CHAPTER 5

During the year 1941 the activities of the Federal Reserve System were increasingly geared to facilitating the transition of the nation's economy to a war basis. The Federal Reserve authorities recognized that the primary function of the financial mechanism of the country in wartime is to help meet the requirements of war production.

The 1941 Annual Report of the Board of Governors of the Federal Reserve System1

During World War II, the Fed's primary purpose once again became to ensure the government could borrow all the funds it required to conduct the war at the lowest rate of interest possible – just as it had been during World War I. To carry out this responsibility, the Fed pegged the rate at which it would buy Treasury bills at 3/8 of 1% (37.5 basis points). This arrangement kept the cost of government borrowing low, but it required the Fed to buy government debt and to extend Federal Reserve Credit on a much greater scale than it had ever done before. This chapter describes the indispensable role the Fed played in making credit available to finance the war.

War Financing

Between June 1940 and the end of 1945, the US government raised approximately $380 billion. Of that amount, $152 billion (or 40%) came from taxes. The rest, $228 billion (or 60%) was borrowed. Of the amount borrowed, $133 billion came from selling government securities to non-bank investors. The rest, approximately $95 billion, was raised by selling government securities to the commercial banking system.2 Currency in circulation increased by nearly $20 billion, or 380%.

During the war, the Fed purchased $22 billion of government securities, thereby injecting reserves into the banking system that made possible both the banks' purchases of government securities and the expansion of currency. The Fed's 1945 Annual Report explained the Fed's purchases of government securities as follows:

Federal Reserve purchases of securities provided the basis for the rapid growth of currency in circulation and also supplied the banks with additional reserves needed to support the expansion of bank credit and deposits.

Federal Reserve purchases of 22 billion dollars of Government securities, together with 7 billion of reserves in excess of requirements held by member banks in 1940, provided the basis for a wartime currency expansion of 20 billion and a growth of 8 billion in member bank required reserves.3

The following sections describe the evolution of the Fed's assets and liabilities during the war in order to illustrate how the Fed made it possible for the government to borrow all the funds it required to win the war.

Balance Sheet

Assets

During the four years between 1941 and 1945, the Fed's total assets expanded by 80%, from $25 billion to $45 billion, as shown in Chart 5.1.

CHART 5.1 The Fed's Total Assets, 1914 to 1945

Source: Data from “The Federal Reserve System’s Weekly Balance Sheet Since 1914” and accompanying spreadsheet. Johns Hopkins University, SAE/No.115/July 2018. See Bibliography.

During the 1930s, a very large increase in the Fed's holdings of gold certificates had been responsible for the surge in the Fed's total assets. That was not the case between 1941 and 1945. During World War II the Fed's total assets jumped because the Fed acquired US government securities by extending Federal Reserve Credit.

The Fed supplied much more Federal Reserve Credit during the Second World War than during the First, as shown in Chart 5.2.

During World War I, the annual increase in Federal Reserve Credit peaked at $1.4 billion in 1918. By contrast, Federal Reserve Credit leapt by $4.2 billion during 1942 and peaked at an annual rate of increase of $7.5 billion during 1944.

Before World War II, Federal Reserve Credit outstanding had peaked at $3.4 billion in 1920. In 1922, it contracted back to $1.0 billion. In December 1941, the month the United States entered the war, it was still only $2.2 billion. Over the next 12 months, Federal Reserve Credit nearly tripled to $6.0 billion. By the end of 1945, the amount of Federal Reserve Credit outstanding had reached $24.5 billion, more than 10 times its prewar level (see Chart 5.3).

CHART 5.2 Federal Reserve Credit, Annual $ Change, 1915 to 1945

Source: The Federal Reserve4

Chart 5.3 shows that practically all of the Federal Reserve Credit took the form of credit to the government through the purchase of US government securities. The Fed did not acquire any other kind of securities, so there were no bills bought. Nor did the Fed extend credit through discounting operations, so its holdings of bills discounted were also at a very low level.

It must be noted that, although the Fed's primary mission was the same in both World War I and World War II, the method the Fed employed to accomplish that purpose was not the same. During World War I, the Fed had used discounting operations to finance government debt indirectly. As described in Chapter 2, the Fed had lent money to commercial banks at an interest rate that guaranteed that the banks would make a profit if they bought government securities. This enabled the government to sell as much government debt to the banks (and to the banks' customers) as necessary to finance the war.

