Chapter 9

Tomáš Klír

Introduction

On the threshold of the early modern period, we record deep changes in the social, economic, and demographic regimes of European peasant society. The early modern peasantry seems to us in comparison with the late medieval as strongly monetarised, commercialised, oligarchised, and also saturated with sophisticated credit regimes. This was accompanied by changes in economic management, improvement living standards, and the beginnings of consumer society. The causes of the peasantry transformation are sought through the combined effects of external and internal factors that have generated an increasing financial burden on peasant households and the need to regularly obtain high amounts of cash. Attention is drawn to demographic growth, the price revolution, state fiscalism, changes in the practice of property disposition, and inheritance law and the difficult position of the primary heirs of farmsteads within the primogeniture. However, our knowledge is very erratic. While the social and economic structures and processes within the early modern peasantry are well known in detail, the situation in the late Middle Ages is rather modelled and remains hypothetical (for the Czech Lands in particular Kostlán 1987; Cerman & Zeitelhofer 2002; Chocholáč 1999, 2005; Procházka 1963; Čechura 1990; Míka 1960, pp. 208–21). The lack of late medieval data is characteristic of the whole of Central Europe (Cerman 2008). The Eger (Cheb) city state is the exception where we can see inside the peasant economy thanks to the unique interplay of fiscal and court records (Klír et al. 2016). Our question is what was the degree of monetarization of the Eger peasantry and what was the nature and extent of the peasant credit market in the late Middle Ages?

We narrow our view to a relatively short but sufficiently representative period of 1435/1442–1456 because the highest quality source base is available for this period. In doing so, we build on previous studies (Klír et al. 2016; Klír 2018, 2019). We will focus only on the ‘subject’ farmsteads that prevailed in the Eger city state (95%); we leave aside ‘free’ farmsteads.

Region and sources

In the late Middle Ages, the Eger region had the status of an imperial pledge to the Bohemian king (1322), later the Crown of Bohemia, and its territory was already more or less stabilised geographically (after 1413). Territorial power was in fact executed by the city council in Eger (Cheb), which was materialised by the annual collection of the land tax and organisation of the land militia. Eger’s city state in the 15th century had a size of around 400 km2, included 11 parishes with approximately 130 rural settlements, 1,000 farmsteads and roughly 10,000 denizens (Klír et al. 2016, pp. 31–58, 124–7; Klír 2019, pp. 344–6). In terms of geographical and market conditions, its entire territory can be divided into several zones, from the agro-climatically optimal part of the Eger Basin along the River Eger (400–500 m a.s.l.) to foothill, climatically harsh and agriculturally unfavourable areas (500–650/700 m a.s.l.). Agricultural production in the Eger city state was characterized by a three-field fallow system and, especially in the Eger Basin, market-oriented cattle breeding (Klír 2018, pp. 177–9, 201–2, 224; Klír 2019, pp. 345–6).

The period of 1435/1442–1456 was relatively calm, defined, on the one hand, by the so-called Hussite and on the other the Hungarian wars. At the same time, it was a period of a power vacuum when the power of the Eger city council peaked (Klír et al. 2016, pp. 19–21). We judge according to the geographically relatively close Nuremburg data that the period after 1440 until 1465 was also abnormally stable as whole also in the Eger city state, in terms of crop yields, demography, and prices (Bauernfeind 1993, pp. 178–201).

The main source for knowledge of the Eger peasantry in the late Middle Ages are the fiscal sources. They are the registers of the land tax (1392–1757) and registers of the city tax (1390–1758). Thanks to this high-quality source base, we are informed on the monetary value of all of the real estate and moveable property in the countryside and in the city. For the ‘subject’ tenants, we know not only the amount of the land tax, but also the land rent (Klír et al. 2016; Klír, in print). The so-called debt protocols, kept at the Eger city court, are crucial for understanding the credit market (Schuldprotokolle, 1387–1496).

All of the peasant households which held a farmstead paid the land tax. The land tax was property, progressive, and the tax rate fluctuated most often in the range of 1.5–3.0%. The amount of the tax was determined according to the monetary value of the (1) tenure right to the farmstead; (2) horses, cattle, and sheep; (3) the so-called non-farmstead plots; (4) other rights, properties, and moveable property (Klír et al. 2016, pp. 144–57, 175–7; Klír 2018, pp. 181–2).

All of the members of the city community (burghers) paid the city tax. In the 15th century, the city tax was assessed both as a fee for a fireplace (chimney) and further as a progressive tax for all the real and moveable property (tax rate of 1.5–2.0%). The rural properties of the burghers were also subject to the city tax.

The tenants had a relatively wide disposition, family property and inheritance rights to the ‘subject’, that is ‘purchased’ farmstead. The farmstead was usually passed as whole to only one of the heirs (the so-called primary heir), and the remaining members of the family received an ideal share from its monetary value. A distinction was made between full-fledged peasant farmsteads (‘Hof’) and smallholder/ cottager farmsteads (‘Herberge’) which usually did not own a team of horses. Full-fledged peasant farmsteads predominated in the Eger city state (77–80%; Klír et al. 2016, pp. 146–50; Klír 2018, pp. 184–91; Klír 2019, p. 346; cf. Procházka 1963; Cerman 2008, pp. 58–64).

In addition to inalienable land, firmly bound to ‘subject’ farmsteads, there were other, independent and separately taxed plots in the Eger city state, subject to ‘fief’ law, which the holder could relatively freely dispose of (so-called non-farmstead plots). Their absolute share in the land fund was relatively low (estimated at 2–5% of fields, ca 25% of meadows) but the economic importance was high (Klír et al. 2016, pp. 152–4; 2018, p. 185).

The landlords’ rights in the late medieval Eger city state were extraordinarily fragmented and dispersed. Estates in the sense of economically consolidated dominions were lacking. Land rent most often had in-kind nature (grain); the labour rent was minimal. This all indicates a relatively weak landlord control of the property transfers of peasant land (Klír et al. 2016, pp. 159–61, 237–41; Klír 2018, pp. 187–8).

Feudal rent was comprised of the land rent, land tax, and church tithe. The land rent had a fixed nature; it reflected the size of the peasant holding and favoured some ‘subject’ farmsteads. The land tax was progressive and in principle respected the level of commercialisation and monetarisation of the farmsteads. Both forms of feudal rent drew on the seasonal agricultural surplus and were complementary in time and physically. The land rent drew directly from the grain surplus (collection on St Michael); the land tax indirectly on the animal surplus (collection after St Martin). The church tithe was of an extremely variable nature, compared to the rent of the land, it was 10–25% (Klír, in print). The analysis of land rent, land tax, and church tithe showed that the feudal rent as a whole was set to a minimum production level of farmsteads, below which they did not reach even in the agriculturally unfavourable years in the monitored time segment. Most peasants thus surely had an available surplus in hand, the specific amount of which fluctuated year-on-year (Klír, in print).

Monetarisation

The question is how much cash the peasants needed to pay feudal rent (external factor) and how much to potentially pay siblings or buy a farmstead, livestock, and non-farmstead plots (internal factor). The first part of the question is answered by the analysis of the above-mentioned land tax and land rents in the register of the land tax from 1469 (Klosteuerbuch, 1469). The second part of the question is answered by an analysis of monetary value of the properties in the tax register from 1438 and taxation book from 1456 (Klír et al. 2016; Klír 2018, pp. 188–98). An essential prerequisite for the interpretation is naturally knowledge of the prices of grain and cattle (Table 9.1).

Table 9.1 Indicative price of grain and livestock in the Eger city state in 1438 and 1456

|

Commodity |

Draught horse |

Cow |

Calf |

Sheep |

1 ‘Kar’ of grain (ca 3 hectolitres) |

|

Price |

120–140 gr. |

50–55 gr. |

8 gr. |

7 gr. |

15 gr. |

Note: gr. – Prague groschen.

Source: Klír 2018, pp. 191–3; cf. Vaniš 1981; Míka 1959.

As far as the cash necessary to pay the feudal rents, the situation of individual families varied enormously. Considering that our aim is a comparison with the early modern situation, we can simplify reality to the average values (Table 9.2). The land tax had an exclusively monetary form, representing for the ‘Hof’ farmstead on average an annual burden of 28.5 Prague groschen and for ‘Herberge’ farmstead 11.5 Prague groschen. Land rent was mostly in kind and, therefore, did not force most peasants to raise cash. Only one-fifth of the peasant farmsteads had to pay the land rent in cash, on average each was required to pay 29.5 Prague groschen annually. If the land tax met with a cash land rent, the average financial burden was 68 groschen. We can summarise that in the monitored period the average peasant household in the late medieval Eger city state needed to acquire at least 30–60 Prague groschen of cash each year. That corresponded to the price of one and a half cows, or 8–16 hectolitres of rye. At the same time, low prices mean that the annual reproduction of the peasant farmstead was not extremely expensive.

