FIVE

From the peak of the cycle in the summer of 1929 to the bottom of the depression in March 1933, the stock of money—currency and demand deposits—fell by 28 percent and industrial production fell by 50 percent. The sizable declines in the two series merit attention not only because the social consequences of the decline in output were large and pervasive, but because the policies pursued during the period and the justification of them provide considerable evidence about the framework that guided Federal Reserve policy and the response of the Federal Reserve to a crisis.

This chapter gives special attention to the Federal Reserve’s response to the contraction, considers some previous explanations of its actions and inaction, and uses the history of the periods and the statements of participants to discriminate among alternative explanations of Federal Reserve behavior. Inevitably, this leads to a central issue about the 1929–33 decline: why the decline was so severe. There is no doubt that early in the decline the Federal Reserve knew a major contraction was under way. Whatever its causes, monetary policy could have lessened the decline. At issue here is why it failed to do so.1

The chapter does not attempt to resolve the more difficult problem of assessing the relative contribution of nonmonetary factors to the start of the Great Depression. It is now generally accepted that the depth of the depression, its duration, and its spread through the world economy are mainly the result of monetary actions or inactions. Warburton (1966), Friedman and Schwartz (1963), and at an earlier date Currie (1934) highlighted the role of monetary forces in the United States. More recent work by Eichengreen (1992) and Bernanke (1994) accepts the role of money and concentrates on the international character of the decline and the influence of the international gold standard. Agreement is limited, however. There are several different, and at times conflicting, explanations of the severity of the decline.

DIFFERENT INTERPRETATIONS

Following Bernanke (1994) and Mishkin (1976), several authors have revived a version of Irving Fisher’s (1933) debt-deflation explanation of the severity of the Great Depression.2 These authors supplement the monetary explanation by highlighting the role of capital market imperfections resulting from differences in borrowers’ net worth. Borrowers with relatively low net worth face more restricted opportunities to borrow, so they depend more on banks. As firms’ net worth fell during the depression, banks refused additional loans. Also, bank failures removed the principal lenders for businesses with moderate net worth. On this explanation, bank failures contributed to the depression not only by reducing the money stock, as claimed by Currie (1934), Warburton (1966), and Friedman and Schwartz (1963), but by raising the cost and availability of loans more than would have occurred based on the monetary and credit contraction resulting from Federal Reserve policies.

Friedman and Schwartz (1963, 407–19) attributed the Federal Reserve’s behavior in the early thirties to the death of Benjamin Strong in 1928 and the shift of power from the Federal Reserve Bank of New York to other parts of the System. George L. Harrison, who replaced Strong as governor of the New York bank, lacked Strong’s ability to organize and lead other members of the open market committee. In this interpretation, the period is unique not only because of the severity of the contraction but because the Federal Reserve behaved as it had not behaved earlier and should not be expected to behave again.

In his history of the interwar gold standard, Barry Eichengreen (1992) revived the idea that lack of central bank cooperation, the workings of the interwar gold exchange standard, and the requirement that Federal Reserve notes be backed 40 percent by gold produced and prolonged the decline. Lack of cooperation weakened the operation of the interwar gold standard Eichengreen (1992, 213). Cooperation would have enhanced the credibility of the System by encouraging speculators to believe that gold parities would be defended with the help of foreign central banks (xi, 257, 390). Monetary contraction in the United States and a decline in its international lending in 1928 put unsupportable strain on a fragile system, necessitated contraction in many countries, and “set the stage for the 1929 downturn” (392).3 Gold stocks were most heavily concentrated at the Bank of France and the Federal Reserve, but even these banks “had very limited room for maneuver” (393).

Elmus Wicker (1966, ix, 155, 195) attributed the Federal Reserve’s failure to its incomplete understanding of how monetary policy influenced economic activity and the price level. The Federal Reserve Board and the governors of the reserve banks were confused and misled by their interpretation of the events they watched. Power within the System was so diffused that leadership from New York or Washington was not possible (195). Even if there had been strong leadership, the uniqueness of the events of 1932 and 1933 immobilized the policymakers.

Wicker argues that Federal Reserve policy in 1929–33 was consistent with its actions in the 1923–24 and 1926–27 recessions. The Federal Reserve followed the practices laid down by Governor Benjamin Strong: use open market operations to reduce member bank borrowing below $500 million and reduce borrowing by New York banks commensurately. Once this was done, policy would be “easy.” Wicker added that international cooperation motivated open market purchases in 1924 and 1927, specifically to help Britain return to and remain on the gold standard.

A problem with some of these explanations is that the Federal Reserve was not entirely passive for the three and a half years of the decline. More than once it purchased securities or lowered the rediscount rate. It actively responded to events such as the departure of Britain from the gold standard in October 1931 by raising the rediscount rate to stem a gold outflow, as gold standard rules required. Although disputes persisted about the locus of power within the System and there were clashes between personalities, these are overtones that do not adequately explain the dismal record. If the crisis was largely due to an absence of leadership, more effective action would have been taken later, after the System reorganized, given additional authority and a strong chairman. But in the middle and late thirties, just as in the early thirties, the Federal Reserve did next to nothing to foster recovery. In a period of prolonged and widespread unemployment, the Federal Reserve’s principal policy action was the 1937–38 series of deflationary and contractive increases in reserve requirement ratios taken to forestall a possible future inflation.

Although Friedman and Schwartz offered an interpretive history based on what might have happened if Governor Strong had lived, a main point of their explanation is of doubtful validity. It is true that W. Randolph Burgess, and others at the New York bank, proposed expansive policies, and at times Harrison suggested purchases. In fact, Harrison argued vigorously for open market purchases at times, but at other times he was a leading proponent of open market sales. The timing of Harrison’s decisions to purchase or sell can be explained (approximately) by the conjunction of the Riefler-Burgess and real bills doctrines. These ideas or beliefs misled Harrison and others in the Federal Reserve at critical points in the early thirties and thereafter. As noted by Wicker (1966), Brunner and Meltzer (1968b), and Wheelock (1990, 1992), Federal Reserve officials behaved consistently in the 1923–24, 1926–27, and 1929–33 declines.4

The difficult issue to resolve is whether Strong’s colleagues on the Open Market Policy Conference (OMPC) would have supported expansive policies had he proposed them.5 Many of his fellow governors had been persuaded to go along but were not convinced that his arguments were correct in 1924 and 1927. Moreover, member bank borrowing remained high in 1924 and 1927, so domestic concerns (and the desire for earnings) reinforced international reasons for purchasing government securities. During most of 1929–33, member bank borrowing remained low; on Riefler-Burgess views, domestic policy was easy. Further, Adolph Miller and others at the Board blamed Strong’s policies for the depression. They interpreted the depression as the inevitable consequence of the preceding growth of bank credit and asset prices that followed the 1927 policy actions Strong had urged. Because credit expansion had increased without equivalent purchases of real bills, this policy was inflationary. Deflationary policy should have followed in 1928. That mistake had to be corrected.

Several governors agreed with this interpretation. Although the price level had fallen, Strong’s policy had violated the rules of the real bills doctrine. The violation had to be purged.6

Eichengreen’s claim that the gold standard prevented action is difficult to reconcile with the System’s responses in the 1923–24 and 1926–27 recessions. These actions had received praise at the time and encouraged the belief that the System had taken countercyclical action to lessen the downturn. If the Federal Reserve had risked the temporary loss of gold on these occasions, why would it fail to run the same risk in the much steeper decline after August 1929?

The Federal Reserve was in no danger of abrogating its gold reserve requirements in 1929, 1930, or early 1931. In fact, the System experienced a gold inflow in 1930 and early 1931. By June 1931, the monetary gold stock was almost 15 percent above the August 1929 level, whereas gold collateral required for notes had increased no more than 2 percent and collateral for bank reserves had increased only $40 million—less than 2 percent.