During World War II, on the other hand, the Fed bought government securities directly through open market operations. The Fed's holdings of government securities increased from $2 billion in 1941 to $24 billion when the war ended in 1945.

CHART 5.3 Federal Reserve Credit and Its Components, 1914 to 1945

Source: Data from “The Federal Reserve System’s Weekly Balance Sheet Since 1914” and accompanying spreadsheet. Johns Hopkins University, SAE/No.115/July 2018. See Bibliography.

Meanwhile, the Fed's holdings of gold certificates declined during the war, as can be seen in Chart 5.4.

Notice in that chart that the assets acquired with Federal Reserve Credit became a larger component of the Fed's total assets than gold certificates in 1944, prefacing a change that would soon become the norm.

The composition the Fed's assets and liabilities underwent an extraordinary change as the result of the acquisition of so much government debt during the war, as shown in Chart 5.5.

Other than during a brief period in the aftermath of World War I, gold had always been the largest asset on the Fed's balance sheet. By the end of 1945, however, the Fed's holdings of government securities were 36% larger than its holdings of gold certificates. This was an important break from the past. The Federal Reserve Act of 1913, which created the Fed, was crafted to discourage the Fed from owning government securities. At that time, Congress believed that it was undesirable for the central bank to finance government debt.

CHART 5.4 The Fed's Total Assets: Gold vs. Assets Acquired with Federal Reserve Credit, 1914 to 1945

Source: Data from “The Federal Reserve System’s Weekly Balance Sheet Since 1914” and accompanying spreadsheet. Johns Hopkins University, SAE/No.115/July 2018. See Bibliography.

During World War I, the Fed had provided Federal Reserve Credit by lending money to commercial banks through discounting operations, where, as collateral, the banks offered the Fed loans they had made to their customers which, in turn, were collateralized by government securities. The Fed could then use the bills discounted that it obtained this way as “eligible collateral” to back the Federal Reserve Notes it issued.

CHART 5.5 A Breakdown of the Fed's Major Assets & Liabilities, 1914 to 1945

Source: Data from “The Federal Reserve System’s Weekly Balance Sheet Since 1914” and accompanying spreadsheet. Johns Hopkins University, SAE/No.115/July 2018. See Bibliography.

During World War II, the Fed bought government bonds outright through open market operations. This change was made possible by the Glass-Steagall Act of 1932 which amended the Federal Reserve Act to allow the Fed to directly use government securities as collateral to back the Federal Reserve Notes it issued. That amendment made it possible for the Fed to purchase government securities on a very large scale during World War II and to use those bonds as “eligible collateral” to back the very large amount of Federal Reserve Notes it issued during the war.

Liabilities

Notice in Chart 5.5, above, that while the growth in the Fed's holdings of government securities dominated the asset side of the Fed's balance sheet, it was the growth in Federal Reserve Notes that dominated the liabilities side.

Between 1941 and 1945, Federal Reserve Notes outstanding surged from $8 billion to $25 billion. This requires some explanation since when the Fed acquired the government securities it paid for them by making deposits into the reserve accounts at the Fed of the commercial banks from which it acquired the bonds. The act of making the deposit created the Federal Reserve Credit.

Had all other factors remained unchanged, the reserves held by member banks at the Fed, the dark gray line in Chart 5.5, would have increased by $22 billion, exactly in line with the amount of government securities purchased by the Fed. Other factors did not remain unchanged, however. The most important change was a surge in demand for currency.

During these years, individuals withdrew cash from their bank accounts for precautionary reasons. The public's desire to hold cash increases during wars and economic crises. Furthermore, businesses needed more cash to carry out production for the war. The government, too, needed more cash to conduct the war. Consequently, Federal Reserve Notes outstanding (the dashed line in Chart 5.5) tripled.

As the demand for currency grew, the Fed provided the Federal Reserve Notes to the commercial banks; and, in exchange for the Federal Reserve Notes, the Fed debited the reserve accounts those commercial banks held at the Fed. So, the increase in Federal Reserve Notes offset the increase in reserves that otherwise would have occurred when the Fed bought the government securities. This explains why Bank Reserves held at the Fed increased only modestly instead of one-for-one with the increase in the Fed's holdings of government securities.