Table 9.2 Overview of average monetary values of peasant property (1438, 1456) and cash and in-kind burdens on Eger ‘subject’ farmsteads of the year (1469)

|

‘Subject’ farmstead |

Number of cases |

||||

|

‘Hof’ farmstead |

‘Herberge’ farmstead |

||||

|

Average price |

Purchase right |

1438 |

11 ss 45 gr. |

5 ss 18 gr. |

609 / 86 |

|

1456 |

13 ss 42 gr. |

632 |

|||

|

Horses and cattle |

1438 |

11 ss 38 gr. |

3 ss 28 gr. |

820 |

|

|

1456 |

12 ss. 11 gr. |

655 |

|||

|

1 ploughed ‘Morgen’ (ca 0.57 ha)* |

2 ss 12 gr. |

81 (1438) / 75 (1456) |

|||

|

1 meadow ‘Morgen’ (ca 0.57 ha)* |

4 ss 30 gr. |

86 (1438) / 111 (1456) |

|||

|

Average annual land tax (1438) |

28 gr. |

11.5 gr. |

763 |

||

|

Average annual land rent only in cash (22.5% of farmsteads) |

29.5 gr. |

132 |

|||

|

Average annual land rent only in grain (71% of farmsteads) |

6.8 grain ‘Kar’ (ca 20 hectolitres) |

416 |

|||

|

Church tithe |

10% – 30% of the amount of the land rent |

31 |

|||

Notes: gr. – Prague groschen; ss – threescore Prague groschen* – only a minority of peasant families owned this

Source: Klír et al. 2016; Klír 2018, pp. 190–6; Klír, in print.

The average monetary value of the tenure right to a ‘subject’ farmstead, the livestock and non-farmstead plots is shown in Table 9.2. The relatively low price of the tenure right for the farmsteads is striking. It was true for the ‘subject’ farmsteads that the value of the tenure right was about half the value of all property, the other half was the value of livestock. If the peasant households also owned non-farmstead plots, then the value of the tenure right was on average one-third of the overall value, the second third was the livestock, and the third was the non-farmstead plots (1:1:1). Or, the average ‘subject’ farmstead in and of itself could be acquired for the price of 10–12 cows, or 3 draught horses.

The contrast to the early modern price relations is clear. Although the early modern situation has not yet been analysed for the Eger city state, we can help by comparison with other well-known regions. For example, for the area of the Saxon town of Grimma near Leipzig, it was established on the basis of data from the Turkish tax registers of 1542 that the livestock value was only about 10% of the total value of the peasant property (Schirmer 1996, p. 62). Similar relations are also supported by data from the oldest land registers for Bohemia or Moravia (Míka 1960, pp. 213–18, 352–405; Chocholáč 1999, pp. 72–97). Horses and cattle were less than one-tenth of the estimated price of rich farmsteads in the grain areas. The ratio of the monetary value of horses and cattle to the estimated value of the courtyard with land fluctuated around 1:8 (Hanzal 1963, pp. 42–4).

Thus, although the norms of property disposition and inheritance law in the late medieval Eger city state did not in principle differ from those we know in early modern Bohemia, their economic and social consequences for the functioning of peasant communities were fundamentally different – due to different price relations and demographic regime. Thanks to the relatively low value of the tenure right to the ‘subject’ farmstead, the position of the primary heir apparent in the Eger city state was not in any way economically burdensome because the obligations to the other heirs could be relatively easily and immediately settled in natural commodities, non-farmstead plots, or relatively attainable cash. Model considerations as well as specific examples show that neither a loan nor repayment of shares was necessary in most cases.

We can formulate the hypothesis that the late medieval peasantry of Eger was not forced to be in intensive interaction with the market. We speak of course on the level of the average because the Eger city state was not homogeneous and it is necessary to count with differences between the agriculturally advantageous and foothill zones, or the small and large farmsteads. The hypothesis of generally low level of the monetarization and commercialization of the peasantry will be tested in the next chapter using a credit market analysis.

Credit market

The relationship between the peasant society and the credit market has attracted the long-standing systematic attention of historians, as shown by the number of monographs, volumes, and a special issue of the journal ‘Continuity and Change’ from 2014 (e.g. Briggs & Zuijderduijn 2018; Schoefield & Lambrecht 2009). At this point, we will use the established methodological framework to examine the nature, structure, availability, function and importance of the credit market in the late medieval Eger countryside.

Knowledge of the Eger credit market is made possible by the protocols of the city court. The Eger city court sat relatively regularly, namely on Mondays and Fridays, extraordinarily on Wednesdays. A wide spectrum of people who had receivables from Eger burghers – not only the Eger burghers themselves, burghers from other towns or Jews, but also the peasantry – ‘subject’ and ‘free’ tenants from the countryside could turn to the court. The city court and its protocols were a key institutional element providing guarantees for debt recovery and the efficient functioning of the urban-rural credit regime. What is important is that the peasantry was given the same guarantees as the inhabitants of the city, which was an incentive to enter the credit market.

The court protocols recorded (1) the petitions of the creditors on the debtors; and (2) to a lesser extent also the declarations of the debtors on the specific obligation, repayments and guarantees. In the first case, we see formal and informal credits, which failed. In the second case, they are formal credit, specifically loans, regardless of whether they were repaid. Those recorded were mainly those loans, with which the creditor wanted to secure his rights and the enforceability of the debt. It is thus not surprising that records of Jewish creditors predominate. The creditor usually was satisfied with the admission of the debtor himself before the city court, only in one case is also the presence of his landlord documented.

The subject of our analysis are the petitions from 1442–1456 and the declarations of the debtors from 1435–1456 (Schuldprotokolle, 1429–1439; 1439–1452; 1452–1470).

The testimony of the petitions

When the creditor turned to court, he first brought the first petition, and if the claim was not paid, it was followed by the second and finally the third petition, forfeiture of the pledge, or other remedial action was accepted. Both the amount due (principal) and interest (‘damage’ of the creditor) were regularly recorded. It is fundamental that even small debts, less than 10 Prague groschen, were discussed before the court in the period in question, so the earlier city council’s resolution was not applied, namely that only the enforcement of debts from a certain amount of money was to be recorded in the books (Schuldprotokolle, 1387–1416, pp. 1–3).

We have identified, among the 12,276 petitions from 1442 to 1456, a total of 257 (2.1%) cases when the plaintiff came from a rural settlement or market village, whether from Eger city state or outside of it (Table 9.3). Of these petitions, 165 were primary; the rest were repeated petitions. Among the plaintiffs, it was possible to identify 133 unique individuals. The majority of them were peasants. In the registers of the Eger land tax, it was possible to find 61 plaintiffs – peasants directly in the year of the petition. Among the other plaintiffs, a significant share were rural millers (9% of the plaintiffs; 17% of the petitions) and even parish priests were represented.

Table 9.3 Amount of the debt for claims sued by plaintiffs from outside Eger before the city court in 1442–1456

|

Amount of the debt (Prague groschen) |

Primary petitions |

|||

|

number |

% |

Eger ‘butchers’ |

%* |

|

|

7–30 |

50 |

31.6 |

12 |

24.0 |

|

31–60 |

47 |

29.7 |

17 |

36.2 |

|

61–120 |

31 |

19.6 |

12 |

38.7 |

|

121–300 |

23 |

14.6 |

6 |

26.1 |

|

300–3,600 |

7 |

4.4 |

0 |

0.0 |

|

Total |

158 |

100.0 |

47 |

29.7 |

* – share within the shown monetary category.

Source: Schuldprotokolle, 1439–1452; 1452–1470.

The first question is what type of credit the claims concerned. Was it a failed loan, or a sale on credit? The specific cause of the debt can only be traced exceptionally in the protocols – unpaid wages occurred three times, an unspecified trade transaction twice, loaned money twice, likely an unpaid inheritance share once, debt created by the sale of grain twice, and of dill once. Nevertheless, a total of 47 primary petitions (28.5%) were brought against burghers – butchers, six petitions concerned Eger millers and five weavers (c.f. Losungsbuch, 1446). On the level of the general tendency, we therefore assume that the petitions relate predominantly to sale credit that failed, or that they were unpaid wages. In other words, among the plaintiffs, there are mainly the suppliers of the city market for meat, grain, and wool (both direct producers and intermediaries). In this case, the credit market and its institutional security by the city court indirectly helped to supply the city efficiently, as they compensated for seasonal fluctuations and secured agricultural commodities even in a situation of cash shortage.