Eichengreen (1992, 297–98) accepts the argument in the Federal Reserve’s 1932 annual report that its response in 1931 was limited by the decline in the gold stock and the requirement to use gold as backing for Federal Reserve notes, the so-called free gold problem.7 Although there is some dispute about the relevance of the problem, any relevance is limited to the period following Britain’s departure from gold on September 20, 1931, and the passage of the Glass-Steagall Act on February 27, 1932. During the rest of the decline, gold cover for the notes was not an issue.8 The Federal Reserve did not use government securities as collateral for notes until May 1932, after increasing its holdings of governments more than $650 million between February and May.

Stripped of its technical details, the free gold explanation asserts that System open market purchases would have reduced the ratio of gold to notes and deposits below the required ratios of 40 percent and 35 percent. Technical restrictions seem a weak explanation for the lack of response. Bagehot’s well-known writings had instructed the Bank of England that it could not protect its gold reserve by failing to expand. On several occasions in the nineteenth century, the Bank of England had suspended the gold reserve requirement and relaxed restrictions on eligible paper for discounts when required to stop a panic. When necessary, the government had indemnified the bank against claims arising as a result of the suspension. This history was known within the Federal Reserve and referred to on more than one occasion.

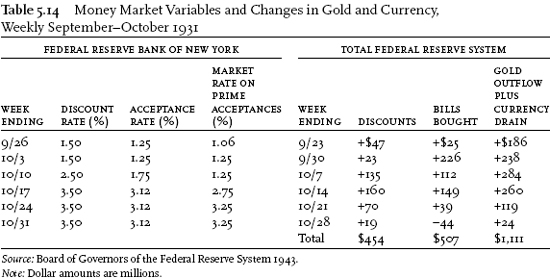

Charles S. Hamlin, a member of the Federal Reserve Board from 1914 to 1936, discussed the loss of gold at a meeting in Boston on November 20, 1931, two months after Britain had suspended convertibility (Federal Reserve Bank of Boston 1931, 13–16). Hamlin began by summarizing the main movements of gold into and out of the United States since 1914. He described the $750 million outflow from September 17 to October 30, 1931, as “the largest ever sustained by any country in such a short space of time” (15). Nevertheless, the Federal Reserve, he said, held more than $1 billion of gold reserves above the amounts required for Federal Reserve notes and member bank balances. Then he added: “In addition, there is about $1,000,000,000 in gold certificates in circulation in this country, a considerable part of which could if desired be replaced with other forms of currency. We not only have ample gold to cover the legal requirements but our monetary gold stocks, even after the heavy withdrawals, are only slightly below the prosperous years of 1928 and 1929” (16).

Hamlin next commented on the reason for protecting the gold reserve: “The experience of recent weeks brings home to Federal Reserve officials their heavy responsibility, the necessity for keeping their powder dry, so that in these troublous times they may remain the rock that can withstand all storms and upon which world confidence may once more be reconstructed” (ibid.; emphasis added).9

Eichengreen correctly points out that before and during the world economic decline, France contributed to the onset and the severity of the world depression by sterilizing much of its gold inflow. From June 1928 to September 1929, the French bought $2.6 billion in gold and, in the same period, reduced their foreign exchange reserves by an equal amount.10 From September 1929 to March 1933, the Bank of France acquired an additional $1.6 billion in gold while reducing foreign exchange reserves by $800 million. For the period September 1928 to March 1933 as a whole, French gold reserves increased by 2.8 times while French holdings of gold and foreign exchange increased only 30 percent.

The French money stock rose 18 percent in the two years 1930 and 1931. Greater expansion and less sterilization by the Bank of France would have lessened the severity and scope of the world decline. At issue is whether the failure to expand more resulted from a lack of coordination. The Bank of France was not obliged to sterilize much of the gold inflow. The United States was not obliged to contract as France sterilized.

The critical flaw was not the absence of international coordination but domestic decisions at critical times to not interfere with the contraction of money and credit and the resulting deflation. Protecting the United States gold reserve was at most a secondary effect of the principal decision. Leading central bankers and their advisers believed that credit expansion to finance stock market speculation in 1928–29 was a misuse of credit that had to be eliminated. Bankers, economists, and others stated this view repeatedly during the contraction.

Writing at the time, Oliver M. W. Sprague explicitly rejected both the idea that monetary expansion was desirable and the idea that absence of international cooperation contributed to or exacerbated the depression. Sprague was an expert on banking crises and a close adviser to the Federal Reserve. He also served as economic adviser to the Bank of England from 1930 to 1933.11 In a May 1931 speech in London, Sprague discussed the causes of the depression and the role of international coordination (Board of Governors of the Federal Reserve System, Weekly Review of Periodicals, June 2, 1931, 1–2).12 He began by noting that the depression had become more acute. There was no agreement on its causes or on appropriate remedies. He summarized two divergent views. The “monetary school” wanted the leading central banks to “flood the market with a great amount of additional credit and currency.” The “industrial or economic equilibrium school included all the responsible [sic] people connected with the great central banks of the world.” This school held that falling prices were a symptom, not a cause: “When prices did advance, more currency and credit would be employed, but they did not believe that simply by injecting more currency and credit into the situation they could certainly bring about the desirable rise in prices and business activity.”

The problem was not lack of agreement between the principal central bankers: “It was not because of any difficulty of securing agreement among the three banks, (France, U.K., U.S.) but because none of them harbored the belief that it was the appropriate remedy” (ibid., 1–2).

Sprague, like the central bankers in France, England, and the United States that he described, accepted the “industrial equilibrium” explanation. The world’s economies would reach a new equilibrium at lower prices and wages. It would take time, they recognized, but they believed deflation was the correct solution to the mistakes of 1928–29.

In a speech to the Royal Statistical Society a few weeks later, Sprague explained why the deflationary solution was proper. There had been overproduction particularly in the American automobile industry. Further, there had been a speculative boom. He blamed Federal Reserve policy in 1928, when it would have been “possible to check the speculative wave on the New York Stock Exchange” (Weekly Review, June 24, 1931, 1).

Paul Warburg wrote in the American Banker for January 20, 1931, “The way to avoid a depression (or lessen its severity and duration) is to ‘sit on the bulge’ during an excessive upward swing. Once acute over-expansion has taken place, acute overcontraction must follow with inexorable certainty. Unfortunately, it would seem politically impossible for any government to use its influence toward checking a wave of prosperity, even though it was clearly a fake prosperity destined to end in a crash” (Weekly Review, January 27, 1931, 5).

These were not the only views, but they were common views of central bankers. M. H. deKock of the South African Reserve Bank thought that the “maintenance of pronounced monetary ease for any length of time almost inevitably leads to inflation and speculation in one form or another” (Weekly Review, February 3, 1931). In the same report, the noted British economist Lionel Robbins argued against the view that there was a worldwide shortage of gold. Like most others, he failed to distinguish between real and nominal interest rates: “If insufficiency of gold is the main cause of depression, why is there a depression in America. And with a 2 percent discount rate in New York, it is hard to contend that credit conditions are stringent” (2–3).

Robbins also mentioned the maldistribution of the gold stock, a common complaint at the time. However, he assigned more importance to the unhealthy character of the boom in 1928. Money rates had been held too low for too long.13

Charles S. Hamlin shared the view that speculative excesses had to be purged from the financial system and the economy. On November 8, 1929, shortly after the 1929 stock market break, he told a group of New England bankers:

The present crisis through which we are passing is typical of the kind of crisis that the framers of the Federal Reserve Act had in mind. The Act was designed to prevent the close dependence or interdependence of American industry upon speculative activity throughout the community. ... The Federal Reserve System was designed to break up the vicious circle under which a speculative orgy accompanied every forward step of industry....