By the time the war ended, the Fed had issued so many Federal Reserve Notes and created so much Federal Reserve Credit that its holdings of gold certificates were on the verge of becoming insufficient to allow the Fed to meet its legal obligation to hold 40% gold certificate backing for Federal Reserve Notes and 35% gold certificate backing for the reserves commercial banks held in their reserve accounts at the Fed. The Fed's gold cover ratio dipped to just 42% at the end of 1945 (see Chart 5.6)

CHART 5.6 Gold Cover Ratio: Ratio of the Fed’s Gold Reserves to Note and Deposit Liabilities, 1914 to 1945

Source: Data from Ratio of Reserves to Note and Deposit Liabilities, Federal Reserve Banks for United States, St. Louis Fed., 1914 to 1948

The drop in the gold cover ratio gave rise to concerns that the Fed's holdings of gold certificates would soon be insufficient to allow the Fed to issue any more currency or Federal Reserve Credit. To eliminate that possibility, Congress, in June 1945, reduced the amount of gold certificates the Fed was required to hold relative to the size of its liabilities. Afterwards, the Fed was required to maintain only 25% gold certificate backing for both Federal Reserve Notes and for the reserves commercial banks held in their reserve accounts at the Fed. This important revision to the Federal Reserve Act significantly increased the amount of credit the Fed could create relative to the amount of gold certificates it owned.

Here is how the Fed later described this unprecedented change:

… the decline in the Reserve Banks’ ratio of reserves to combined note and deposit liabilities during World War II threatened the Federal Reserve’s freedom of policy action. In this situation the Congress in 1945 deemed it wise to reduce the reserve requirements of the Reserve Banks from 40 per cent for Federal Reserve notes and 35 per cent for deposits to 25 per cent for each kind of liability.5

Federal Reserve Credit and Commercial Bank Credit

During the 1930s, the huge inflow of gold into the United States supplied the commercial banks with far more reserves than they needed to satisfy the statutory reserve requirements set out by the required reserve ratio. Even though the Fed doubled the required reserve ratio during 1936 and 1937, as described in Chapter 4, the banking system's excess reserves continued to grow as gold kept pouring into the country. Excess reserves peaked at $7 billion in October 1940.6 The following year, the demand for currency increased, causing Bank Reserves to fall, since when the Fed provides the banks with Federal Reserve Notes it debits their reserve accounts at the Fed, in exchange. Nevertheless, at the end of 1941, excess reserves still amounted to $3.1 billion.

Although that was an exceptionally high level of excess reserves compared with past norms, they quickly proved to be insufficient given the growth in demand for cash during the war. As noted above, the amount of Federal Reserve Notes in circulation expanded by $17 billion during the war, from $8 billion in 1941 to $25 billion in 1945. In 1941, total Bank Reserves amounted to only $12.5 billion, including the $3.1 billion of excess reserves.7

An increase in Federal Reserve Notes reduces Bank Reserves one-for-one. Therefore, the increase in currency in circulation would have quickly eliminated all Bank Reserves had the Fed not supplied the banking system with more reserves by acquiring $22 billion of government securities. Recall that when the Fed acquires a government bond, it pays for it by making a deposit into the reserve account at the Fed of the bank from which it acquires the bond. That transaction adds to that bank's level of reserves and, by extension, to the level of reserves of the entire banking system. In other words, by acquiring government securities, the Fed supplied the banking system with sufficient reserves to meet their legal reserve requirements, despite the extraordinary drain of reserves brought about by the large increase in Federal Reserve Notes in circulation.

It is also important to note that the banking systems' reserve requirements expanded during the war because of the very sharp rise in the amount of deposits held by the banking system.

Deposit Creation by Commercial Banks

Commercial banks create deposits by extending credit. This process will be explained in detail in Chapter 8. However, the extent to which this occurred during the war is so striking that it is useful to highlight it here.

It is counterintuitive that banks create deposits by extending credit. It seems as though banks should only be able to lend out deposits they already possess. That is not the case, however. Banks create deposits when they lend.

