Chapter 10

Piotr Łozowski

Introduction

This chapter presents the results of research on the credit market of late medieval Old Warsaw. Since its establishment at the end of the 13th century, the city has experienced a systematic social and economic development: from a centre of about 4,000 inhabitants in the 15th century to one of the largest and most important cities in Central and Eastern Europe with a population of 100,000 (Bogucka & Samsonowicz 1986, p. 119; Kuklo 2009, p. 233). This modern blossoming would have been much slower (or impossible) without the solid medieval root, which was based mainly on trade in wood, grain, fur, and other forest products floated down the Vistula River to Toruń and Gdańsk from where it was transported to London, Bruges, and Amsterdam (Samsonowicz 1972). Therefore, the period of the late Middle Ages seems to be an extremely valuable research topic as it offers the possibility to observe economic indicators during the development of the town. The credit market is one of the most important indicators, best represented in sources. The chapter is divided into two parts: one presents the functioning of Warsaw market on a general scale (value of loans, duration of contracts, interest rates, security methods, moment of conclusion and repayment); the other covers the social background in the form of market activities of craftsmen, merchants, and other social estates. Obtaining such a precise and diverse picture allows for referring not only to the discussion about the economic crisis of the late Middle Ages in Poland (Guzowski 2008), but also about the social and territorial scope of the credit instrument, the horizontality of the market (Schofield 2002), the level of trust between creditor and debtor observed, for instance, through changes in interest rates and the duration of contracts (Nightingale 2007; van Zanden, Zuijderduijn & de Moor 2012), or the well-known ‘de Soto problem’ (de Soto 2000).

The source of the deliberations is formed by six preserved court records from 1427–1527. It should be noted that there is no jury record from 1473–1496 and the fact that the completeness of the council records increased significantly only at the end of the 15th century. Studying Old Warsaw market, we come across a basic problem for almost all credit analyses, that is the possibility of capturing only a fragment of the entire loan movement, due to voluntary agreement registration in city books. Importantly, despite the obvious imperfections of the material, it was possible to separate a group of 1,558 contracts involving 1,647 people with a total value of 1,337,447 groszes,1 which, given the size of the city, constitutes a convenient basis for drawing a conclusion on the economic condition of Old Warsaw. In order to better describe the long-term changes, a period of 100 years was assumed from the beginning of the oldest surviving city book in 1427.

Economic and legal background

The Warsaw credit market registered in court records was based on simple debt obligations concluded between the burghers as a declaration of payment of a specified amount of money to a person on a specified date, with the simultaneous reservation of consequences resulting from non-performance of the agreement. Rent contracts (census) appeared sporadically: in total we registered 182 entries constituting 12% of all transactions and 15% of their total value. The creditor was usually the town jury or council and the agreement itself took the form of a new repurchase rent. There was no turnover in old rents or life annuities. If the obtained picture of low popularity of annuities is true and does not result from disappearance of a separate annuity book (there is no strong evidence of its existence), then the Warsaw credit market should be regarded as less developed than in Prussian towns such as Toruń, Elbląg, Gdańsk (Kardasz 2013), or Western and Southern Europe (Zuijderduij 2009) where annuity was an extremely popular instrument.

The value of loans taken out in Old Warsaw in the late Middle Ages amounted to 920 groszes according to the average and 270 groszes according to much more reliable median indications. In the course of the analysed century, the median contract value increased from 240 groszes in the first half of the 15th century to 300 groszes in the years 1457–1527, thus illustrating the trade in increasingly larger capital. 73% of the contracts did not exceed the amount of 600 groszes, which was a credit for consumption or for supporting small investments in craft workshops, home development, or small trade. The second group of 27% included contracts concluded mainly by the merchants, exceeding 600 groszes and fulfilling a typical investment and trade role. The proportion between groups is reversed if we look at the share in the total market value where consumer contracts (up to 600 groszes) covered only 16% of the turnover, while investment contracts (above 600 groszes) covered as much as 84%. On the one hand, this shows the market based on the number of small credit agreements and, on the other hand, it shows the scale of wealth differences between the lower and middle strata and the elites, as well as the economic importance of the wealthiest groups. The median of the contract in both groups was 210 and 2,580 groszes (3.5 and 43 sexagenae) so the elites participating in the distant trade used the amounts more than twelve times higher.