The success of the Federal Reserve System is apparent today.... These events [losses] are deplorable, but they were of course inevitable and could not have been avoided. (Federal Reserve Bank of Boston 1929, 28)

The opinions of bankers and central bankers at the time are similar to the statement of Federal Reserve policy in the tenth annual report (Board of Governors of the Federal Reserve System, Annual Report, 1923). As Friedman and Schwartz note, the statement was compatible with two interpretations. One, the “real bills” or “productive credit” view of policy, required the Federal Reserve to provide “credit” for the “needs of trade” but not for “speculative” uses. The second interpretation is that the Federal Reserve would attempt to counteract inflation and deflation by countercyclical open market operations.

Only the first interpretation, the real bills view, appears in the minutes of the Open Market Policy Conference for the early thirties and in the statements of bankers and central bankers above. It is possible that the references to statements in the tenth annual report were made to justify views that were held for other reasons. Even if this was true, however, it is striking that none of the governors objected to the interpretation or presented an alternative. Even more striking is the absence, at most of the meetings of the OMPC, of any statement favoring an expansive policy. Even those governors who occasionally pressed for open market purchases and reductions in the discount rate expressed doubt that monetary (or credit) policy alone would have much effect on output. They too appear to have been greatly influenced by the notion that the prevalence of low nominal interest rates and low borrowing showed that policy was “easy.”

Benjamin Strong shared many of these interpretations. He often relied on the volume of member bank borrowing as a measure of ease or restraint.14 Nothing in either the Riefler-Burgess doctrine or the real bills doctrine distinguished between real and nominal rates of interest or recognized that the level of borrowing depends on anticipated income and inflation.

The minutes of the Open Market Investment Committee, the Federal Reserve Board, and the Conference of Governors of the Reserve Banks, considered below, show that most of the policy decisions remained consistent with the Riefler-Burgess and real bills frameworks. This should not suggest that everyone slavishly followed a formula. Many other inherited notions, mentioned in the minutes, contributed to the Federal Reserve’s failure to act or justified inaction. Concerns about “redundant reserves” or “excessive liquidity in the banking system” are variations on the real bills theme but may have other origins. Whatever the source of these ideas, many of the policymakers opposed expansive policy action because they believed that expansive action was inappropriate. Concern about future inflation caused several governors to hesitate to act, to regard deflation as the inevitable consequence of previous speculative excesses, for much the same reasons that Strong and others had viewed the severe deflation of 1920–21 as a consequence of inflationary wartime policies and a necessary prelude to the price stability of the middle twenties. Speculative credit and nonreal bills had to be purged. This was the message of Hamlin, Warburg, Robbins, Sprague, and many other bankers and central bankers.

Once borrowing and short-term market rates had fallen below the range familiar to governors and commercial bankers, policy was “easy.”15 They saw no reason for further additions to reserves and further reductions in market rates. Expansive policy would finance speculative credit and become the source of a future inflation that, once under way, would be difficult to stop. The System’s holdings of government securities were much smaller than the level of member bank borrowing during much of the twenties and were not substantially larger than the level of borrowings in the early thirties. Not having enough securities on hand to prevent a future inflation had been a recurring concern since the start of the Federal Reserve System. The concern seems a ludicrous reason for not expanding, but it appeared very real to several of the governors at the time. Since nominal interest rates had been reduced to levels that were comparatively low by the historical standards or experience the governors and members relied on, they saw little reason to increase speculative credit and accept the risk of inflation.

Some officials either did not fully share the dominant view or differed about particular events. At times some showed clear understanding of the role the System might play, although they did little to promote their views against the dominant view in the System. Included in this group are two members of the Federal Reserve Board—Eugene Meyer and Adolph Miller—who at times questioned Harrison and the other members of the open market committee about their reasons for not pursuing a more expansive policy. W. Randolph Burgess at the Federal Reserve Bank of New York urged more expansive policies at critical times, with support from the directors of the New York bank.

The policy problems of the early thirties were not unique. Books discussing the appropriate means of handling these problems were known to some of the members of the open market committee or their staffs. The effect of changes in the quantity of money had been discussed for more than a century, and many outstanding economists had contributed to the analysis. Some, like Henry Thornton (1965) and Walter Bagehot (1962), whose works are discussed in chapter 2, had described the appropriate response of a central bank to a crisis. Both Thornton and Bagehot suggested some of the principal reasons for large-scale currency withdrawals, and both had indicated that during a currency drain the central bank should expand.

Three of Thornton’s recommendations to the Bank of England are particularly relevant to—and contrast sharply with—the behavior of the Federal Reserve during the thirties. First, he argued repeatedly that there was rarely any reason for reducing the quantity of money (Thornton 1965, 259). Second, he urged the governors of the bank to meet an increase in the demand for currency by temporarily increasing the bank’s liabilities (259). Third, he recommended that the bank use the quantity of money—and not the volume of commercial bank borrowing from the central bank or of private borrowing from commercial banks—as a measure of its policy and the influence it would have on prices and output (271).

It is possible, but unlikely, that Thornton’s work was entirely unknown.16 However, there is no doubt that officials knew Bagehot’s work, since references to his book, Lombard Street, appear in the OMPC minutes. Bagehot had demanded repeatedly that the Bank of England acknowledge publicly that it served as lender of last resort, and subsequently the bank had done so. And Bagehot had discussed fully why it was a mistake for a central bank to seek to protect its gold reserve by failing to lend during a run on commercial banks.

Numerous other writers had analyzed the effects of changes in the quantity of money and the responsibilities of central banks in a crisis. Two of the most able monetary economists of all time, Irving Fisher (1920, esp. chap. 4) and John Maynard Keynes (1930, 1931), had argued in scholarly books, in pamphlets, and in newspaper articles of the period that a decline in the quantity of money would first affect the level of output and employment and only later affect the price level.17 Neither the absence of relatively simple, comprehensible alternative theories, nor the absence of facts about developments in the economy, nor the absence of strong leadership can explain the dismal record. The main reason for the failure of monetary policy in the depression was the reliance on an inappropriate set of beliefs about speculative excesses and real bills. This set of beliefs, embodied in the Riefler-Burgess framework, directed attention to short-term market interest rates and member bank borrowing and encouraged their use as indicators of the magnitude and direction of monetary stimulus.

THE FIRST YEAR OF DECLINE: POLICY FROM AUGUST 1929 TO SEPTEMBER 1930

To show how policy responded to the economic decline, the discussion comments on each meeting of the Open Market Investment Committee and its successor the Open Market Policy Conference, or their executive committees, between the peak of the expansion in August 1929 and the trough of the recession in March 1933. A series of twenty tables shows some of the information available at each meeting. Three types of data suggest the direction of monetary policy and the levels or changes in other variables that the committee discussed from time to time at its meetings or that influenced its decisions. One type of data shows cumulative change from the peak of the expansion to the nearest month. A second type, called “recent changes,” shows the change in various measures between meetings. The third group shows the levels of variables that are of interest, again dated to the nearest month.18 Data for the money supply were not available at the time, but currency and demand deposits were available separately.

Responses to the Financial Panic

At the peak of the cycle in August 1929, the level of member bank borrowing exceeded $1 billion, the highest level reached since 1921. The interest rate on new stock exchange call loans was 8.15 percent, more than 1.5 percent below the high for the year in March. Other short-term market rates had passed their peak, while long-term rates were generally at the highest levels of the expansion. The seasonally adjusted monetary base was 1 percent below the peak reached more than a year earlier.

In the first six weeks the policy, agreed on in August, worked as planned; the System provided seasonal credit expansion by lowering the acceptance rate while raising the discount rate. Harrison told the Board that the total seasonal increase was about average. The acceptance portfolio increased $162 million, more than offsetting the $130 million decline in discounts. In addition the System purchased $20 million in the open market. Harrison asked for an OMIC meeting in September to consider open market purchases to supplement acceptance purchases (Board of Governors File, box 1435, November 12, 1929; these are minutes of the September meeting).