The second question is how much the individual petitioned debts amounted to. This also tells us how much money the peasants were getting at one time by selling their products. The amount of monetary debt varied in a wide range from seven groschen to 60 threescore Prague groschen. Nevertheless, a total of 61% of the debt can be considered to be small, not exceeding one threescore Prague groschen. Another 20% of the debts were between one and two threescore of Prague groschen. The boundary of 10 threescore Prague groschen was crossed only exceptionally (three cases). Receivables from Eger butchers had the highest representation in the category of a half to two threescore Prague groschen. This range corresponds to the assumption that normal trade with agricultural, especially livestock, products was behind the large part of the petitioned claims.

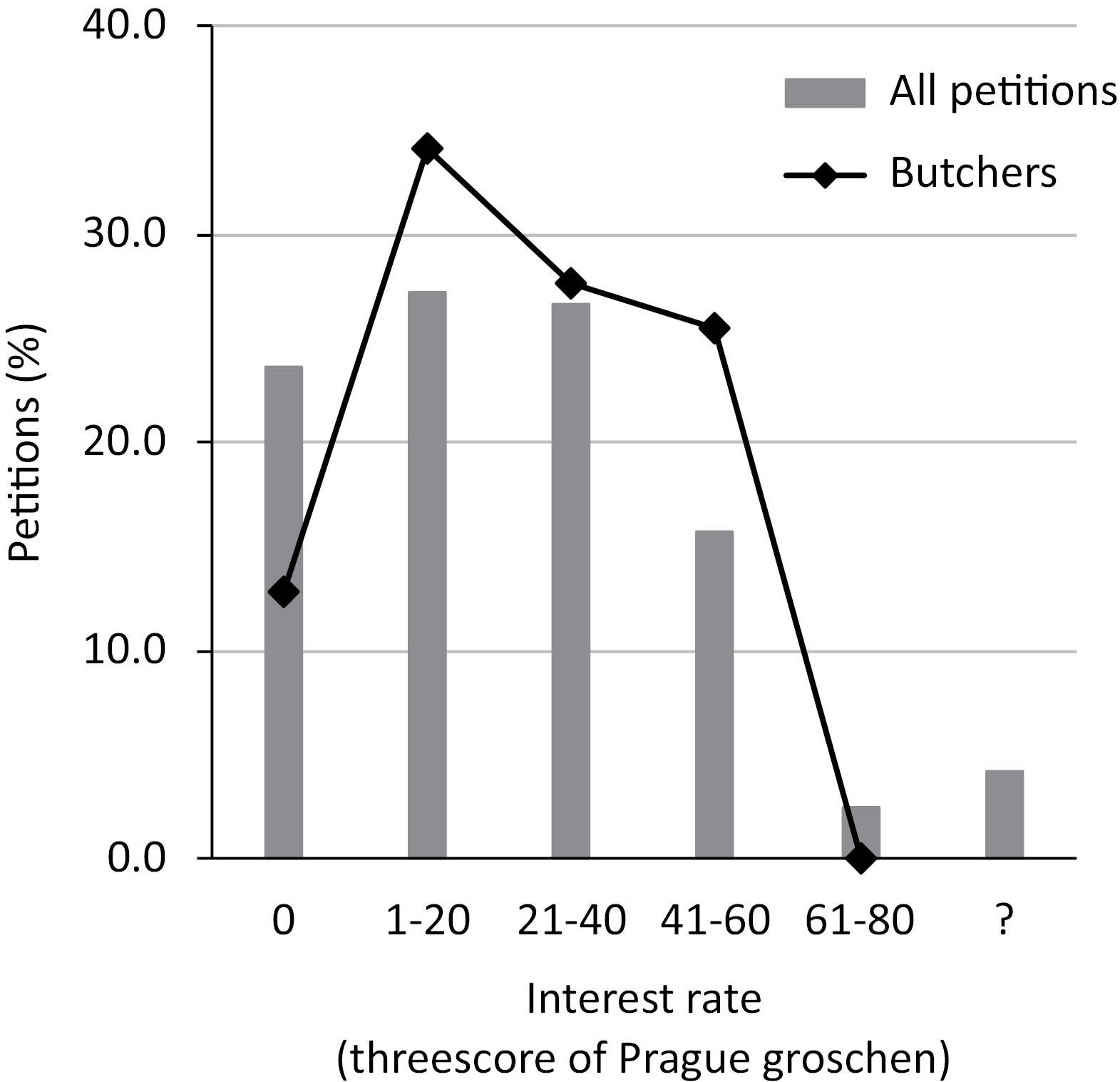

The third question is how much interest was associated with the credit. We unfortunately do not know the time between the creation of the debt and the deadline for its payment. The records of the petitions listed the interest rate for loaning the money in 119 of the cases (72%); in 46 cases, it was interest-free debt. In total volume, the amount of the petitioned debts was 295 threescore Prague groschen, of which 177 threescore was connected with an interest in the amount of 43 threescore (24%). The interest rate fluctuated in a wide range of 7–79%. Most often, the interest was in the interval of 7–20% and 21–40%, only exceptionally it exceeded 60% (Figure 9.1). The analysis did not show a convincing dependence of the amount of interest on the size of the principal, the occupation of the debtor, the social status of the plaintiff or creditor, the number of petitions, or the year of the petition.

Figure 9.1Amount of the interest for loaning money.

Source: Schuldprotokolle, 1439–1452; 1452–1470.