In order to better capture the real value of the agreements, we will use their relationship to the prices of farming-food products, commercial products, and exemplary bare-bones baskets. The amount of 3.5 sexagenae made it possible to buy, according to the prices in the Warsaw district, registered in the court books from 1427–1453: stack (acervus) of rye and wheat or about 40 bushels of each of these cereals, 4 stones of pepper, 2 barrels of herring, 4 barrels of salt, about 400 pieces of hewn wood, and a horse. Correspondingly, for the sum of 43 sexagenae, one could buy 10 stacks, 10 lasts or more than 500 bushels of rye and wheat, 57 stones of pepper, 32 barrels of herring, 54 barrels of salt, almost 5,200 pieces of hewn wood, and 14 horses. Assuming the prices registered in Cracow in the second half of the 15th century and at the beginning of the 16th century (Pelc 1935), for 3.5 and 43 sexagenae there could be bought, respectively: 11.5 and 143 bushels of oat, 9 and 107 barrels of beer, and 0.5 or 6 barrels of wine, 2.4 and 30 pounds of saffron or 105 or 1,290 elbows of canvas. It is also worthwhile to convert it into the so-called bare-bone baskets. An average family of four needed about three such baskets; the price of a single basket in Cracow and Lvov in the first quarter of the 16th century oscillated between 32–33 grams of silver (Malinowski 2016, pp. 3, 5). The amount of 210 groszes converted into the amount of bullion (1 grosz = 0.78 Au) allowed the purchase of five baskets which not only provided food for the whole family, but also allowed the purchase of more than the minimum quantity of selected goods. This short list shows the enormous scale of trade opportunities offered by the elite but also confirms that, apart from satisfying consumption needs, the representatives of the community (e.g. craftsmen) could occasionally take part in small trade. In the case of investments in the real estate market, the amount of 210 groszes covered only half of the price of an average wooden house in Old Warsaw (480 groszes) so it could be used only to carry out minor renovation and construction works. Similarly, a trade credit was used primarily for trade or investments in wooden houses, as the purchase of a tenement house at the market square should have involved (Łozowski 2020).

Some researchers are convinced that the dynamics of interest rate changes are closely related to the stability and health of the urban economy which ultimately influences the level of credit risk by raising or lowering interest rates. In Old Warsaw, the rent received on borrowed capital ranged from 2.4 to 10% per annum but the most common (61% of records) was one mark per annum on 10 sexagenae groszes, that is 8%. It is worth noting that this interest rate functioned mainly in the second half of the 15th century, while after 1500, it was reduced to 6.66%. Relating this fact to the aforementioned assumption, we can conclude that the Old Town credit market is still developing and the credit risk reduction resulting from the stability of economic life is resulting in a simultaneous increase in trust between the creditor and the debtor.

Data analysis showed that the credit market of civitatis Antiquae Varsoviae was mainly based on short-term contracts. In total, 30% of all records did not exceed three months, over 55% were within the six-month period, and as much as 86% lasted less than a year. Only 14% of contracts were concluded for a period longer than 12 months, of which 7% were within one to two years. The average duration of the transaction was 9.7 months, with slight changes in this value during the analysed century. The loan term systematically increased from an average of seven months in the years 1427–1453, through 10 months between 1454 and 1485, to 11 months at the beginning of the 16th century which can be seen as another proof of market stability and lenders’ lack of fears about the borrower’s insolvency as well as a positive assessment of their future financial standing by debtors. As regards the status of burghers’ budgets and long-term revenue and expenditure forecasting, the correlation between the duration of a contract and its value provides a great deal of valuable information. It turns out that the smallest transactions (2 sexagenae) were concluded for a six-month period with the amount doubling in relation to the six- / twelve-month period (4.3 sexagenae). The liabilities lasting one to two years amounted to 5.3 sexagenae, while the repayment of loans of the highest value was spread over more than 24 (9 sexagenae) and 36 months (as many as 12 sexagenae). Based on the results obtained, we can see that townspeople were able to accumulate a cash surplus of 4 sexagenae per year. The issue of predicting future income and repayment of liabilities is related to the use of the instalment system. In the Warsaw credit turnover, it was present only in 20% of contracts. If repayment was scheduled in instalments, two (61%) or three (25%) parts were most often chosen. The main factor influencing the application of instalment payments was the duration of the agreement. Among liabilities lasting up to two years, the division into two and three parts prevailed, while loans exceeding the limits of 24 or 36 months were divided into four or more instalments.

