Chapter 12

Monika Kozłowska-Szyc

Credit was of great importance in the economic life of the early modern period. It played a special role in urban circumstances, hence trade economy developed there best. It was applied for consumption, as well as in investments and commodity exchange. The credit market functioning in small Podlasie towns, however, largely served private needs. The objective of this chapter is to show and discuss the phenomenon of credit in a small private town, which is the case of Białystok. Determining the size and the structure of turnovers, the duration of agreements as well as the way of their securing will allow us to outline the rhythm of the economic life of the urban centre under analysis and will help to determine the degree of its economic development. The analysis was based on the oldest preserved municipal registers. The material was complemented with promissory notes and documents kept in the Roskie Archives and the Branicki Archives. All the used archive records reside in the Central Archive of Historical Records in Warsaw (Księgi miejskie białostockie, 1744–1795; Archiwum Roskie, 1737–1794; Archiwum Branickich z Białegostoku, 1786).

Located at the borderline between the Crown of the Kingdom of Poland and the Grand Duchy of Lithuania, Białystok was one of larger urban centres in Podlasie (beside Tykocin and Bielsk Podlaski). In the 18th century, it had c. 2,500 residents, 41% of which were Christians, 35.5% Jews, and 23.5% soldiers (Łopatecki 2015, p. 351; Dobroński 2001, p. 38). It is important to emphasise that such small towns dominated in the landscape of the Polish-Lithuanian Commonwealth, hence they constituted over 90% of all urban centres of old Poland (Bogucka & Samsonowicz 1986, pp. 379–82). What is also worth noting is the fact that Białystok was the headquarters of the Podlasie latifundium of the Branicki family. The town emerged as a base of a magnate seat and formed along with the development of the landlord’s manor. The development of such centres made up a characteristic quality of the modern era not only in the Polish-Lithuanian Commonwealth but also throughout Europe. However, residential towns in Poland differed from those in Western Europe by the fact that they were not a monarch’s work but the magnates’ (Stone 2001, p. 298; Bogucka 2001, p. 23; 2009, p. 18).

The Branicki family, as the owners of Białystok, had almost unlimited possibilities to intervene in all areas of life in the town. They were also of great importance on the Podlasie credit market. The most affluent residents of towns and estates belonging to the Branickis deposited their funds at Jan Klemens Branicki and Izabela Branicka, as well as people being at the top of the court hierarchy (Łopatecki & Kupczewska 2016, p. 490). Moreover, they had instruments controlling the local credit market. Through their officials they issued regulations limiting the opportunity of taking loans by the troops stationing in Białystok (Łopatecki 2015, p. 356), or permits allowing the local Jewish communities to run credit operations (Leszczyński 1980, p. 80). Moreover, the Branicki family created new town offices at their discretion: one of them was the position of governor, among whose tasks was, among other things, making sure that the properties of people who were not able to pay off debt claims were auctioned (Sztachelska-Kokoczka 2009, p. 21).

However, it was lack of bank institutions, where burghers, especially those more affluent, could take a loan or deposit their property, that affected the development of mutual loans at interest. A considerable role in the development of credit-monetary operations was primarily played by the Jewish population (Leszczyński 1980, pp. 188–202). It was the Jewish religious communities (kahal) that offered fringe banking services where not only burghers, but also neighbouring nobility and clergy lodged their money (Samsonowicz 1981, p. 128). The financial activity of Jewish communities had also its disadvantage: excessive liabilities of the kahal in the 18th century resulted in its insolvency and the necessity of the intervention from the dominion power (Dubnow 2001, p. 293). According to specification of liabilities presented in 1795, the Białystok kahal was in debt for almost 12,000 zlotys. It seems, however, that the liabilities could be much higher. The insolvency of the Białystok kahal was no exception; the community in nearby Tykocin struggled much more serious financial problems:1 its debt of the mid-18th century is estimated for c. 90,000 zlotys; and also in Cracow (c. 508,000 zlotys), Lvov (438,000 zlotys) or Poznan (403,000 zlotys) (Leszczyński 1994, p. 141). It is estimated that the sum of Jewish communities’ liabilities in the Polish-Lithuanian Commonwealth reached even 2.5 million zlotys (Stone 2001, pp. 306–7).