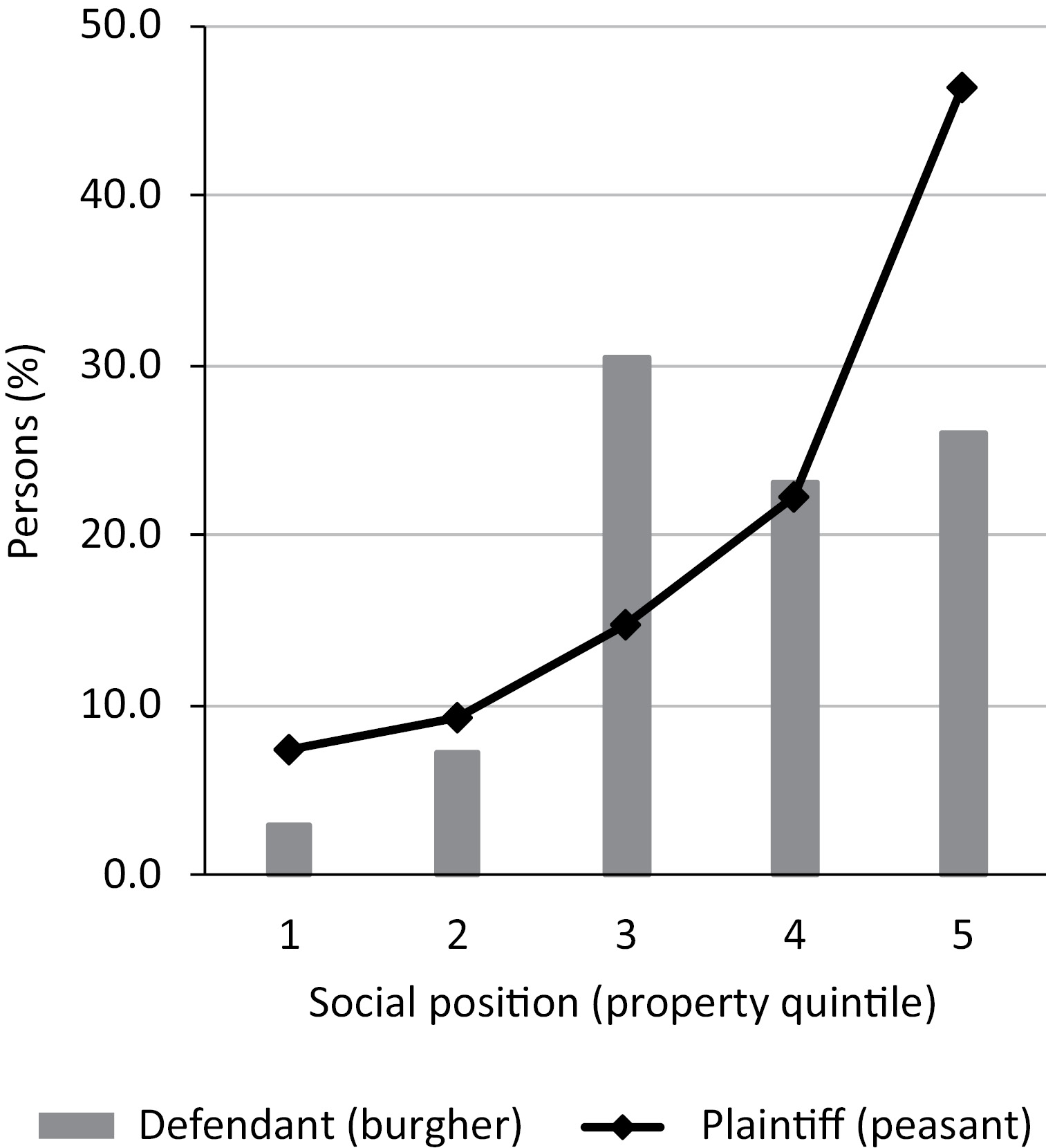

The fourth question is what the property positions of the plaintiffs (peasants) and defendants (burghers) were. We have determined the status of the peasants based on the land tax attributed in the year of the petition, the status of the burghers according to the city tax register from 1446. Of the statistical methods, we have used quintile analysis, that is we ranked all taxpayers according to the prescribed tax and divided them into five categories from the poorest to the richest (Klír 2018, pp. 202–4; 2019, p. 347). In total, we have evaluated the status of 54 plaintiffs in 69 petitions and 31 defendants in 62 petitions (Figure 9.2). The richest peasants predominated among the plaintiffs. The status of the defendant burghers was more balanced, with moderately wealthy and very wealthy burghers represented equally. It follows that the city’s foodstuffs market was mainly supplied by the richest peasants who were willing to sell to the burghers on credit.

Figure 9.2Social status of the creditors and debtors in the Eger city state, 1442–1456 (sale on debt).

Source: Klosteuerbücher, 1442–1456; Losungsbuch 1446; 1439–1452; 1452–1470.

The testimony of the records of the loans

The protocols also contain records of the loans. In them, among others, the term of the anticipated repayment was listed, or the repayment calendar, often also a pledge. The interest rate for loaning the money was never given; many records were later crossed out, that is the loan was repaid.

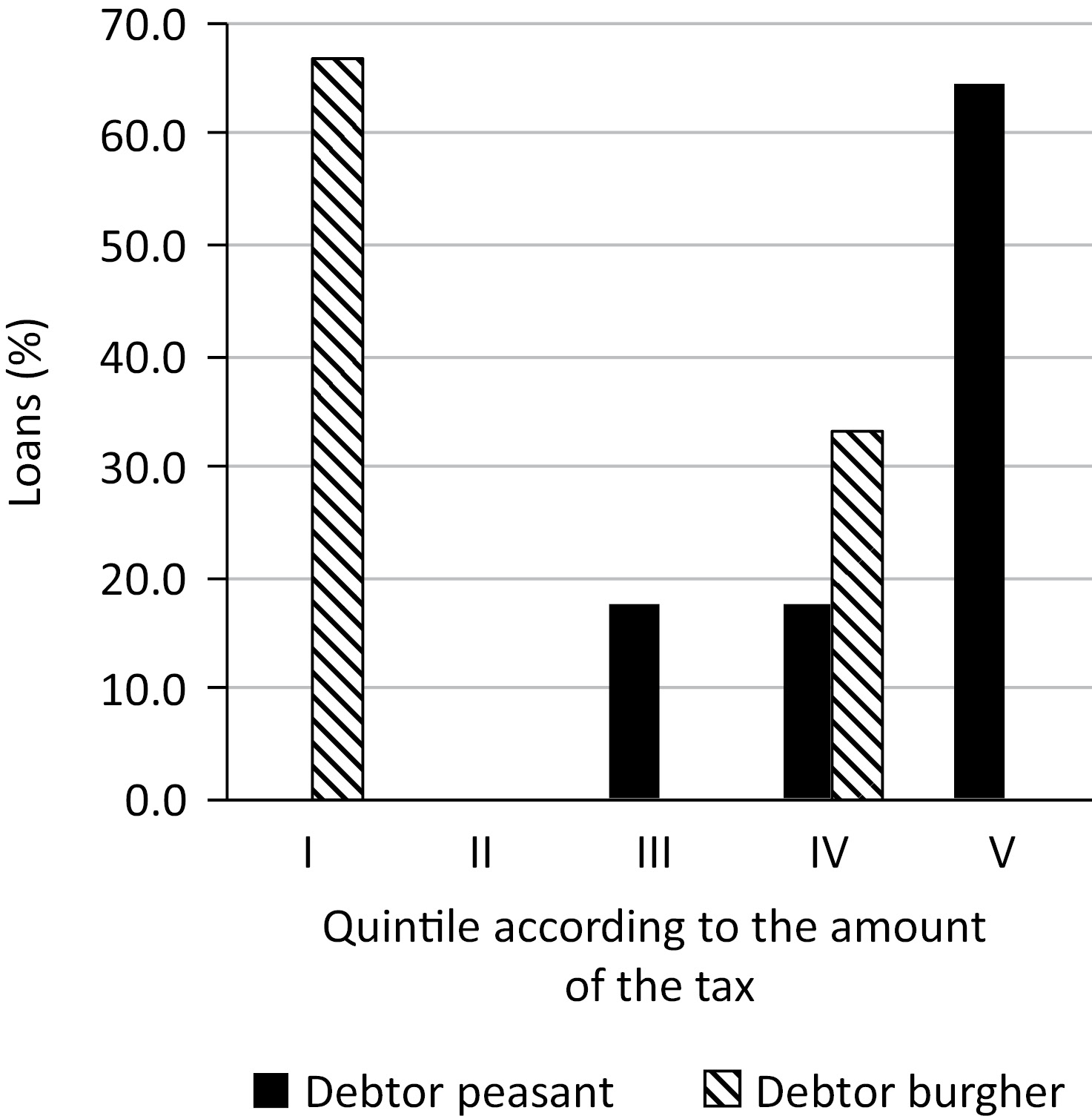

We have analysed the protocols from 1435–1456 which contained a total of 779 declarations of debtors on the acceptance of the financial obligation. Of this number, only 36 (4.6%) concerned peasants, demonstrating their low level of involvement in the market with formal loans. We identified the peasants according to the predicate and then searched in the registers of the Eger land tax (Klosteuerbuch, 1435; 1438; 1441–1456).

The records of the loans show the reverse direction of the flow of economic resources than the records of the petitions. In 86% of the records, the peasant was the debtor and the burgher the creditor. Behind a total of 31 records of loans, there were 23 individual peasants because some peasants bound themselves to debts repeatedly. We most often encounter individual peasants (61%), the representation of a ‘society’ of the two peasants and a ‘society’ of a peasant with a burgher was approximately equal (17 and 22%). The Eger Jews predominate among the creditors (61%); the rest fall to burghers. A declaration where a peasant was the creditor of another peasant was not recorded even once.

Some studies point to the important role of millers in the rural credit market (Guzowski 2014, p. 134). In the analysed court protocols, millers only occurred twice among individual debtors. Rural millers did not appear among the creditors.

Regarding the social status of the peasants and the burghers in the year of the record of the declaration, we again relied on the testimony of the land tax registers, the city tax register of 1446 and the quintile analysis. The result of the analysis was not surprising (Figure 9.3). Only the richest peasants borrowed money through a formal credit market. The creditors also came from the ranks of the wealthiest burghers. Among the peasants we find tenants of ‘subject’ farmsteads, in one case the holder of a ‘free’ farmstead.

Figure 9.3Social status of the debtors in the Eger city state, 1435–1456 (loans).

Source: Klosteuerbuch, 1435; 1438; 1441–1456; Losungsbuch, 1446; Schuldprotokolle, 1429–1439; 1439–1452; 1452–1470.

Figure 9.4Nominal amount of the loans of the peasants in the Eger city state, 1435–1456.

Source: Schuldprotokolle, 1429–1439; 1439–1452; 1452–1470.