During the four years between 1941 and 1945, deposits at commercial banks more than doubled from $82 billion to $166 billion, as shown in Chart 5.7.

The deposits held by commercial banks grew because the banks bought government bonds. The government's budget deficit exploded when the war began. In 1941, the deficit was $5 billion, the largest since 1919 in the immediate aftermath of World War I. In 1942, the deficit jumped to more than $20 billion. The cumulative deficit during the four years of war came to $170 billion (see Chart 5.8).

CHART 5.7 Commercial Banks: Total Deposits, 1914 to 1945

Source: Data from Board of Governors of the Federal Reserve System (U.S.), 1935-. Banking and Monetary Statistics, 1914–1941; Board of Governors of the Federal Reserve System (U.S.), 1935-. Banking and Monetary Statistics, 1941–1970.

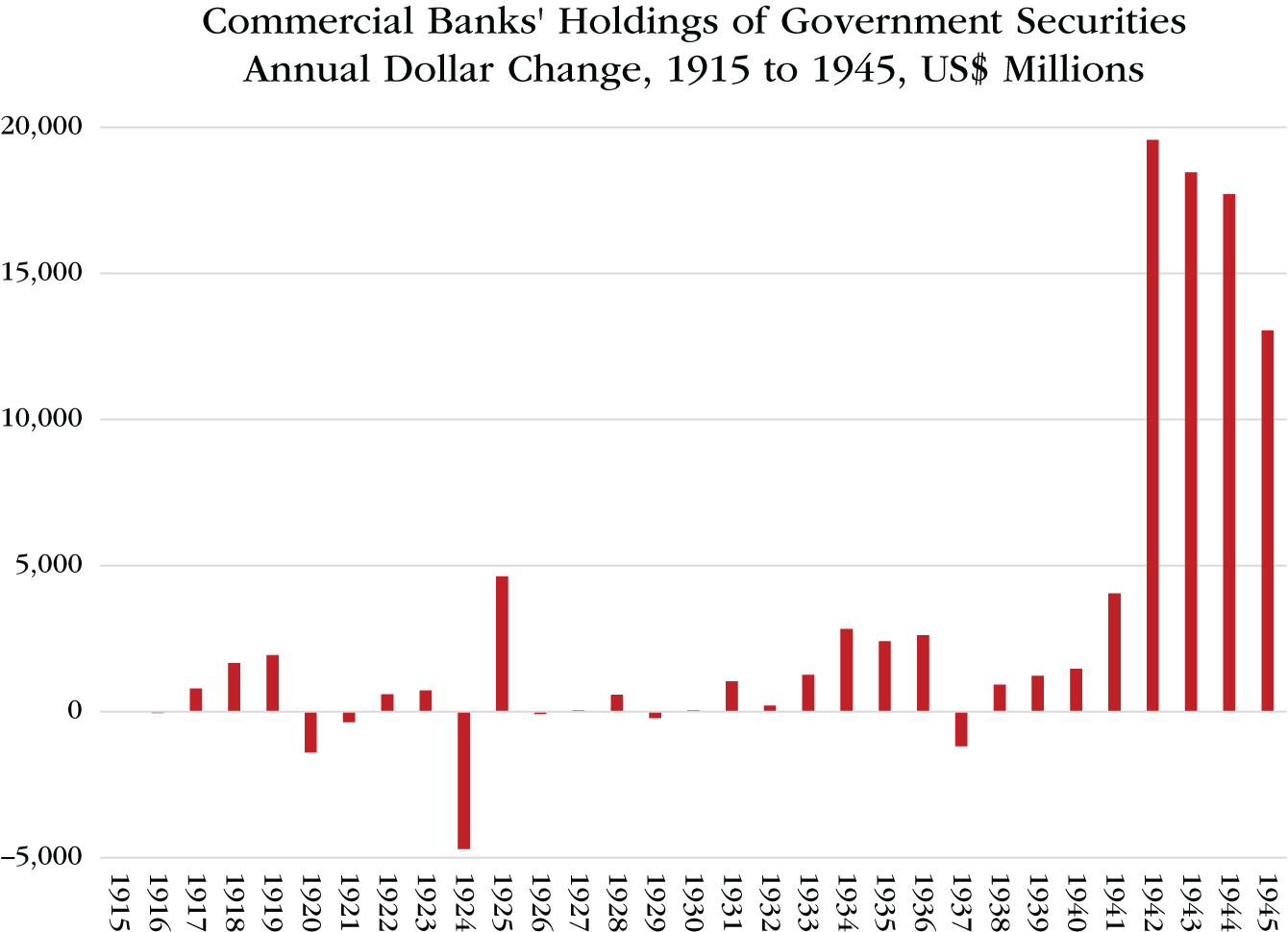

The commercial banks bought $69 billion of government securities during those four years, as depicted in Chart 5.9.

That took their portfolio of government securities up from $22 billion to $91 billion; and increased their total loans and investments from $51 billion to $124 billion (see Chart 5.10).

By the end of the war, the commercial banks holdings of government securities made up 73% of all their loans and investments combined (see Chart 5.11).

Each time a commercial bank bought a government bond from the government, the commercial bank financed its acquisition of that bond by creating bank credit, not by transferring funds that already existed. When the government spent the money it obtained from selling that government bond, whoever received the money the government spent deposited that money into their bank account, which added to the deposit base of the entire banking system. In 1941, the entire deposit base of the commercial banks was only $82 billion. By the end of the war, it had grown to $166 billion. Those deposits were created when the banks extended credit as they acquired government securities. Until then, they did not exist.

CHART 5.8 US Government Budget Surplus or Deficit (–), 1900 to 1945

Source: Data from the Office of Management and Budget, Historical Tables, the White House.

The process through which banks create deposits by extending credit will be explained in detail in Chapter 8.

Bretton Woods

Finally, it is necessary to mention the establishment of the Bretton Woods international monetary system and the constraints it placed on the Fed's “freedom of policy action.”