The first stage of the analysis of the Białystok credit market is examining the issue of the frequency of records. From the preserved documents records referring to loan agreements, we managed to extract reports for the appraisal of pledged properties or liabilities recorded in testaments. The most transactions were noted in the 1770s and 1780s but the most sources come from that period. It is also important to emphasise the fact that only part of credit turnover can be found in the preserved books. Not all transactions were recorded in the files. The evidence thereof is the part of the records which refer to the debts which were not paid off on time and include the reports for the appraisal of pledged movables. Moreover, recording a particular transaction in court registers was connected with the necessity of notary fees. Thus, it could happen that the notary costs connected with recording the promissory notes in the files were equal or higher than the amount of liabilities; therefore, such transactions were not recorded in municipal books. It is also important to remember that part of Białystok merchants’ liabilities could have been recorded in court books of other urban centres, for example, those where their business partners came from. Therefore, a full reconstruction of the credit market is impossible but the following analysis allows for general orientation in the scale and the nature of the phenomenon.

An important element in studies on economy is the analysis of the concentration of a particular phenomenon within particular wealth groups (as can be seen in Table 12.1). Unfortunately, for 6% of the transactions, we have no information of the amount of the credit agreement. The data presented in Table 12.1 demonstrate that even 67.8% of the value of all loan agreements was concentrated in the hands of a small group of people (9% of cases). In Białystok, credit turnover numerically dominated small transactions (up to 50 zlotys: 41%) but their value was a margin of the turnover (1.8%). Also, debts of 51–100 zlotys had little share in the market (2%). Also medium-value loans (101–500 zlotys) were popular: their value made 13.4% of the whole credit turnover. The highest interest was attracted, however, by transactions up to 100 zlotys: they made up jointly 52% of the number of all contracts, and their value did not exceed 4% of the total.

Table 12.1 The structure of the value of credit market turnover in Białystok in the second half of the 18th century

|

Value (in Polish zlotys) |

Up to 50 |

51–100 |

101–500 |

501–1000 |

Above 1000 |

Unknown value |

Total |

|

Number of transactions |

108 |

29 |

64 |

23 |

25 |

15 |

264 |

|

Value of transactions |

2,142 |

2,400 |

15,991 |

18,007 |

81,115 |

– |

119,655 |

|

% of the number |

41 |

11 |

24 |

9 |

9 |

6 |

100 |

|

% of the value |

1.8 |

2 |

13.4 |

15 |

67.8 |

– |

100 |

A certain facilitation in determining the weight of a particular debt is becoming familiar with the purchasing power of the money the local burghers traded in the 18th century. To illustrate this phenomenon, I will use, for example, prices of real estates in Białystok. For 100 zlotys, one could purchase the cheapest wooden house, a place of average value cost c. 300 zlotys, whereas the most expensive brick houses were worth even a few thousand zlotys (Kozłowska 2017b, p. 111). Simultaneously, wages of construction workers (builders, carpenters) available in the sources were 250 zlotys per year (Kozłowska 2017a, p. 210).

In Białystok, like in other Podlasie towns, petty consumption loans dominated, although there was also big credit. However, its share in the general market structure was quite small. Higher sums were mainly connected with big commerce and goods purchase and sale transactions. An example of such a loan is a series of credit transactions resulting from founding a trade company by Paliter Dawidowicz (a Białystok merchant and broker) as well as Jan Aleksander Lindsay (a major of an infantry regiment of the Grand Crown Buława). In the years 1761–1762, Dawidowicz, with a surety from Lindsay, borrowed altogether 5,425 zlotys, which allotted for a purchase of goods in Torun (Archiwum Roskie 1737–1794). It is important to bear in mind, however, that Podlasie towns were not considerable trade centres; like other towns of that rank, they were places of exchange of agricultural produce, craft products, as well as commodities brought by local merchants (Oleksicki 1985, p. 51; Sztachelska-Kokoczka 1992, pp. 101–10). In the scale of the whole region, Jewish merchants from Tykocin had the largest shares in trade turnover (Wroczyńska 1995, p. 27).

The analysed credit agreements show that the loans were provided mainly by the people with Polish-sounding family names: they constituted c. 51.5% of the creditors. Many of them also incurred liabilities (they made up 51% of debtors). A quarter of all credit transactions took place within the population of Polish-sounding family names. They were largely petty loans, sometimes of just 4 zotys, even though we find also manifold higher liabilities, of over 300 zlotys.