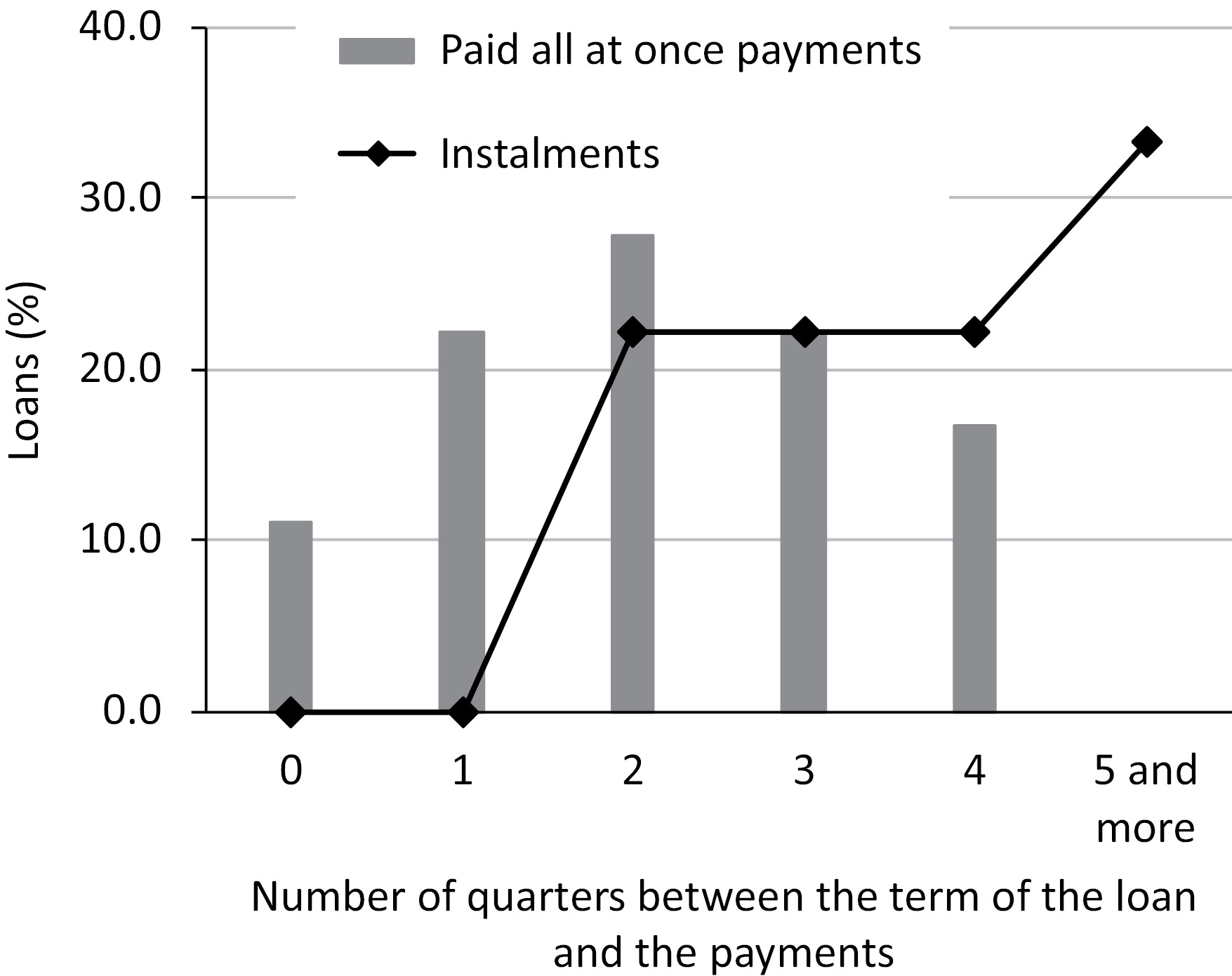

The amount of the loan was not usually enormously high or extremely low (Figure 9.4). The minimal loan was 40 Prague groschen, the maximal 26 threescore Prague groschen. Most often, peasants borrowed amounts from one to three threescore Prague groschen and then from six to ten threescore Prague groschen. The loans to 6 threescore were repaid at once with exceptions; higher amounts were in half of the cases divided into two to four instalments. It follows that the rich peasants did not have a problem to suddenly get the amount of up to 6 threescore but higher amounts were already difficult to put together.

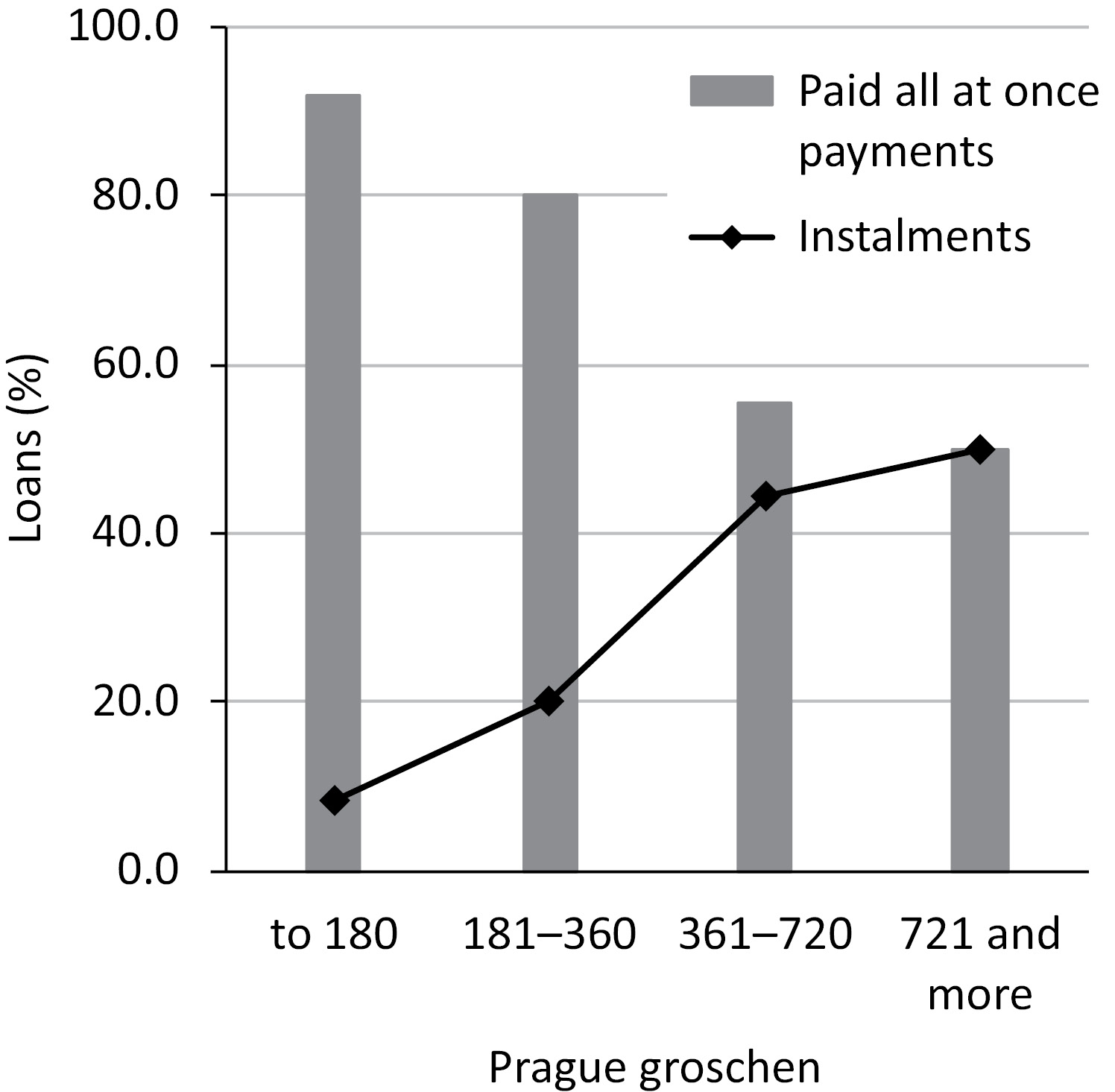

Loans were of a short-term nature. If the debt was repaid at once, the loan never exceeded one year, usually repaid within six months (Figure 9.5). Most of the debts paid in instalments were also paid within one year. The first instalment followed within six months of granting the loan. The longest loan was repaid in four instalments over two years.

Figure 9.5Length of the repayment of peasant loans.

Source: Schuldprotokolle, 1429–1439; 1439–1452; 1452–1470.

One third of the records also stated the pledge that the debtor guaranteed to the creditor (eleven times). The mention of the pledge was more common with nominally higher debts. The peasants secured the loans with non-farmstead plots (five times) or all the property (four times), less already the farmstead (once) or a house in the city (once).

We do not know the precise purpose of any of the loans but we can estimate thanks to the price relation. The most frequent amount of 1–3 threescore Prague groschen corresponds in price of one horse, several cows or one ‘Morgen’ of a non-farmstead field (ca 0.57 ha). Loans falling into the second most frequent interval of 6–12 threescore corresponded to the prices of all of the livestock animals on an average farmstead, two ‘Morgen’ of non-farm meadows or four ‘Morgen’ of fields, or half the amount for which it was possible to acquire the tenure right to a good ‘subject’ farmstead.