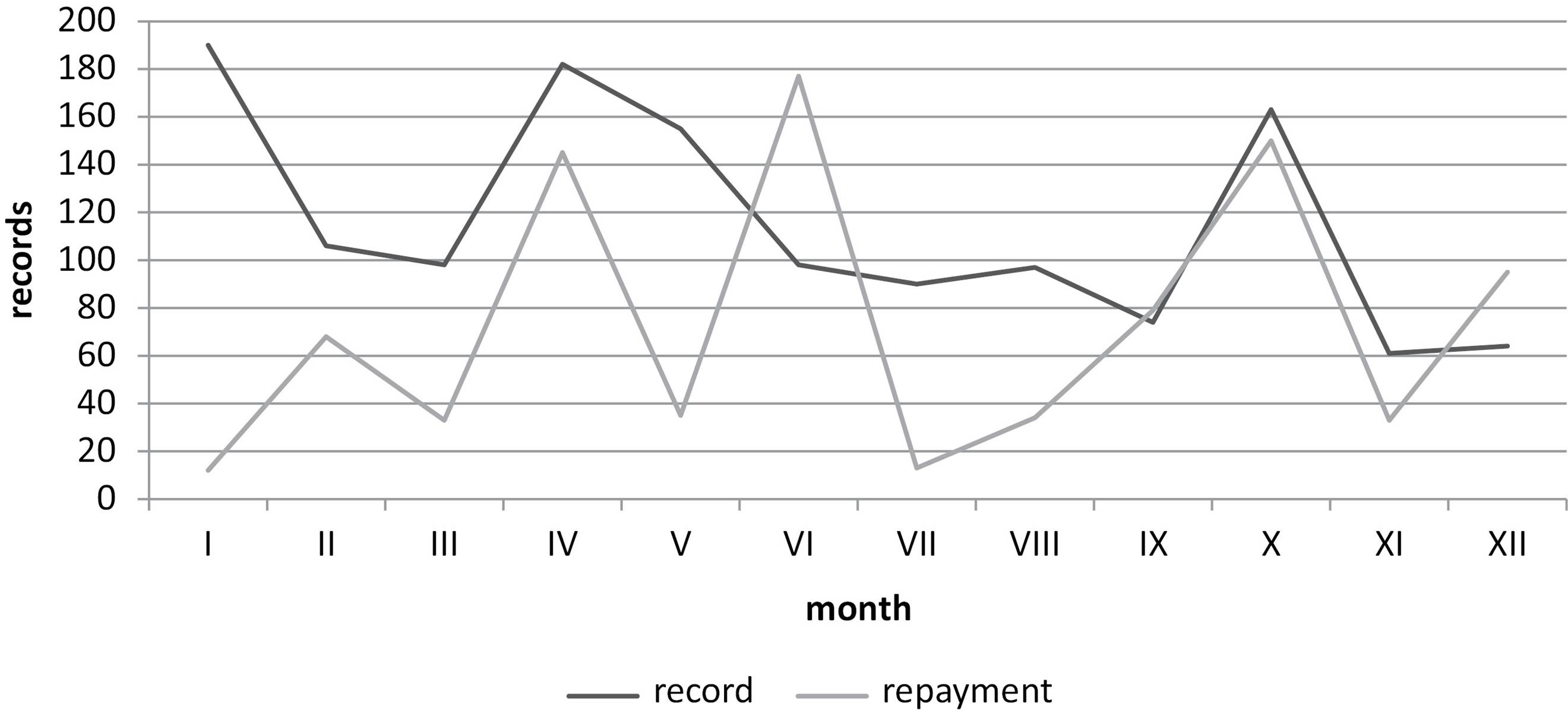

The material stored in the books enables the identification of the day of the beginning of the loan agreement in the case of 95% of entries and the declaration of the repayment date appeared in 60% of the transactions. Using this data, we are able to identify the moments of the highest demand for cash on a yearly basis and the periods of payment of liabilities. Observing the indications presented in Figure 10.1, we can see three distinct moments of credit registration intensification: January (14%), April and May (13 and 11%) and October (12%). It seems that the increased financial needs of townspeople at the beginning of the year should be associated primarily with the need to buy additional food in a difficult winter period. The spring summit could, to a large extent, be associated with the beginning of the trading and sowing season, while the end of the year with the obligation to pay rents and prepare provisions for the coming winter. At the same time, it is also worth noting the reduced interest in loan trading in the summer when, apparently, the townspeople had enough money in the context of their activities. An almost identical rhythm of court records can be observed in other late medieval Polish medium-sized and small towns (Bartoszewicz 2003), which shows that the system of three peaks (hungry gap, spring, and autumn) was characteristic for them. The repayment of the liability was most often made in April (17%), June (20%), and October (17%). The analysis of exact daily dates showed close connection with both the Warsaw fair system and the days of patrons of local churches – extremely popular terms were: St George and St Wojciech (Adalbert, April 23), St John the Baptist (June 24, patron of the Warsaw Collegiate Church), St Hedwig (October 15), and on a slightly smaller scale St Michael (September 29), St Martin (November 21) and Christmas (December 25). Interestingly, the presented regularity did not occur at the moments of notation, which were made throughout the month. The sketched picture of the scheme of taking out and settling credit agreements was maintained without major changes in the 15th and first quarter of the 16th century.

Figure 10.1Number of credit records depending on the month in Old Warsaw in 1427–1527.

Capital investment in the credit market is burdened with the risk of debtor’s insolvency, therefore various ways of securing the borrowed cash were used. One of the most probable was the entry of the contract in the town books; however, this form was repeatedly supplemented with additional clauses. First of all, the level of a debtor’s creditworthiness conditioned the state of his possession and, to some extent, his position in the municipal hierarchy, therefore there was a simple relationship where greater affluence increased the chance of obtaining a higher