CHART 5.9 Commercial Banks' Holdings of Government Securities, Annual Dollar Change, 1915 to 1945

Source: Data from Board of Governors of the Federal Reserve System (U.S.), 1935-. Banking and Monetary Statistics, 1914–1941; Board of Governors of the Federal Reserve System (U.S.), 1935-. Banking and Monetary Statistics, 1941–1970.

As the end of the war approached, efforts to rebuild the global financial architecture got underway. The Bretton Woods system was created at the United Nations Monetary and Financial Conference held at Bretton Woods, New Hampshire, in July 1944. Its purpose was to establish a rule-based system to regulate international trade and monetary relations so as to promote balanced growth in international trade. The conference was a tremendous success. Never before had an “international monetary system” been created by an agreement between nations. The gold standard had simply emerged over the course of centuries because gold had proven to be the most reliable medium of exchange.

CHART 5.10 Commercial Banks: Total Loans & Investments vs. Holdings of Government Securities, 1914 to 1945

Source: Data from Board of Governors of the Federal Reserve System (U.S.), 1935-. Banking and Monetary Statistics, 1914–1941; Board of Governors of the Federal Reserve System (U.S.), 1935-. Banking and Monetary Statistics, 1941–1970.

The Bretton Woods system was designed to replicate the best aspects of the gold standard. It was structured to prevent member countries from pursuing unfair trade practices that had contributed to the Depression. In particular, it sought to prevent unilateral currency devaluations and trade tariffs.

Simply returning to the gold standard was not an option. By the end of the war, the victors held most of the world's gold. Gold was not distributed widely enough around the world to allow international trade to recommence. The United States had by far the largest gold holdings, followed by France. Moreover, the United States had become the largest creditor nation in history.

CHART 5.11 Commercial Banks' Holdings of Government Securities as a Percentage of Total Loans & Investments, 1914 to 1945

Source: Data from Board of Governors of the Federal Reserve System (U.S.), 1935-. Banking and Monetary Statistics, 1914–1941; Board of Governors of the Federal Reserve System (U.S.), 1935-. Banking and Monetary Statistics, 1941–1970.