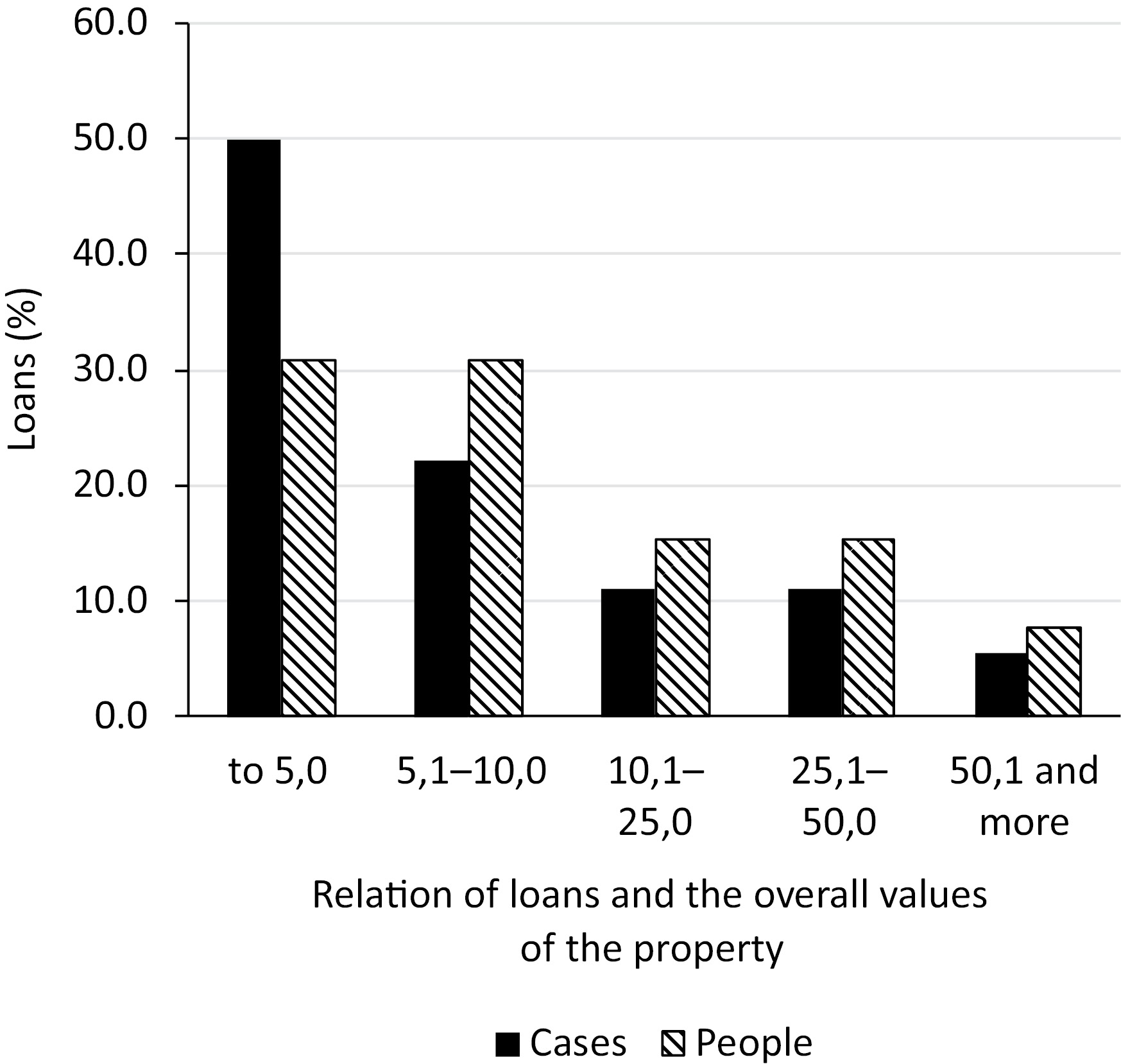

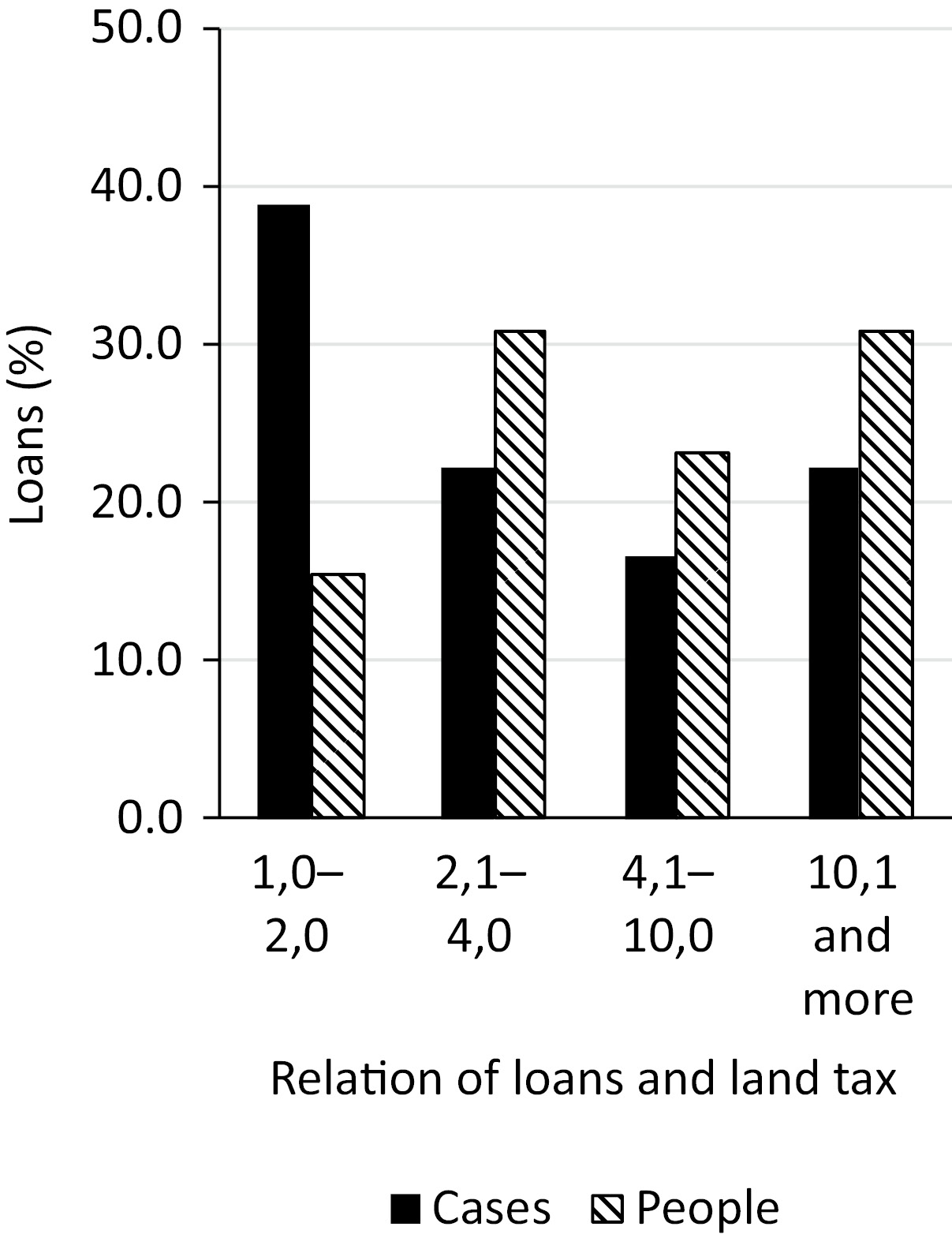

An important testimony is borne by the ratio of the borrowed amount to the total value of the debtor’s assets, respectively its ratio to the land tax (Figures 9.6 and 9.7). In 72% of the cases, the loan was less than a tenth of the total value of the property; more than a quarter of the value of the property in 17% of the cases. In 61% of the cases, the amount of the loan was up to four times the amount of tax paid each year. The loan surpassed ten times the annual land tax amount in 22% of the cases.

Figure 9.6Ratio of the nominal amount of the loan and the total amount of the peasant’s property in the Eger city state, 1435–1456.

Source: Schuldprotokolle, 1429–1439; 1439–1452; 1452–1470.

Figure 9.7Ratio of the nominal amount of the loan and the land tax in the Eger city state, 1435–1456.

Source: Schuldprotokolle, 1429–1439; 1439–1452; 1452–1470.