Brokers’ loans continued to increase. Banks used all the reserves obtained from sales of acceptances to the reserve banks to repay discounts, so total bank credit remained unchanged. Interest rates changed little.19

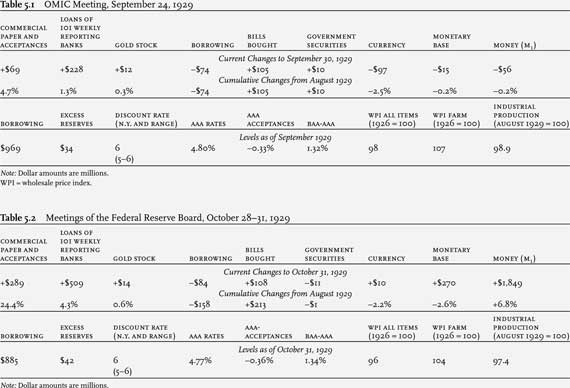

At the September 24 meeting, the governors expressed concern about the levels of discounts and rates of interest. To reduce both while acting against an impending recession, the committee voted to purchase up to $25 million of government securities weekly, if acceptances could not be obtained at the posted buying rates of 5.125 percent. When presenting the proposal to the Board, Harrison, the chairman of the OMIC, noted that “some reduction in this [member bank] indebtedness would be a necessary prerequisite to any further easing of interest rates,” as implied by Riefler-Burgess. The Board delayed accepting the proposal until its members returned from vacation. On September 30 Harrison wrote to Governor Roy A. Young at the Board to report the favorable response of the New York directors to the purchase program and again stressed the importance of reducing interest rates.

The Board approved the committee’s recommendations on October 1. In his reply to Harrison, however, Young noted that the Board’s approval was mainly for seasonal reasons, not a reversal of prevailing policy. There was no suggestion in the monetary indicators the Board and the committee watched, and no recognition in their discussions or letters, that the financial system was about to experience the first of a series of shocks in the following weeks. The committee made no open market purchases until the week of October 30.

The indexes of prices on the New York Stock Exchange reached peaks in September and plummeted in the last week of October. The Federal Reserve lowered the buying rate on banker’s acceptances by 0.125 percent (to 5 percent) on October 25. By October 28, with the decline on the stock exchange continuing, the members of the Board were of the opinion that “no further easing of the bill rate should be made at this time as the easing program of the system seems to be progressing satisfactorily.” The next day the market plunged downward on volume in excess of 16 million shares, nearly five times the average daily volume.

The following day Governor Young reported on his conversation with Harrison. Harrison informed him that the directors of the New York bank had given him authority to purchase government securities for the bank’s account without any stated limit, and he had used this authority to purchase $50 million. Inasmuch as the purchases had been completed, Young concluded: “There was nothing before the Board at that time requiring immediate action.”

The Board was piqued at Harrison and the New York bank for undertaking purchases without prior approval (as was customary), but decided to defer discussion of Harrison’s assumption of responsibility until later. Instead, the discussion turned to action that “might appropriately [sic] be taken.” Cunningham suggested, and the majority agreed, that it would be best to reduce the discount rate at the New York Bank from 6 to 5 percent, “with the understanding that the System will suspend, for the time being, any purchases of government securities, pending further developments in the credit situation as a result of the rate reduction, and further consideration and approval by the Federal Reserve Board.”

Harrison then called to inform the Board that he had purchased an additional $65 million, a total of $115 million for the day. There was no further discussion of policy at the Board meeting.

On the following day, October 30, Young reported to the Board on his conversations with Harrison and James B. McDougal (Chicago). Young’s position was classical; the System should encourage discounting by member banks, and he had told McDougal that “while he could not commit his board, he thought loans should be made freely and liberally.” The conversation with Harrison had apparently been lengthy, owing to a difference of opinion between New York and Washington on the policy that was appropriate for the day. Harrison informed Young that he was planning further purchases of securities. Young reported to the Board that he had advised Harrison that further purchases would “probably lead to the eventual promulgation of a regulation on the subject” by the Board.

The difference of opinion between New York and Washington was another round in the dispute about who had responsibility for decisions. Young reported that he had “advised Governor Harrison that he would not hesitate about lending to a member bank.” He told the Board that “he would go farther and purchase government securities liberally using any resource that the System has in an attempt to minimize the effects of conditions that may develop.” Other members of the Board—Edmund Platt, Hamlin, and Miller—agreed with Young’s position and urged him to communicate these views to the reserve banks.

Young informed Harrison on October 31 that the Board was in favor of reducing the discount rate at New York from 6 to 5 percent and that the “majority appeared to have changed their views with respect to coupling the reduction in the discount rate with an agreement to suspend purchases of government securities for the time being, feeling that the Federal Reserve banks should be prepared to pursue a liberal policy.”

The positions now reversed. Banks had reduced their discounts by more than $150 billion since the cyclic peak. The gold stock had increased, and banks continued to lend on commercial paper, real bills, with only modest changes in interest rates. Harrison told the Board that he had made no purchases on October 30, that he did not plan to make any purchases that day, and that he could see no reason for additional purchases, “although it might become necessary to take on additional amounts later.” His directors had adopted a resolution, unanimously, “that, in the interest of maintaining business and employment, the policy ... for the coming weeks should be to keep a plentiful supply of money in the market ... in order that discounts of the Federal Reserve System may be reduced and at the proper time a further reduction of the discount rate effected with the objective of securing lower interest rates for business throughout the country.”

The prompt and rapid response by the New York bank undoubtedly prevented the rapid decline in stock prices from affecting interest rates in the money market. The monthly data show a slight rise in the interest rates on short-term Treasury notes and longer-term corporate bonds and a substantial decline in the rate charged for new stock exchange call loans. Weekly data on open market rates for the last week of October 1929 show a slight rise in the rate on new stock exchange call loans and a decline in other quoted market rates. Commercial banks in New York made the largest volume of new loans to brokers and dealers shown in any week up to that time and offset to a large extent the reduction in call loans by banks outside New York. Although the average of daily figures in table 5.2 shows the Federal Reserve as a net seller of government securities for the month as a whole, the System purchased $157 million of government securities during the last week of the month, more than doubling the size of its portfolio of governments. In addition, the discounts of member banks with the System increased by $200 million for the week.

Although the Board was in favor of continuing the policy Harrison had started, the committee made no purchases in the following week. On November 1, New York reduced its discount rate to 5 percent and also reduced the buying rate on banker’s acceptances. The monetary base declined by $50 million, almost one-sixth of the increase in the previous week. Open market rates changed very little, and both the market and the System appear to have decided that the crisis had passed. The Board did not press New York to make further purchases. During the rest of 1929, the Board met almost every day, generally discussed routine matters, and rarely mentioned open market policy.

The Board’s minutes for the week of the crisis make it clear that the members were slower than the New York bank to recognize the desirability of large-scale open market purchases. But the lag, or delay, was at most two days. By October 31, Governor Young and most of the Board members wanted further purchases to offset rising discounts, while Harrison and the directors of the New York bank, knowing that the panic had not affected the money market, favored a less aggressive approach.

Part of the dispute about whether the System should act through open market operations or by discounting reflects the entrenched “real bills” doctrine. Those who favored discounting as a means of supplying reserves generally wanted to leave the initiative with the member banks and favored using the “needs of trade” as a guide to appropriate policy. Even in periods of crisis, their discussion contains repeated references to the “demand for Reserve bank credit,” in contexts suggesting that the Federal Reserve should supply the quantity of reserves demanded to meet the “needs of trade” but should avoid using open market operations to supply “redundant reserves” that would generate “speculative excesses.”

