markets, Eastern Bloc countries would have to compete with the developing countries of Latin America and East Asia to sell their goods in the developed West. This competition subjected Eastern Bloc goods to direct competition with capitalist goods and pitted socialist methods of production against the capitalist methods the bloc had long eschewed. Implicit in the Eastern Bloc’s choice to borrow on global capital markets was also the choice to compete on global trade markets.

It was a competition the bloc would lose time and again in the 1970s. Despite constant exhortations from the very top of each state’s governing structure about the importance of increasing exports and eventually producing hard currency trade surpluses, the Eastern European members of Comecon (excluding the Soviet Union) ran a cumulative hard currency trade deficit from 1970 to 1977 of roughly $26 billion.72 Eastern Bloc officials liked to blame their inability to increase exports on the slow growth and high inflation of Western economies as well as discriminatory Western trade policies that prevented their goods from reaching Western consumers. But the reality was that they simply were not producing goods Westerners wanted to buy. “While the world economy is based partly on a socialist and partly on a capitalist social system,” Fekete would write in 1982, “there are not two world markets, there are no ‘capitalist and socialist’ machines and products, but only good or bad machines, modern or obsolete products.”73 By the late 1970s, the Eastern Bloc was most assuredly producing flawed obsolescence. And if the trade surpluses required to pay back the debt could not be created through increases in exports, they would need to be created through decreases in imports. That, in turn, meant only one thing: the challenge of austerity lurked just around the corner.