Sector overview

Definition

Here is the GICS® definition by MSCI and Standard & Poor’s:

The Consumer Staples Sector comprises companies whose businesses are less sensitive to economic cycles. It includes manufacturers and distributors of food, beverages and tobacco and producers of non-durable household goods and personal products. It also includes food & drug retailing companies as well as hypermarkets and consumer super centers.

Companies

This sector contains 40 companies in the S&P 500 and 64 in the Russell 2000. Table 5.1 presents the 10 largest capitalisations at the time of writing, arranged in alphabetical order by ticker.

Table 5.1: Stock examples: S&P 500 Consumer Staples

S&P 500 strategy

Individually relevant factors

Here are the factors from my working list that are individually relevant for the S&P 500 Consumer Staples reference set.

Table 5.2: Individually relevant factors: S&P 500 Consumer Staples

Strategy description

I propose a strategy using two factors checked as individually relevant. Table 5.3 presents the strategy description.

Table 5.3: Strategy description: S&P 500 Consumer Staples

The rationalised interpretation is to choose companies that are cheap relative to their earnings estimates, and with a good net profit margin.

Basic simulation

Fig 5.1: Simulation data and equity curve: S&P 500 Consumer Staples

Hedged simulation

Fig 5.2: Simulation data and equity curve: S&P 500 Consumer Staples, Hedged

Consistency

Annualised returns with hedging by five-year periods:

Table 5.4: Consistency over five-year periods

Comment

Even in the basic version, the maximum drawdown and volatility look reasonable, which is a characteristic of a defensive sector. However, the hedged version gives a steadier equity curve. A Sharpe ratio above one and an even higher Sortino ratio points to a robust strategy. As explained previously, a Sortino ratio above the Sharpe ratio is a positive point: it means that the highest volatility is in gains, not losses.

The annualised return by five-year periods stays between 18% and 29%, which is remarkably stable. The sector is dominated by daily consumption products: it explains why companies are less sensitive to economic cycles.

Russell 2000 Strategy

Individually relevant factors

Here are the factors from my working list that are individually relevant for the Russell 2000 Consumer Staples reference set.

Table 5.5: Individually relevant factors: Russell 2000 Consumer Staples

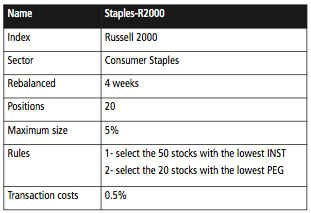

Strategy description

I propose the strategy shown in Table 5.6, using two individually relevant factors.

Table 5.6: Strategy description: Russell 2000 Consumer Staples

The rationalised interpretation is to select small companies that are not yet well known by institutional investors, and are cheap relative to earnings and expected growth.

Basic simulation

Fig 5.3: Simulation data and equity curve: Russell 2000 Consumer Staples

Hedged simulation

Fig 5.4: Simulation data and equity curve: Russell 2000 Consumer Staples, Hedged

Consistency

Annualised returns with hedging by five-year periods:

Table 5.7: Consistency over five-year periods

Comment

If we compare the hedged versions of the large cap and small cap portfolios, the returns and drawdowns are similar. As the Sharpe and Sortino ratios are higher with large caps, in this case there is no incentive to take a liquidity risk with small caps.

We note the same stability in five-year performance. Conservative investors might consider overweighting the Consumer Staples sector in their stock portfolio.