The reactions in New York and Washington are consistent with the Riefler-Burgess view. The pressure on the commercial banks in New York became intense at the time of the stock market decline, in large part because banks outside New York reduced their loans to the call money market. The security purchases by the New York bank undoubtedly prevented both a sharp rise in interest rates during the week and additional borrowing from the Federal Reserve by banks in New York and other large cities. Since the Open Market Investment Committee had decided at the September 24 meeting to reduce borrowing, by open market purchases if necessary, the response by the New York bank is not a deviation from the prevailing policy or from the concentration on interest rates and money market conditions. The reluctance to continue purchasing once borrowing and upward pressure on interest rates declined is further evidence that its behavior at the time was consistent with the Riefler-Burgess framework.20

Friedman and Schwartz (1963, 367) offer a different interpretation of these events. Their discussion, based on Harrison’s papers, makes no mention of the change in responses by Washington and New York after October 29. In their view, New York stopped purchasing securities because of the strong reaction at the Board. More important, they suggest that this episode had a permanent effect on Harrison and that thereafter he was reluctant to engage in open market operations without the consent of the Board or the Open Market Investment Committee. The Board’s records suggest, on the other hand, that the Board members conceded Harrison had been correct in making large-scale purchases of government securities and in encouraging the additional discounts that the Board had urged from the start as a means of meeting the crisis. They disliked New York’s decision to act alone.

The dispute was mainly about procedure, not about substance. Nor was the procedural issue a new one. The Board and the New York bank had differed about the division of responsibility and particularly about the Board’s role in open market policy from the very first years of the System and particularly after 1923, when the importance of open market operations increased. The Board had discussed reorganization of the committee responsible for policy recommendations at meetings in 1928 and 1929.

Harrison wrote to Young on November 7. The New York directors had voted that day to purchase government securities if they did not acquire sufficient acceptances. Their aim was to provide a seasonal increase in reserves while reducing the volume of discounts and open market rates. His letter mentions the directors’ concern “that there may be a greater danger of recession in business with consequent depression and unemployment, which we should do all in our power to prevent” (Open Market, Board of Governors File, box 1435, November 7, 1929).

No purchases were made. Between September 24 and November 8, the System account increased $80 million, by purchases of $30 million and acquisition of $50 million purchased by New York during late October. New York increased its holdings (net) by $108.8 million. Only seven reserve banks participated in the purchases.21

John U. Calkins, president of the San Francisco reserve bank, explained his reasons for not participating in open market purchases.22 He was not “in entire sympathy with the course of open market policy.” He was opposed to the view that “artificial conditions should be created for the purpose of promoting a bond market.... We can not see that this policy can be continuously followed without unfavorable results” (Letter Calkins to Harrison, Board of Governors File, box 1435, January 7, 1930).

Calkins then commented on Strong’s 1927 purchases: “We are unable to see that the 1927 experiment, now quite generally... admitted to have been disastrous, contributed very materially to the welfare of this country by providing or supporting a market for our exports.... [T]he purpose of the Federal Reserve System is to provide and assure adequate finance for trade ... at a cost conducive to stability” (ibid., 2; emphasis added).

This letter, written within a few months of a major financial panic and at a time of deepening recession, represented a substantial body of opinion within and outside the Federal Reserve System. To these real bills advocates, Strong’s 1927 policy had failed on the narrow grounds of expanding exports, on which it had been offered, but it also had been a main cause of the increase in stock prices and brokers’ loans. They wanted no more. They believed that crises and recession were inevitable after speculative lending; they had to be endured to reestablish a sound basis for expansion.23

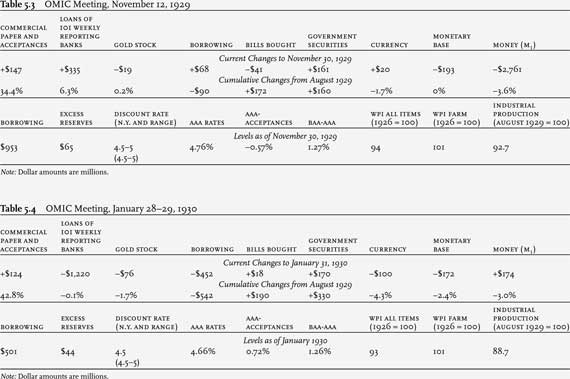

The data in table 5.3 are for the end of November, hence they overstate somewhat the changes that had taken place at the time the committee met. The sizable reduction in the money supply is a reversal of the very large rise in deposits in the last week of October. At the time of the meeting, industrial production was 5 percent below its level at the peak, and by month’s end it was more than 7 percent below the August peak. Short-term interest rates and wholesale prices had continued to decline, but member bank borrowing was higher on average than in the preceding month.

The committee noted that a turning point had occurred and that there had been a “severe liquidation of credit against securities under circumstances which constitute a serious threat to business stability at a time when there were already indications of a business recession.” The time had come for the Federal Reserve System to “do all within its power toward assuring the ready availability of money for business, at reasonable rates.” In the Riefler-Burgess framework, the committee’s statement meant that the discounts of member banks should be reduced. The governors voted to do just that by purchasing bills (acceptances) and, if necessary, by purchasing government securities. At Harrison’s suggestion, the committee changed the limit on purchases from $25 million per week to a total of $200 million between the November and January meetings.

This meeting, within three months of the turning point, showed little disagreement about the interpretation to be placed on the events that had occurred or on the proper means of meeting the expected recession. The committee clearly regarded the fall in security prices and the decline in the public’s wealth as factors intensifying a recession that was already under way. The record in 1929, as at the start of most subsequent recessions, is inconsistent with the often-repeated view that the Federal Reserve is slow to take countercyclical action because it is slow to recognize the onset of a recession. The reluctance to take expansive action that many of the governors showed at subsequent meetings of the committee cannot be explained as a misinterpretation of the then current economic conditions or a failure to recognize that the economy had turned from expansion to recession.

At first the Board refused to approve the committee’s decision. Young wrote to Harrison on November 13 that the Board was willing to authorize purchases for emergencies but would not grant authority to purchase up to the $200 million approved by the committee. Harrison’s memo, recording his subsequent conversation with Young, makes it clear that he viewed the Board’s objection as an opposition to the grant of discretion, not to the purchase policy. He accused Young of wanting to have a central bank operating in Washington and was surprised when Young agreed (Harrison Papers, Conversations, vol. 1, November 15, 1929).

To obtain approval of the purchase program, Harrison offered a temporary solution to the procedural issue. New York agreed to stop purchasing for its own account if the Board approved the committee’s decision without qualification. The Board accepted on November 25. In the first three weeks of December, the System purchased $207 million of securities and $52 million in acceptances. In the remaining weeks of December, market rates fell, acceptances came to the bank at a faster rate, and the System sold nearly $50 million of government securities. The initial crisis was over.

Response to Recession

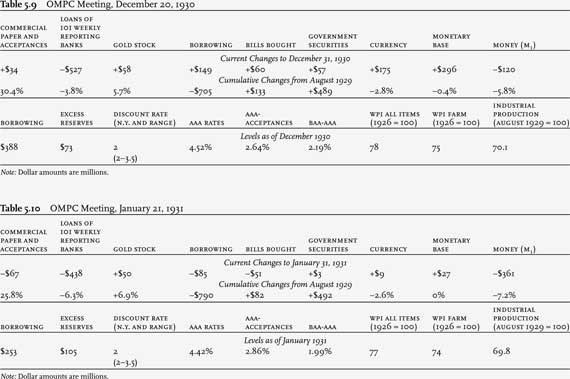

Changes in many of the monetary variables at the time of the January meeting are not markedly different from the changes that characterize other recessions.24 Gold and bank loans had fallen, the latter partly a reflection of the reduction in stock exchange credit. The monetary base had fallen also, but more of the base was held as bank reserves, so the money supply had increased. Short-term interest rates were below the levels reached at the peak and had declined since the previous meeting; the term structure sloped up. (The term premium between Aaa rates and ninety-day acceptances had increased from 0.57 to 0.72.) Member bank borrowing was 50 percent below its peak, the lowest level since early 1928.