To sum up, the short repayment period, the relatively low amount of the loaned amounts, its ratio to the annual land tax, and the total value of the property suggest that mainly seasonal bridging loans or investment loans in non-farm plots were entered in the court protocols.

The flow of capital from the countryside to the city is also documented. The court protocols from 1435–1456 contain five records in which peasants lent cash to the Eger burghers. The analysis of their social status showed a fact that was not surprising – the creditors were rich peasants and, on the contrary, the debtors were poor burghers (Figure 9.3). The amount of the loans was in the range of the cash that the peasants could obtain on a one-off basis (two to seven threescore Prague groschen). Peasants in the role of creditors illustrate the close interaction of the rural and urban economy as well as financial entrepreneurship. We assume that the peasant-creditors were among the rural elite, as its basic characteristics were precisely plural economic activities and income diversity (e.g. Čechura 1994, p. 115; Aparisi 2015, pp. 337–9, 352).

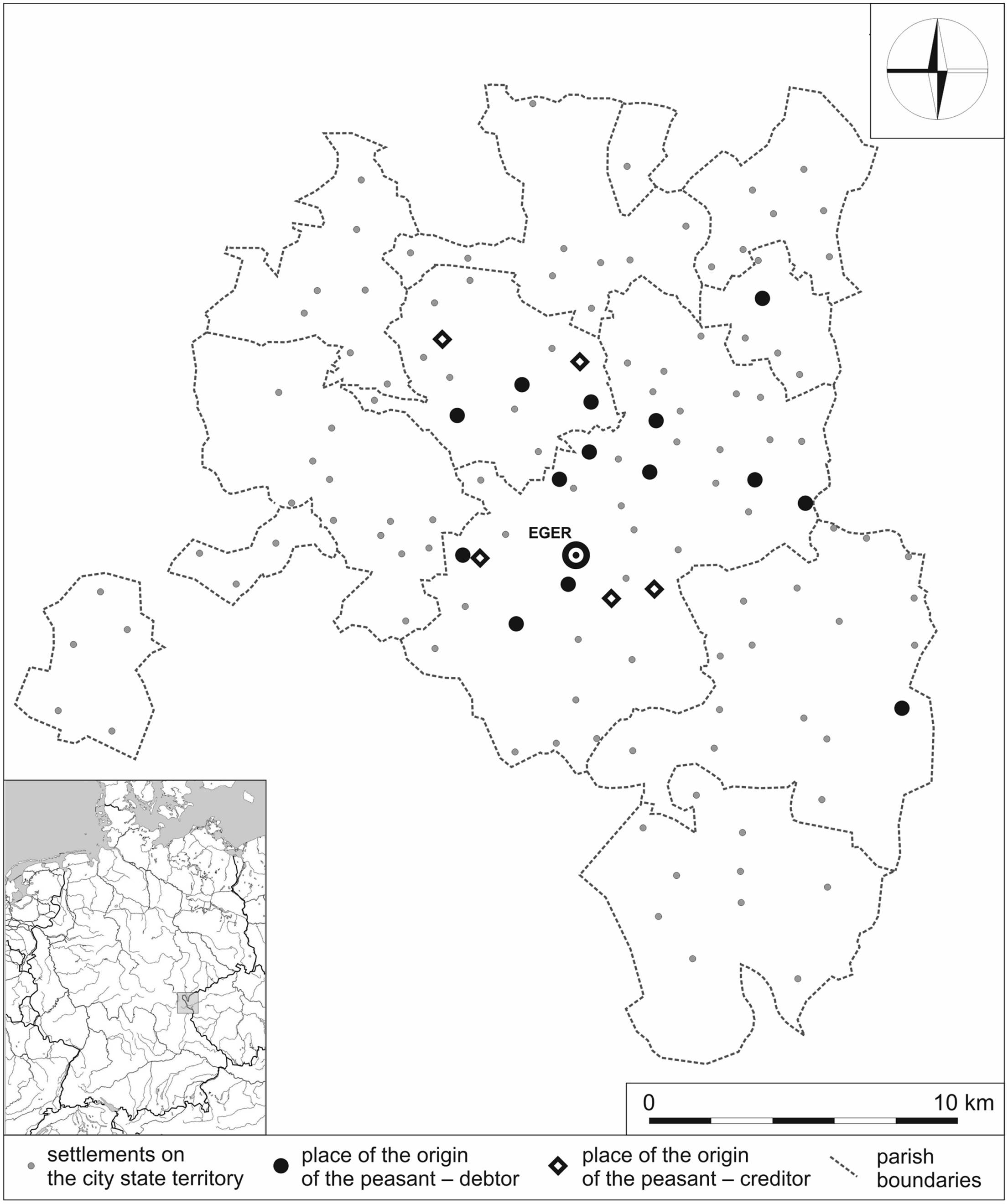

Geographical aspects

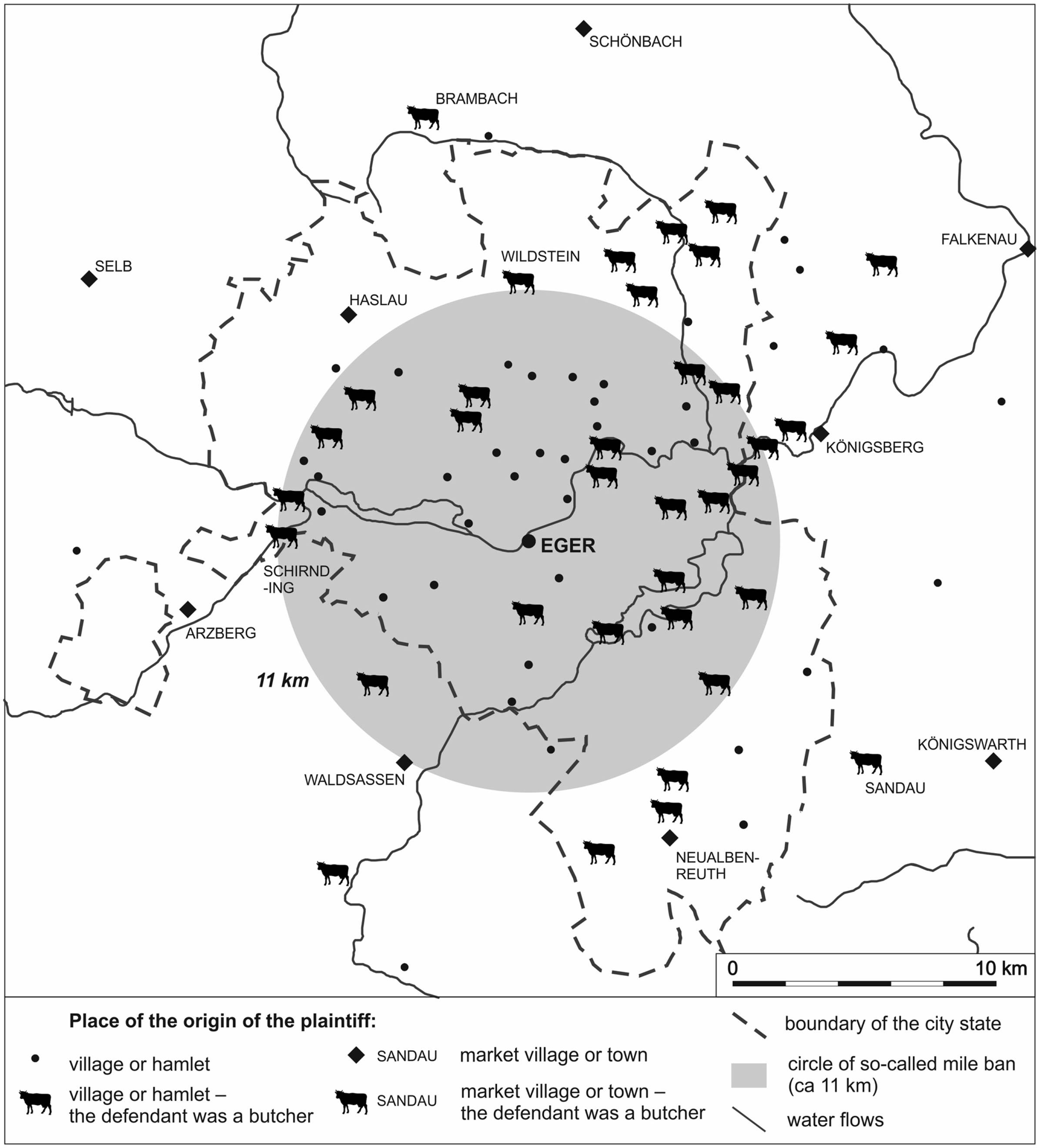

Sales on credit and loans had different spatial reach. In the first case, the credit area was equal to the local market area of the city of Eger, with the perimeter ranging between 12 and 18 km (Figure 9.8). The spatial reach of loans was smaller, reaching 6–8 km from the city of Eger and overlapping with the most fertile and commercialized zone, interwoven with dense information, social and economic networks linking the richest peasants to the city (Figure 9.9).