Also Białystok Jews lent money: they made up 31% of all creditors in the contracts recorded in town books. However, we can suppose that their real share in the credit market was considerably higher, since certain Jewish transactions were recorded in kahal books, which have not survived. There must have gone primarily credit agreements between the Jews. Like in other Podlasie towns (Tykocin, Goniądz, Kleszczele or Orla), providing loans at interest was the fundamental source of income of many members of the Białystok Jewish community (Leszczyński 1980, p. 190). Source records also fail to indicate that Jewish bankers or merchants in Podlasie lent money to the clergy, which happened several times in other Polish towns (Morgensztern 1967, pp. 6–7; Hanejko 2011, p. 148). On the contrary, the Jews were debtors of numerous church institutions (Hundert 2006, p. 77). The Jews also often used money credit at the burghers. However, it is important to point out that the Jewish legislature attempted to reduce opportunities of borrowing money from Christians. From 1673 onwards, in Poland (from 1670 in Lithuania), the Jews had to abide by the so-called credit chazoka, which meant that if a Jew wanted to incur a debt from a Christian, he had to receive the kahal’s permission. The chazoka was primarily expected to protect from reckless indebtedness; it was also a security for Jewish communities from executions which threatened them because of the collective responsibility of kahals for a bankruptcy of its every member (Leszczyński 1980, pp. 194–5; Pogonowski 1998, pp. 78–9). It seems, however, that those provisions were not always applied. In town books, we find many petty as well as more serious loans taken by the Jews. The debtors of the Christians were, for example, merchants and the kahal. For instance, Wolf Gołda, a rich merchant of long distance trade, owed to many Christian creditors a considerable amount of nearly 11,609 zlotys (Księgi miejskie białostockie, 1744–1795). Moreover, the Jews also incurred money liabilities from the town owner. In 1795, the Białystok kahal took a loan of 2,344 zlotys from Izabela Branicka, which allocated for paying off their outstanding debts (Archiwum Roskie, 1737–1794).

An inseparable component of loan turnover was a profit taken from the transactions by the creditors. Unfortunately, the interest was seldom mentioned in credit agreements. However, even on the basis of a few agreements including such data, we may calculate that debtors paid on average 8% of interest a year from the borrowed sum (the lowest interest rate was 5%, the highest rate: 12.5%). It is a relatively high interest rate, also in reference to the state legislature of those days. The Sejm Constitution (act of law) of 1775 introduced limitations on credit transactions which should not have a higher interest rate than 5% a year (Volumina legum, 1860, pp. 112–13). In other Podlasie towns (Tykocin, Orla, Bielsk), an annual interest rate ranged from 6% to even 10% (Leszczyński 1980, p. 198). A similar profit from providing loans was also noted in other Polish towns. For instance, in a small Małopolska private town of Tomaszów Lubelski, in most cases, the interest from the loan was 7–8% (Hanejko 2011, p. 148). On the other hand, in the royal town of Nowy Sącza at the turn of the 17th century, an annual interest rate reached 10% (in the case of the loans secured by the pledge of a real estate even 10–15%) (Dunin-Wąsowicz 1967, pp. 65, 72). A lower interest rate was noted, however, in the towns and regions connected with foreign and long-distance trade. For instance, in the 17th-century Toruń, 6% of interest was paid from the loan taken (the rate ranged between 4% to maximum 8%) (Mycio 1999, p. 65). On the other hand, in Żuławy Wiślane at the turn of the 18th century, burghers and peasants paid not more than 8.5% of interest, and in the 18th c. even 3% (Szafran 1985, p. 198). The aforementioned data show that the loan interest rate in the Commonwealth was higher than in the countries of Western Europe. For instance, in France, Portugal, and England, the interest rate reached maximum 5% annually (Dermineur 2018, pp. 209, 226; Costa, Rocha & Brito 2014, pp. 17–18). The reasons for this discrepancy were different; among them, we can count a weak development of credit instruments in Polish towns, lack of bank institutions, a higher risk of not receiving the money back, or different purposes of the loan.