The January meeting was the first meeting after issuance of the Board’s order replacing the OMIC with a new Open Market Policy Conference (OMPC) on which all reserve banks would serve. Although all governors participated in the January meeting, there was substantial disagreement about the new procedure, and it was not adopted until March 31.25

The new committee recognized that “a business recession has taken place, the extent or duration of which is not yet possible to determine” and that “liquidation is progressing in an orderly fashion.” However, the members were divided about the policy that should be pursued in the coming months. Governor Eugene R. Black (Atlanta) “desired a continuation of credit ease,” arguing that neither business nor the mental attitude of businessmen in his district was conducive to expansion. At the other pole, “Governor McDougal (Chicago) indicated that an easing policy would be worth considering if it would benefit business, but he felt present rates were not restrictive.” “Governor Norris (Philadelphia) believed that open market operations had been carried far enough, that the object of the November policy had been achieved, and he would rather see lower interest rates come of their own accord than as a result of Federal Reserve interference.”

Governors Lynn P. Talley (Dallas), William McChesney Martin Sr. (St. Louis), and John Calkins (San Francisco) joined Norris and McDougal. Calkins noted that there had been “more than the usual liquidation in his district,” but he could see no reason for further changes in interest rates. Others took intermediate positions, several favoring Harrison’s proposed reduction in the buying rate for acceptances.26 No one argued for a program of substantial or even moderate open market purchases. It was “the judgment of the Committee that no open market operations in government securities are necessary at this time either to halt or expedite the present trend of credit.”

Although the committee recognized that changes in loans and investments of reporting member banks were smaller “than the usual growth of credit required by the country’s business,” it voted only to “avoid the hardening of rates which might result from a seasonal demand for additional reserve credit.” Its statement urged caution and restraint. The reasons that prompted most members to proceed cautiously are developed more fully in the committee’s policy statement:

The majority opinion was that what had already been done has set in motion a trend which should result in lower rates. Between a reduction of discounts and large purchases of securities and a reduction of rates to business there is always a lag and that lag is likely to be greater at this time because the appetite of the bankers has been whetted during recent months, and they are slower about coming down. There is every reason to anticipate that the reduction will occur, so that it is believed that the current is set in the direction of easier rates.

We feel we should not interfere in that movement either in the direction of halting it or attempting to expedite it. ... [It] is inexpedient to exhaust at the present time any part of our ammunition in an attempt to stimulate business when it is perhaps on a downward curve ... in a vain attempt to stem an inevitable recession... . The majority of the Committee is not in favor of any radical reduction in the bill rate or radical buying of bills which would create an artificial ease or necessitate a reduction in the discount rate. (Open Market, Board of Governors File, box 1436, January 30, 1930)

The empirical basis for the committee’s conclusions is more clearly set forth in a memo that Harrison had read to the Governors Conference more than a month earlier.27 The memo contained two charts. One showed the relation between member bank borrowing and market interest rates. The other compared the rate of increase in bank credit with the volume of member bank borrowing. Harrison interpreted the charts as showing that “generally speaking the trade and business of the country require an increase in bank credit somewhere in the neighborhood of 4 to 5% a year, and the chart indicates that the rate of increase in bank credit has usually exceeded this rate when the Federal Reserve discounts were under 400 to 500 million dollars, and usually falls under this rate when discounts are over 500 to 600 million dollars.” The memo goes on to spell out these central notions of the Riefler-Burgess framework and, after mentioning some qualifications, concludes that “these charts show in general that under conditions that have prevailed in recent years an amount of member bank borrowing somewhere in the neighborhood of 500 million dollars [the level then current] may be considered a normal at which commercial paper rates have tended to average 4½% and at which the volume of bank credit has tended to increase at the rate generally proportionate to the needs of business.” Since the volume of member bank borrowing had been reduced by $450 million in less than two months and was now within the range Harrison spoke of, it is not surprising that he did not favor or propose an aggressive policy of open market purchases.

When the Board met the next day to discuss the committee’s recommendations, Treasury Secretary Andrew Mellon repeated several of the arguments that had been made in the policy statement. The Board voted to carry out the policy recommendation and approved a minimum effective buying rate of 3.875 percent for any Federal Reserve bank wishing to establish that rate. By a tie vote, the Board followed the OMIC majority and refused to reduce the discount rate at the New York bank to 4 percent. The reasons for the Board’s refusal are not clearly stated in the report, although there is some indication that it regarded the request as premature.

The governors’ statements at this meeting provide a clear indication of their reasons for failing to take more expansive action at the time and throughout the period. Since short-term market interest rates had fallen and were expected to fall further as member bank discounts declined, most governors saw little reason for the Federal Reserve to “interfere” or to hasten the decline in rates. Words like “artificial stimulus” and “inevitable decline” reflect the dominant view that speculative excesses had to be purged. Once that happened, the economy would recover, and the System would be able to expand based on rediscounting of real bills.

Virtually all the governors used the level of market interest rates as an indicator of current policy. Differences between them at the meeting were largely matters of detail. Some opposed the 0.125 percent reduction in the buying rate for bills on the grounds that the reduction would cause the System to acquire bills in much larger quantities temporarily and thus cause market rates to fall faster than they believed desirable. Others opposed the reduction on the similar grounds that the reduction in the buying rate for bills would “force” a decline in the discount rate by contracting the amount of member bank discounts (reducing the demand for reserve bank credit). Only Governor Black advocated a policy of open market purchases.28

After the January meeting the Board approved reductions in the minimum buying rate for bills on February 11 and 24 and on March 5, 6, 11, 14, 17, 19, and 20. By the March meeting, the buying rate was 3 percent. The Board also approved further reductions in the discount rate to 3.5 percent at New York and to 4 or 4.5 percent at the other banks. These changes did not receive the unanimous support of the Board members, and those who voted for the reductions often expressed doubt about the efficacy of a “cheap money” policy.29 No one mentioned that wholesale prices had fallen 7 percent in seven months or that real rates had increased more than nominal rates had fallen.

Despite the nominal rate reductions, the System’s holdings of acceptances had declined since the January meeting, and the volume of member bank discounts was at the lowest level since early in World War I. Long- and short-term interest rates continued to decline, as shown in table 5.5. Although nominal short- and long-term rates had fallen to the levels reached in the recessions of 1924 and 1927, the term spread between short- and long-rates had doubled in the two months to March.

This was the last meeting of the committee for more than two years at which the seasonally adjusted money supply showed a rise from the previous meeting. The increase in money from January to March was largely the result of a gold inflow from Brazil and Japan and the higher base money multiplier produced by the continued decline in the public’s demand for currency in both nominal and real terms.