credit. The majority of the group of proprietors had one property in the form of a house, on which it was possible to secure up to a few loans. If the property status expanded to include other houses, gardens, lands, etc., then the possibilities of using these goods to obtain funds for other investment purposes automatically grew. Therefore, the accumulation of real estate is so characteristic, for example, of a group of merchants. However, we should not forget the ‘de Soto problem’, the role played on the part of borrowers by the institutional framework organizing the system of securing contracts. The lower the risk of a rapid loss of ownership, the greater the interest of potential debtors in a specific form of credit.

In Old Warsaw, the additional security clause concerned 60% of all loans registered in the court records. The catalogue of assurance formulas focused on several categories: real estate (e.g. house, garden, parcel, land, malt house), financial penalties, additional rent collected in case of delayed repayment, third party guarantees, or pledge on movables. The most popular was the security on real estate goods: the house (34%) and all property defined by the term ‘totam bona mobilitas et immobilitas’ (34%). The calculation of additional censum in case of exceeding the loan repayment deadline or contractual penalty (poena) is recorded in 9% of cases. The remaining categories were used occasionally (less than 5%). In total, transactions insured with real estate goods accounted for as much as 78% of all additionally secured contracts. This shows not only the significant role of real estate in the loan trade registered in the books, but also, to a certain extent, the limitation of the market to the group of property owners. However, it is worth remembering that no additional form of insurance is applied to 40% of loans entered in the records, as well as nearly 20% of the percentage of agreements with other security than real estate. This allows us to state that in access to the credit market as debtors, the majority of debtors were owned, however, not owning real estate did not exclude a person interested in raising capital. Moreover, the declaration of assurance on all movable and immovable property was doubly advantageous for the debtor – apart from increasing his creditworthiness, in the event of potential enforcement, it allowed for flexible selection of objects to be auctioned and potential protection of key assets for the less basic ones. This is a direct reference to the ‘de Soto problem’, which, in the light of the results obtained, did not exist in Old Warsaw. This is indicated by the lack of transfer of legal ownership or physical possession of real estate during mortgage pledge (priority formula was used in the queue of creditors during the auction) and by the openness of the market to non-property owners.