To overcome this unequal distribution of gold, the Bretton Woods Agreement established a system of fixed exchange rates in which the US dollar served as the anchor currency. The United States pegged the dollar to gold at the fixed rate of $35 per ounce; and agreed to buy or sell gold to or from the monetary authorities of other countries in order to prevent any fluctuation in the dollar's value relative to gold. Other member countries undertook to maintain the value of their currency near an agreed par value, allowing fluctuation within only a narrow margin. In practice, most countries pegged their currency to the dollar and intervened by buying or selling dollars in order to prevent any significant change in their currency's value relative to the dollar. They also had the right to exchange the dollars held by their monetary authorities for gold held as reserves by the United States via the “gold window” at the Treasury Department.

The monetary authorities at the conference believed that no international trading system could survive for long if trade between nations did not balance. Trade had to be paid for. Imbalances could be financed on credit only over the short run, at best. To ensure trade did balance, the Bretton Woods system was designed to have the same automatic adjustment mechanism as the gold standard. Trade deficits would cause monetary contraction and trade surpluses would cause monetary expansion, in both cases setting off macroeconomic forces that would restore balance. During the conference, the architects of the system created the International Monetary Fund (IMF) to help ease the adjustment process.

The international monetary system created at Bretton Woods worked well for a quarter of a century. So long as the world's leading industrialized nations abided by its rules, it provided a structure in which international trade could (and did) flourish.

However, the Bretton Woods systems imposed constraints on the Fed. If the Fed undertook expansionary monetary policy (i.e., created too much Federal Reserve Credit), it could result in gold leaving the United States. For example, if the Fed created too much Federal Reserve Credit, the US economy would strengthen, employment would rise, consumption would increase, US demand for foreign products would grow, ultimately leading to an increase in imports entering the United States and a deterioration in the country's trade balance. A trade deficit would have to be settled by sending dollars abroad. The recipients of those dollars had the right to exchange them for US gold. If the US lost too much gold, there would not be enough gold left in the country to allow the Fed to meet its obligation to hold gold backing for Federal Reserve Notes and for the Bank Reserves held at the Fed. Furthermore, if the trade deficit persisted for long enough, the United States would lose all its gold, at which point it would become impossible for the United States to allow other countries to convert any more dollars into gold. The same outcome would occur if the Fed reduced interest rates to a level substantially below the interest rates of other large countries. Dollars would have left the United States to profit from the higher interest rates offered abroad.

Therefore, the Bretton Woods system forced the Fed to think carefully before providing monetary stimulus to support economic growth. Dollar convertibility was the cornerstone of the Bretton Woods system. The system would not survive if the United States was unable to meet its obligations to allow dollars to be converted into gold. Eventually, the Bretton Woods system did collapse for exactly that reason. However, the breakdown did not occur until 1971. Until then, the Fed had to consider how its actions would impact the United States' balance of payments and its gold stock.

Conclusion

The Fed provided invaluable service to the country during the war. Its 10-fold expansion of Federal Reserve Credit allowed the government to borrow as much money as it required to win the war, while simultaneously underwriting a 200% increase in Federal Reserve Notes in circulation. In 1945, Congress significantly increased the Fed's power to create credit by reducing the amount of gold certificates the central bank was required to hold relative to its notes and reserve liabilities.

When the war ended, it was generally assumed that the Fed would gradually return to functioning as the relatively passive institution its founders had created in 1913, just as it had done following World War I. Chapter 6 explains why that did not happen. World War II marked a turning point for the Fed. There would be no going back.

Notes

1. The 1941 Annual Report of the Board of Governors of the Federal Reserve System, p. 1.

2. The 1945 Annual Report of the Board of Governors of the Federal Reserve System, p. 1.

3. The 1945 Annual Report of the Board of Governors of the Federal Reserve System, pp. 9–10.

4. Data for 1914 to 1917 from “The Federal Reserve System’s Weekly Balance Sheet Since 1914” and accompanying spreadsheet. Johns Hopkins University, SAE/No.115/July 2018. See Bibliography.

Data for 1918 to 1945 from The Fed’s 2017 Annual Report, page 306

5. Purposes and Functions, The Federal Reserve System, pp. 174–175. https://fraser.stlouisfed.org/files/docs/historical/federal%20reserve%20history/bog_publications/bog_frs_purposes_1963.pdf

6. The 1940 Annual Report of the Board of Governors of the Federal Reserve System p. 52.

7. The 1941 Annual Report of the Board of Governors of the Federal Reserve System p. 48.