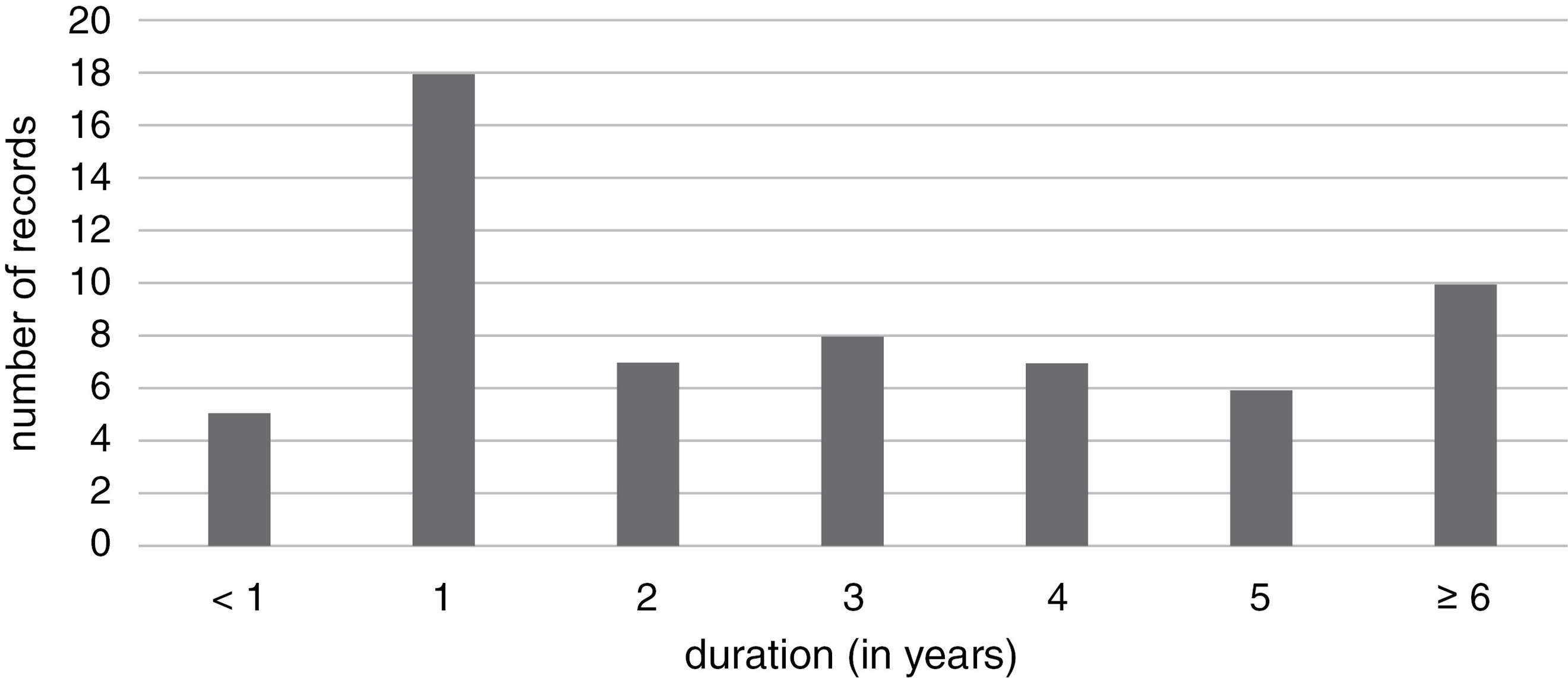

Figure 12.1Credit agreements by duration (in years) in Białystok, the second half of the 18th century.

Another important issue is the duration of loan agreements, which can be divided into short-term ones (lasting a year or shorter) and long-term ones (see Figure 12.1). Not in all cases, unfortunately, the source provides the duration of the loan agreement and we know the time for paying off the debt only in 23% of contracts. Burghers usually concluded agreements for a one-year period. It also observable that 62% of all credit contracts under scrutiny lasted more than a year. This is, however, a result of more frequent recording in town books – transactions not paid on time. In the case of such arrears, one of three possible solutions were applicable: the deadline was prolonged on the original conditions, or the time of contract was prolonged with sharpened contract conditions, or part of the debtor’s property (commensurate with the scale of the debt) was taken over. Sometimes the debt was paid off in instalments. This phenomenon is, however, difficult to grasp, since the Białystok town books hardly ever noted payments of particular instalments. We usually learn about such operations only in reference to the return of the last part of the debt and the mutual acknowledging of the payment by both parties. With such a small number of cases, it is impossible to determine the dependencies between the number of instalments and the amount of the debt, as well as to answer the question, if spreading the payment over several parts affected the duration of the loan agreement, even though we can suppose that both tendencies known from other credit markets also occurred in Białystok. Moreover, we did not observe a mutual dependence between the amount and the duration of the credit transaction, which may result from too small a source basis.