Social background

In the course of the analysed century, a total of 1,647 participants in credit turnover appeared in Old Warsaw, with an annual average frequency of 27 persons in the 15th century and 34 in the 16th century. The nature of the participation of most persons was characterized by one-time presence in all credit registers and one-sidedness when they acted only as a creditor or debtor. One-time participation concerned 81% of lenders and 73% of borrowers. On the other hand, unilateral actions were taken by as much as 90% of all registered persons. These figures and analyses of the personalities of the parties to the transaction prove the horizontality of the market which, in turn, is considered a testimony to its positive condition and the wide circulation of capital. In other words, apart from a large group of single debtors, there was an equally large group of single creditors who, having a certain cash surplus, undertook to invest in the market. What is very important in this context is the lack of dependence of many borrowers on a narrow group of those operating with serious capital, for example the wealthiest merchants (in such a case it would be a less favourable vertical structure). Only 9% of all people appeared on both sides of the market. The most active (more than tenfold presence) and proportionally smallest (less than 2% of all creditors and 1% of debtors) part of this group was formed by elites. However, their share was neither even nor equal. We see unevenness in the participation of only a part of the representatives of the wealthiest families, many wealthy merchants appeared in just a few contracts. On the other hand, inequality is expressed in different strategies adopted by the elites, some specialized in the role of creditors, another group mainly collected capital, while others operated on both sides of the market. In both cases, there is no uniform model of elite credit activity, characterized by clear differentiation.

The professional landscape of the medieval city was a real mosaic of various professions and specializations. Guild crafts were undoubtedly the most numerous but the leading position in terms of wealth was occupied by merchants; therefore, it is worth a closer look at the activity of both groups. The craftsmen of Old Warsaw comprised several main branches: construction, wood, metal, leather, food, services, and textiles, while the greatest wealth was achieved by goldsmiths and leather professions, which was also greatly influenced by the water-transported trade to Prussia. In the years 1427–1525 a total of 70 trades were recorded and the number of craftsmen increased five times (Koczorowska 1972). In the period covered by the analysis, 423 craftsmen taking part in the Old Town credit market (26% of the total number of people) were recorded. Artifices appeared in 596 cases with a total value exceeding 340,000 groszes. In total, their activity, against the background of general indicators describing the loan turnover, covered 41% of the number and 25% of the total value of all credit records. The median value of concluded agreements was 3 sexagenae, that is 1.5 sexagenae lower than the general market median. On the other hand, the annual frequency of occurrence was seven cases on average, which was twice as low as the average set for the whole market, with the highest activity occurring at the turn of the 15th and 16th centuries. Craftsmen most often used a loan authenticated in the books once (66% of people), mainly taking capital from the market twice as often as they invested. Investments were undertaken mainly by elites formed by goldsmiths, painters, some furriers, saddlers, and butchers. Nevertheless, the majority of master craftsmen treated the credit market as an incidentally used source of additional cash and not as an investment sphere. A completely different picture emerges from the analysis of merchants’ activity. On the basis of the old town court records, a group of 155 merchants was separated, who constituted only 9% of the persons present on the market but, at the same time, were parties to almost half of all contracts (46%). The total value of transactions exceeded 842,000 groszes, that is over 60% of the total turnover recorded in the books. The wealth of this professional group is evidenced by the average (21 sexagenae) and median (6.5) exceeding by 2 sexagenae the median value of the obligation established in relation to the whole market. However, the frequency of occurrence of 6.6 cases per year was twice lower than the general city average. Merchants used the market for investment purposes as well as to obtain a loan, however, the tendency to invest capital was predominant. The custom of generating additional income from loan operations occupied a stable place in the investment strategy of Warsaw merchants for nearly eight decades which, at the same time, seems to be a positive sign of the stability and liquidity of the Old Town credit market.

The town of the Middle Ages and modern era did not make a closed environment limited only to the group of its inhabitants but concentrated economic activities of many social groups. Beside the burghers themselves, representatives of the nobility, clergy and peasants as well as the Jewish religious community participated in the life of almost every centre. The population growth of the city could not be achieved without migration and long-distance trade would not exist without a wide network of external relations to attract suppliers and business partners. After analysing the activity of particular groups, we will look at the territorial coverage of the Warsaw market.