Much of the discussion at the meeting was about New York’s decision to purchase $50 million of government securities early in March. Although the committee had voted against further purchases at the January meeting, New York explained, as it had in a letter earlier in the month, that the purchases had been made, after consultation with the Federal Reserve Board, because it had been “impossible to maintain the bill portfolio” in the face of an increasing demand for bills by banks and financial institutions. The “unfavorable business situation” was also mentioned as a factor in the decision to purchase.30

The discussion makes it clear that the main reason for the purchases was to correct a problem that the members regarded as technical. An inflow of gold—from Japan and South America according to the minutes— had increased the reserves of the New York banks. The banks used the new reserves to purchase acceptances, forcing the Board to lower the buying rate for acceptances or allow the acceptance portfolio to decline. At first the Board reduced the acceptance rate, but the acceptance portfolio continued to fall in early March because the gold imports continued and the Treasury’s balance at the reserve banks declined. The falling acceptance rate was regarded as a technical reaction because a rise in the rate on other short-term instruments—for example, stock exchange collateral loans, particularly brokers’ and dealers’ loans—accompanied the decline.31

The preliminary memorandum prepared for the meeting noted that the recession was probably more severe than the recessions of 1924 or 1927 and that unemployment had increased. However, it also observed that “the effects of easy money and freely available credit have been, in the first place, to stimulate a vigorous recovery in the bond market. Bond prices have risen to the highest points in more than a year.” This was a particularly important piece of information within the framework that most of the members used. The rise in bond prices and the reduction in member bank borrowing seem to have provided the entire basis for the decision to make no further purchases of government securities. In the committee’s words, “The steps already taken by the Federal Reserve System in easing the money market through open market operations have gone as far in providing the stimulus of easy money for business use as seems desirable at this time.”

With hindsight, it is clear that this was an important meeting. The decision to avoid further expansive action because monetary policy was judged to be “easy” came just as there were signs of a turning point or a bottom of the recession. The preliminary memorandum prepared for the meeting noted a slight improvement in “business and trade” between December and January and further slight improvement from January to February. The data now available partly confirm the observations made at the time. Industrial production, seasonally adjusted, rose in January and declined very little in February. More important, there was a slight drop in industrial production from March to April and larger declines in May and June. The index of common stock prices had restored approximately 25 percent of the October decline in the value of common stocks by the end of March, but the rise in stock prices ended in April.

If the governors of the Federal Reserve had used the stock of money instead of interest rates as an indicator of monetary policy, they would not have concluded that monetary policy was “easy.” Additional open market purchases at this time would have contributed to the expansion. Instead, the further contraction of money contributed to the decline in output and to the bank failures that came with increased frequency after this meeting.

The striking fact about the meeting is that although there was little dissent about the size of the recession, there was little support for a policy of monetary expansion. The committee’s main recommendations were designed to prevent a further reduction in bills: it voted to reduce the buying rate for bills to 2.5 percent, but not to purchase below 3 percent except in an emergency, and to engage in no open market purchases. A memo prepared for the meeting and made part of the record showed that the System’s earning assets were lower than in the previous year, largely as a result of the fall in member bank discounts.

The discussion at the meeting showed no evidence of disagreement between New York and Washington. On March 14 New York reduced its discount rate to 3.5 percent, with Board approval. Other banks remained at 4 to 4.5 percent. In a letter to Governor Young, J. Herbert Case described the 3.5 percent rate as a possible danger, but he urged the Board to approve the step “in the hope that business may be benefited” (Board of Governors File, box 1435, March 17, 1930). He hoped that the System would act promptly to prevent excessive credit expansion.

Outside New York, reserve banks remained skeptical about additional ease. Although he saw “plenty of evidence ... that what had appeared to be an upturn in January has not held,” Governor Talley (Dallas) wrote opposing any additional expansive actions.32 “Everyone seems to want to keep business jazzed up all the time and have it run along at boom figures.... [T]he sounder course to pursue ... is to catch up and let the public pay some of its debts or at least acquire larger equities in its automobiles, radios, and real estate (Talley to Case, Board of Governors File, box 1435, March 13, 1930, 3).33

Between the March and May meetings of the Open Market Policy Conference, the Board considered a request from New York to lower the discount rate from 3.5 percent to 3 percent. At first the Board unanimously disapproved. The Board’s minutes for April 24 record a “considerable variance of opinion between the New York Bank and the Federal Reserve Board with regard to Federal Reserve policy.” The Board favored “the maintenance of stability rather than further easing through Federal Reserve action.” Within a week, however, Governor Young changed his mind and announced that he favored reducing the discount rate and the buying rate for bills. On May 2 the Board approved New York’s request, and in the following weeks the effective buying rate for bills declined to 2.5 percent, below the rate that the March conference had suggested as a minimum.

New York’s request was a response to the deteriorating economy. At a meeting on April 24, Harrison reported to his directors that production and trade had declined in March and that preliminary figures for April, covering building contract awards and railroad car loadings, showed a further decline. Harrison also reported that commodity prices had fallen, that foreign trade had declined during the first quarter, and that gold continued to flow in. He recommended a reduction in the discount rate as a means of improving the bond and mortgage markets, which “historically and logically appear to be a precedent or a necessary accompaniment of recovery in business and prices after a period of depression.” The following week Harrison again discussed a discount rate reduction with the directors. This time the Board approved.34

The data for this meeting, in table 5.6, show the renewed decline in industrial production and the fall in wholesale and farm prices. Although bank lending (at weekly reporting banks) had increased since March, commercial paper and banker’s acceptances had fallen. The data also show that standard policy actions were not having their expected effect. Lowering short rates had not reduced long rates. Rates on Aaa bonds were only twenty-four basis points below the August 1929 peak, while prime banker’s acceptances had been reduced by 2.625 percent. The term premium had increased by a factor of three, from 0.7 to 2.1 percent since the end of January.

Some of the New York directors continued to press for expansive action. They instructed Harrison to inform the Board that they wished to purchase government securities. Governor Young suggested a meeting of the conference so that “all Federal Reserve Banks may be informed of the program which the New York Bank seems to have in mind” (Board Minutes, May 15, 1930).

New York was not the only bank dissatisfied with the conduct and achievements of open market policy. At the May meeting, Governor Young presented five suggestions that had come before the Board. Two called for open market sales; two called for purchases; and one bank wanted to maintain the prevailing policy but provide from $350 million to $400 million for seasonal requirements through open market purchases and increases in bill holdings during the fall.

Several features of the Federal Reserve’s approach to policymaking are mentioned to support or justify the three proposals. Some governors, following one aspect of the real bills doctrine, regarded the end use of credit as the most useful guide to appropriate policy. They believed open market sales would “check speculation” and help the banks to liquidate security loans. Their main evidence of speculation at this time was the increased volume of brokers’ and dealers’ loans that had accompanied the increased volume of security purchases and rising stock prices in the months before the meeting. Others, concerned about the distribution of the Federal Reserve’s earning assets, wanted to sell $200 million of securities and reduce discount rates “so that rediscounts might be approximately equal to the total of government securities and bankers acceptances held.” This proposal reflected a different aspect of the real bills doctrine, the view that a main purpose of monetary policy was to respond to changes in the demand for reserve bank credit. Some governors believed that open market sales would ease credit by encouraging banks to reduce interest rates and force them to borrow on real bills. The proper policy, they claimed, was to lower discount rates and sell securities.

Poor timing was one reason the proposal for open market sales and lower discount rates did not receive more widespread support. The provision of the Federal Reserve Act calling for an “elastic currency” was interpreted as a requirement to meet the seasonal “needs of trade.” One governor who favored seasonal expansion in the fall expected the seasonal demand for bank credit to be larger than the current (May) demand. He expressed the view of several governors when he suggested that open market purchases would have more effect if they were made at a time of increased demand for bank credit and for reserve bank credit.35

Of the two banks proposing purchases, one favored monetary expansion and the other had the traditional concern about reserve bank earnings. Since interest rates had fallen and member bank borrowing had not been fully offset by an increase in bills and securities, the reserve banks’ income had fallen. Some of the banks faced losses. The conference agreed that supplementing the income of a reserve bank was not a “proper reason for the purchase of government securities,” and the matter ended. This issue arose again in the middle thirties.

The committee could not find any “proper reason” for engaging in either purchases or sales at the time. It was too early to provide for a seasonal demand that would not arise until fall. The only agreement reached was the empty statement that “conditions merit continuous careful observation of the Federal Reserve System in order that the System will be prepared to act promptly in the event that conditions further develop in such a way as to make actions seem advisable.”