It is also difficult to establish an exact date of incurring and paying off the liabilities, since a considerable part of the records concerns reporting for appraisal of pledged movables for debts not paid in due time. Moreover, certain records also include claims from previous periods. It seems, however, that loan agreements were mainly concluded in the period from April to June, which was connected with deficiencies of food and cash. The arranged day of payment often fell on the period of St John the Baptist fair. It was the greatest Białystok fair, organized on the name day (patron saint’s day) of the town order (Sztachelska-Kokoczka 1992, p. 105; Grochulska 1973, p. 802).

All types of credit operations are connected with a risk of losing the lent money. Therefore, different methods of insuring loan agreements were developed. In the case of Białystok, 32% of transactions, beside a promissory note itself, a loan agreement, a bill of exchange, or a record in court books, was additionally secured by the pledge of movables and immovable property. The most often collaterals in Białystok were man’s and woman’s clothes (kontusz, żupan, skirts, vests, hats, pants, kerchiefs, belts, frock coats). Debt collaterals were also everyday objects (e.g. dishes, bowls as well as tin plates, spoons and knives, a brass iron, a silver jug, mugs). On the other hand, guarantees based on immovable properties as well as all possessions were mainly granted by the Jews, more rarely by the Christians. If the debtor was the kahal management, the whole community collectively guaranteed the loan. Moreover, such items as a violin, four pictures framed in glass, a military saddle, a clock, French pistols, or liturgical utensils were left to the debtors. The creditor could sell the items being a collateral of a loan agreement in the event of a default in due time. In this case the creditor should report the items for appraisal in the town office. They were assessed by an expert in a particular field (for example, clothes were priced by a tailor, a wooden house by a carpenter). After the appraisal the town authorities called the debtor for paying off the liability and buying out the pledge, usually within 30 days. In the event of the appraisal of the pledged items above the amount of the debt the creditor, having sold the items, should return the surplus to the office. If the collateral was assessed below the value of the debt, the creditor suffered a loss. It also happened that the town court, after the appraisal of the pledge, ordered the debtor to work off the missing part of the debt. Records in the preserved town books also show that certain Jews ran pawnshop activities in Białystok.

Knowing the ways of securing the loan, it is also important to investigate the amounts of loans reached in each of the distinguished groups of collaterals (see Table 12.2). It is clearly visible that the amount of collateral depended on the amount of the incurred debt. Petty debts were guaranteed by pledging clothes and other movables (up to 100 zlotys). Those slightly higher were secured on immovable property, usually land. High loans were insured by a record referring to the whole property. The situation was similar in other Podlasie towns. In Tykocin, considerable sums were secured on all types of immovable property (houses, plots of land, breweries). Smaller ones were guaranteed by different objects. Sometimes a collateral was even livestock: for example, in Goniądz, the loan collateral was a calf (Leszczyński 1980, pp. 192, 199).

Table 12.2 Value of debts incurred in Białystok in the second half of the 18th century by an additional way of their securing (arithmetical average)