Figure 9.8The origin of the creditors from outside of the city of Eger who sued Eger burghers (1442–1456). Predominantly sale on credit.

Source: Schuldprotokolle, 1439–1452; 1452–1470.

Figure 9.9The origin of the rural debtors and creditors (1435–1456).

Source: Schuldprotokolle, 1429–1439; 1439–1452; 1452–1470.

Conclusion

The rate of commercialization and monetarization of the late medieval peasantry of Eger (c. 1450) was low compared to the early modern period. As for the external factors that forced the peasants to acquire cash, it was mainly the land tax, namely to a bearable degree. As for the internal factors, the peasant needed cash for the annual reproduction of his farmstead or for the payment of inherited shares. But even this was not burdensome given the price range. We tested the hypothesis that the average peasant household needed cash only to a small extent by analysing the credit market.

The credit market in the Eger city state was institutionally secured by the city court, which provided guarantees not only to the burghers, but also to the peasants in the countryside. The relevant protocols make it possible to identify both formal loans (repaid and failed) and informal sales on credit (failed). The involvement of the peasantry in the loan market appears to be small and limited to the richest peasants. We find peasants mostly in the role of debtors (85% of the cases); their creditors were wealthy burghers. If, on the other hand, the peasant appeared as a creditor (15%), his debtor was a poor burgher. Loans were of a short-term nature, mostly not enormously high. The peasants were far more active in selling agricultural commodities to burghers, especially meat, on credit. This sale credit artificially increased the inflow of economic resources from the countryside to the city because market transactions could have been realized even in the absence of cash.

Funding

This work was supported by the European Regional Development Fund-Project ‘Creativity and Adaptability as Conditions of the Success of Europe in an Interrelated World’ (No. CZ.02.1.01/0.0/0.0/16_019/0000734). Text translated by Sean Mark Miller (Prague). Special thanks to Martin Janovský (Prague).

References

Archival sources

Klosteuerbuch (1435). Fonds 1 (the city of Cheb), book Nr. 1066, State District Archive Cheb.

Klosteuerbuch (1438). Fonds 1, the city of Cheb, book Nr. 1067, State District Archive Cheb (copy from 1769; edition by Klír et al., 2016).

Klosteuerbücher (1442–1456). Fonds 1, the city of Cheb, books Nr. 1069–1083, State District Archive Cheb.

Klosteuerbuch (1469). Fonds 1 (the city of Cheb), book Nr. 1096, State District Archive Cheb.

Klosteuerbuch (Schätzungsbuch) (1456). Fonds 1, the city of Cheb, book Nr. 1084, State District Archive Cheb (edition by Klír et al., 2016).

Losungsbuch (1446). Fonds 1, the city of Cheb, book Nr. 1424, State District Archive Cheb.

Schuldprotokolle (1387–1416). Fonds 1, the city of Cheb, book Nr. 894, State District Archive Cheb.

Schuldprotokolle (1429–1439). Fonds 1, the city of Cheb, book Nr. 896, State District Archive Cheb.

Schuldprotokolle (1439–1452). Fonds 1, the city of Cheb, book Nr. 897, State District Archive Cheb.

Schuldprotokolle (1452–1470). Fonds 1, the city of Cheb, book Nr. 898, State District Archive Cheb.

Literature

Aparisi, F. (2015). Village entrepreneurs: The economic foundations of Valencian rural elites in the fifteenth century. Agricultural History 89, pp. 336–57.

Bauerfeind, W. (1993). Materielle Grundstrukturen im Spätmittelalter und der Frühen Neuzeit. Preisentwicklung und Agrarkonjunktur am Nürnberger Getreidemarkt von 1399 bis 1670. Neustadt a. d. Aisch: Stadtarchiv Nürnberg.

Briggs, Ch. D. & Zuijderduijn, C. J., eds. (2018). Land and Credit: Mortgages in the Medieval and Early Modern European Countryside. Cham, Switzerland: Palgrave Macmillan.

Cerman, M. (2008). Social structure and land markets in Late Mediaeval Central and East-central Europe. Continuity and Change, 23, pp. 55–100.

Cerman, M. & Zeitelhofer, H., eds. (2002). Soziale Strukturen in Böhmen. Ein regionaler Vergleich von Wirtschaft und Gesellschaft in Gutsherrschaften, 16.–19. Jahrhundert. Wien: Verlag für Geschichte und Politik; München: Oldenbourg Wissenschaftsverlag.

Čechura, J. (1990). Die Bauernschaft in Böhmen während des Spätmittelalters: Perspektiven neuer Orientierungen. Bohemia, 31, pp. 283–311.

Čechura, J. (1994). Die Struktur der Grundherrschaften im mittelalterlichen Böhmen unter besonderer Berücksichtigung der Klosterherrschaften. Stuttgart – Jena – New York: Walter de Gruyter GmbH & Co KG.

Chocholáč, B. (1999). Selské peníze: Sonda do finančního hospodaření poddaných na západní Moravě koncem 16. a v 17. století. Brno: Matice moravská.

Chocholáč, B. (2005). Güterpreise, Verschuldung und Ratensystem: Eine Fallstudie zu den finanziellen Transaktionen der Untertanen bei Besitzübertragungen in Westmähren im späten 16. und im 17. Jahrhundert. In Cerman, M. & Luft, R., eds. Untertanen, Herrschaft und Staat in Böhmen und im “Alten Reich”. Sozialgeschichtliche Strukturen. München: Oldenbourg, pp. 89–125.

Guzowski, P. (2014). Village court records and peasant credit in fifteenth- and sixteenth-century Poland. Continuity and Change 29, pp. 115–42.

Hanzal, J. (1963). Poznámky ke studiu ceny poddanské nemovitosti v 16.–17. století. In Příspěvky k dějinám cen nemovitostí v 16.–18. století. Praha: Univerzita Karlova, pp. 39–48.

Klír, T. (2018). Sociálně-ekonomická mobilita rolnictva v pozdním středověku. Chebsko v letech 1438–1456. In Nocuń, P., Fokt, K. & Przybyła-Dumin, A., eds. Wieś miniona, lecz obecna. Ślady dawnych wsi i ich badania. Chorzów: MGPE, pp. 159–231.

Klír, T. (2019). Socioeconomic mobility and property transmission among peasants: The Cheb region (Czech Republic) in the Late Middle Ages. In Brady, N. & Theune, C., eds. Settlement Change across Medieval Europe: Old Paradigms and New Vistas. Leiden: Sidestone, pp. 341–55.

Klír, T. (in print). Rolnictvo na pozdně středověkém Chebsku. Sociální mobilita, migrace a procesy pustnutí. Praha: Karolinum.

Klír, T., et al. (2016). Knihy chebské zemské berně z let 1438 a 1456. Praha: Filozofická fakulta Univerzity Karlovy, Ústí nad Labem: Filozofická fakulta Univerzity Jana Evangelisty Purkyně v Ústí nad Labem, Dolní Břežany: Scriptorium.

Kostlán, A. (1987). “Cenová revoluce” a její odraz v hospodářském vývoji Čech. Folia Historica Bohemica, 11, pp. 161–212.

Míka, A. (1959). Nástin vývoje cen zemědělského zboží v Čechách v letech 1424–1547. Československý časopis historický, 7, pp. 545–71.

Míka, A. (1960). Poddaný lid v Čechách v první polovině 16. století. Praha: Nakladatelství Československé akademie věd.

Procházka, V. (1963). Česká poddanská nemovitost v pozemkových knihách 16. a 17. století. Praha: Nakladatelství Československé akademie věd.

Schirmer, U. (1996). Das Amt Grimma 1485–1548. Demographische, wirtschaftliche und soziale Verhältnisse in einem kursächsischen Amt am Ende des Mittelalters und zu Beginn der Neuzeit. Beucha: Sax-Verlag.

Schofield, P.R. & Lambrecht, T., eds. (2009). Credit and the rural economy in North-western Europe, c. 1200–c. 1850. Turnhout, Belgium: Brepols.

Vaniš, J. (1981). Ceny v Lounech v druhé polovině 15. století. Hospodářské dějiny, 8, pp. 5–93.