No one attempted to set out the conditions that would make open market purchases advisable. Nevertheless, Harrison’s advocacy of purchases contrasts with the views expressed by several others. He believed that the “possible necessity for the purchase of government securities might be imminent at any time.” Another member called for immediate purchases “to remove every possible restraint from business as far as credit was concerned.” Still another suggested that the conference agree on a formula for the total amount of reserve bank credit as a guide to the desirable volume of purchases. None of these suggestions received much attention.

The minutes described money conditions as slightly “easier” because of the inflow of gold, the further decline in the amount of currency in circulation, and the reduction in member bank borrowing. But no one mentioned or appears to have noticed that the money supply (or demand deposits) had declined by more than $1 billion in the previous two months. Since most of the decline was in deposits, there must have been some recognition of the decline at major banks.

The governors not only were aware of the worldwide scope of the depression, they sensed that there was a connection between the depression and the New York money market. Harrison gave the standard explanation of the economic decline and the central role of real bills. There had been overproduction of “certain principal commodities,” accompanied by a “shortage of working capital and thus a restriction of purchasing power.” In the previous year, funds had been used for speculation, mainly in New York but in other markets as well. The recovery of world trade appeared to depend “in no small degree on a restoration of purchasing power through the medium of foreign borrowers on the New York money market, just as the recent recovery of domestic trade appeared to be much dependent on the new financing for domestic enterprise in the United States.”

This statement places Harrison well within the mainstream of Federal Reserve thinking and accounts for his failure to mention the substantial decline in demand deposits. However, within the common framework there are two main differences between New York and other parts of the System.

One is the minor point that New York developed more information and expressed more concern about current money market conditions and was more eager to take action to correct or offset money market changes. The second and more important difference within the committee concerns the interpretation of changes in member bank borrowing and interest rates and the System’s responsibility for bringing about further reductions in both. Some governors argued that the Federal Reserve should attempt to lower interest rates further by reducing discount rates and, if that failed, to lower interest rates and encourage member bank borrowing by engaging in open market purchases. Others—McDougal of Chicago and Norris of Philadelphia were leaders of this group—wanted to wait for the member banks to demand more reserve bank credit. In their view, the decline in borrowing meant that the System should sell securities to force an increase in member bank borrowing. With the possible exception of Governor Black, none of the governors argued for an aggressive purchase policy, and none professed a belief that such a policy would succeed.

Although the Board’s minutes indicate that the meeting was called to discuss New York’s program, Harrison did not present a program and, at the meeting, seemed most concerned about matters of timing and procedure, particularly the Board’s failure to agree quickly to requests for reductions in the buying rate on acceptances and discount rate changes. Young told the committee that “he had hesitated to vote favorably on the New York application for a three percent discount rate because of the position of the governors at the OMPC meeting on March 25.” This reopened a continuing disagreement. Harrison replied that decisions about discount rates were primarily the responsibility of the individual reserve banks and that “he did not believe the action of the Open Market Policy Conference should be regarded as in any way restricting freedom of action on discount rates.” Several governors agreed with Harrison, and the conference voted that discount rates “were not within its proper province and that the directors of any Federal Reserve Bank must feel free at any time to change the discount rate of their bank subject only to the review and determination of the Federal Reserve Board.”

This was a partial victory for New York. It removed any control that McDougal, Norris, or other governors might have had over the decisions about the discount rate at New York. Since New York’s 3 percent rate was one percentage point lower than the rates at ten of the eleven other banks, the banks with higher rates could not press New York to raise its rate by a formal vote of the conference. But it left New York, as before, dependent on the decisions of the Board.

To further strengthen New York’s position, Harrison argued for greater control of the acceptance rate by the reserve banks. The Board’s delays in approving applications for lower bill buying rates had left New York without “downward flexibility.” The committee voted to support Harrison, and after the meeting the Board sent a letter to all the reserve banks accepting the conference’s decision.

Although most of the decisions at the May meetings concerned operating procedures, they show that New York was no more isolated from the rest of the System in regard to procedure than in regard to policy. The conference was willing to support New York on day-to-day policy and to provide discretionary “flexibility” in managing the account. The Board and the conference were unwilling to allow New York to purchase and sell government securities on its own initiative and for its own account, but it is not clear that most would have opposed a program of open market purchases for the System if Harrison had supported the program vigorously. In fact, the members responded to Harrison’s statement that “the possible necessity for the purchase of government securities might be imminent at any time” by voting to reconvene or to act promptly on the recommendations of its five-man executive committee, which Harrison headed. When Harrison proposed open market purchases only ten days later, a majority of the conference voted in favor.

New York Seeks Expansion

Harrison’s approach to policy comes out clearly in the decision to purchase $50 million of securities early in June 1930. The discussions leading to the decision show the importance he attached to short-term factors affecting interest rates and money market conditions and his failure to develop a long-term program.36 They also show Harrison as a broker trying to reconcile differences between opposing groups. Three points stand out. First, Harrison twice changed his mind about the desirability of purchases. Both changes coincide with changes in the technical position of the money market. Second, Harrison did not suggest a program of steady expansion. In fact, he did not propose as expansive a policy as some of the New York directors urged on him. Third, Harrison never answered, and at times appears to have accepted, the main criticisms of the policy of expansion made by Norris and other opponents.

The first suggestion that purchases should be made came at the May 8 meeting of the directors of the New York Federal Reserve bank. Several of the directors spoke in favor, but others opposed on grounds that recovery in bond prices had been delayed by the floating of a large foreign loan— the $300 million German annuities loan. The directors who opposed purchases expected interest rates to resume their decline once the offering was sold. The directive recommended that Harrison discuss the possibility that open market purchases “may become desirable” with other governors and the Board. On May 19, two days before the Governors Conference, the executive committee of the New York directors remained divided. Most agreed that purchases of open market securities would be “inflationary” (which to them often meant that bond prices would rise), but some believed this danger should be faced “to check a decline in commodity prices.”

The following week, Harrison reported on the results of the Governors Conference to the executive committee of the New York directors. One of the directors remarked that there had been a net withdrawal of Federal Reserve funds from the money market during the preceding six months.37 He urged that these funds should “now be restored to the market by the purchase of government securities,” and he suggested that if this were done bankers would be encouraged to make loans to business borrowers. Then, in a statement that is considerably at variance with the real bills and Riefler-Burgess doctrines, a director pointed out that “if government securities should now be purchased in sufficient amount so that member banks would no longer be able to use the funds thus made available to pay off advances and rediscounts, expansion of bank investments would be forced and business would perhaps be stimulated.”

Support for purchases was rising in New York. Harrison reminded the directors that the governors had considered purchases but had voted not to take any action. Some of the directors disagreed with this policy. In their opinion, “it would be unfortunate if the banking system would not be used to facilitate recovery.” Three days later, on May 29, the full meeting of New York’s directors unanimously approved the report of the Open Market Policy Conference, then seized on the section that permitted the committee’s decision about open market policy to be reopened. Although only a week had passed, they voted that “it now seems desirable to undertake the purchase of government securities in moderate amounts.”

During the next few days, Harrison and Burgess telephoned the other governors to discuss their directors’ recommendation. Frederic H. Curtiss (Boston) believed that the situation had “retrogressed,” so he favored purchases of $20 million to $25 million for the next few weeks to test out the situation, “feeling that no harm would result and some good might be accomplished.” E.R. Fancher (Cleveland) also favored purchases, “believing that it might possibly help and that in any event it would be preferable to err on the side of ease rather than on the other side.” McDougal (Chicago) believed purchases would “do little or no good,” so he preferred not to purchase. Black (Atlanta) was very much in favor; Norris and Calkins were opposed.