|

Type of collateral |

Number of records |

Average value of the loan |

|

Property |

12 |

577 |

|

Land |

7 |

136 |

|

Clothing |

37 |

29 |

|

Everyday objects |

4 |

67 |

|

Clothes and everyday items |

12 |

60 |

|

Indefinite items |

7 |

93 |

|

Others |

6 |

56 |

The analysis of the oldest Białystok court books indicates that an important manifestation of economic activities of the burghers was credit operations. Loans were used not only in the turnover of commodities and investments but, primarily, for consumption purposes. The Białystok credit market was largely based on small value contracts (up to 100 zlotys), usually incurred for a one-year period, although most of transactions had no payment deadline. A considerable part of liabilities was also additionally secured by a collateral, the value of which depended on the amount of the debt. It is also important to note that the development of credit-monetary operations of the town under scrutiny was considerably affected by the Jews, who, according to data in the preserved sources, constituted at least 31% of all creditors, even though their real share in the market, perhaps much more considerable, is difficult to determine because of the lack of preserved kahal books. Despite the growth of the number of recorded transactions from the 1770s onwards, on the Białystok credit market there is no sign of modernization processes, so visible in, for example, Warsaw (Łozowski 2018, pp. 177–78), and the vast majority of transactions belong to the sphere of traditional private credit, the recognition of which should be one of the priorities of Polish economic historiography. Small towns like Białystok constituted the vast majority of urban entities in the Commonwealth but the evaluation of their economic life standard requires specific studies, which are still missing.

Note

1Tykocin, like Białystok, was a private town belonging to the Branicki family. In the 18th century, it had c. 3,000 inhabitants, 51.7% of whom were Christians and 48.3% Jewish (Kusiński 1966, p. 272, Choińska 2009–2010, p. 38). The Jewish community in Tykocin was the fifth largest community in old Poland and supervised c. 50 neighbouring settlements in Podlasie. In 1771, as a result of the intervention of dominion power, it transferred the supervision of those villages and towns to the younger Białystok kahal (Kaźmierczyk 2002, p. 148; Rogalewska 1995, p. 17).

References

Archiwum Branickich z Białegostoku. (1786). Warsaw: The Central Archives of Historical Records. 48.

Archiwum Roskie: akta osobisto-rodzinne i majątkowo-prawne (1737–1794). Warsaw: The Central Archives of Historical Records. 628, 633, 634, 636.

Bogucka, M. (2001). Miasta a władza centralna w Polsce i w Europie wczesnonowożytnej (XVI–XVIII w.). Warszawa: Wydział I Nauk Społecznych PAN.

Bogucka, M. (2009). Miasto i mieszczanin w społeczeństwie Polski nowożytnej (XVI–XVIII wiek). Czasy Nowożytne, 22, pp. 9–49.

Bogucka, M. & Samsonowicz, H. (1986). Dzieje miast i mieszczaństwa w Polsce przedrozbiorowej. Wrocław: Zakład Narodowy im. Ossolińskich.

Choińska, M. (2009–2010). Powinności mieszczan w mieście królewskim a w mieście prywatnym: przykład Tykocina w XVI–XVIII wieku. Studia Podlaskie, 18, pp. 7–110.

Costa, L. F., Rocha, M. M. & Brito, P. (2014). Money Supply and the Credit Market in Early Modern Economies: The Case of Eighteenth-Century Lisbon. Lisboa: Gabinete de História Económica e Social.

Dermineur, E. M. (2018). Rural Credit Markets in Eighteenth-Century France: Contracts, Guarantees and Land. In Briggs, Ch. & Zuijderduijn, J., eds. Land and Credit: Mortgages in the Medieval and Early Modern European Countryside. Basingstoke: Palgrave Macmillan, pp. 205–31.

Dobroński, A. (2001). Białystok – historia miasta. Białystok: Zarząd Miasta.

Dubnow, S. M. (2001). History of the Jews in Russia and Poland 1: From the Beginning until the Death Of Alexander I (1825). Skokie: Varda Books.

Dunin-Wąsowicz, A. (1967). Kapitał mieszczański Nowego Sącza na przełomie XVI/XVII wieku. Wpływ na ekonomikę miasta i zaplecza. Warszawa: Państwowe Wydawnictwo Naukowe.

Grochulska, B. (1973). Jarmarki w handlu polskim w drugiej połowie XVIII wieku. Przegląd Historyczny, 64(4), pp. 793–821.

Hanejko, E. (2011). Miasto w okresie od wielkiego sporu o Ordynację do I rozbioru Polski. In Szczygieł, R., ed. Tomaszów Lubelski. Monografia miasta. Lublin–Tomaszów Lubelski: Tomaszowskie Towarzystwo Regionalne, pp. 127–215.

Hundert, G. D. (2006). Jews in Poland-Lithuania in the Eighteenth Century: a Genealogy of Modernity. Berkeley: University of California Press.