According to the data presented in Table 10.1, the loan turnover was characterized by estate homogeneity expressed as a definite domination of burghers: 81% among lenders and as many as 96% among borrowers. Representatives of other estates acted mainly as creditors, although the scale of their activity was definitely marginal. Most often the burghers entered into credit relations with the nobility (10%) and clergy (6%), while peasants (2.7%) and Jews (1.2%) had a much smaller share. A characteristic feature of these unions was the one-time presence of the majority of creditors. The main source of cash and simultaneously the area of its investment was town market which sufficiently satisfied the capital needs of the inhabitants of Old Warsaw.

Table 10.1 Social structure of creditors and debtors in Old Warsaw in 1427–1527

|

Social group |

Creditors |

Debtors |

||

|

Number of people |

% |

Number of people |

% |

|

|

Burghers |

476 |

80.7 |

633 |

95.6 |

|

Nobility |

58 |

9.8 |

10 |

1.5 |

|

Clergy |

33 |

5.6 |

4 |

0.6 |

|

Peasants |

16 |

2.7 |

5 |

0.8 |

|

Jews |

7 |

1.2 |

10 |

1.5 |

|

Total |

590 |

100 |

662 |

100 |

Considering not only the nobility, clergy, peasants, and Jews, but also townsmen from other centres, we can clearly see that the majority of external transactions covered villages and towns within a radius of about 30 km from Warsaw. There was also a close correlation between the increase in the transaction value and the distance from the city: if contractors came from the Kingdom of Poland, Lithuania, Prussia or Silesia, the median ranged from 22 to 50 sexagenae groszes and included the Warsaw elite, while the most numerous people in the immediate vicinity of the city concluded contracts for a median of 3 sexagenae, focusing on the middle and poorer strata. Moreover, we observe the phenomenon of one-time activity concerning as much as 90% of all persons coming from outside Warsaw and their role as creditors (75% of transactions). These facts seem to clearly indicate the lack of stability of credit ties, which were established sporadically, on the margins of conducted business and trade in goods. It also proves that there is a clear changeability in the composition of the retail network connecting Old Warsaw with other areas, which, especially in the context of the immediate vicinity of the city, indicates that the market is open to access by other people, while at the same time there is no long-term domination of one narrow group. Nevertheless, a more important conclusion is the statement that the intra-city credit market was characterized by estate and territorial homogeneity, expressed in the acquisition and investment of cash in the internal turnover created by private Christian burghers with a marginal, unstable network characterized by a short territorial range of the external relations.

Conclusion

From the preserved urban sources of late medieval Old Warsaw emerges a picture of the credit market serving both the lower and middle classes, as well as the elites. Low-value agreements serving consumption purposes or small investments in small trade, workshops or house extensions dominated in terms of numbers. However, over 80% of total market turnover was made up of loans concluded by merchants with a value twelve times higher than the median of the consumer contract which directly illustrates the significant level of property differences between the middle classes and elites. The burghers were most often interested in an instrument with a short (of a few months) deadline but there was also a close correlation between a higher value of the contract and a longer loan duration. The demand for cash increased in the hungry gap period, spring and autumn, while the system of repayments was linked to the cycle of annual fairs which were the culminating points of the burghers’ economic activity. Analyses of the additional security clauses of the agreement proved that there was no limitation of the market institutional framework resulting from the de Soto problem. Even as a result of repayment problems, the debtors were not threatened with a rapid loss of key assets and creditors had a flexible catalogue of recoveries at their disposal which encouraged both parties to participate in the market. Another optimistic signal is the fall in interest rates at the end of the 15th century.