Kaźmierczyk, A. (2002). Żydzi w dobrach prywatnych w świetle sądowniczej i administracyjnej praktyki dóbr magnackich w wiekach XVI–XVIII. Kraków: Księgarnia Akademicka.

Kozłowska, M. (2017b). Rynek obrotu nieruchomościami w Białymstoku w XVIII wieku. Studia Podlaskie, 25, pp. 103–27.

Kozłowska, M. (2017a). Rynek kredytowy w XVIII-wiecznym Białymstoku w świetle analizy ksiąg miejskich. Roczniki Dziejów Społecznych i Gospodarczych, 68, pp. 199–222.

Księgi miejskie białostockie. (1744–1795). Warsaw: The Central Archives of Historical Records. 1, 2, 3.

Kusiński, W. (1966). Przemiany funkcji Białegostoku w przeszłości. Rocznik Białostocki, 6, pp. 267–96.

Leszczyński, A. (1980). Żydzi Ziemi Bielskiej od połowy XVII w. do 1795 r. (studium osadnicze, prawne I ekonomiczne). Wrocław: Zakład Narodowy im. Ossolińskich.

Leszczyński, A. (1994). Sejm Żydów Korony 1623–1764. Warszawa: Żydowski Instytut Historyczny w Polsce.

Łopatecki, K. (2015). Ustrój XVIII-wiecznego miasta Białystok. Miscellanea Historico-Iuridica, 14(1), pp. 349–79.

Łopatecki, K. & Kupczewska, M. (2016). Dyspozycje majątkowe Izabeli z Poniatowskich Branickiej na wypadek śmierci. Kwartalnik Historii Kultury Materialnej, 64(4), pp. 485–93.

Łozowski, P. (2018). The Social Structure of the Real Estate Market in Old Warsaw in the Years 1427–1527. Economic History of Developing Regions, 33(2), pp. 147–82.

Morgensztern, J. (1967). Operacje kredytowe Żydów w Zamościu w XVII w. (wierzytelności I zadłużenia). Biuletyn Żydowskiego Instytutu Historycznego, 64, pp. 3–32.

Mycio, A. (1999). Formy kredytu mieszczańskiego na początku XVII wieku w świetle ksiąg ławniczych Starego Miasta Torunia. Rocznik Toruński, 26, pp. 55–70.

Oleksicki, A. (1985). Socjotopografia Białegostoku w XVIII w. w świetle inwentarza miasta z 1771/72 I planu Beckera z 1799 r. In Majecki, H., ed. Studia i materiały do dziejów miasta Białegostoku, 4. Białystok: Białostockie Towarzystwo Naukowe, pp. 41–56.

Pogonowski, I. (1998). Jews in Poland: A Documentary History. New York: Hippocrene Books.

Rogalewska, E. (1995). Rozwój giny żydowskiej w Tykocinie. In Rogalewska, E., ed. Żydzi tykocińscy 1522–1941. Tykocin: Towarzystwo Przyjaciół Ziemi Tykocińskiej.

Samsonowicz, H. (1981). Początki banków prywatnych w Polsce. Sobótka, 36(1), pp. 127–38.

Stone, D. Z. (2001). The Polish-Lithuanian State, 1386–1795. Seattle: University of Washington Press.

Szafran, P. (1985). Kredyt na Żuławach Gdańskich w XVII-XVIII wieku. Rocznik Gdański, 45 (1), pp. 139–48.

Sztachelska-Kokoczka, A. (1992). Handel w miastach dóbr podlaskich Jana Klemensa Branickiego. In Dubas-Urwanowicz, E. & Urwanowicz, J., ed. Miasto, region, społeczeństwo. Studia ofiarowane profesorowi Andrzejowi Wyrobiszowi w sześćdziesiątą rocznicę Jego urodzin. Białystok: Dział Wydawnictw Filii UW, pp. 101–10.

Sztachelska-Kokoczka, A. (2009). Białystok za pałacową bramą. Białystok: Urząd Miejski.

Volumina legum: vol. 8 (1890). Petersburg: Jozefat Ochryzko.

Wroczyńska, E. (1995). Rozwój żydowskiego osiedla w Tykocinie do końca XVIII w. In Rogalewska, E., ed. Żydzi tykocińscy 1522–1941. Tykocin: Towarzystwo Przyjaciół Ziemi Tykocińskiej.