The most important proof of the positive condition of the Warsaw economy is horizontality of the loan turnover. The credit instrument functioned in a broad social range, both among creditors and debtors. There was no dependence of broad groups of borrowers on a small group of wealthy elite members, investments were undertaken by numerous representatives of middle and poorer strata. There is also a visible pattern of credit relations based on a similar property group, that is the middle classes provided cash to their own group, just as the elites usually traded capital within their circle. This did not rule out a vertical flow of money. The homogeneity of capital turnover is also visible in the scale of the city’s relations with other regions; external transactions did not constitute a significant percentage of the market (18% of the total number of entries) and, in their largest part, served primarily to contact the immediate surroundings of Warsaw, while, at the same time, the elites cooperated with merchants from hundreds of kilometres away. The most important were: Toruń, Gdańsk, Wrocław, Nuremberg, Wilno, Grodno, and Lwów. Thus, despite its average size for Central and Eastern Europe, Old Warsaw has become an important link in the trade chain connecting this part of Europe with the West. The boom (not the crisis) in the late Middle Ages created a convenient foundation for an even more dynamic development that came with the advent of premodern times.

Note

1In Old Warsaw, they calculated in the system of accounting groszes and sexagena of groszes, (sexagena = 60 groszes). The basic coin was a crown half-grosz of Władysław Jagiełło, 120 of which = sexagena.

References

Archival sources

Archiwum Główne Akt Dawnych w Warszawie /The Central Archives of Historical Records in Warsaw

AGAD, Stara Warszawa, 527, 528, 529, 530.

Literature

Bartoszewicz, A. (2003). Czas w małych miastach. Studium z dziejów kultury umysłowej późnośredniowiecznej Polski. Warszawa: Aspra-JR.

Bogucka, M. & Samsonowicz, H. (1986). Dzieje miast i mieszczaństwa w Polsce przedrozbiorowej. Wrocław: Ossolineum.

Ehrenkreutz, S., ed. (1916). Księgi ławnicze miasta Starej Warszawy z XV w., vol. 1: Księga nr 525 z lat 1427–1453. Warszawa: Warszawskie Archiwum Główne.

Guzowski, P. (2008). Kryzys gospodarczy późnego średniowiecza czy kryzys historiografii?. Roczniki Dziejów Społecznych i Gospodarczych, 68, pp. 173–93.

Kardasz, C. (2013). Rynek kredytu pieniężnego w miastach południowego pobrzeża Bałtyku w późnym średniowieczu (Greifswald, Gdańsk, Elbląg, Toruń, Rewel). Toruń: Towarzystwo Naukowe.

Koczorowska-Pielińska, E. (1972). Liczebność i specjalizacja rzemiosła w Starej i Nowej Warszawie w latach 1417–1526. Rocznik Warszawski, 11, pp. 5–22.

Kuklo, C. (2009). Demografia Rzeczypospolitej przedrozbiorowej. Warszawa: DiG.

Łozowski, P. (2020). Kredyt i dom. Rynki obrotu pieniężnego i nieruchomościami w Warszawie okresu XV i początków XVI wieku. Białystok: PTH.

Malinowski, M. (2016). Little Divergence revisited: Polish weighted real wages in a European perspective, 1500–1800. European Review of Economic History, 20(3), pp. 345–67.

Nightingale, P. (2007). Money and credit in economy of late medieval England. In Nightingale, P. Trade, Money and Power in Medieval England. Aldershot: Ashgate Publishing, pp. 51–71.

Pelc, J. (1935). Ceny w Krakowie 1369–1600. Lwów: IPPTN.

Samsonowicz, H. (1972). Warszawa w handlu średniowiecznym. In Gieysztor, A., ed. Warszawa średniowieczna, 2. Warszawa: PWN, pp. 9–31.

Schofield, P. (2002). Access to credit in the early fourteenth-century English countryside. In Schofield, P. R. & Mayhew, N. J., ed. Credit and Debt in Medieval England c. 1180–1350. Oxford: Oxbow, pp. 106–26.

de Soto, H. (2000). The Mystery of Capital. Why Capitalism Triumphs in the West and Fails Everywhere Else. London: Basic Books.

van Zanden, J., Zuijderduijn, J. & de Moor, T. (2012). Small is beautiful: the efficiency of credit markets in the late medieval Holland. European Review of Economic History, 16(1), pp. 3–22.

Wolff, A., ed. (1963). Księga radziecka miasta Starej Warszawy (1447–1527). Wrocław: Ossolineum.

Zuijderduij, J. (2009). Medieval Capital Markets. Markets for Renten, State Formation and Private Investment in Holland (1300–1550). Boston: Brill.